sanfel

EVgo (NASDAQ:EVGO) is one of the best-positioned EV charging infrastructure operators to benefit from the electrification wave in the U.S. With a comprehensive portfolio of charging offerings - spanning an owned and operated DC fast charging ("DCFC") networking, an operated-only eXtend network, a fleet-facilitating network, and supporting software and technology - EVgo's infrastructure effectively addresses the needs of every critical vertical of the EV ecosystem.

While the multi-faceted strategy allows the company to partake in a larger EV charging TAM, it also comes at a higher price. Building out its owned and operating network is a highly capital-intensive endeavour, while demand risks remain elevated in the near term given the U.S. is still in the early stages of EV adoption. Between now and when EVs become the predominant choice for consumers, EVgo's business model also faces incremental costs of adapting to rapidly evolving preferences in the industry - such as the recent opening of Tesla's (TSLA) Supercharger network to non-Tesla vehicles, which would require EVgo to retrofit its stalls to comply with the North American Charging Standard ("NACS"). Despite improving utilization rates and accelerating revenue growth, the capital-intensive and speculative nature of EVgo's business has been a major overhang on the stock under today's uncertain macroeconomic outlook.

In addition to capital raising, strategic arrangements with auto OEMs and retail partners, as well as government subsidies remain critical non-dilutive sources to funding EVgo's success. The company itself has also adopted a strategic roadmap for evaluating development projects to ensure optimized returns. These "internal hurdles for investments", which management has often alluded to for green-lighting its installations, include a returns threshold in the low-double digit range, estimated at 10% to 15%.

We work collaboratively with OEM, utilities, suppliers, housing contractors to construct and operate charging and construction. Definitely, EVgo is a financially disciplined operator. We will only build sites when they are projected to meet our double-digit return requirements.

Looking ahead, we expect the materialization of National Electric Vehicle Infrastructure ("NEVI") funding under the Bipartisan Infrastructure Law to be a tailwind for EVgo's ROI formula. The company's recent receipt of its first shipment of "Build America, Buy America" ("BABA") compliant charging equipment paves the way for the earlier-than-expected realization of millions of dollars in NEVI funding both directly and indirectly awarded to EVgo since the program was announced. The latest development is likely to bolster its liquidity position, while also serving as an accelerant to EVgo's investment returns. Paired with broader electrification tailwinds in the industry, EVgo's stock is likely to emerge from its current slump soon.

An Overview of EVgo's Funding Sources

With an understanding that it is running a capital-intensive business in a highly nascent industry, EVgo has been prudent in staying disciplined and conservative in its build-out strategy. In addition to a strategic focus on the build-out of a DCFC-only network in "high traffic, high density" areas to better address increasing public charging needs, the company also follows a set of strict internal return hurdles. The disciplined and selective approach to evaluating prospective projects includes "low-double digit hurdle rate" estimated in the 10% to 15% range. In order to meet said criteria, the company is selective on its network location and depends heavily on external funding sources through both strategic partnerships and government incentives to shoulder the investment costs.

Said strategic arrangements are underpinned by auto OEM and retail partners. One of EVgo's most notable OEM partners in its core owned-and-operated charging network business is GM (GM). As part of the EVgo-GM partnership, both companies will build 3,250 DCFC chargers across the U.S. by March 31, 2026. GM co-pays approximately $33,000 - or 25% - of the per-stall capital build cost, and EVgo will own and operate the related facilities. EVgo has built 1,000 DCFC stalls, covering 27 states in the U.S., under the arrangement to date.

EVgo also bolsters its share of the EV charging TAM through its eXtend program, which is a "white label offering". Under the eXtend program, EVgo will take on the planning, installation, and post-deployment operations of the charging stall for a fee. Meanwhile, site hosts / eXtend partners take on the full ownership of the infrastructure and resulting revenues. Its most notable eXtend partnership is with GM and the Pilot Company, whereby EVgo has been commissioned to build out a network of 2,000 DCFC stalls across the U.S. under the "Pilot Flying J" and "Ultium Charge 360" brand. These DCFC stalls will be installed across "500 Pilot and Flying J travel centers", which are typically located in alternative fuel corridors, such as highways and underserved rural areas. This highlights the benefit of the eXtend program in expanding EVgo's reach into charging revenue opportunities beyond its owned-and-operated business' focus on high-traffic, high-density locations, without requiring significant capital outlays under the capital-light strategy.

