Summary

- Cross Timbers Royalty Trust stock has underperformed the S&P 500 since my latest article, shedding 15% while the index remained flat.

- However, the stock remains risky.

- The outlook for oil and gas markets suggests lower prices in the upcoming years due to the shift towards renewable energy sources.

mysticenergy

About three years ago, I stated that Cross Timbers Royalty Trust (NYSE:CRT) could double over the following two years, as its stock price had been beaten to the extreme amid the coronavirus crisis. The stock doubled in just 15 months and doubled once more later thanks to the Ukrainian crisis, which led the prices of oil and gas to skyrocket. About four months ago, I recommended selling the oil and gas trust due to a rich valuation from a long-term perspective and the threat related to the boom of green energy projects. Since that article, the stock has underperformed the S&P 500 by a wide margin, as it has shed 15% whereas the index has remained flat. Cross Timbers Royalty Trust has declined 39% off its peak in February and thus it may lead some investors to consider the stock a bargain. However, the trust remains risky from a long-term point of view.

Business overview

Cross Timbers Royalty Trust is an oil and gas trust that holds a 90% net profit interest in some producing properties in Texas, Oklahoma and New Mexico and a 75% net profit interest in a few other properties in Texas and Oklahoma. The trust generates approximately 50% of its revenues from oil and the other 50% from natural gas. Therefore, it is important to examine the outlook of both the oil market and the natural gas market in order to evaluate the stock.

Cross Timbers Royalty Trust has been thriving since early last year thanks to the Ukrainian crisis. Shortly after the invasion of Russia in Ukraine, the U.S. and the European Union initiated strict sanctions on the oil and gas exports of Russia. As the latter had a market share of about 10% in the global oil market and 35% in the European gas market, both markets became extremely tight and thus the prices of oil and gas skyrocketed to multi-year highs last year.

These developments were ideal for a pure upstream oil and gas producer, such as Cross Timbers Royalty Trust. To be sure, the trust grew its distribution per unit 78% last year, from $1.10 in 2021 to an 8-year high of $1.96 last year.

The prices of oil and gas have moderated off their blowout levels last year, as the global energy market has begun to absorb the impact of the war in Ukraine. Nevertheless, as there is a lag between benchmark prices and the actual realized prices of the trust, Cross Timbers Royalty Trust has offered total distributions of $1.52 in the first 9 months of this year. When annualized, this performance is roughly in line with the performance of the trust last year. At the current stock price, these distributions correspond to a 10.9% annualized yield.

However, in the second quarter, the price of oil decreased 18% over the prior year's quarter while oil production remained flat. The average realized gas prices rose significantly, but their effect was offset by reduced gas output due to timing of sales. As a result, the distribution of the trust in the second quarter decreased 16% year-on-year.

Moreover, the realized oil and gas prices of Cross Timbers Royalty Trust decreased further in the third quarter, as they finally caught up with the decrease in benchmark prices. Although Cross Timbers Royalty Trust will report its third quarter results in November, we already know that its distributions in the third quarter fell 34% over the prior year's period.

As Cross Timbers Royalty Trust is highly sensitive to the prices of both oil and gas, we will examine the outlook of each market separately in order to evaluate the stock.

Outlook of the oil market

As mentioned above, the price of oil reached a multi-year high last year due to the sanctions of western countries on Russia. However, Russia has finally found ways to offset the impact of the sanctions by directing higher volumes of crude oil to China, India and a few other Asian countries.

On the other hand, OPEC and Russia have implemented several rounds of production cuts in order to limit the global oil supply and thus support the price of oil. The latest decision of Saudi Arabia and Russia to extend their production cuts of 1.3 million barrels per day until the end of the year triggered a 22% rally of the oil price in just one month. Overall, the price of oil has remained above average, even though it has deflated off blowout levels last year.

However, it is important to realize that the strategy of OPEC and Russia results in a transfer of market share from these countries to non-OPEC countries. As per the latest Oil Market Report - September 2023 - Analysis - IEA of the International Energy Administration [IEA], the aggregate production cuts of 2.5 million barrels per day of OPEC and Russia since early this year have been offset by record U.S. and Brazilian output and a steep production increase from Iran. Therefore, OPEC and Russia are not likely to continue reducing their production much further to support the oil price.

Moreover, demand growth is expected to decelerate from next year due to the exponential increase in the sales of electric vehicles and a record number of green energy projects that are in their development phase. The boom in green energy projects, which has resulted from the sky-high oil prices experienced last year, is not likely to abate until oil prices plunge from current levels. Given also the proven cyclicality of oil prices, it is prudent to expect lower oil prices in the upcoming years.

Outlook of the natural gas market

The price of natural gas collapsed early this year due to an abnormally warm winter but it has recovered strongly since then thanks to strong demand, though it remains about 65% lower than its multi-year peak last year.

