Summary

- ResMed's shares have fallen 37% due to struggles with profitability and investor fears of weight loss drugs, but I believe in its long-term potential.

- The company reported a 16% increase in revenue and strong demand for its products, but margins were a concern.

- ResMed's three-pillar strategy and market outlook remain robust, and it has a solid balance sheet and healthy cash flow.

onurdongel/iStock via Getty Images

Introduction

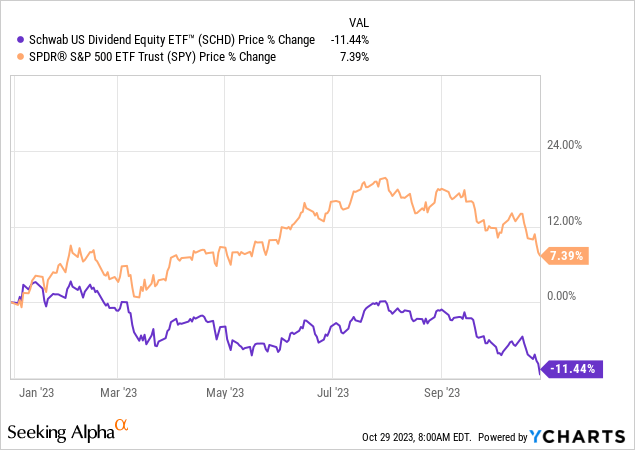

This is a very challenging year. A lot of dividend (growth) investments are under tremendous pressure from weakening economic growth, elevated rates, and sticky inflation.

Data by YCharts

Data by YCharts

Nonetheless, I'm quite happy with the way things are going, as I was able to add to some of my favorite investors and benefit from secular trends in areas like energy and defense.

Also, as buying beaten-down stocks is a key part of my strategy, I'm not complaining about some of the opportunities this market keeps giving us.

Having said that, this year, I started covering ResMed (NYSE:RMD), a highly advanced company offering tools for respiratory support and an advanced software platform that allows healthcare providers to cut down on costs and help patients more efficiently.

On July 4, I wrote an article titled Compound Your Wealth With ResMed, highlighting the aspects that would, technically speaking, provide fertile ground for long-term outperformance.

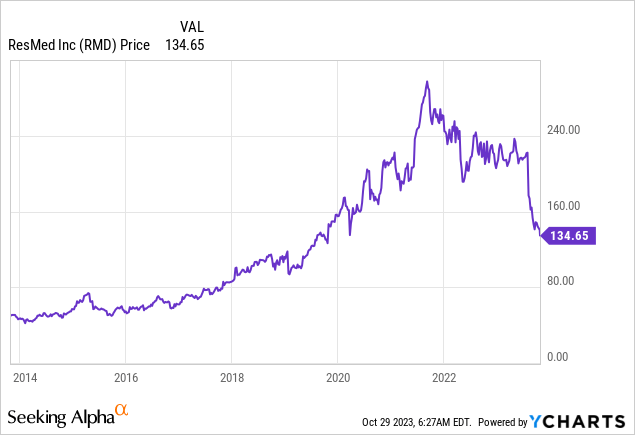

Unfortunately, since then, shares have fallen 37%, pressured by the company's struggles with profitability (margins), investors' fears of weight loss pills (so-called GLP-1s), and a general shift in sentiment on the stock market.

Data by YCharts

Data by YCharts

Shares are down 24% since my August 10 article. The total sell-off from its all-time high is 55%.

As the company just released its quarterly earnings, I get to update my bull case.

While it has been a disaster so far and one of my worst calls ever, I have to say that I still believe that RMD will generate tremendous long-term wealth.

The company's (expected) growth rates remain elevated, product innovation is going well, and it doesn't look like the company will suffer from weight loss drugs or similar headwinds.

Given the valuation, I expect shares to bottom around current prices, allowing me to expand what has been a very small starter position.

So, let's get to the details!

ResMed Remains On Track For Growth

I hope I don't have to explain that I don't write damage control articles. I am not married to my investments. I truly believe that RMD has a lot of room left for growth. If I believed otherwise, this article would have been a final goodbye to RMD.