In addition to its strategic operating model, EVgo also relies on government incentives to fund the build-out of its network. These include tax credits under the Inflation Reduction Act, NEVI subsidies under the Bipartisan Infrastructure Law, local state funding (e.g. CALeVIP; Charge Ready NY 2.0), and the sale of regulatory credits.

Taken together with $257 million in cash on the balance sheet, and a remaining at-the-market facility of $183.5 million at the end of 2Q23, the company expects to have sufficient liquidity to fund investments "well into 2025".

Implications of NEVI Funding

As discussed in a previous coverage, the Biden administration has allocated $7.5 billion out of the Bipartisan Infrastructure Bill towards building out the U.S. EV charging network. Out of the $7.5 billion, $5 billion is allocated through the NEVI program, which is facilitated by the U.S. Department of Transportation's ("DOT") Federal Highway Administration ("FHWA").

Under the NEVI program, $1 billion is handed out per year through 2026, with the funding specifically deployed towards the build-out of EV charging stations. The initial allotment of funding will prioritize the build-out of EV charging availability across alternative fuel corridors such as the interstate highway, then flow through to public high-density locations. And EVgo is well-positioned to capitalize on both focus areas of the NEVI program.

On one hand, the company has access to millions of dollars of initial NEVI program funding that prioritizes build-outs across alternative fuel corridors through its eXtend partnerships. Specifically, EVgo has already secured $13.8 million in preliminary NEVI funding from the Ohio DOT. EVgo was made eligible for the funding through its eXtend partnerships for the deployment of 20 DCFC stalls, with 14 of which related to its arrangement with Pilot Company. Pilot Company has also been independently awarded about $1.7 million in NEVI funding from the Pennsylvania DOT, which EVgo could potentially benefit indirectly from through their eXtend partnership. Meanwhile, on the other hand, EVgo has also independently secured subsidies for one (Strasburg) of 36 sites that the Colorado Energy Office aims to deploy $17 million in initial-round NEVI funding towards in 2023.

