Summary

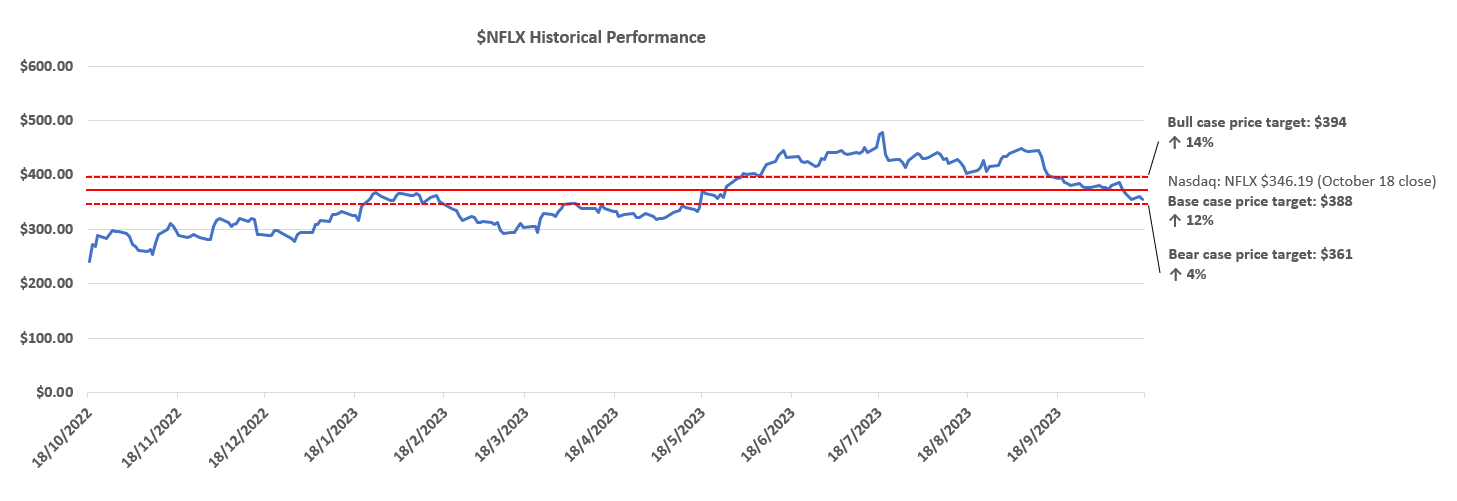

- Netflix, Inc. stock underperformed broader markets in Q3 due to mixed prospects following the global rollout of password sharing and an ad-supported tier.

- Better than expected Q3 results show progress in restoring growth and expanding profit margins, but ad sales and subscriptions still need improvement.

- The following analysis will walk through Netflix's Q3 results and forward guidance, and dive deeper into potential limitations to the stock's near-term upside potential.

Mario Tama

Netflix, Inc. (NASDAQ:NFLX) stock underperformed broader markets during the third quarter, as investors mulled on its mixed prospects following the global rollout of password sharing and an ad-supported tier. The stock had largely been held back by a soft guidance offered in Q2, which had indicated tepid progress in ad sales and subscription amid its early-stage introduction.

Yet Q3 outperformance indicates Netflix is finally turning a page on the newly introduced initiatives aimed at restoring growth amid intensifying competition. Profit margins also expanded, underscoring progress in disciplined spend management to compensate for looming ARM headwinds.

Taken together, Netflix is tracking positively towards its near-term growth ambitions, which we believe the stock’s current value fairly represents. However, we believe Netflix’s in-line Q3 performance has yet to demonstrate that it can kick its ad prospects up a notch, which could be a limiting factor to incremental upside potential within the near-term. Investors are likely looking forward to further optimized leverage of Netflix’s market leadership to take advantage of secular declines in linear TV and drive up ad sales critical to growth reacceleration and bottom line expansion going forward.

Advertising in Question

Netflix completed the rollout of paid sharing and advertising initiatives during Q3, improving visibility into its forward outlook. In addition to solid Q3 outperformance, management has reiterated the company’s full year guidance for incremental growth acceleration through Q4, yet continues to caution limited contributions from the newly introduced revenue streams.

