Summary

- Ford Motor Company stock has declined by about 10% since the UAW strike began, trading at around $11.

- Despite the tentative agreement reached with the UAW earlier this week, Ford stock slid further, highlighting the impact of Ford's disappointing EV outlook coming out of the Q3 earnings release.

- Increasingly clouded visibility on Ford's EV strategy and ongoing UAW risks are likely to keep pressuring the stock's performance ahead.

Vera Tikhonova

Ford Motor Company (NYSE:F) stock has been on a steady decline since the United Auto Workers ("UAW") strike began on September 14, erasing close to 10% of its market value over the same period. The stock now trades at about $11, despite having reached a tentative deal with the UAW. This is in line with our previously discussed predictions relevant to the potential implications of UAW-related near- and longer-term costs, which include current volume impacts and incremental pressure on Ford’s margin expansion roadmap as the new wage contract takes place over the next four years.

Combined with the mixed outlook on Ford’s electric vehicle ("EV") strategy coming out of the latest Q3 earnings disappointment, which follows a substantial drop in F-150 Lightning volumes due to previously scheduled facility upgrades during the summer, the stock’s post-earnings performance in late trading remains pressured. Meanwhile, Ford Pro remains a spotlight, offsetting the weak EV progress and ongoing UAW risk overhang which has caused management to withdraw the company’s full-year guidance. While the eventual finalization of the UAW agreement could drive an incremental valuation uplift, the relevant upside potential faces increasing risks of being hindered by stiffening headwinds to Ford’s capital-intensive EV roadmap. Taken together, we are remaining on the sidelines in the stock, as we believe its current market value is fairly reflective of the underlying business’ near-term prospects given the overhanging risks.

UAW Strike Update

The UAW has been on a partial strike across Detroit’s three largest automakers (“D3”), including Ford, since September 14 after the once-every-four-years contract negotiations fell through without an agreement. Under a newly implemented “phased out” strike strategy that impacts the D3’s operations simultaneously, the UAW walkouts ordered to date have impacted three of Ford’s plants. They include the Michigan Assembly during the beginning of the strike, followed by the Chicago Assembly and the Kentucky Truck Plant earlier this month, impacting builds of the Ranger, Bronco, Explorer, Lincoln Aviator, Lincoln Navigator, and some of Ford’s Super Duty Trucks; the best-selling F-Series trucks remain spared from disruption.

More than 34,000 of about 146,000 UAW members have joined the picket line since the strikes started, underscoring risks of a prolonged dispute as negotiations continue. In response, Ford has also let go of more than 3,000 employees across the affected facilities due to the “knock-on effect” of the strike. Earlier this month, Ford had upped its wage increase offer from the previous 20% to 23%, which still trailed the UAW’s adjusted demand for as much as a 36% pay raise from the initial 46% target. UAW leader Shawn Fain had cited “there is more to be won” in his latest weekly live video update, though also signaling some light at the end of the tunnel in the union’s relentless fight. And in the latest development, Ford has stricken a tentative deal with the UAW, agreeing to a 25% pay bump in the contract that dictates union worker wages over the next four years.

In its latest earnings update, Ford specified that the company has incurred $1.3 billion in UAW costs to date, with current relevant expenses representing about a $200 million weekly run-rate. Incorporating these incremental costs to our fundamental forecast, resulting EBIT remains within the management’s previous $11 billion to $12 billion guidance on the lower end. This suggests the near-term UAW strike related costs have remained manageable. However, implications of strike-related impacts in recent weeks on production volumes could linger in the near-term, as it will take time to re-ramp productions at the affected Michigan, Chicago and Kentucky assemblies and make up for previously lost output. Meanwhile, the longer-term margin implications from the resulting pay bump likely remains a headwind to Ford’s growth plans, particularly for its capital-intensive EV strategy.

