Summary

- Many individual investors focus on high dividend-paying stocks and funds, like Vanguard High Dividend Yield ETF, for consistent cash payments.

- VYM has underperformed the S&P 500 over the past decade and offers a marginally lower average rate of return.

- VYM and the S&P 500 offer low returns compared to 5.5% yielding short-term Treasury bonds.

- VYM's dividend yield is currently just ~1% higher than the 10-year real Treasury rate, implying overvaluation to bonds of at least ~20%.

- I expect VYM to fare slightly better than the S&P 500 due to its reduced exposure to growth stocks, but income-oriented investors will likely find better yields, with lower volatility, in bonds.

Dilok Klaisataporn

Many individual investors today focus on high dividend-paying stocks and investment funds, particularly retired investors. High dividend funds, such as the popular Vanguard High Dividend Yield ETF (NYSEARCA:VYM), are attractive because they offer consistent cash payments. In an economic and political world with a general lack of consistency, it is understandable that investors are very attracted to ETFs with dependable dividends.

Dividend investing remains extremely popular today due in part to the many retired investors. That said, higher dividend stocks have often outperformed over long periods. Of course, whenever any investing strategy becomes too popular, it is at greater risk of overvaluation and unreasonable expectations. Past performance is not a good predictor of future returns. In my experience, solid past performance can predict impending underperformance due to overvaluation and unjustified expectations.

I believe this issue is more significant today than ever before due to the concentration issue plaguing many large-cap market capitalization-weighted ETFs. As investors allocate into large-cap ETFs, more money flows toward the most extensive stocks in the fund or those with the highest market capitalization - thus pushing their market capitalization even more elevated and creating added concentration risk factors. Hence, most large-cap ETFs are seeing tremendous exposure to only a few companies compared to the expected levels of diversification.

"High dividend" ETFs such as VYM also face some risks related to changes in interest rates. Bond yields are much higher today, with long-term Treasury bonds offering yields of around 5%. VYM's dividend yield is just 3.25%, and it has not raised its dividend materially in years due to profit pressures on many of its constituents. This issue could grow as companies in VYM refinance their debt and higher interest rates, causing them to pay less in dividends and more in interest. Thus, higher long-term rates may lower the dividends on VYM and make VYM a comparatively worse investment than higher-yielding bonds.

Of course, VYM and its peers have many positive qualities compared to other large-cap ETFs. VYM has been more stable than the S&P 500 and other large indices over the past two years. Further, its superior sector diversification limits its exposure to issues facing specific sectors disproportionately owned in the S&P 500. As such, I believe it is an excellent time to take a closer look at VYM compared to the S&P 500 to determine its risk-reward value for retired investors better.

Historical Risk-Reward Differences

In my view, investors should not focus too much on reward or risk but look to maximize reward potential while minimizing risk. In other words, find the best investments within a particular band of risk tolerance. In part, higher dividend stocks are often viewed as less risky because more mature and established companies usually focus on dividends. In contrast, growing companies or those with falling profits must reserve cash flows. Notably, VYM generally excludes stocks with extremely high dividend yields over 10% because it is market cap weighted; such stocks usually pay high yields due to leverage and not corporate maturity.

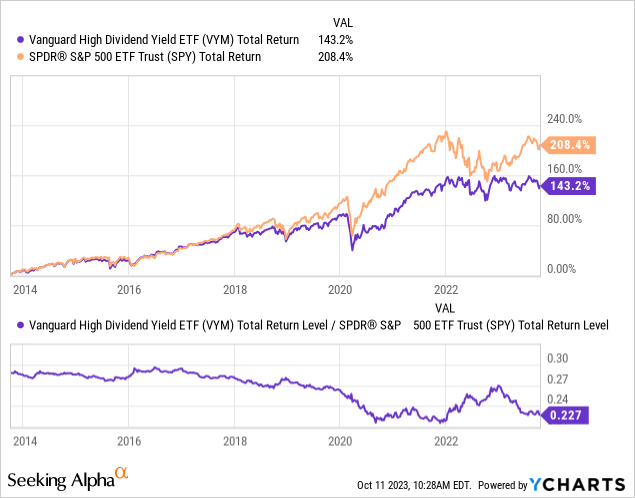

Over the past decade, VYM has underperformed the S&P 500 significantly, particularly since 2019. It has delivered a total return (including dividend reinvestments) of 143% over the past decade compared to the S&P 500 at 208%. See below:

Data by YCharts

Data by YCharts

VYM's most significant period of underperformance was around 2020 when growth stocks significantly outperformed due to the decline in interest rates. Compared to the S&P 500, VYM has less growth exposure, with a 12.5% earnings growth rate compared to 18% for the S&P 500. Growth stocks generally have greater exposure to interest rates than dividend stocks; however, both typically perform better as rates decline. Still, for this reason, VYM outperformed the S&P 500 in 2022 as interest rates rose. Its absolute performance has generally been flat throughout recent years, so its performance differences are mainly due to changes in growth-stock valuations in the S&P 500.

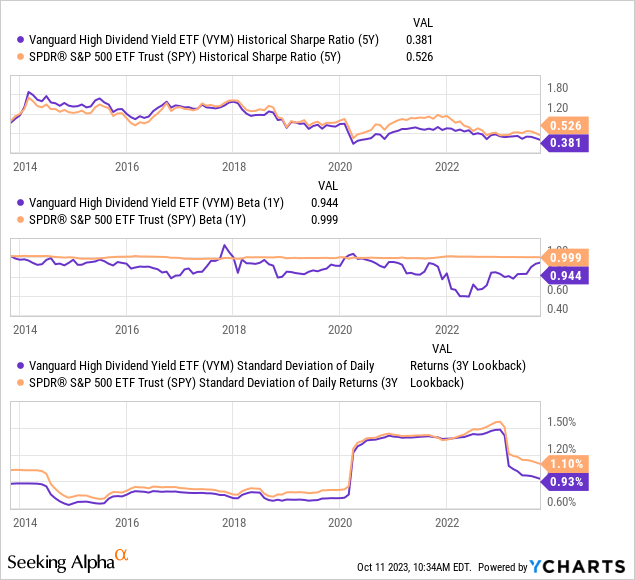

Compared to the S&P 500, VYM is usually a mildly lower-risk investment. Over the past three years, its overall volatility has been around 85% of the S&P 500 and has essentially always been lower over the past ten years. VYM's "beta," or expected price change given a 1% change in the S&P 500, is almost always lower. Over the past year, a 1% change in the S&P 500 is associated with a 94.4 bps change in VYM; however, in 2022, that figure dropped as low as 60 bps due to a decline in VYM's correlation. See its risk metrics below:

Data by YCharts

Data by YCharts

VYM is a lower-risk asset than the S&P 500, but does it offer a better risk-reward trade-off? Based on the Sharp ratio, a performance measure minus interest rates to volatility, it is historically a worse risk-reward investment. VYM's Sharpe over the past five years is 0.38 compared to 0.53 for the S&P 500, meaning its "risk-free return" is 38% of its performance standard deviation.

Crucially, the Sharpe Ratios of both VYM and the S&P 500 have trended lower over the past decade, with the most notable decline since 2022. The key reason for its low Sharpe ratio today is the high risk-free return rate, currently of 5.5%. Investors can buy short-term Treasury bills like those in the ETF (SGOV) for a 5.5% risk-free return. Treasury bills are considered risk-free because the US Treasury can expect to create money to pay its bills if need be. Of course, if the US government defaulted on its debt permanently, I doubt most stocks would retain their value. Thus, a vastly superior risk-for-reward tradeoff is found in short-term Treasury bonds than in either VYM or the S&P 500. Rarely, short-term Treasury bonds currently pay a higher yield than even "high dividend" ETFs like VYM.

Overall, compared to the S&P 500, VYM is not too different. VYM is a less risky equity investment, given its lower volatility, due to its reduced exposure to sensitive interest-rate growth stocks. VYM's lower volatility is likely attributable to its superior sector diversification, having a ~10-20% exposure to most sectors compared to ~5% to 30% in the S&P 500. That said, even accounting for dividends, VYM is only marginally less risky than the S&P 500 and offers a marginally lower average rate of return. Further, both VYM and the S&P 500 are, in my view, inferior to short-term Treasury bills because they offer a higher yield with magnitudes lower volatility.

VYM's Short and Long-Term Outlook

VYM faces risk and reward factors related to economic and financial market changes. Compared to the S&P 500, VYM has greater exposure to financials (20% vs. 12.5%) and much less to technology (7% vs 28%). Those are the two only significant differences in the sector exposures of each. VYM's lower technology exposure is a positive because I believe that segment is more overvalued today. However, VYM's greater financial exposure could be an issue given the potential solvency risks remaining in banks, correlated to higher interest rates.