Diving deeper into advertising, which remains a key focus area for investors, the relevant revenue stream has yet to show substantial progress in both consumer adoption rates and ad sales. While paid net additions continued to expand sequentially, revenue growth in Q3 was comparatively modest, underscoring the continued pressure of a soft ad sales ramp-up and concentrated subscriptions from lower-ARM regions.

Consumer Subscriptions: Specifically, on the consumer-facing front, ad-tier subscriptions increased by 70% q/q, tempering from observations in Q2. However, the base remains small altogether, with ad-supported subscriptions still representing a nominal share (estimated at less than 5% on 30% of subscription net add mix) of Netflix’s sales mix. While this is in line with gradual adoption trends observed at peers like Warner Bros. Discovery’s (WBD) and Disney’s (DIS) ad-supported offerings, investors had expected more from Netflix’s market leading competitive position. Markets currently project that Netflix’s ad progress is only “running at about half of internal projections,” which is corroborated by management’s reiterated conservatism on aspirations to grow ad-related contributions into 10% of the company’s revenue mix.

Yet total subscriber net adds continued to grow at a healthy pace, consistent with management’s observations of less churn from recent business model adjustments, and indicative of moderate impact from stiffening competition and broader softness in the consumer spending backdrop than feared.

But this does not mean the overhanging risks should be overlooked. American households are already subscribed to 3.7 streaming services on average, fuelled primarily by a combination of cord-cutting dollars moving online and the increasing availability of different platforms to choose from. Recent industry checks have highlighted content, price and ads as three key considerations among consumers when choosing a streaming service. Most consumers have also indicated high ad-tolerance, regardless of their demographics or tax bracket. Based on recent industry checks, more than a fifth of streaming users "prefer ads to subscriptions on an absolute basis," with more than half of the cohort citing pricing sensitivity for their choice.

Yet the combination of deteriorating household income and savings, tightening credit conditions and ballooning household debt in Netflix’s core U.S. market are further limiting the amount of discretionary income that consumers can allocate to the ever-growing number of streaming platforms available. While Netflix comes out on top among consumers’ key considerations when choosing a streaming service, the weak ramp-up of its value-for-money ad-supported tier indicates also a potentially inadequate go-to-market strategy. This is corroborated by the recent reshuffle of senior management at Netflix, including the replacement of its President of Advertising with longtime Studio Operations executive, Amy Reinhard. The company has also recently announced incremental investments into an internal ad sales and technical infrastructure team to complement efforts at ad technology partner Microsoft (MSFT, which could add pressure on operating expenses going forward.

Advertising: Meanwhile, on the ad sales front, management has reiterated that the revenue stream remains a nominal contribution to Netflix’s consolidated mix. Instead, management remains focused on rolling out and scaling new technologies and features to better address advertisers’ needs. This includes prioritizing the build-out of ad membership volumes, and improving video quality and programming slate to drive further engagement required by advertisers. Netflix is also working on the addition of new advertising formats that would complement its market leading reach, and improve its value proposition to prospective advertisers. This includes the recent launch of “title sponsorships,” and the upcoming introduction of sponsored commercial-free episodes for binge watchers.

As mentioned in the earlier section, current industry trends imply that Netflix’s ad sales are still running substantially below initial internal projections. This is likely reflected in management’s continued conservatism over the revenue stream’s roadmap to contributing 10% of Netflix’s consolidated sales mix, and reiterated focus on the work that needs to be done to ramp up the strategy.

The tepid results at early-stage ramp-up continues to highlight Netflix’s exposure to competitive headwinds and potentially other idiosyncratic weakness in penetrating AVOD opportunities in our opinion. The modest progress in both ad-tier subscriptions and ad sales largely diverges from broader secular tailwinds ensuing from the wind-down of linear TV – which represent the bulk of ad dollars that management is prioritizing, second to broader digital opportunities – and the capability of Netflix’s market leading reach to consumers.

