Summary

- National Storage Affiliates Trust has underperformed the market due to the impact of high interest rates on its interest expense and its valuation.

- The REIT has room for future growth, a resilient business model and a healthy balance sheet, making it likely to endure the downturn.

- The stock is currently trading at a nearly 10-year low price-to-FFO ratio and offers a nearly 10-year high dividend yield.

bin kontan

National Storage Affiliates Trust (NYSE:NSA) has dramatically underperformed the broad market in the last 12 months, as it has declined 21% whereas the S&P 500 has rallied 19% and the Real Estate Select Sector SPDR Fund ETF (XLRE) has shed only 1%. The underperformance of the REIT has resulted primarily from persistent inflation, which has led the Fed to raise interest rates to a 16-year high. High interest rates have nearly doubled the interest expense of National Storage Affiliates while they also exert pressure on its valuation, as they significantly reduce the present value of future cash flows.

However, the stock of National Storage Affiliates seems to have been beaten to the extreme. It is currently trading at a nearly 10-year low price-to-FFO ratio of 11.9x and is offering a nearly 10-year high dividend yield of 7.3%. As the REIT has ample room for future growth and has a healthy balance sheet, it is likely to endure the ongoing downturn without any problem. Therefore, whenever interest rates moderate, the stock is likely to highly reward investors, given its extremely cheap valuation level right now.

Business overview

National Storage Affiliates is a self-managed REIT that focuses on the operation and acquisition of self-storage properties located within the top 100 metropolitan areas throughout the U.S. and Puerto Rico. The REIT owns 1,117 self-storage properties in 42 states and Puerto Rico, with 72.8 million rentable square feet.

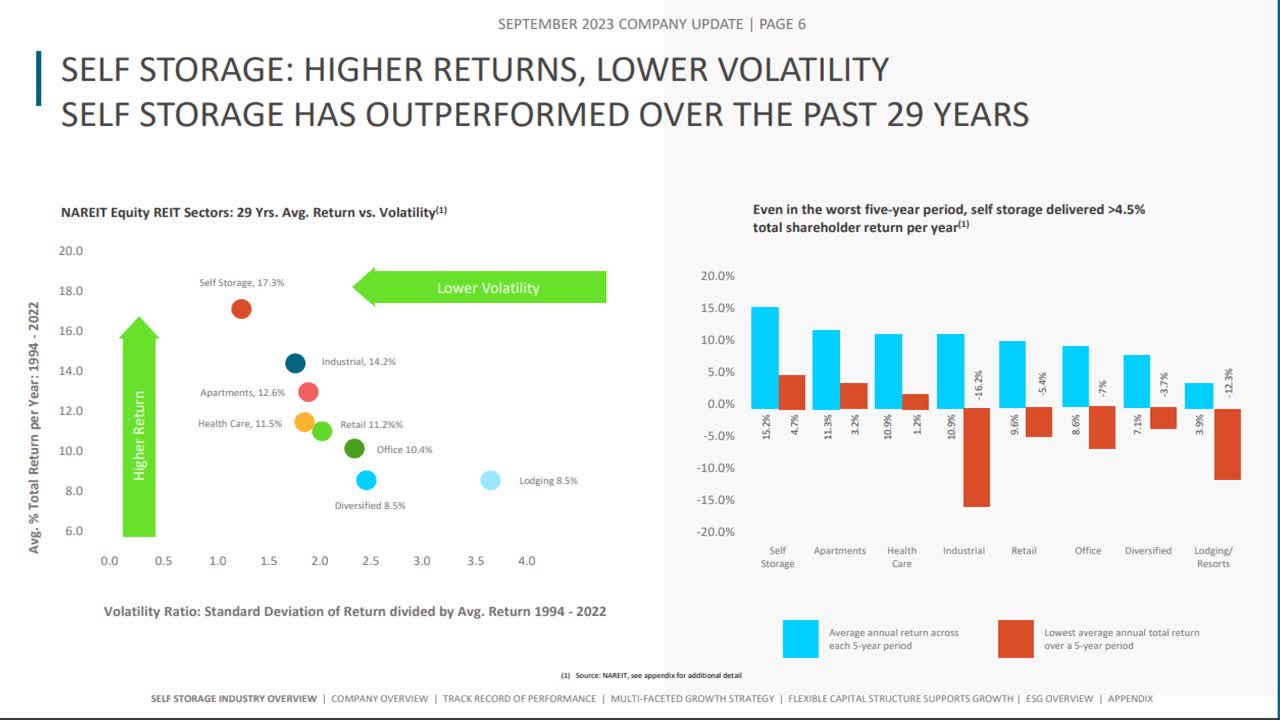

Self-storage REITs have outperformed the other categories of REITs with much lower volatility over the last 29 years. This is clearly reflected in the chart below.