VYM has had decent dividend growth over the past decade; however, its dividend has hardly changed since 2020 and has become considerably more volatile. The income levels of its holdings have risen over this period, but the companies have not raised dividends significantly. Many stocks in VYM are older and more established, some with considerable bond market debt. As rates are much higher today, many firms face an impending $1.8T debt repayment wall and will likely choose to pay the debt off instead of refinancing at higher interest rates. This issue faces all companies with debt leverage and could be a significant issue going into 2024, requiring some dividend cuts to improve cash positions.

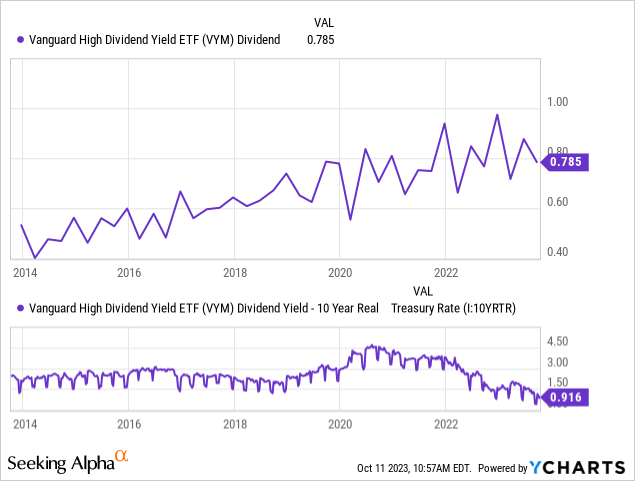

While VYM's dividend has stagnated, its spread to the real Treasury yield has crashed tremendously. In my view, real Treasury yields, based on after-inflation returns on inflation-indexed Treasury bonds, are very relevant to VYM because VYM's dividend should be tied to inflation in the long term. For example, if inflation is very high, buying VYM at a lower dividend yield than fixed-rate bonds is reasonable because we can assume its dividend will rise with inflation. However, because VYM's dividend is much lower than the inflation-indexed long-term bond yield, VYM is likely overvalued to bonds. See below:

Data by YCharts

Data by YCharts

Historically, VYM's dividend is around 2% above the 10-year Treasury real yield. Today, it is just 91bps higher, indicating VYM's yield would need to rise by about 1% to bring it back into parity with the inflation-indexed bond market. In other words, investors are likely better off buying 10-year inflation-indexed bonds, such as those in the ETF (TIP), than VYM if they seek the best total dividend return. A 1% increase in VYM's yield at its current price would lower its value by ~23%.

The Bottom Line - Just Buy Bonds

Overall, I am bearish on VYM and believe it is not a significant investment over the next year and likely beyond. Although it is less volatile than the S&P 500, it is functionally about as risky and should decline similarly during a recessionary crash. The only significant difference between the two is VYM's reduced growth-stock exposure, giving it a lower inverse correlation to fixed interest rates. Still, it is a generally poor investment with a far-below-average spread compared to inflation-hedged interest rates.

Further, with some models suggesting a greater than 50% recession probability in 2024, one can argue that equities should trade at a discount to bonds due to the possibility of lower distributable cash flows. Instead, VYM trades at a considerable premium to bonds based on its yield spread. Further, like the vast majority of established large-cap stocks, VYM is likely exposed to the impending record corporate bond maturity wall. Over the past decade, as corporate debt has risen, companies have refinanced at low rates but will now need to repay or lose profits from interest rate increases. This issue will ramp up in 2024 and peak around 2025, likely impacting dividend-paying companies by increasing corporate cash needs.

Still, despite its risks, I prefer VYM to the S&P 500. For one, VYM is not as exposed to technology companies, which I believe are today's most overvalued sector. Secondly, its general sector diversity is higher, giving it less "concentration risk" than the S&P 500. While I expect both VYM and the S&P 500 to crash in a recession, VYM may outperform the S&P 500 more than historically. To me, far superior risk-reward (and total return) potential can be found in the bond market, particularly inflation-hedged and short-term Treasury bonds, which offer better dividends at lower risk than VYM. Still, I remain bearish on long-term fixed-rate bonds due to inflation volatility.

Comments