Specifically, the AVOD industry remains a core beneficiary of secular tailwinds in digital advertising, despite the ongoing impact of broader macroeconomic headwinds. AVOD ad sales are expected to increase by more than 11% this year, outpacing the 10% growth expected in the broader digital media vertical. Yet slow growing ad sales at Netflix is likely a reflection of ongoing kinks in key advertiser requirements including targeting, engagement, conversion, placements, and measurement. This also bodes unfavorably by the premium pricing Netflix levies on its advertisers, which we had previously discussed as a potential execution risk factor in the process of ramping up ad sales.

The combination of modest ad-supported subscription and ad sales growth amid heightening competition and broader macroeconomic weakness is likely to imply the continuation of single-digit growth at Netflix for full year 2023 as management had guided. Netflix’s results in recent quarters highlights a lack of differentiation in its ad strategy despite its market-leading consumer reach, highlighting the company’s mishap in fully taking advantage of the new monetization opportunities stemming from ads and paid sharing. This could remain a limiting factor on the stock’s near-term performance, and increase its exposure to broader market volatility amid ongoing macroeconomic uncertainties.

A potential respite to Netflix’s ad strategy is live sports, which management is likely paving way for through the new slate of sports adjacent programming coming in November. Sports have been a fundamental lifeline to linear TV viewership and ad performance, highlighting the segment’s potential for complementing Netflix’s market-leading reach to consumers. However, there remains limited clarity on this foray, and relevant integration will likely take time, thus offering limited respite to Netflix’s efforts in ramping up ad sales over the near-term.

Pricing Impact

Meanwhile, Netflix also faces continued pricing headwinds in the near-term due to the anticipated lapping of price increase tailwinds implemented in early 2022. Despite its recent removal of the lower-ARM basic ad-free tier in UCAN and specific EMEA regions (UK, Italy) to encourage ad-tier sign-ups, which yields a higher ARM, they have been insufficient to offset the lapping price headwinds, as well as the incremental impact of higher net add volumes from lower-ARM regions – particularly LatAm and APAC with their growing contributions to the quarterly paid net membership additions mix. Netflix’s ARM weakness again highlights the urgency to yield better results in ramping up the ad-tier initiatives.

Recent speculation on price increases following resolution of the outstanding SAG-AFTRA strike could also be a two-edged sword for Netflix. On one hand, the implementation of another price hike could alleviate the near-term pressure on ARM amid the ongoing ramp-up of ad-related opportunities and increasing penetration into less affluent regions. This strategy would also follow similar price increases observed at peers this year, as the broader industry looks to turn profitable amid rising competition, and potentially reduce consumers’ aversion to the decision.

Meanwhile, on the other hand, any impending price hikes would come at a time of increased macroeconomic uncertainty. The narrative over a weakening consumer spending backdrop has been brewing since the beginning of the Fed’s latest monetary tightening cycle. Yet the broader economy has largely stayed resilient, thanks to strong labor demand which has been the primary counteractive force to the adverse combination of dwindling pandemic-era savings and persistent inflationary pressure. But this link is likely to give soon – the labor market typically starts to feel the impact of monetary policy tightening about 18 to 24 months after the first rate hike, which means the countdown starts now.

This is corroborated by surging credit card delinquencies that are above pre-pandemic levels in recent months. And the resumption of student loan repayments this month is likely to further exacerbate household budgets. Economists currently estimate a $100 billion displacement in annual discretionary spending due to the resumption of student loan repayments; this translates to a potential adverse impact of 0.1% in GDP growth this year and 0.3% the next. As a result, any implementation of price increases amid the mixed macro backdrop is likely to increase churn or encourage subscription downgrades, which would backfire on Netflix’s aims at expanding ARM and profit margins ahead.

While price increases are typically representative of topline expansion, Netflix likely faces a conundrum in the near-term implementation of said strategy. On one hand, it highlights Netflix’s intentions to raise subscription rates while it still holds pricing power given its unmatched market leadership in order to preserve profitability amid an expensive shift in its business model to support ads. But on the other hand, such a strategy would clash with the deteriorating macroeconomic backdrop.