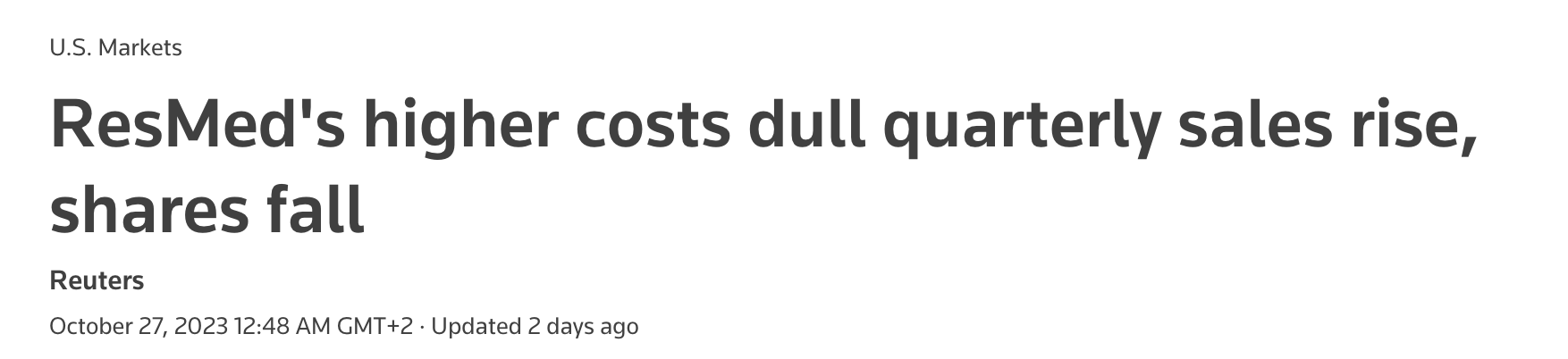

A few days ago, the company reported the first quarter earnings of the 2024 fiscal year. As the headline below suggests, it gave investors another reason to sell shares.

Reuters

As reported by Reuters, the issues continue to be margins (emphasis added):

Medical device maker ResMed reported weaker first-quarter margins on Thursday as steep costs overshadowed a 16% rise in sales, sending its shares down more than 5% in extended trading.

ResMed makes continuous-positive-airway-pressure machines ("CPAP") to treat sleep apnea, a condition where the airway gets repeatedly blocked while sleeping.

Its gross margin decreased to 54.4% from 56.9% a year earlier, pressured by higher component and manufacturing costs, among other factors.