Near-Term Strike Impact on Volumes and Costs

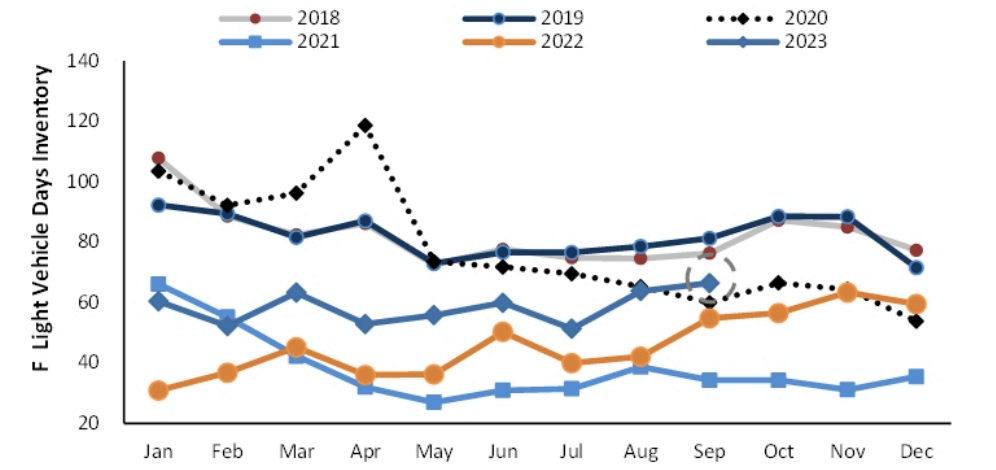

In addition to the current UAW costs at the ~$200 million weekly run-rate, an extended strike could further disrupt Ford’s output volumes. Ford is currently waiting for the UAW to vote on the tentative agreement on October 29, and even if it passes smoothly and productions resume at the affected plans then, volumes will likely continue to be impacted by ramp-related challenges. The company currently has about 66 days’ inventory. Although gradually improving from about 58 days during the summer and historical lows in 2021 / 2022, the metric continues to trail Ford’s historical average of 70 to 80 days’ inventory prior to the pandemic. And the ongoing UAW strike has only heightened derailment risks to recent progress made.

Motor Intelligence

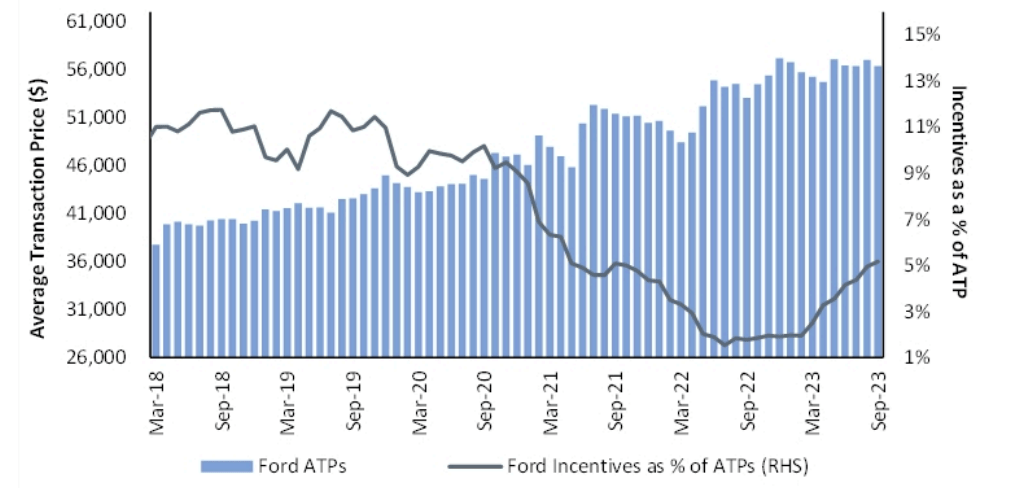

Meanwhile, the company has also reported a stabilizing average transaction price (“ATP”) of about $55,000 through the third quarter, which remains well above industry’s average of about $47,899. Although any ensuing volume impact from the latest UAW strike could improve Ford’s pricing power, any sort of relevant remedy could potentially backfire given the mixed consumer spending backdrop amidst tightening financial conditions. This is already corroborated by the rapid increase in sales incentives offered at Ford. Specifically, the company now offers sales incentives at more than 5% of its ATP, surging rapidly from 2% just eight months ago. A similar upsurge is observed in the broader industry, underscoring normalization in the demand environment as years of supply constraints start to ease, which could be exacerbated by implications of the slowing economy.

