Summary

- Amazon.com, Inc. stock has underperformed the broader markets over the past month, reflecting investor wariness over the mixed consumer spending backdrop.

- Yet another consecutive quarter of robust outperformance underscores recovering strength in its e-commerce and AWS moats, which support continued margin expansion at scale alongside implementation of broader cost-savings initiatives.

- With the stock still trading trailing its historical and the mega-cap Internet peer group average, fundamental strength backed by AI monetization at AWS and fulfilment efficiencies underscores further upside potential.

FinkAvenue

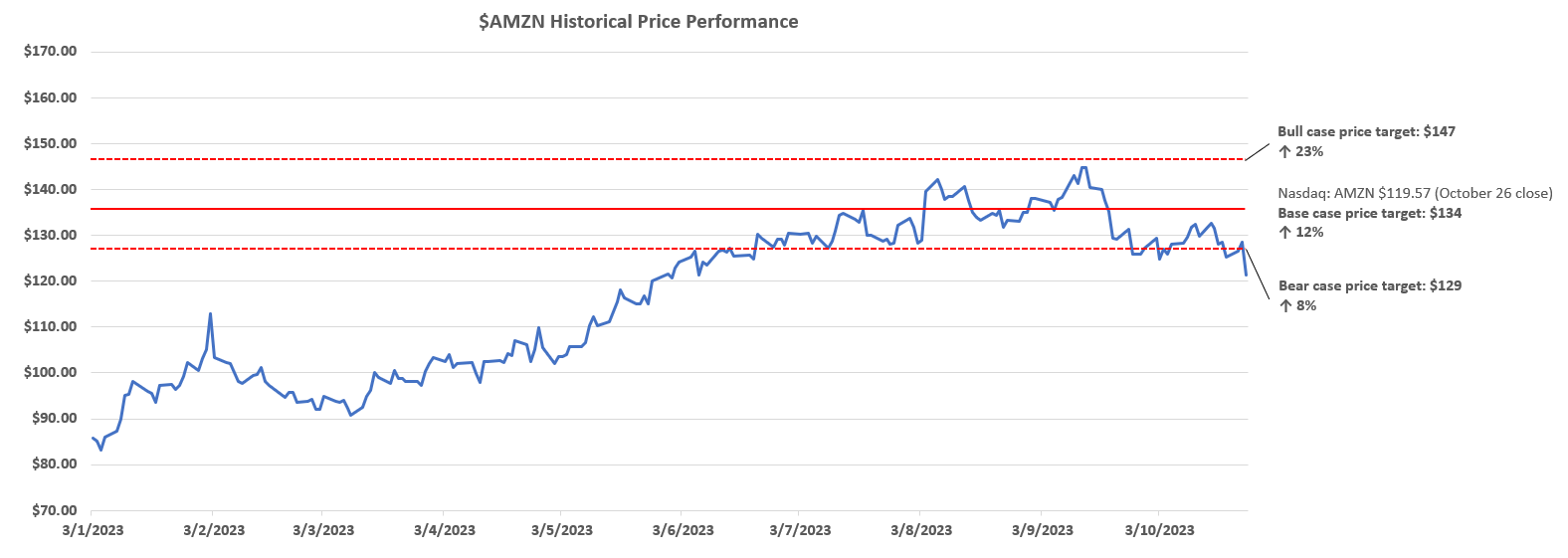

Amazon.com, Inc. (NASDAQ:AMZN) stock has underperformed broader markets over the past month. Declines are nearing 8% over the past month, relative to the ~4% drop observed over the same period in the S&P 500 (SP500) and ~4% drop in the tech-heavy Nasdaq 100 (NDX). The stock’s recent weakness continues to reflect investors’ growing wariness over the e-commerce giant’s exposure to the mixed consumer spending backdrop as the Fed reiterates needs for further tightening of financial conditions to tame the overheated economy and keep inflationary pressures in check.