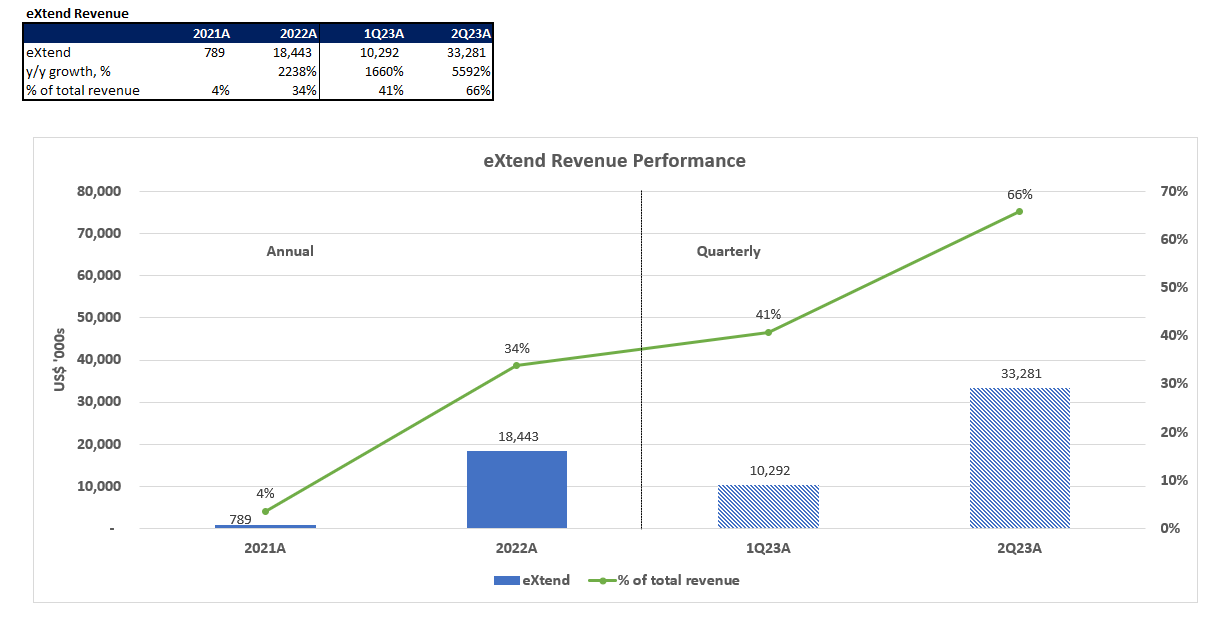

The realization of NEVI program funding is expected to bolster EVgo's eXtend program, which has been a key area of growth since its launch in late 2021. Given eXtend's capital-light business model relative to EVgo's core owned-and-operated charging network business, the white label product's sales are higher-margin in nature. The product is already cash flow positive, which is accretive to EVgo's valuation prospects. eXtend's strength is further corroborated by robust acceleration in recent quarters, with the revenue stream now representing more than half of total company sales during the second quarter.

Data from investors.evgo.com

While management expects a step down in eXtend growth heading into the second half in 2023, as the predominant source of related revenue shifts from hardware sales to construction-related sales, we think results will turn out better than expected. Specifically, management had expected minimal hardware sales entering the second half as EVgo "awaits the availability of BABA-compliant chargers", which will unlock the flow-through of NEVI funding received by its eXtend partners into revenue. The sale of BABA-compliant equipment was not expected to materialize until 2024 given the anticipated timeline of supplier build-out of relevant inventories.

However, in the latest development, EVgo has received its initial shipment of 10 BABA-compliant 350 kW chargers earlier this month from its primary supplier Delta Electronics' manufacturing facility in Plano, Texas. This is expected to expedite the timing of relevant equipment testing and eventual deployment. We believe this is a positive development, as it accelerates EVgo's timeline to restoring eXtend acceleration and realization of NEVI funding-driven revenues by months. It also reinforces the achievability of guided revenues between $120 million and $150 million for full year 2023, with expectations for earlier-than-expected deployment of BABA-compliant equipment opening the door for potential outperformance. Given the high-margin nature of the eXtend revenue stream, fast-tracked realization of NEVI-driven growth is likely to bolster EVgo's profitability profile. We consider this a value accretive factor to the stock, as it helps alleviate some of the capital cost burden, especially under the currently uncertain macroeconomic outlook and elevated rate environment.