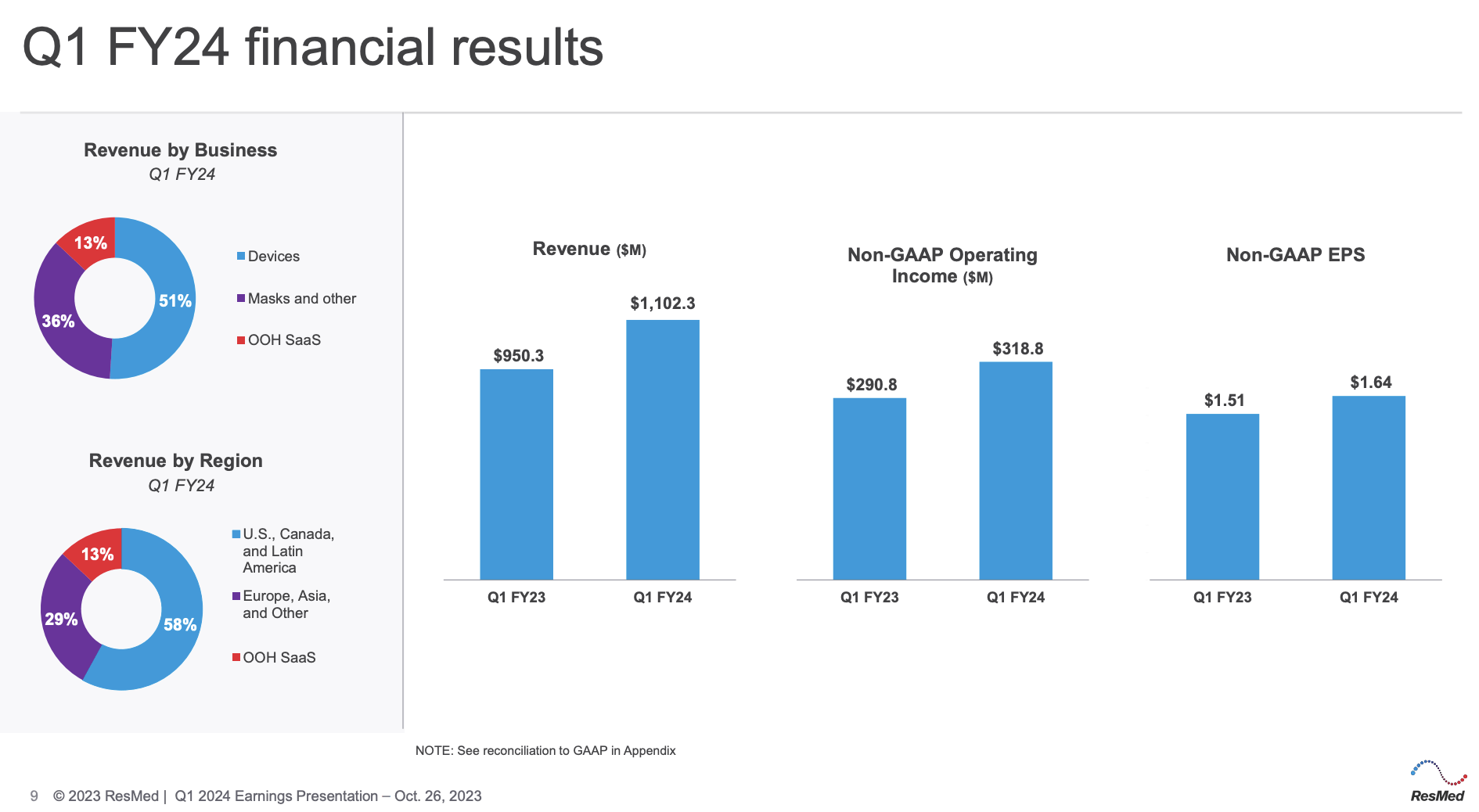

Revenue for the quarter was $1.1 billion, representing a 16% increase over the previous year.

In constant currency terms, the revenue grew by 15%.

This growth was attributed to the availability of AirSense 10 and AirSense 11 sleep devices, strong demand for mask products, and favorable foreign currency movements, which added approximately $10 million to revenue.

ResMed Inc.

Sales in the U.S., Canada, and Latin America increased by 10%, while sales in Europe, Asia, and other markets increased by 18% in constant currency terms.

- Device sales globally grew by 8%, and mask and other sales increased by 21%.

- Device sales in the U.S., Canada, and Latin America increased by 2%, while mask and other sales grew by 23%.

- In Europe, Asia, and other markets, device sales increased by 20% in constant currency terms, reflecting strong demand.

SaaS (software as a service) revenue increased by 32% in 1Q24, driven by the contribution from last year's MEDIFOX DAN acquisition and strong performance in the HME vertical.

Excluding the acquisition, SaaS revenue grew by 7%. MEDIFOX DAN contributed $25.7 million in revenue, consistent with expectations.

While these numbers are far from bad, the problem was margins. If there's anything investors hate (and rightfully so), it's poor margins ruining the top line.

Gross margin declined by 160 basis points to 56% in the quarter, primarily due to increased component and manufacturing costs.

- Operating expenses, including SG&A and R&D, increased, with SG&A expenses increasing by 15% and R&D expenses by 20% in constant currency terms.

- SG&A expenses represented 20.2% of revenue.

The company anticipates SG&A expenses to be in the range of 18% to 20% for fiscal year 2024, reflecting a recent workforce reduction of 5%, which made some headlines in the industry.

Google News

R&D expenses were 6.9% of revenue, which the company expects to be in the range of 6% to 7% for fiscal year 2024.

Operating profit increased by 10%.