However, the company’s Q3 blockbuster outperformance across both its core e-commerce and Amazon Web Services (“AWS”) cloud-computing segments have caused the shares to rise in post-earnings late trading. Specifically, AWS stabilization after seven consecutive quarters of weakness amidst persistent industry optimization headwinds and broader macroeconomic challenges, alongside substantial margin expansion, were a bright spot. They were indicative of progress in the segment’s AI strategy, providing reinforcement to AWS’ market leadership against rising concerns of potential share loss to rivals. Meanwhile, Amazon’s core U.S. e-commerce business also maintained margin expansion from Q2, highlighting the continued realization of efficiencies in its recently revamped “regionalization” fulfilment strategy.

Looking ahead, Q3 outperformance underscores the return of an idiosyncratic value proposition from Amazon to the consumer that could safeguard the company’s resilience against a still mixed macroeconomic backdrop. This is expected to be complementary to seasonal tailwinds for the e-commerce segment heading into Q4, and reinforce Amazon’s second half weighted growth story. Meanwhile, sequential AWS reacceleration and AI deployment ramp, alongside continued market share gains in retail media advertising also bolsters the company’s pace of consistent margin expansion. Taken together, Amazon stock remains well-positioned to weather through the near-term macroeconomic impact on both its fundamental and valuation outlook from current levels.

Restoring Its E-Commerce Moat

Amazon’s online store and third-party (“3P”) seller service revenues grew 7% and 20% y/y, respectively. Strength was prevalent across both of Amazon’s North America and International businesses, likely reflective of continued progress in ramping up the recently regionalized fulfilment strategy in the U.S. and realizing broader efficiencies implemented across its global portfolio. Specifically, North America revenue grew 11.5% y/y, accelerating from the prior quarter, with operating margins expanding another percentage point sequentially to 5% in Q3. Improvements in Amazon’s key e-commerce components underscore resilience relative to weakness in the global consumer spending backdrop.