Fundamental Considerations

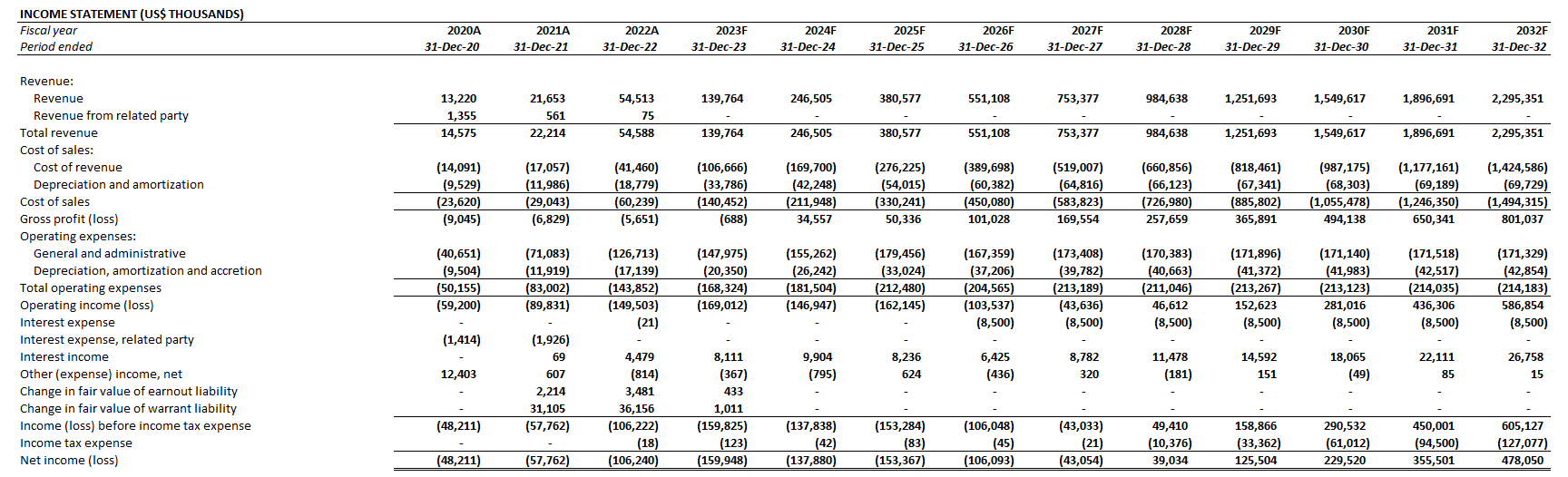

Taken together with improving utilization rates across EVgo's core charging business revenues, increased availability of its DCFC network, improving EV battery technology, and broader secular tailwinds tied to EV adoption, our base case forecast estimates revenue to expand at a 32% 10-year CAGR. In addition to EVgo's accelerating pace of revenue growth, which has recently bolstered by eXtend and government incentive programs, our growth assumption also considers the anticipated need for public charging infrastructure in the U.S. electrification roadmap.

Author

Specifically, U.S. EV sales have stayed resilient under the shaky consumer spending backdrop, with their share of total passenger vehicle sales exceeding 7% in 1H23. This is a tailwind to utilization at EVgo, especially in California where EV sales have been the most robust - utilization rates in California EVgo stalls are as high as 50%, versus the EVgo network average of above 10% and peers' average (ex-Tesla) in the "mid-to-high single digits".

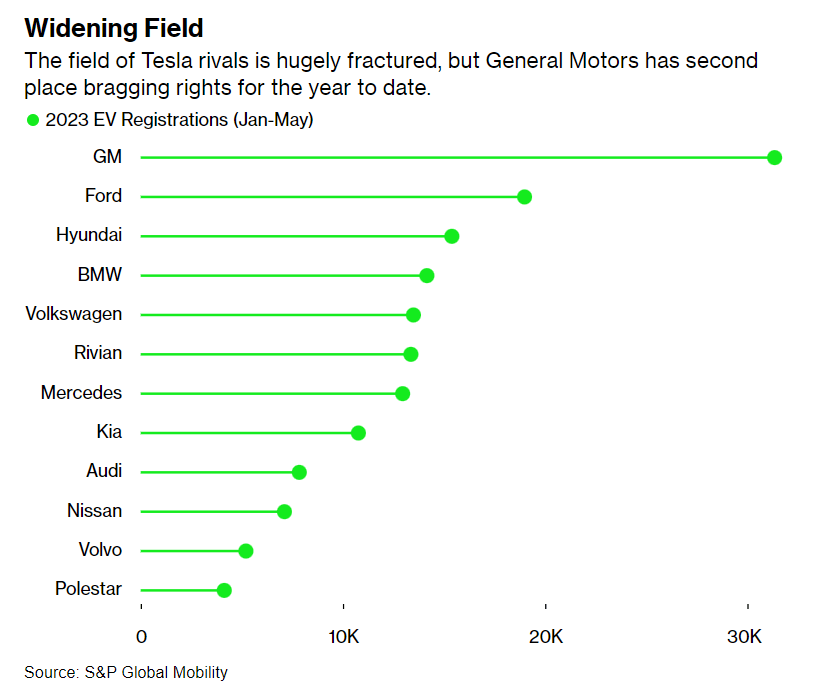

While Tesla continues to dominate the U.S. EV fleet, which inadvertently gives the Supercharger network a significant lead over EVgo, consumers' increasing embrace for electric alternatives and the expanding variety of electrified models are starting to level out Tesla's market share leadership. Specifically, GM currently holds second place in U.S. EV sales, which is a strong tailwind to EVgo given its strategic partnership with the automaker.