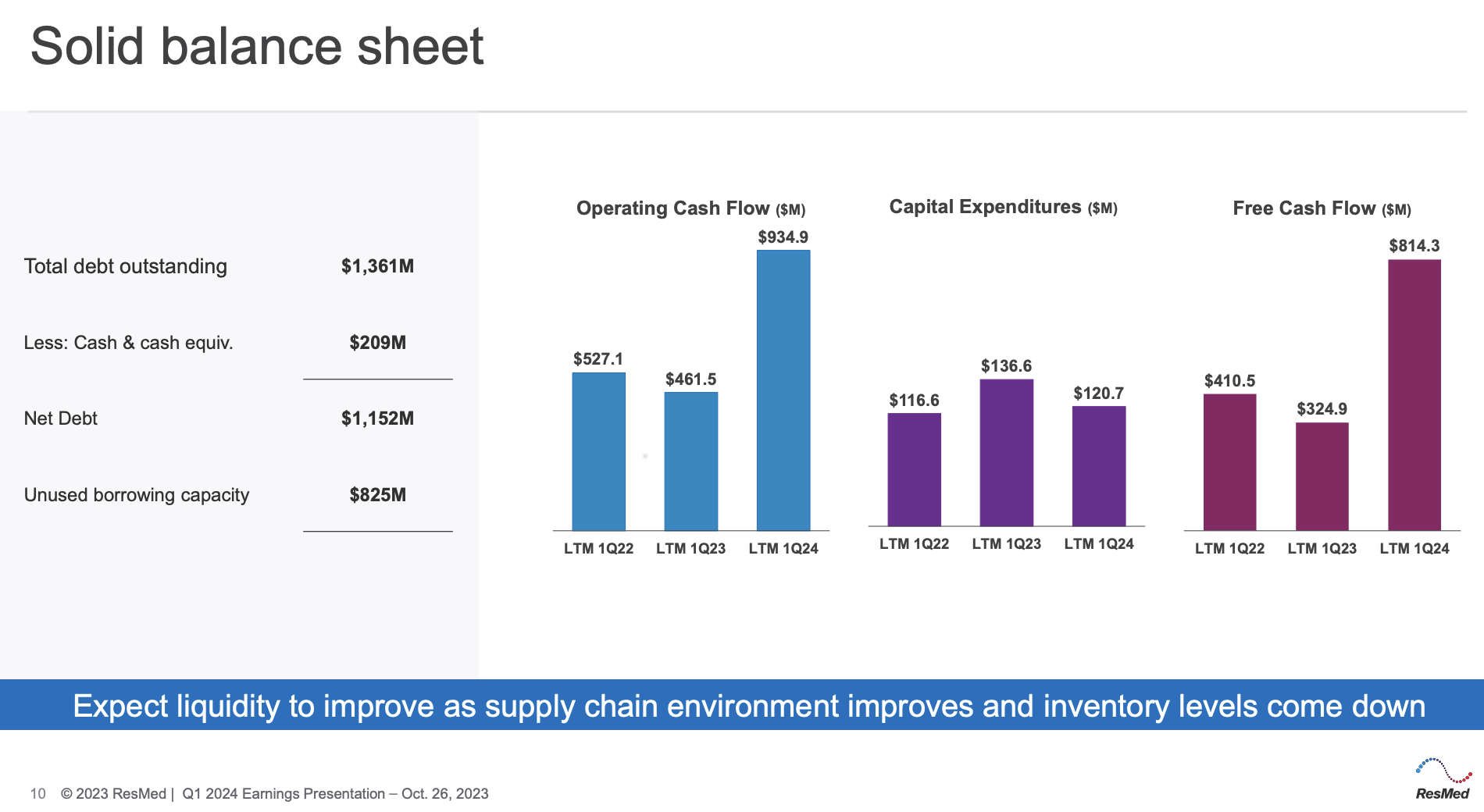

The company generated $286 million in cash flow from operations in the quarter and reduced its debt by $80 million.

ResMed ended the quarter with $209 million in cash balance, $1.4 billion in gross debt, and $1.2 billion in net debt.

In this fiscal year, the company is expected to lower net debt to just $530 million, which would translate to a sub-0.5x EBITDA leverage ratio.

ResMed Inc.

Thanks to strong free cash flow and a healthy balance sheet, shareholders remain in a good spot - at least when it comes to distributions.