Kelley Blue Book and Motor Intelligence

In the unlikely event that the UAW turns down the tentative deal, which has captain Fain’s support, in the upcoming ratification, an extended strike could eventually hit Ford’s best-selling and most profitable vehicles, including the F-Series pick-up trucks. The resulting implication could be much more adverse relative to the impact from current disruptions over some of Ford’s less popular models, which remains well absorbed by existing inventory levels. However, an extension of the UAW strike to the production facilities of Ford’s best-selling models would also likely represent the last and strongest lever for the union, indicating light at the end of the tunnel and limit the relevant impact on the automaker’s near-term bottom-line.

Longer-Term Pay Bump Impact on Profitability

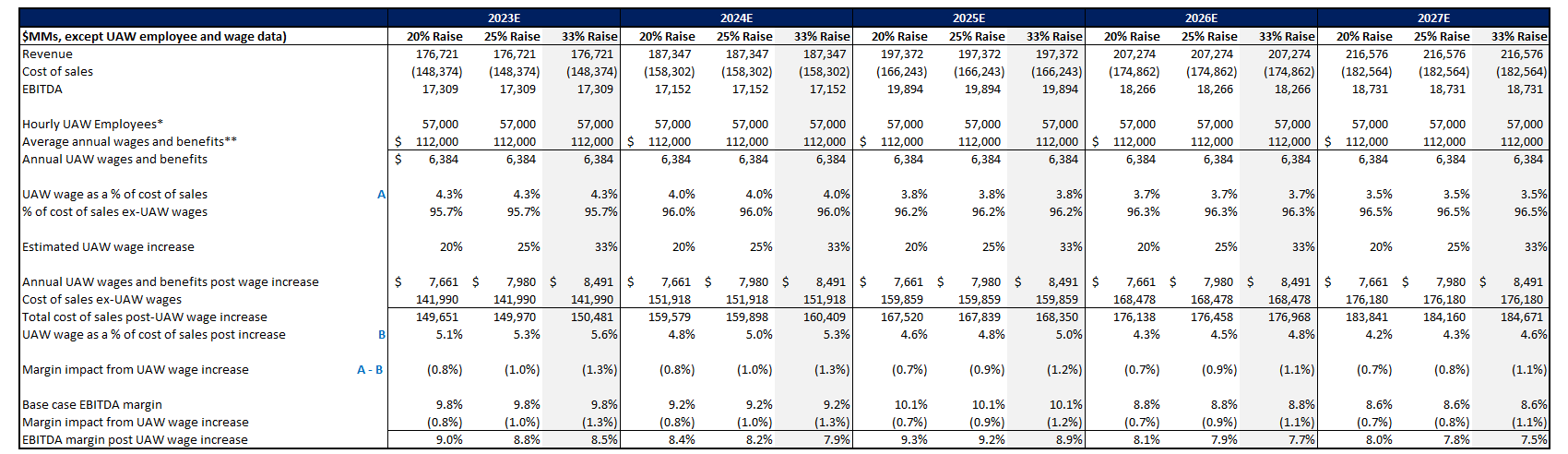

Instead, the longer-term implications of the upcoming pay bump is of greater concern. In order to gauge the potential implication of a 25% pay raise based on the latest tentative agreement, we have performed a sensitivity analysis on the updated fundamental forecast for Ford’s actual Q3 results and forward prospects considering management’s latest commentary.

Our updated base case forecast for Ford expects revenue to expand at a 4.2% five-year CAGR. The assumption is driven primarily by Ford Pro (+7.7% five-year CAGR) in line with the segment’s strength in recent quarters and market leadership, as well as Ford Model E (+9.5% five-year CAGR) consistent with the company’s growth roadmap, and offset by modest expansion at Ford Blue and Ford Credit considering their stabilizing market share.

