Summary

- Goodyear Tire & Rubber expects the business to recover in late 2023, leading to a low forward price-to-earnings ratio.

- The company has exhibited poor business performance in the first half of the year due to lower demand and destocking of customers.

- Goodyear Tire & Rubber has a high debt load and is unlikely to grow its earnings in a sustainable way due to intense competition.

JHVEPhoto

After a poor business performance in the first half of the year, Goodyear Tire & Rubber (NASDAQ:GT) expects its business to begin to recover late this year. As analysts agree on this outlook, the stock is trading at only 9.1x times its expected earnings in 2024. Such a low earnings multiple is likely to lead many investors to think that the stock is a bargain. However, Goodyear is not as cheap as it seems on the surface due to a series of risk factors.

Business overview

Goodyear has a 125-year history and has grown from a small rubber manufacturer to one of the largest tire companies in the world. It manufactures its products in 57 facilities in 23 countries around the globe and has consistently demonstrated innovation in its business.

Goodyear has exhibited poor business performance in the first half of the year. Heading into the second quarter, the company was expecting improved trends but its expectations proved too optimistic. The number of tire units sold decreased 11% over the prior year’s quarter due to continued destocking of customers and lower demand from consumers. The trend was worse in the commercial replacement industry, which experienced a 21% decline in sales due to accelerated channel destocking. Total sales were assisted by price hikes but they decreased 7%. Notably, the total volume sold was 16% below its level in 2019, just before the pandemic. In other words, sales were much lower than normal levels and the tailwind from pent-up demand after the pandemic has essentially disappeared.

Given also a 25% increase in interest expense as well as higher pension costs, the company switched from earnings per share of $0.50 to a loss per share of -$0.34, thus missing the analysts’ consensus by a massive $0.50. Total revenue of $4.9 billion missed the analysts’ estimates by $300 million. Overall, it was a highly disappointing quarter, which confirmed that high inflation is taking its toll on consumer spending on tires, leading them to replace them later than normal.

On the bright side, management expects a significant improvement in business trends in the second half of the year thanks to moderating inflation and declining costs of raw materials, which can enhance operating margins. It is also encouraging that June was the first month of the year in which U.S. consumer replacement industry exhibited growth. Moreover, demand for travel is growing, with miles driven up about 2% over the prior year. This is a positive trend for Goodyear, as it is likely to somewhat accelerate the replacement of tires. Furthermore, the company is in the process of curtailing some costs in order to enhance its operating margin. Thanks to all these factors, Goodyear expects to improve its operating margin from marginally negative in the second quarter towards its near-term target of 8% in the second half of this year.

Analysts seem to agree on the outlook of management. Despite the loss per share of -$0.64 in the first half of the year, analysts expect Goodyear to post just a marginal loss per share of -$0.04 in the full year. Even better, they expect a strong recovery next year, with earnings per share of $1.33. The stock is currently trading at only 9.1x times its expected earnings in 2024. Nevertheless, investors should be aware of the risks of Goodyear.

Risk #1: Poor performance record

Goodyear has exhibited a poor and volatile performance record. To be sure, its total revenues steadily declined between 2013 and 2020. They have recovered strongly since 2020 thanks to the recovery of the global economy from the pandemic but they have hardly grown over the last decade. During the last 12 months, Goodyear has generated total revenues of $20.5 billion. This amount is just 5% higher than the revenues of the company in 2013. Given also the sky-high inflation in 2022, it is evident that Goodyear has failed to grow its inflation-adjusted revenues over the last decade.

This is a testament to the highly competitive nature of the business of the tire manufacturer. While the company does its best to differentiate its products in quality from competitors, other companies produce high-quality tires as well. In addition, numerous consumers prefer cheaper brands for their vehicles.

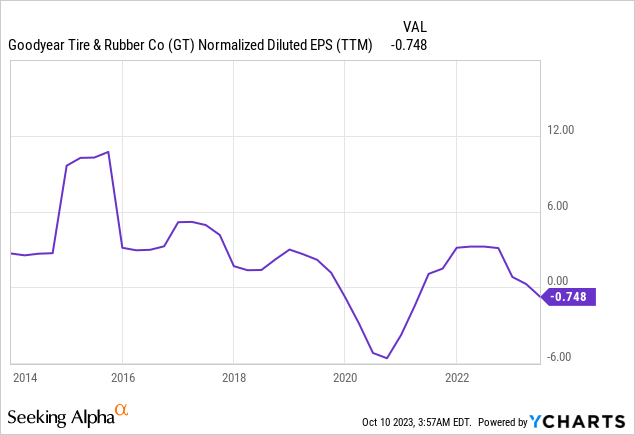

The bottom line performance of Goodyear is even worse, as the earnings per share of the company are extremely volatile.

Data by YCharts

Data by YCharts

It is also remarkable that Goodyear posted material losses in 2019, 2020, and the last 12 months. The poor performance record of Goodyear is clearly reflected in its dramatic underperformance vs. the broad market over the long run. During the last decade, the stock has declined 47% whereas the S&P 500 has rallied 146%.

The vast underperformance of Goodyear may lead some investors to think that the time has come for the stock to outperform the broad market. However, there are no signs of a sustainable recovery on the horizon. Even if the current headwinds from the impact of high inflation and a slowing global economy on consumer spending abate, the intense competition in this business is likely to remain in place. Moreover, it is a prudent investing strategy to avoid stocks that underperform the broad market over the long run. It is unreasonable to have exposure to the risk of a single stock when the broad market offers a much higher risk-adjusted return over the long run.

Risk #2: Debt

The other major risk factor of Goodyear is its weak balance sheet. Its net debt (as per Buffett, net debt = total liabilities – cash – receivables) is standing at $13.5 billion. This amount is more than 4 times the market capitalization of the stock and hence it is excessive. Its burden on the results of the company is prominent, as net interest expense ($445 million) has exceeded operating income ($398 million) by a wide margin in the last 12 months. High interest expense is a key factor behind the losses of Goodyear in the last 12 months.

Moreover, Goodyear has a heavy debt maturity schedule over the next seven years.

Debt load of Goodyear (Investor Presentation)

Source: Letter to shareholders

While it has no debt maturities next year, it is facing debt maturities of $801 million in 2025 and $1.565 billion in 2026. Under normal business conditions, the company may be able to refinance its debt. However, whenever it faces an unforeseen downturn, such as a recession, it is likely to struggle to service its debt.

Final thoughts

Goodyear is likely to begin to recover in the upcoming quarters but it carries a significant amount of risk. The combination of volatile business performance, vulnerability to recessions and a high debt load render the stock highly risky from a long-term point of view. Its vast underperformance vs. the S&P 500 over the long run is a testament to the high risk of this stock. Goodyear may be suitable for traders who try to time the business cycles of the stock but it is not a buy-and-hold stock.

Comments