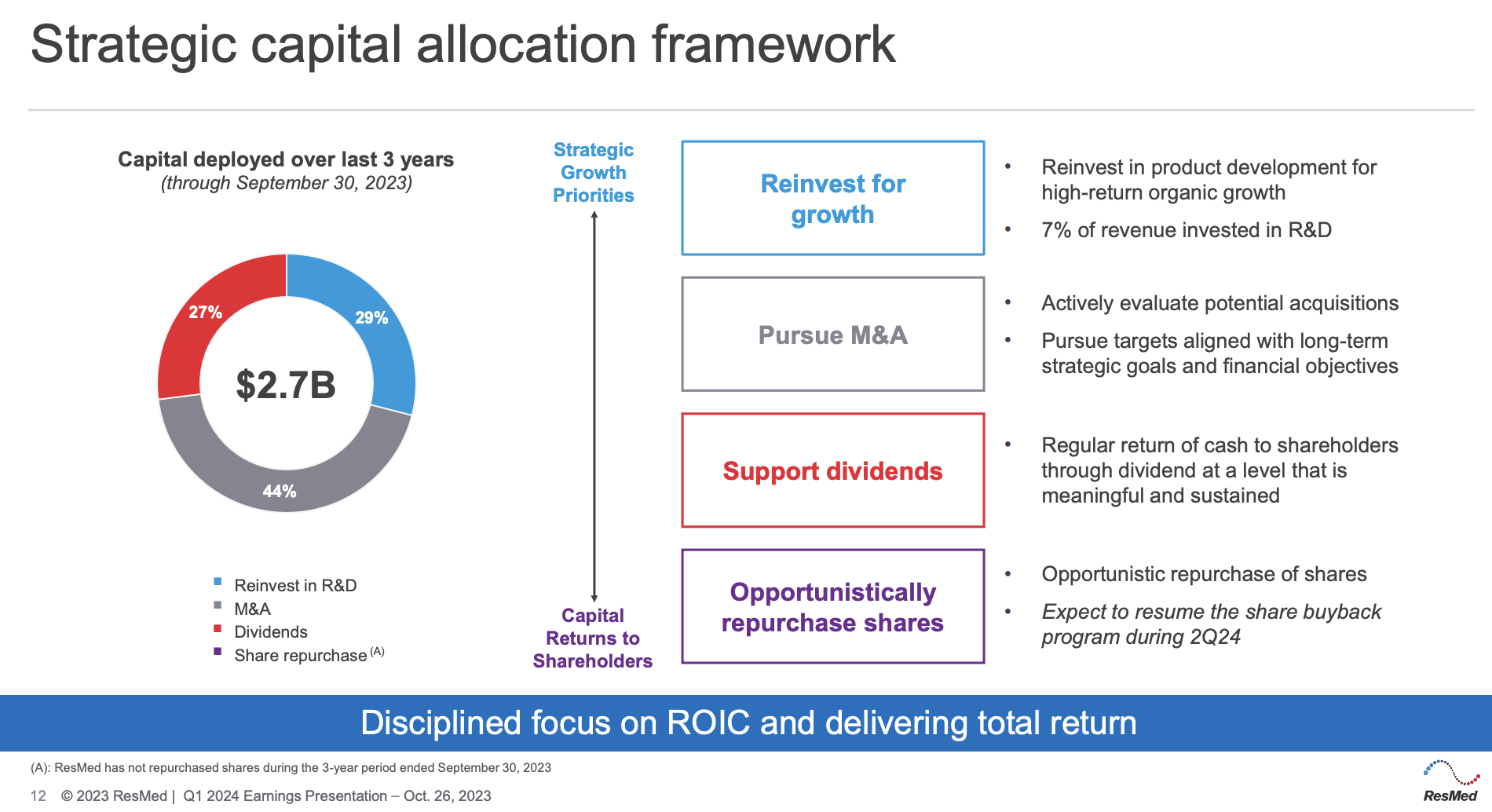

The company paid a $0.48 per share dividend in the quarter, which translates to a 1.4% yield. This is 9% above the dividend it paid earlier this year.

In addition to dividends, ResMed plans to resume its previously authorized share buyback program starting in the second quarter. The company intends to purchase shares valued at approximately $50 million per quarter.

This would translate to roughly 1% of the market cap on an annualized basis. It's not a lot, but it's a great start, as the company is still in the early phases of growing its free cash flow.

This year, for example, free cash flow is expected to almost double to $1.0 billion, which would translate to a 5.0% free cash flow yield. Next year, that number is expected to rise to $1.2 billion, paving the road for accelerated buybacks and dividends down the road - on top of potential larger M&A projects.

However, for the time being, both internal and external growth trump spending on shareholder distributions.

ResMed Inc.

With that said, let's take a look forward.