Author

We estimate combined EBITDA margins average 9% over the forecast period, which builds on management’s expectations for stable EBIT contributions from Ford Blue over the longer-term to drive Ford Pro’s path to 14% EBIT and Model E’s path to 8% EBIT by 2026.

Author

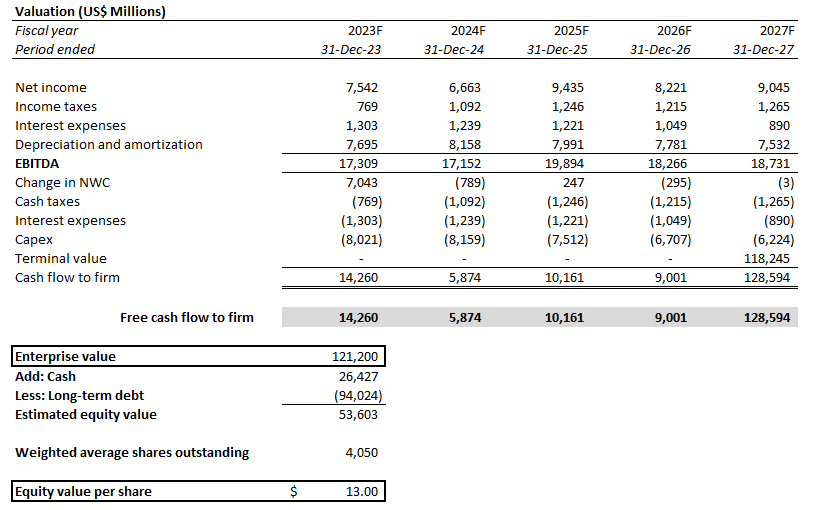

Ford_-_Forecasted_Financial_Information.pdf.