Bloomberg News

Outside of Tesla, there are currently close to 50 EV models for Americans to choose from, spanning a wide variety of vehicle and pricing segments, and range capabilities. This will remain a mainstay driver to EVgo's utilization rates and, inadvertently, growth and profitability profile in the long run. Although EVgo was one of the few non-Tesla networks that has been capable of charging the Tesla fleet since launch, relevant volumes have consistently accounted for less than 10% of its utilization. This highlights EVgo's reliance on broader EV adoption, as well as emerging tailwinds as the leading mix of Tesla vehicles becomes increasingly displaced by both legacy incumbents and new industry entrants over the longer term.

However, near-term challenges remain, including the increasing adoption of Tesla's NACS plug as the industry standard, which will lead to incremental capital costs for EVgo. There is also intensifying competition stemming from both auto OEMs and charging infrastructure rivals, which could weigh on EVgo's pricing power and, inadvertently, profitability. Specifically, rivals such as ChargePoint (CHPT), which primarily runs an asset-light strategy without full ownership of its network, could pressure the expansion of EVgo's eXtend program. Meanwhile, OEM-operated charging infrastructure, such as Tesla's Supercharger network, could cannibalize EVgo's relatively nominal market share further, while also pressuring EVgo's pricing power given different financial incentives of their businesses - while EVgo seeks to profit from its charging infrastructure network, Tesla's motive may be to incentivize vehicle purchases through its complementary network. This effectively raises the risks of a delayed profitability trajectory for EVgo, underscoring the potential for further fundraising needs when existing liquidity sources are exhausted around mid-decade.

On the profitability front, we expect increasing operating leverage as a direct result of improving charger utilization rates. This is in line with some of EVgo's investments, such as eXtend and some of its higher utilization charging stalls, having gradually turned cash flow positive in recent quarters, as U.S. EV adoption passes a critical inflection point. The margin expansion trend is expected to improve further as EVgo utilization rates continue to benefit from rising U.S. EV penetration rates, improving from 0.5% exiting 2021 to now surpassing 7% during the second quarter. This is consistent with management's identification of 5%, 10%, and 15% as critical EV adoption milestones for driving broader company profitability.

Author

EVgo_-_Forecasted_Financial_Information.pdf

Valuation Considerations

Author

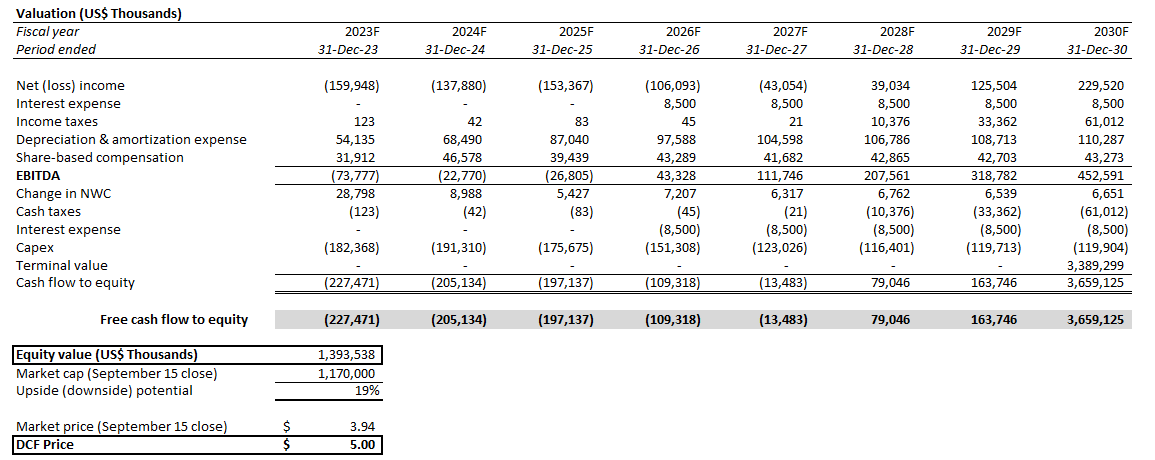

Our $5 base case price target is the result of equally weighing outcomes from the discounted cash flow and multiple-based valuation approach, which, in our opinion, adequately captures both short- and longer-term prospects for EVgo's stock.