ResMed's Outlook Remains Strong

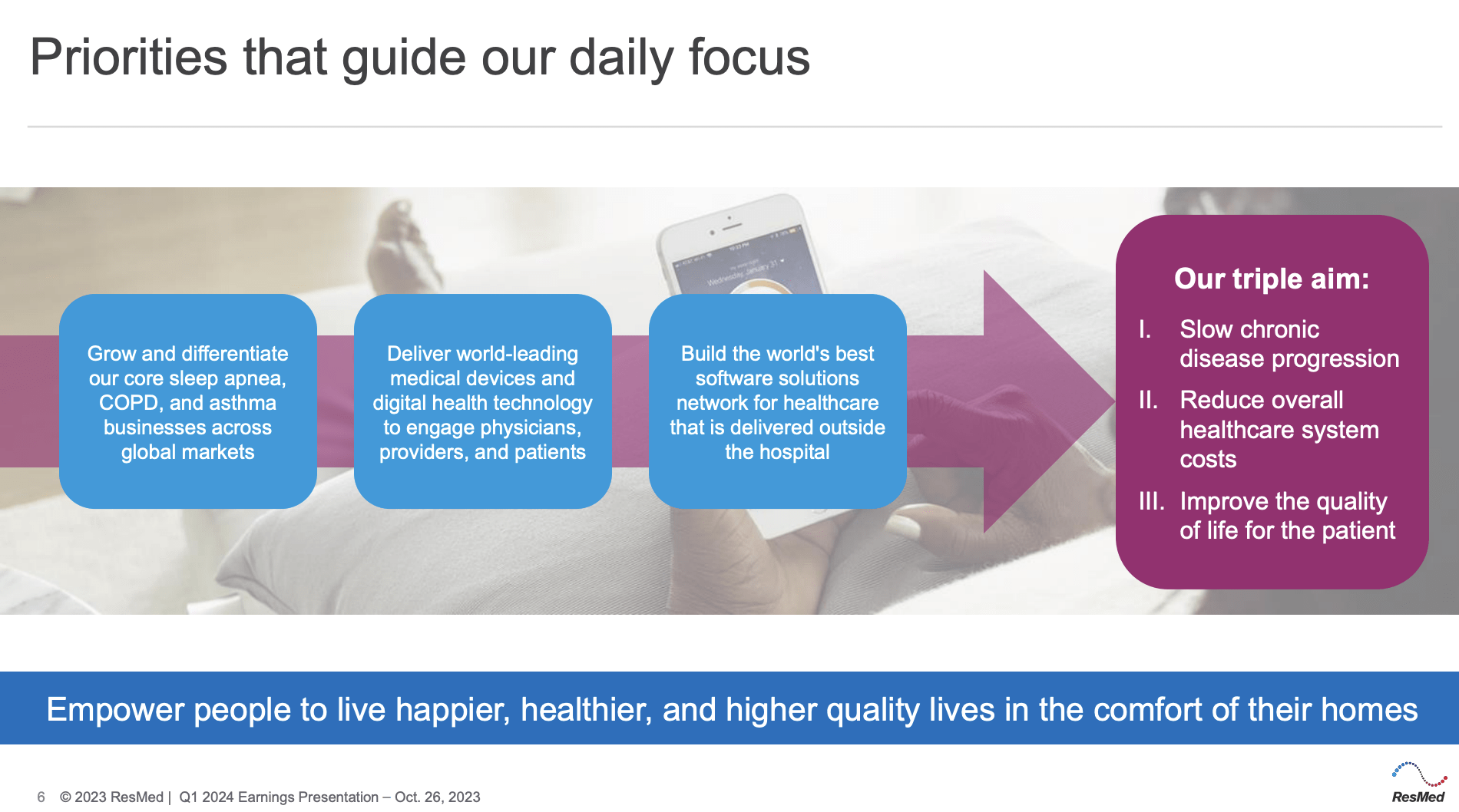

As I've discussed in prior articles, RMD is focused on a three-pillar strategy that would provide it with prolonged secular growth.

Growing and Differentiating Core Business: The company is focused on growing and differentiating its core Sleep Apnea and Respiratory Care business, with over 2 billion people worldwide suffering from related conditions. ResMed aims to deliver healthcare solutions that are cost-effective, low acuity, and comfortable, often within the patient's home. This is essentially what the company is known for. The reason it exists, so to say.

Medical Technology and Digital Health Solutions: ResMed is dedicated to designing, developing, and delivering market-leading medical technology and digital health solutions that can be scaled globally. They view the healthcare system's "outside hospital" segment as a field with tremendous potential, which they call "residential medicine." This is the reason RMD is able to grow, as it has found a new secular growth trend that goes so well with its existing platform.

Software Solutions for Care Outside the Hospital: ResMed aims to create, innovate, and grow the world's best software solutions for care delivered outside the hospital, serving as a digital concierge to guide patients in their personalized healthcare journey. While it's hard to assess who has the best strategy, SaaS has, so far, shown promising growth.

ResMed Inc.

To maintain elevated long-term growth rates, the company is actively investing in marketing and patient engagement efforts, leveraging both traditional healthcare channels and cost-effective direct-to-consumer campaigns.

These efforts aim to guide patients through the screening, diagnostic, treatment, and management pathway, acting as a digital concierge.