As per the latest Short-Term Energy Outlook of the Energy Information Administration [EIA], U.S. natural gas consumption is expected to have grown by 5% in September over the prior year, to a new all-time high, after record levels in July and August. This helps explain the approximate 50% rally of the price of natural gas off its lows this year.

However, U.S. natural gas consumption is expected to decrease from 89.7 to 88.8 billion cubic feet per day next year while production is expected to grow by 2.2 billion cubic feet per day. While higher LNG exports are likely to cover part of the resultant surplus, the gas market is likely to be well supplied next year, in the absence of severe winter weather. Given also the aforementioned boom in green energy projects, which resulted from the fierce energy crisis experienced last year, it is prudent not to expect higher gas prices in the upcoming years. As soon as all the renewable energy projects being developed begin to generate energy, they will probably reduce the consumption of natural gas.

Distribution - Valuation

Most stocks are evaluated based on their price-to-earnings ratios. However, oil and gas trusts distribute all their net income to their unitholders. Therefore, they can be evaluated based on their distribution yield. More precisely, investors can compare the current distribution yield to the historical average distribution yield of a trust to draw a conclusion on the valuation of the trust.

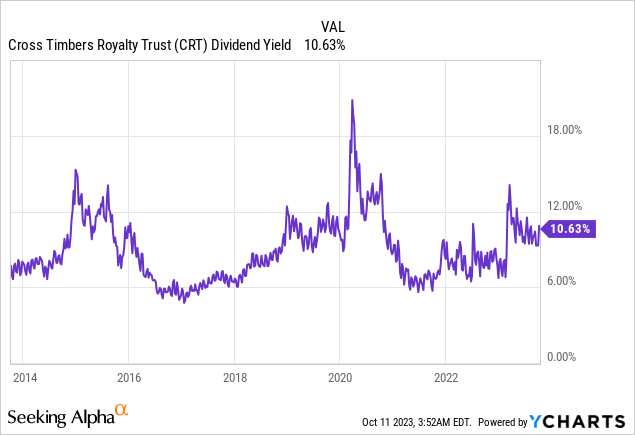

As mentioned above, Cross Timbers Royalty Trust has offered total distributions of $1.52 in the first 9 months of the year, corresponding to a 10.9% yield at the current stock price. However, as oil prices have decreased and gas prices have plunged off last year’s blowout levels, this yield is misleading.

The trust has offered total distributions of $0.49 in the last four months. These distributions, which correspond to an annualized yield of 7.9%, are more representative of normal commodity prices. The 7.9% yield may seem high on the surface, but it is lower than the 10-year average yield of 9.3% of the stock.

Data by YCharts

Data by YCharts

The market has historically required such a high yield from Cross Timbers Royalty Trust over the last decade primarily due to the risk related to the long-term natural decline of the production of the trust. The trust has repeatedly stated that it expects its oil and gas production to decrease by 6%-8% per year on average over the long run. This is an extremely strong headwind for future returns. To be sure, despite the 13-year high prices of oil and gas last year, the distributions in 2022 were 26% lower than those in 2014.

To conclude regarding the valuation of Cross Timbers Royalty Trust, we note that its current yield (7.9%) is lower than its 10-year average yield (9.3%). Therefore, the stock appears overvalued right now.

Notably Cross Timbers Royalty Trust is currently offering a higher yield than its peers Sabine Royalty Trust (SBR) and Permian Basin Royalty Trust (PBT), which are yielding 6.0% and 5.9%, respectively, based on their distributions in the last four months. However, these trusts are probably overvalued as well thanks to the above average prices of oil and gas prevailing right now.

As mentioned earlier, it is prudent to expect oil prices to deflate off current levels and gas prices to moderate, primarily due to the accelerated shift of the entire world from fossil fuels to renewable energy sources. Whenever oil and gas prices incur a material correction, Cross Timbers Royalty Trust will probably have significant downside risk.

In order for Cross Timbers Royalty Trust to reach a reasonable valuation level, the stock should correct by about 18% (=9.3%/7.9% -1) and then by at least ~20% in order to account for the expected moderation of commodity prices and the production decay of the trust. Therefore, a more reasonable stock price would be approximately $12.2 (=$18.64 * 0.82 * 0.80).

Upside risk

The long-term outlook for oil and gas prices is bearish due to the boom of green energy projects but a temporary rally of these prices cannot be excluded. If OPEC and Russia keep reducing their output, they will trigger a rally of the price of oil or avert its correction. A geopolitical event, such as the recent turmoil in Israel, could also fuel a rally of the oil price. In addition, natural gas prices will probably rally if we experience an exceptionally cold winter. In all these cases, the stock of Cross Timbers Royalty Trust is likely to enjoy a rally off its current price.

Final thoughts

Cross Timbers Royalty Trust is offering a seemingly attractive yield of 7.9%. However, oil and gas prices are likely to decrease at some point in the upcoming years due to the ongoing transition from fossil fuels to clean energy sources. As a result, distributions are likely to decrease in the future. Given also the material decrease in the production of the trust over the long run, the stock has significant downside risk.

Comments