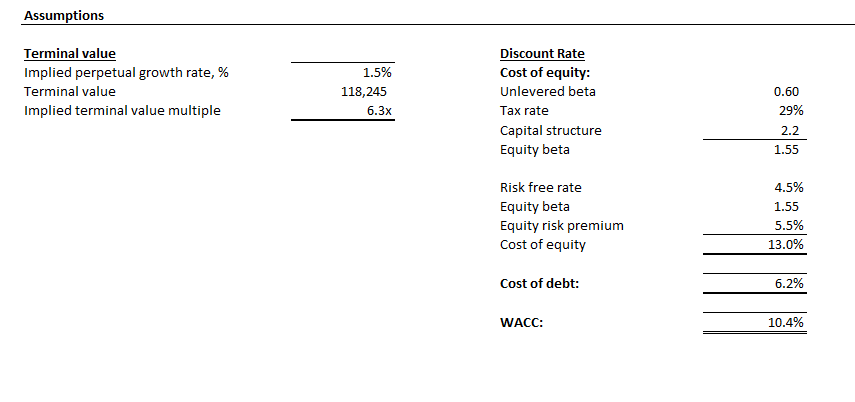

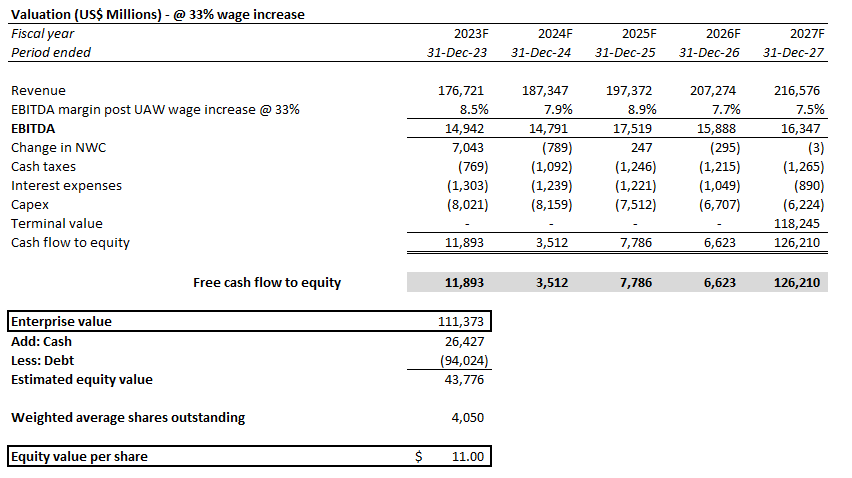

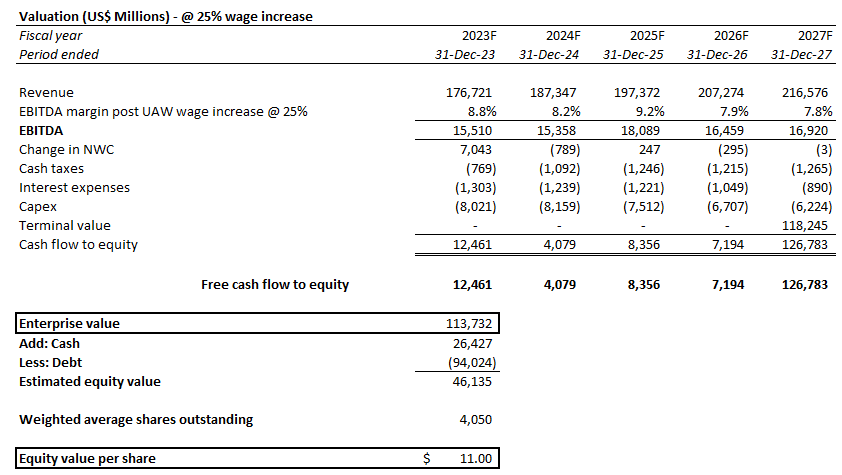

By applying a 10.4% WACC and 1.5% perpetual growth rate to projected cash flows, adjusted for the company’s net debt profile, Ford stock has an estimated intrinsic value of $13 per share. The discount rate applied takes into considering Ford’s capital structure (including capital attributable to Ford Credit) and its risk profile relative to currently elevated benchmark Treasury yields. Meanwhile, the estimated perpetual growth rate applied reflects Ford’s maturing growth trajectory, with its EV roadmap expected to eventually displace its market leadership in legacy auto sales in the longer-term rather than being a significant accretive factor to top line expansion.

Author

Author

By holding all key fundamental growth assumptions unchanged from our updated base case estimates, and only sensitizing Ford’s cost structure based on the estimated UAW wage increase of 25% through 2027, we isolate the estimated impact of the impending pay bump on the company’s profitability and valuation prospects. Specifically, the 25% pay bump over the next four years, paired with the resumption of cost-of-living allowances (“COLA”), is expected to drive the top wage rate increase to 33%.

By applying the estimated 25% to 33% range of impending wage increases to our updated fundamental forecast based on the same methodology discussed in our previous coverage, the upcoming UAW contract is expected to drive an average of 90 bps to 120 bps headwind to Ford’s EBITDA margins through 2027.

Author

The relevant discounted cash flow, or DCF, analyses on the sensitized fundamentals based on the impending UAW wage increase, while holding all base case valuation assumptions (10.4% WACC; 1.5% perpetual growth rate) unchanged, suggests a downside scenario equity value of about $11 apiece, in line with our previous projections.

Author

Author

This indicates that the headwinds relevant to the ongoing UAW negotiations may have already been priced into the stock at current levels.

Mixed EV Outlook

While the anticipated implications of the latest round of UAW contract negotiations may have already be priced in, the increasingly mixed outlook on Ford’s EV strategy represents another emerging headwind. Declines in F-150 Lightning volumes during Q3 due to pre-scheduled facility expansion work has already dealt a further setback to the stock earlier this month following a consistent slew of negative headlines over Ford’s EV strategy.