Outperformance of Self-Storage REITs (Investor Presentation)

Source: Investor Presentation

Even in the worst 5-year period, self-storage REITs outperformed the other REITs by more than 4.5% in total shareholder returns.

A major factor behind the impressive outperformance of self-storage REITs is the high fragmentation of this industry. The top 100 operators own just one-third of the total self-storage facilities while National Storage Affiliates has a market share of only 2%. As a result, the REIT has ample room for growth for several years.

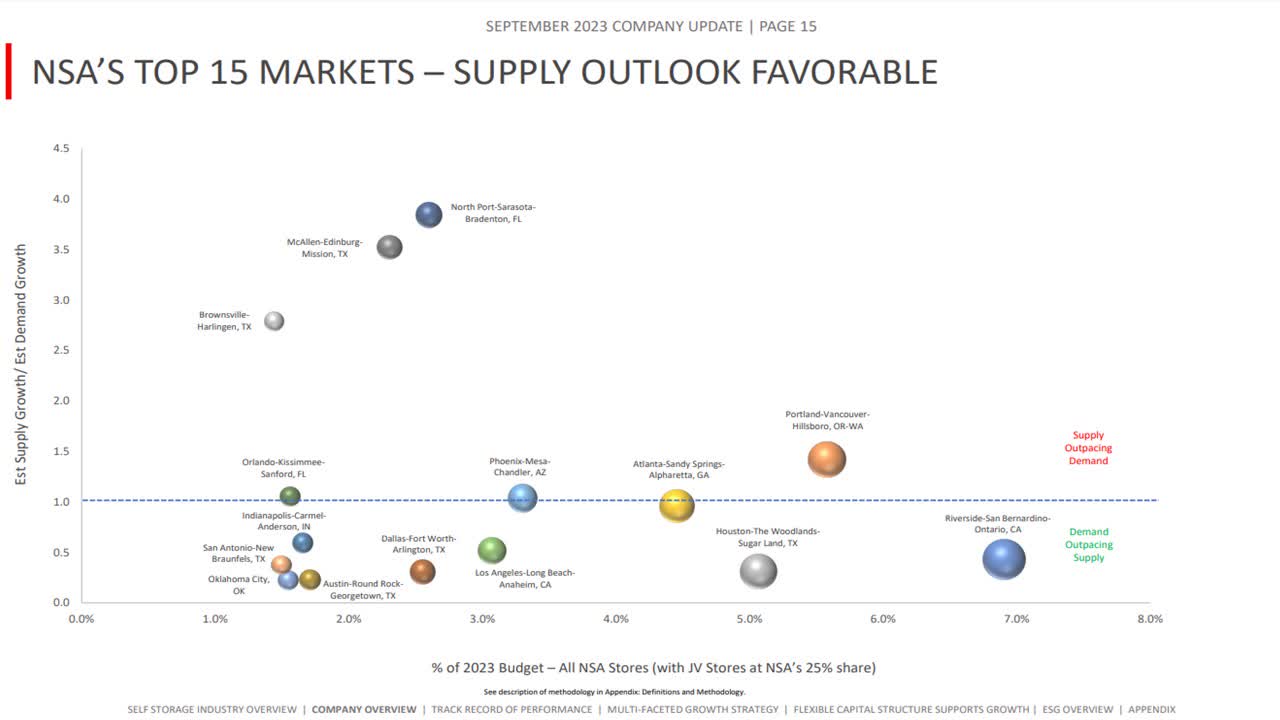

Moreover, National Storage Affiliates has 66% of its properties in the Sun Belt region. This region enjoys higher economic and population growth than the rest of the country, thus providing a tailwind to the business of National Storage Affiliates. Furthermore, the top 15 markets of the REIT have favorable supply-demand characteristics.

Supply/Demand in Top 15 Markets of NSA (Investor Presentation)

Source: Investor Presentation

More precisely, in 11 of the top 15 markets of National Storage Affiliates, the estimated growth in the demand for self-storage properties outpaces the estimated growth in their supply. This fact is likely to provide the REIT with strong pricing power in most of its top markets.

The favorable characteristics of the self-storage industry have contributed to the exceptional performance record of National Storage Affiliates. The company has grown its FFO per unit every single year since 2015, at an outstanding average annual rate of 19.9%. The growth rate is undoubtedly impressive but the consistent business performance is equally important, as it reveals a robust business model. Even in 2020, which was marked by the fierce recession caused by the coronavirus crisis, National Storage Affiliates grew its bottom line by 10%, from $1.53 to $1.69.