Bloomberg News

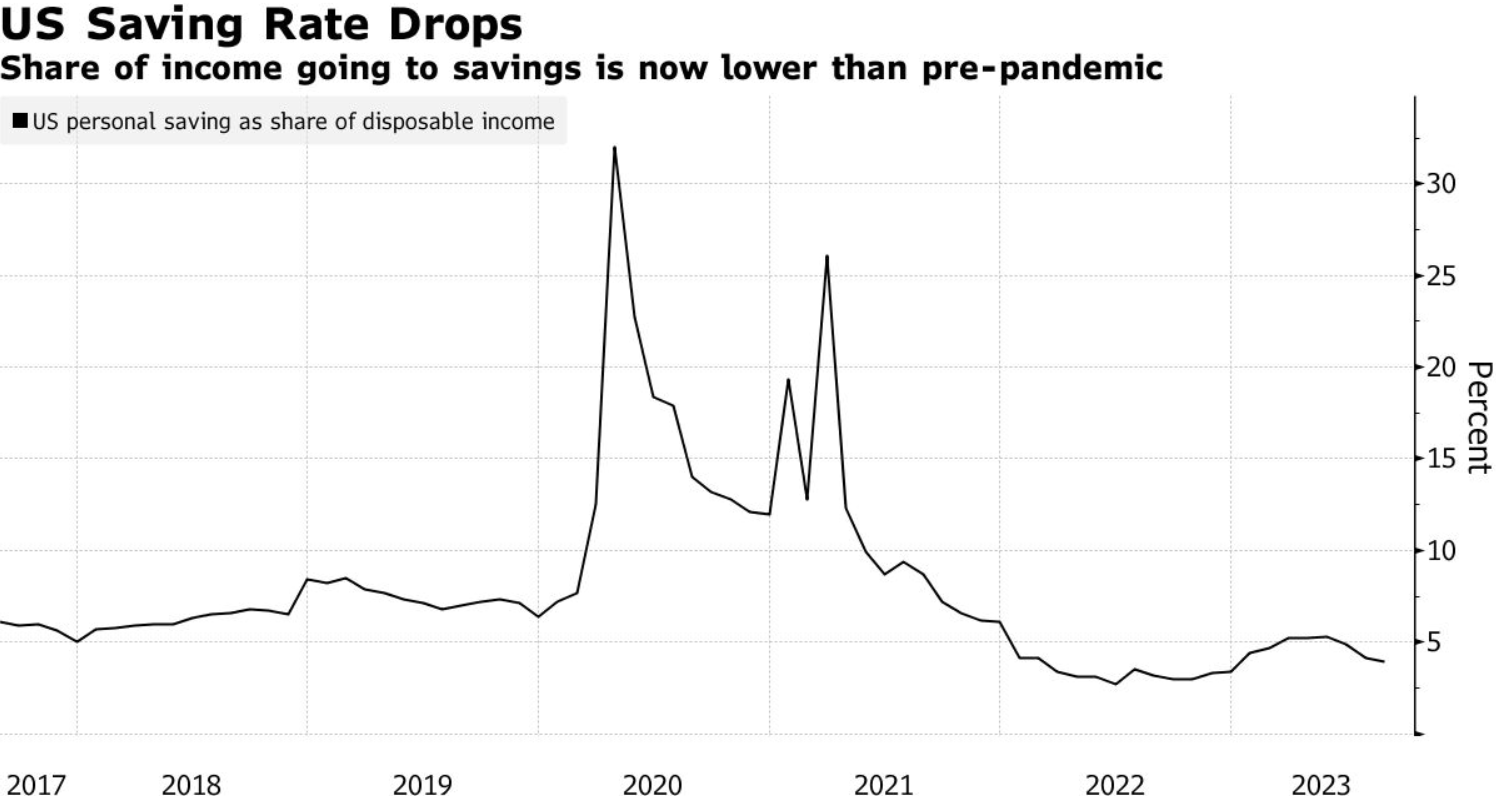

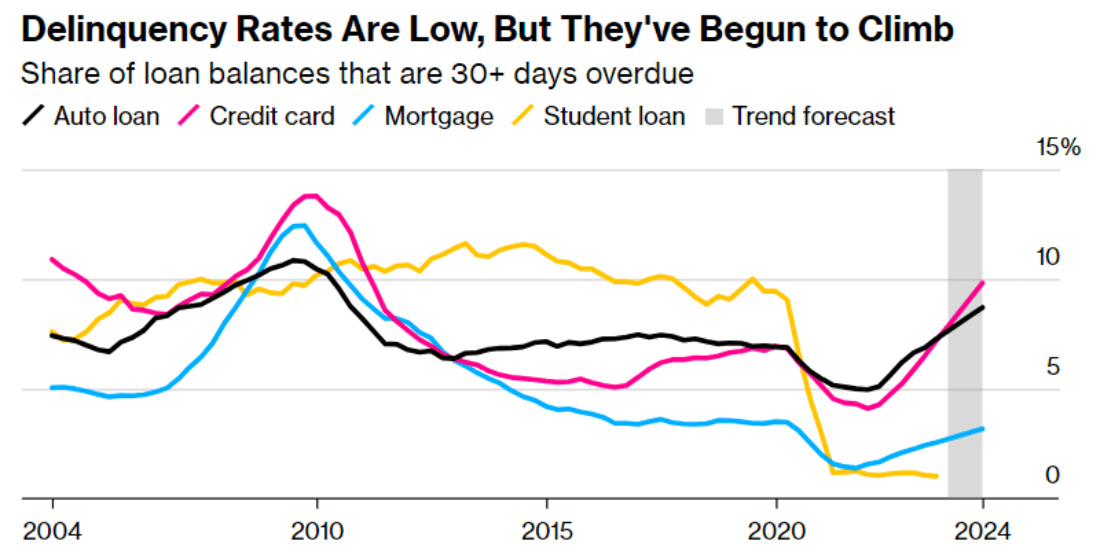

Specifically, at home in the U.S., consumers face the combination of deteriorating household income and savings. Meanwhile, household debt is also ballooning at the same time when interest rates are climbing towards all-time highs. Credit card delinquencies are also surging above pre-pandemic levels, while the resumption of student loan repayments this month is likely to weigh further on consumer discretionary spending.

Bloomberg News

The impact of tightening financial conditions in the economy on consumer spending is further corroborated by recent deceleration in U.S. retail sales. Although Q3 non-store – or e-commerce – sales grew by 8.2% y/y, slightly accelerating from 7.9% in Q2, they have been in consistent deceleration on a monthly basis over the same period. September non-store sales grew by only 6.2% y/y, slowing from “8.4% in August and 10.2% in July.”