Author

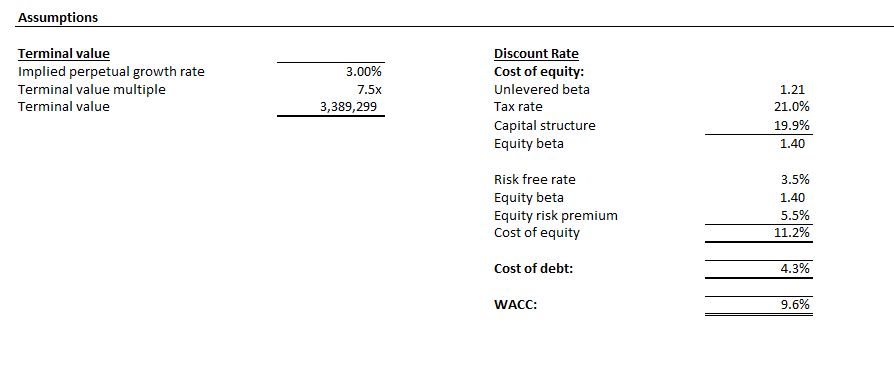

Under the DCF approach, we have considered projected cash flows out to 2030 in conjunction with our fundamental analysis. A WACC of 10%, reflective of EVgo's capital structure and risk profile, and estimated perpetual growth rate of 3%, in line with the company's prospects, is applied. The DCF computation yields an estimated intrinsic value of $1.4 billion for the company, or $5 apiece, representing upside potential of about 33% from current levels.