Even better, National Storage Affiliates still has ample room for future growth thanks to the highly fragmented status of its industry. The company has identified 281 properties, which have an approximate value of $3.0 billion and are attractive as acquisition targets. As this amount is 75% of the market capitalization of National Storage Affiliates, it is evident that the trust has ample room to continue growing for several more years.

Valuation

National Storage Affiliates is currently trading at a forward price-to-FFO ratio of 11.9x. This FFO multiple is much lower than the 8-year average price-to-FFO ratio of 17.5x. On the one hand, a somewhat cheap valuation can be attributed to the surge of interest rates to a 16-year high, as high interest rates significantly reduce the present value of future cash flows.

On the other hand, interest rates are not likely to remain around their 16-year highs for years. Thanks to its aggressive policy, the Fed has already managed to cool inflation from a peak of 9.2% in June 2022 to 3.7% now. It can thus be reasonably expected to restore inflation to its target zone of 2.0%-2.5% at some point in 2024 or 2025. Whenever the Fed achieves its goal, it will probably begin reducing interest rates towards normal levels. When that happens, the valuation of National Storage Affiliates is likely to revert towards its historical average. Overall, the REIT will have great upside potential whenever interest rates normalize.

Dividend

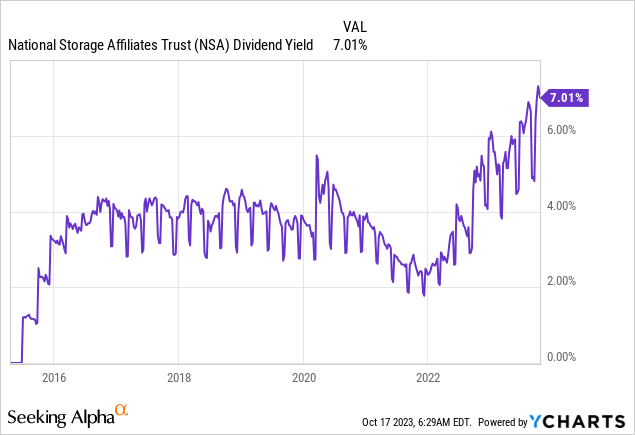

Due to its 21% decline in the last 12 months and its exceptionally cheap valuation level, National Storage Affiliates is currently offering a nearly 10-year high dividend yield of 7.3%.

Data by YCharts

Data by YCharts

The REIT has grown its dividend by 14.3% per year on average over the last five years, much faster than the entire REIT sector, which has grown its dividend by only 0.3% per year on average. However, as National Storage Affiliates has a forward AFFO payout ratio of 90%, investors should not expect meaningful dividend growth, at least in the short run.

Due to the surge of interest rates to a 16-year high, Interest expense has nearly doubled over the last two years, from $72 million in 2021 to $141 million in the last 12 months. As a result, it now consumes 43% of operating income. However, net debt (as per Buffett’s formula, net debt = total liabilities – cash – receivables) is standing at $3.7 billion. This amount is not negligible but it is 90% of the market capitalization of the stock and about 11 times the annual FFO. Therefore, the debt of National Storage Affiliates is manageable, particularly given the reliable growth trajectory of the REIT. It is also important to note that the REIT has received an investment grade credit rating of BBB+ from Kroll Bond Rating Agency. Overall, the dividend of National Storage Affiliates appears to have a meaningful margin of safety.

Risk

Given the defensive nature of the self-storage industry and its resilience to the pandemic, National Storage Affiliates is likely to prove fairly resilient whenever the next recession shows up. Therefore, a potential recession does not pose a major threat to the defensive REIT.

The only material risk factor is the adverse scenario of persistently high inflation for several years. In such a case, interest rates are likely to remain at excessive levels for years and thus they will have a negative effect on the interest expense of National Storage Affiliates. However, as the REIT has an interest coverage ratio of 2.3, it is not likely to face any problem servicing its debt.

The adverse scenario of persistent inflation would also cause the valuation of the stock to remain under pressure for longer than currently expected. However, such a scenario is unlikely. As mentioned above, thanks to its determination, the Fed is likely to restore inflation to its target range at some point within the next two years. To cut a long story short, the stock of National Storage Affiliates will be adversely affected in the event of sticky inflation for years but such a scenario has low odds of materializing.

The bottom line

National Storage Affiliates is a high-quality self-storage REIT, which has many attractive characteristics. It is on a reliable growth trajectory thanks to the high fragmentation of its industry, it is fairly resilient to recessions, it is cheaply valued and currently offers a nearly 10-year high dividend yield of 7.3%. Whenever interest rates begin to moderate, the stock is likely to highly reward patient investors.

Comments