Meanwhile, if Netflix holds off on price hikes until the economy recovers, competition might be too strong then, exposing it to the risk of diluted pricing power. The situation again highlights why investors might be demanding further progress to Netflix’s ad strategy in the near-term, given it represents an immediate opportunity that leverages the company’s existing market leadership competitive advantage, while also critical to preserving its moat.

Fundamental and Valuation Analysis Update

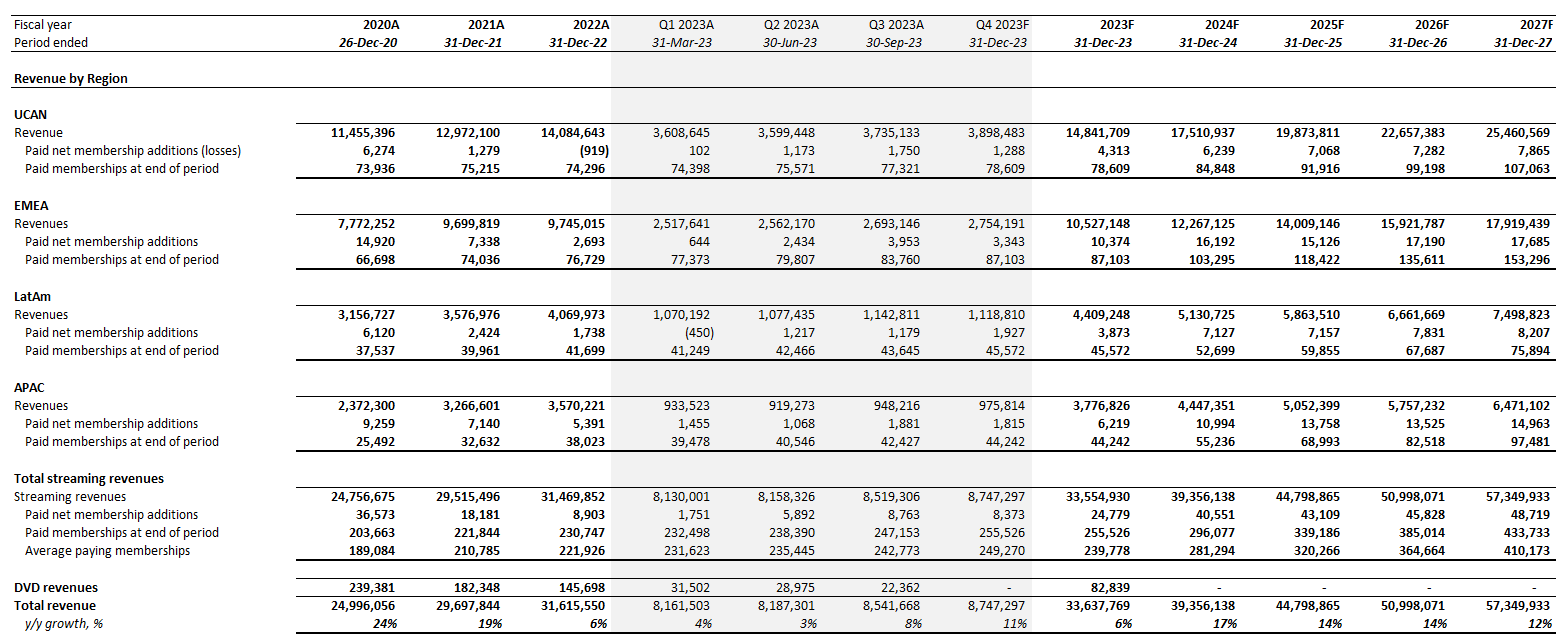

Adjusting our previous forecast for Netflix’s actual Q3 performance and full year expectations as discussed in the foregoing analysis, we expect full-year 2023 revenue to expand 6% to $33.6 billion. This is complemented by anticipated paid memberships of 8.4 million exiting 2023 and flat y/y ARM in line with the absence of PY price increase tailwinds, and tepid progress in near-term ad sales.