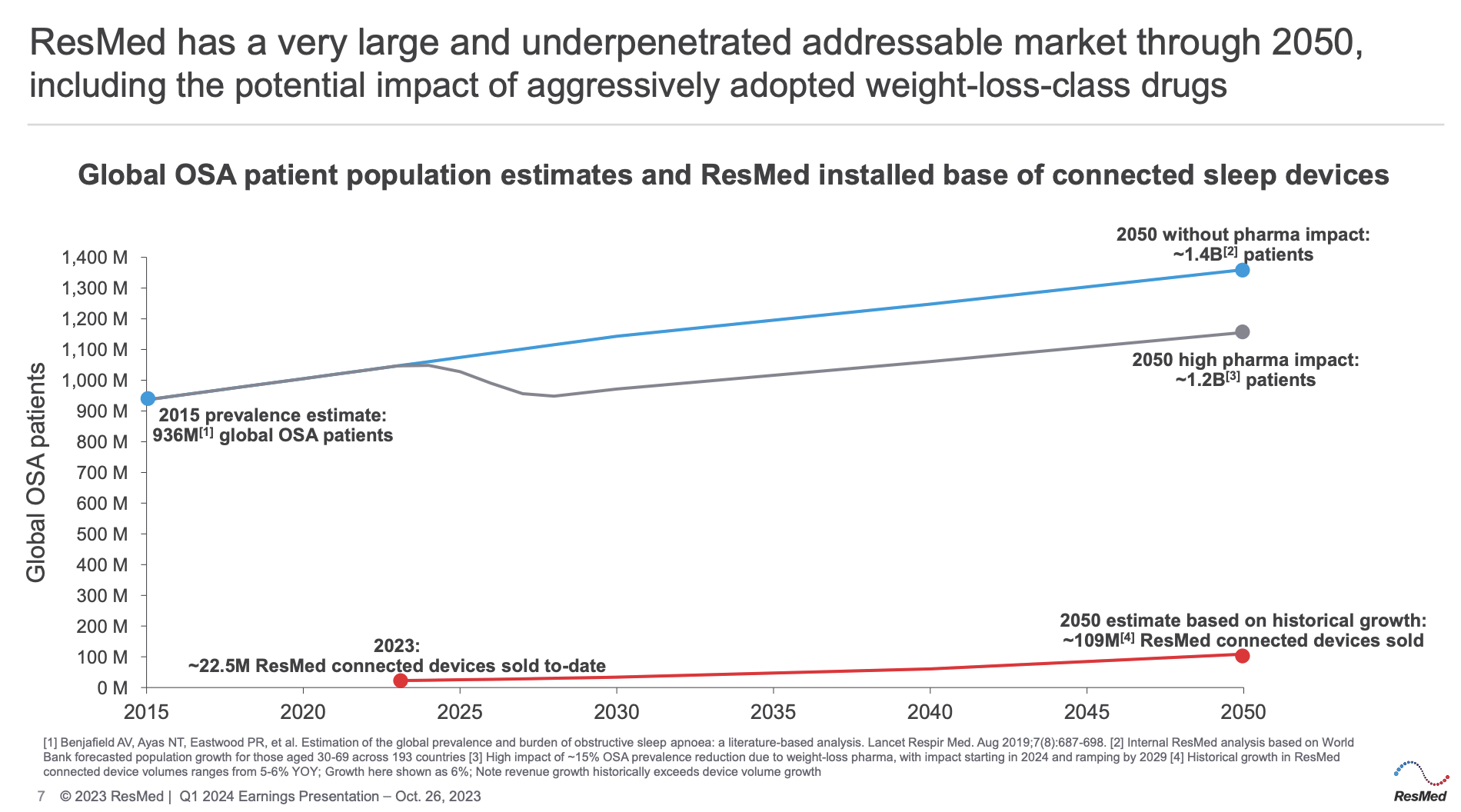

Furthermore, ResMed has developed a forward-looking epidemiology model for sleep apnea, projecting over 2-3 decades into the future. The model is based on global prevalence data, starting with 936 million people in 2015 and growing to an estimated 1.4 billion people suffering from sleep apnea in 2050.

The company has assumed aggressive market penetration for its pharmaceuticals, aiming to address a significant portion of the market.

ResMed Inc.

ResMed also forecasts market growth for their Positive Airway Pressure ("PAP") therapy, with around 109 million patients on PAP therapy by 2050.

This leaves a large addressable market for additional therapies, given that some patients do not adhere to PAP treatment.

In the first quarter, ResMed reported an all-time high in patient flow, with strong growth in patients entering the healthcare funnel.

Having said that, one major fear of investors is that weight loss drugs could derail the bull case. If people can lose weight by taking pills, it would reduce the need for respiratory support, which is a good thing for patients but not for RMD.

During the 1Q24 earnings call, the company mentioned that it is monitoring the impact of obesity drugs, specifically GLP-1 medications, on patient adherence and participation in resupply programs for sleep apnea and COPD patients.

Currently, there is no significant change in PAP adherence rates or participation in resupply programs for patients on combined therapies.

ResMed anticipates that these obesity drugs may lead to a net positive effect on patient flow and growth in sleep apnea and COPD treatment.

In other words, weight loss drugs are becoming a treatment that can be combined with RMD's products and services, benefiting RMD instead of hurting its sales.