Author

Author

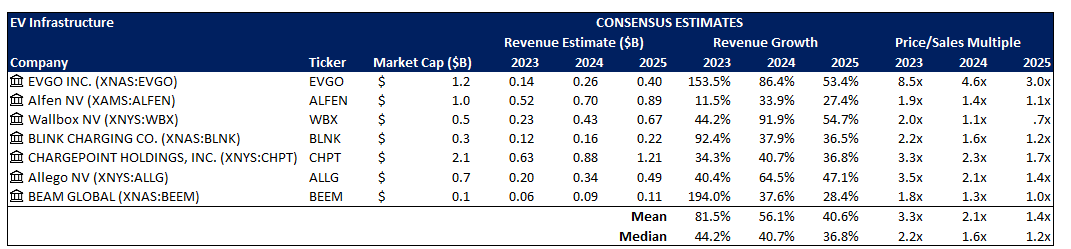

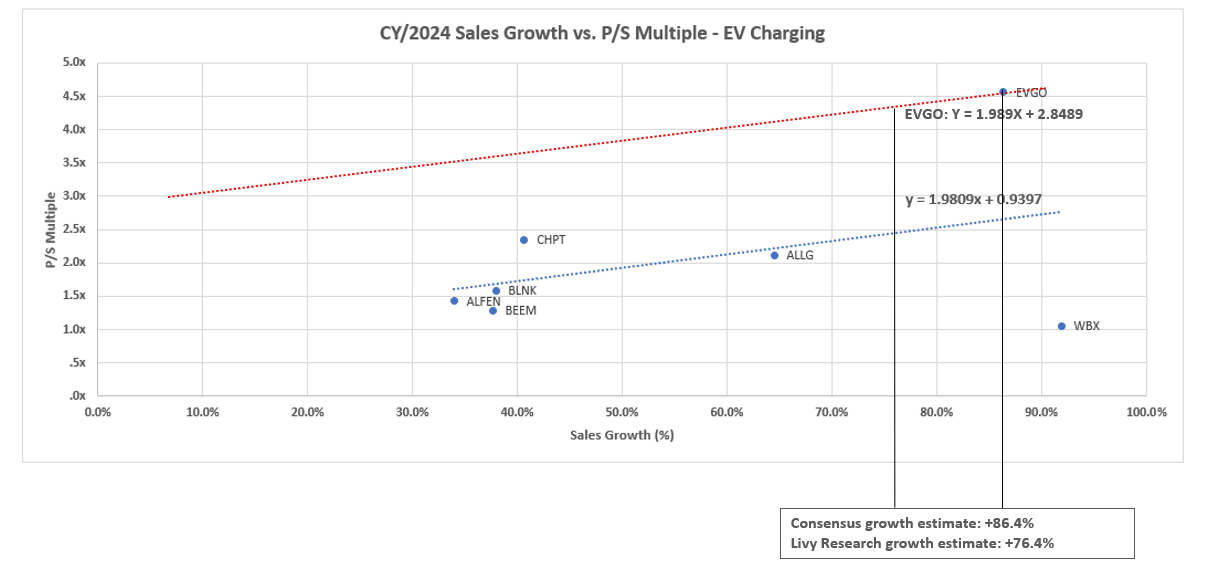

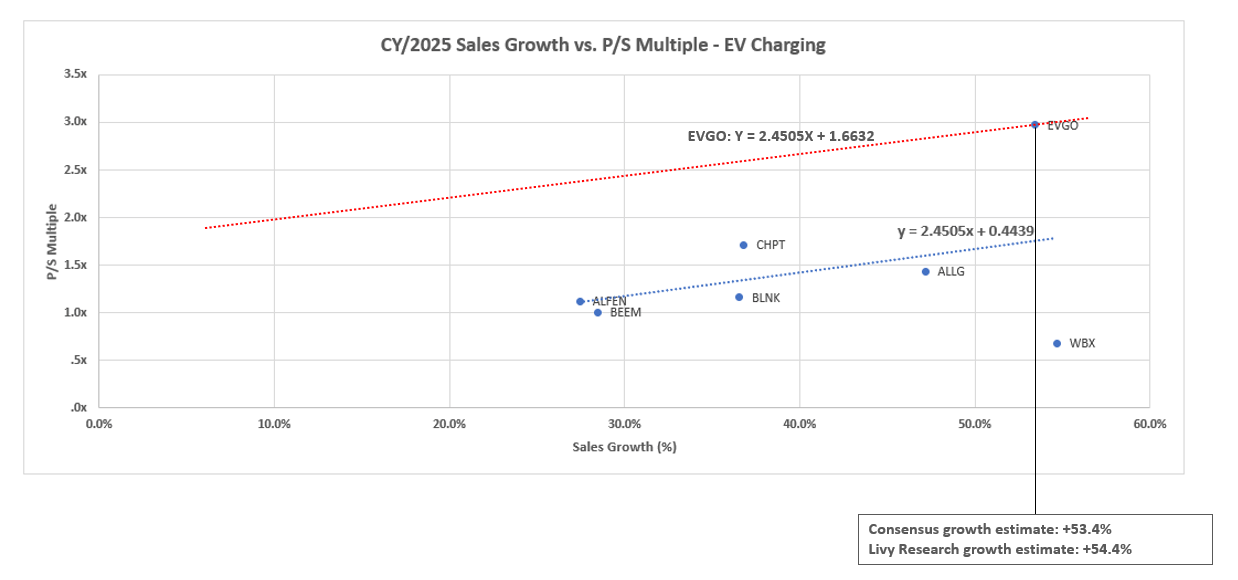

Meanwhile, under the multiple-based valuation approach, we have considered the growth prospects and stock performance of EVgo's peers in the EV Infrastructure sector.