Author

On the cost front, we expect full year operating margin to lean towards the higher end of management’s guidance at about 20%, in line with management’s guidance. However, we remain cautious of pressure from ad sales ramp-up costs in the near term.

Author

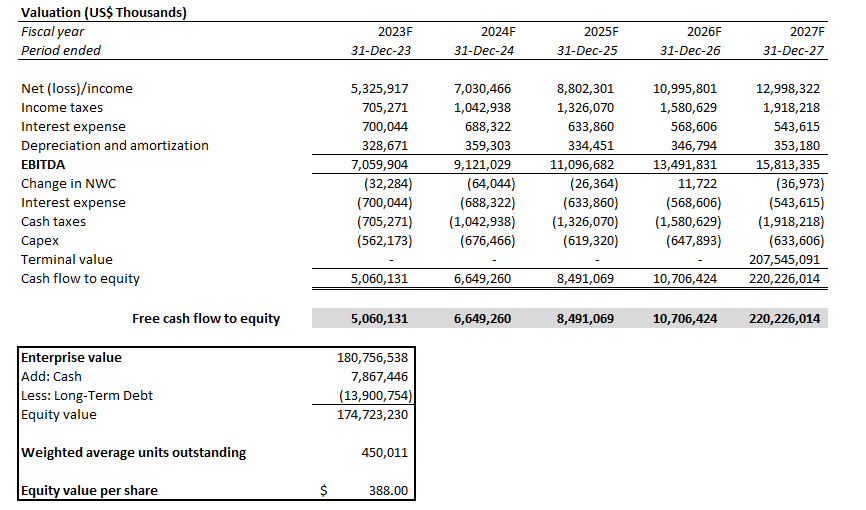

Our base case $388 price target for Netflix is based on the discounted cash flow ("DCF") methodology, which values projected cash flows taken in conjunction with the fundamental forecast above.

Author

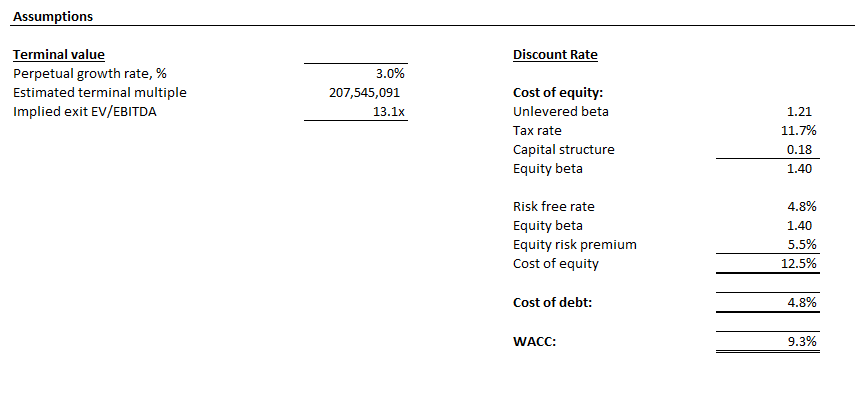

A 9% WACC in line with Netflix’s capital structure and risk profile is applied alongside a perpetual growth rate of 3%, or terminal value multiple of 13x, consistent with the company’s growth trajectory. This is in line with levels the stock is currently trading at, reflective of our view that Netflix’s market valuation fairly represents its near-term fundamental prospects.

Author

Author

The Bottom Line

The tepid ramp-up of Netflix, Inc.’s paid sharing and ad-related initiatives observed in Q3 continues to temper initial optimism over the emerging growth opportunities stemming from the streaming platform’s market leadership and competitive advantage against peers from both the fundamental and market share standpoint. Netflix remains the market share leader in long-form video streaming view time, while also representing the only profitable platform at the moment. Yet the setback ensuing from the slow ramp of ad-tier subscription and ad placement sales is bringing investors back to the sidelines, as corroborated by the stock’s modest uptrend after Netflix’s solid Q3 performance.

We believe Netflix is gradually reverting back to a one step forward, two steps back story. Management has much work left to do to restore the company’s credibility as the unmatched leader in the transition to streaming – both in terms of market share growth and profitability.

Comments