Valuation

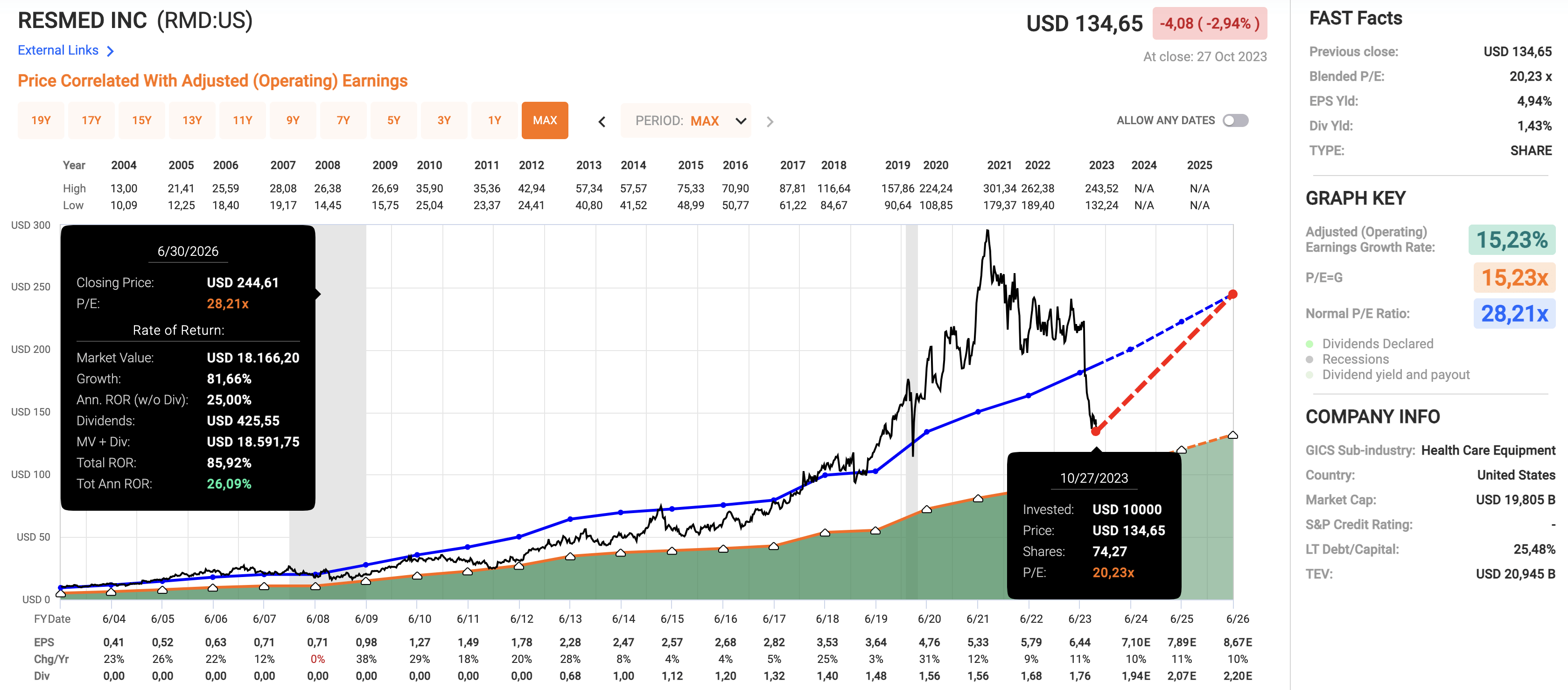

RMD is currently trading at 20.2x EPS. The long-term normal P/E ratio is 28.2x. That's the blue line in the chart below.

FAST Graphs

A return to this valuation could result in a 26% annual return through 2025, as seen in the chart above.

This is also based on a strong growth outlook.

- EPS is expected to grow by 10% this year after 11% growth in 2023.

- 2025 EPS is expected to grow by 11%.

- 2026 EPS is expected to grow by 2026.

In other words, the company is expected to maintain prolonged double-digit EPS growth, which would be in line with average non-COVID years.

- The 2024/2025/2026 average annual expected EPS growth rate is 10.4%

- Six months ago, that number was 10.9%.

In other words, despite weak headlines and GLP-1 fears, the growth outlook has barely come down while the stock was crashing!

Additionally, analysts expect the company to grow its net margin to more than 23% in 2026, which would exceed the strong pandemic years by almost 200 basis points.

This bodes very well for RMD's future and expected total returns.

When adding the strong long-term secular bull case, I stock to a Strong Buy rating.

Takeaway

Despite a 37% decline in the RMD share price since my first article, I stand by my belief that RMD holds the potential for significant long-term wealth.

The recent earnings report highlighted issues with margins, but there's a lot to be optimistic about.

RMD continues to grow with a 16% increase in revenue and strong demand for its products. Margins are a concern, but they're actively addressing this and poised to achieve record margins in the years ahead.

The company's solid balance sheet and healthy cash flow promise shareholder-friendly moves in the future.

Furthermore, RMD's three-pillar strategy points toward sustained growth, and its market outlook remains robust. Despite concerns about weight loss drugs impacting the business, it seems RMD can adapt and even benefit from this trend.

With an attractive valuation, strong growth forecasts, and solid margins, I maintain a Strong Buy rating on ResMed.

This journey may have had its ups and downs, but the long-term potential is too compelling to ignore.

I hold a very small position in RMD and will likely expand it going forward.

Comments