Data from Seeking Alpha

Data from Seeking Alpha

Data from Seeking Alpha

Data from Seeking Alpha

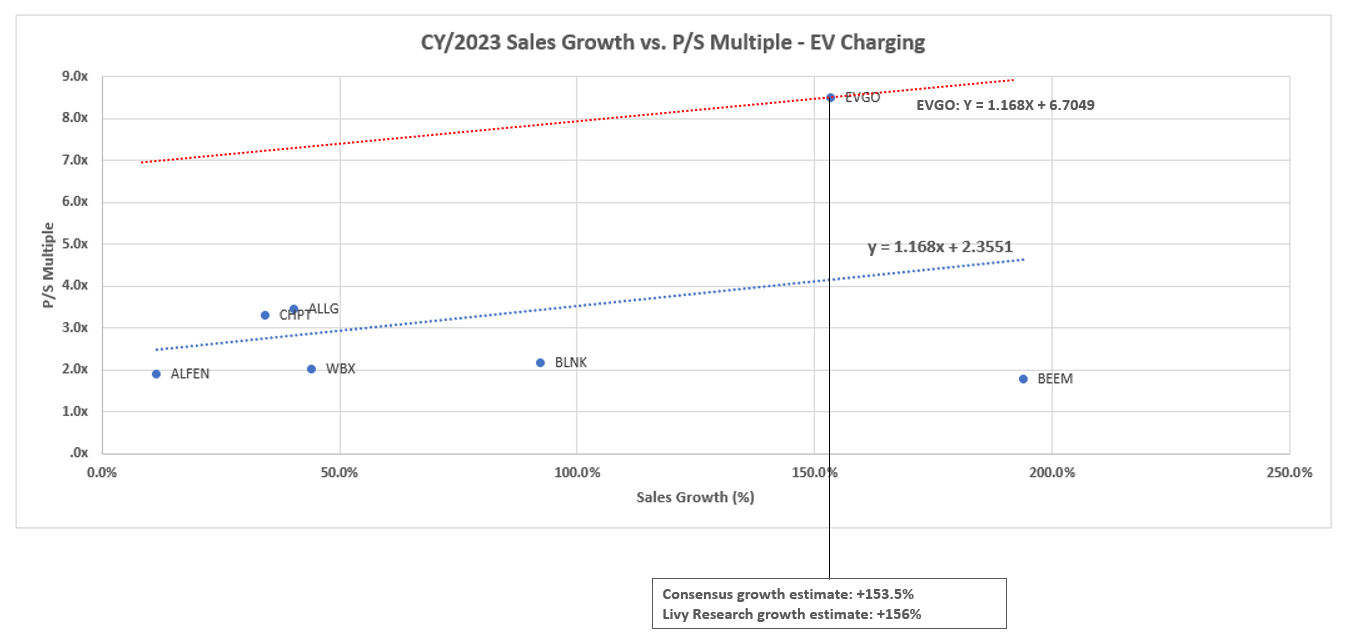

Considering EVgo's valuation curve (dotted red line) relative to the sector's performance (dotted blue line), and applying the relevant multiples across our base case growth estimates for the company, the computation yields a valuation of about $4 apiece. We believe EVgo's current valuation premium to the sector average is reflective of its above-average growth, buoyed by a combination of improving utilization rates in the owned-and-operated charging network business, as well as accelerating sales in the emerging eXtend revenue stream, with ecosystem stickiness complemented by ancillary services such as PlugShare.

Author

However, the high capital intensity of EVgo's business, broader weakness in consumer spending trends, as well as tightening financial conditions remain overhanging risks to sector multiples, which could drive volatility to the stock's near-term performance in our opinion. As such, we believe the combined consideration of outcomes from both the DCF and multiple-based approach adequately captures consideration of both the near-term risks to the stock's valuation performance, as well as longer-term opportunities as utilization of EVgo's network continues to scale.

Final Thoughts

The combination of improving utilization rates and resilient EV adoption in the U.S. market remain intact long-term tailwinds to EVgo, despite ongoing macroeconomic uncertainties. We believe the realization of NEVI-driven growth and relevant funding is a near-term catalyst for the stock, as it bolsters eXtend and charging revenue growth, while also complementing EVgo's ROI formula, both of which are value accretive factors in our opinion.

However, we remain cautious of the near-term macroeconomic setup, nonetheless, particularly the consequences of a higher for longer rate environment on sector multiples, and the impact of an uncertain consumer spending backdrop on EV adoption and charging utilization rates critical to scaling EVgo's business. The combination of near- and longer-term considerations drive our 12-month base case PT of $5 for the stock, representing upside potential of 33% from current levels.

Comments