The F-150 Lightning has already succumbed to an ongoing price war launched by EV titan Tesla (TSLA), with Ford cutting the F-150 Lightning’s MSRP by as much as 17% this year. While these price cuts have “helped drive a sixfold increase in orders and threefold increase in web traffic,” F-150 Lightning sales currently represent only about 2% of total F-Series deliveries. This highlights the lack of a previously anticipated first-mover advantage in Ford’s electric pick-up truck sales over the past 18 months since the F-150 Lightning’s launch. Since the F-150 Lightning assembly plant in Dearborn resumed productions following its six-week shutdown over the summer for capacity expansion, output volumes have also been withheld by the company, with management citing “unspecified quality reasons.” Meanwhile, management has also renewed their support for hybrid vehicle sales, which defy previous confidence and optimism over fully electrifying Ford’s slate as part of the longer-term Ford+ growth plan.

Taken together, Ford’s EV strategy remains a “one step forward, two steps back” narrative, with increasingly clouded visibility into the longer-term demand for its electric models. This is also in line with close rival General Motors' (GM) recent caution over the ongoing uncertainties in its EV demand outlook, given the automaker’s limited production volume relative to key industry competitors like Tesla. The company-specific and industry trend underscores continued risks of elevated capital outlay and losses from the transition to EVs. This setup bodes unfavorably with ongoing margin headwinds at Ford Blue due to the UAW strike and ensuing cost pressures, in addition to implications from broader macroeconomic challenges in the near-term.

Ford Pro Spotlight

Meanwhile, Ford Pro remains a spotlight at the automaker. Ford Pro revenue grew 15% y/y to $13.8 billion during the third quarter, continuing a trend of robust growth. This has supported a segment EBIT of $1.7 billion in Q3 (12% EBIT margin), which represents 77% of Ford’s consolidated EBIT during the period.

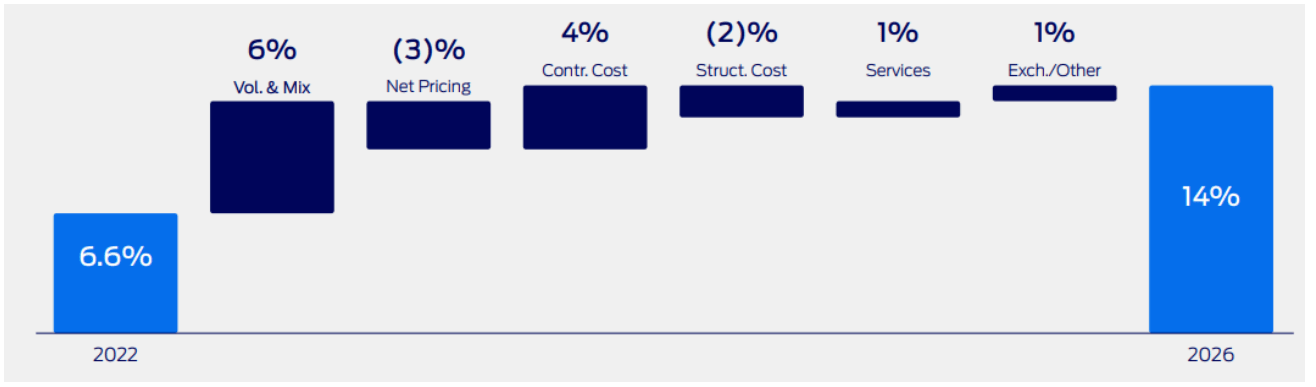

The latest results continue to corroborate solid market share gains in the commercial segment, reinforcing its leadership across the U.S. and Europe. Specifically, Ford Pro currently commands more than 40% of the U.S. “class 1-7 full-side truck and van market,” which is more than double the share of market’s runner-up. And the continued delivery ramp-up on the newest Super Duty trucks in the U.S. is likely to further complement the gradual market share gains, in line with the two-point increase from 41% in Q2 to 43% in Q3. In Europe, Ford Pro also leads the commercial van market with 15% market share, with further momentum expected through the year with the ramp of an “all-new version of the Transit Custom van.” Paired with robust paid software subscription growth to almost 600,000 subscribers at the end of the third quarter, with Ford Pro accounting for about 80%, the segment remains well on track towards its longer-term sustained EBIT target of 14% by 2026 from 6.6% in 2022.

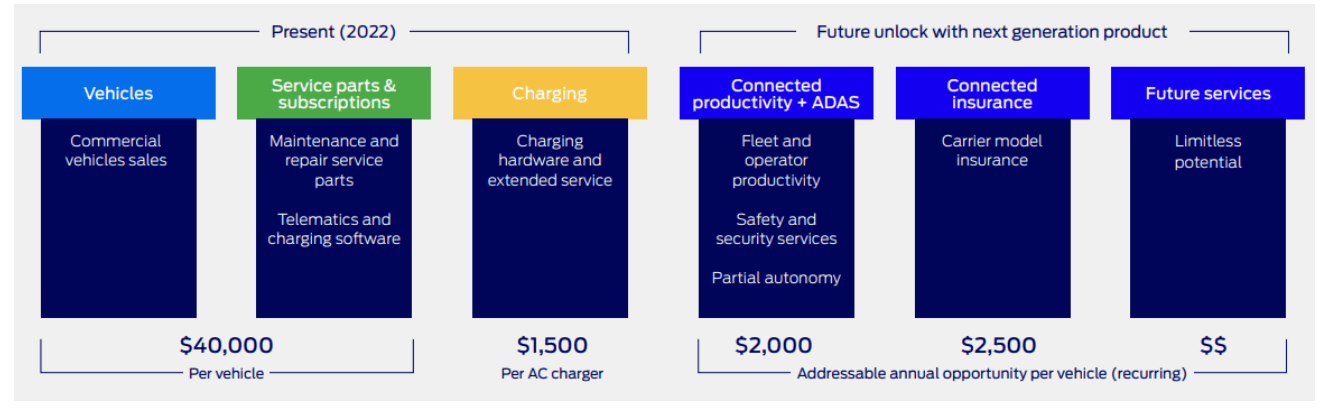

Specifically, the improvements to Ford Pro vehicle and subscription sales in recent quarters continue to highlight strength in some of the key drivers cited by management for the segment’s EBIT growth trajectory. This includes $6,000 in incremental margin opportunities per vehicle stemming from value-add services such as charging hardware and service sales (~$1,500 per vehicle) with the gradual introduction of electric vans, as well as the ramp-up of connected productivity / ADAS ($2,000) and Ford Pro connected insurance ($2,500) subscriptions.

shareholder.ford.com

The consistent string of robust results at Ford Pro remain corroborative of its capability in monetizing the relevant incremental revenue opportunities, which are key contributors to the substantial volume/mix component in Ford Pro’s projected EBIT bridge.

shareholder.ford.com

Final Thoughts

Ford stock continues to underperform the broader market this year, as its underlying business reels from a capital-intensive electrification strategy amid tightening credit conditions with limited visibility into longer-term demand. There are also lingering concerns over the broader impact of intensifying industry competition, as well as the broader impact of a softening consumer spending backdrop.

More importantly, the latest UAW negotiations continue to brew into a bigger problem than management had previously expected as well. Ford’s latest 25% wage increase offer, which translates to a 33% top wage rate with COLA, is substantially up from the initial 20% that was likely factored into its initial guidance and previous business growth plans. Note that the union still has multiple levers up its sleeve to get the 36% pay bump they had previously desired, ranging from the expansion of strikes at Ford’s highest-demand vehicle production facilities, to a durable strike fund thanks to the novel walk-out strategy implemented. With the final decision still pending from the UAW, risks of an extended strike remain, which should not be overlooked as it could potentially continue to weigh on the stock’s near-term performance.

Although Ford stock now trades at our worst-case scenario price in the $11 range, which implies upside potential when the eventual UAW deal is reached and complement consistent growth and EBIT strength at Ford Pro, related optimism could potentially be dulled by the emerging challenges to the company’s capital-intensive EV roadmap. Taken together, we remain incrementally cautious on Ford Motor Company stock near-term prospects from current levels.

Comments