Yet Amazon’s solid e-commerce performance in Q3 highlights the value proposition of both its e-commerce marketplace and Prime member benefits offered to consumers worldwide, especially as their sensitivity to price changes increase amid tightening financial conditions. Specifically, more than 60% of consumers are on the hunt for discounts heading into the holiday shopping season, as they look to “spend the least amount of money possible.” Increased consumer price sensitivity is further corroborated by the robust showing at Amazon’s two-day Prime Big Deal Days shopping event earlier this month. Customers spent $144.53 on average on Amazon.com during the two-day sale. Albeit just a modest 2% increase from the average spending per customer during last year’s Prime Big Deal Days event, the results still outperform the broader industry’s by three points – competing retailers running similar discounts during the two-day shopping event saw sales decline by 1% y/y. Amazon also reported particular strength in demand for discretionary goods during the two-day sale, with “apparel, beauty, home, and toys among the best-selling categories.”

In order to retain demand, Amazon has also been making progress in scaling the deployment of its revamped fulfilment strategy in the U.S. in order to improve customers’ shopping experience and improve the value proposition of its Prime membership subscriptions. The company reported a record 54-minute time from order to delivery during the first day of the Prime Big Deal Days sale earlier this month, while also delivering “hundreds of thousands of items within four hours of purchase” through the course of the two-day event.

The newly introduced regionalization fulfilment strategy also complements the e-commerce arm’s cost structure, ridding its adverse reputation for underutilization when CEO Andy Jassy stepped into his role at the helm during the peak of the pandemic. The ensuing trend of margin expansion with scale is expected to be complemented by the recent implementation of AI and robotics to improve the fulfilment process from inventory management to deliveries.

Specifically, Amazon has implemented “AI-equipped sortation machines” and a proprietary “Sequoia” robotic system at its Houston facility earlier this month. The full-scale roll-out of relevant innovations across its fulfilment capacity is expected to reduce the time from order to delivery by as much as 25%, improve inventory management efficiencies by up to 75%, and enable a safer workplace for warehouse employees. While the ensuing efficiencies might imply further cost-savings from headcount consolidation, we are more optimistic on the relevant improvements to the profit margins of 3P seller service – particularly Fulfilment by Amazon (“FBA”) – revenues. The combination of faster order processing and delivery times, and improved inventory management capabilities are likely to improve FBA’s appeal to merchants, while also complementing the consumer shopping experiences to retain end-market demand.

AWS Stabilization

Stabilization in AWS growth in Q3, following seven consecutive quarters of preceding deceleration, was a highlight of Amazon’s latest earnings results. Specifically, AWS revenue grew 12% y/y and 4% q/q to $23 billion during Q3, while the segment’s operating margin also improved by a whopping six percentage points from Q2 to 30%, nearing the all-time highs. The results have largely alleviated some of investors’ wariness of market share loss, especially given Amazon’s seemingly late start to marketing its expertise in AI relative to rivals Microsoft (MSFT) and Google (GOOG, GOOGL).

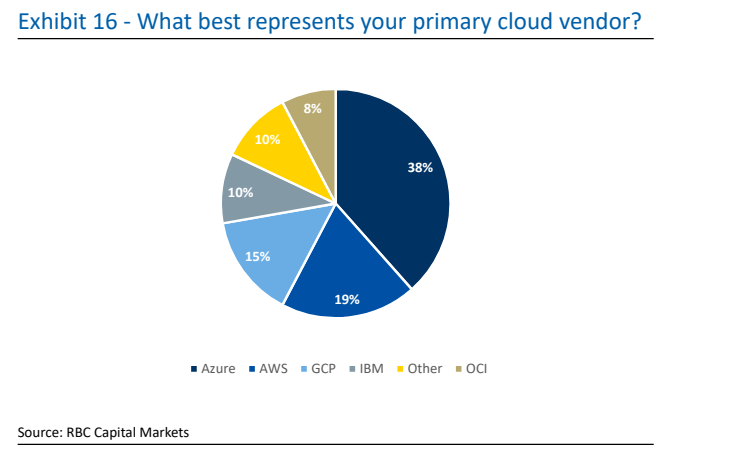

Specifically, AWS’ reaccelerating growth in Q3 highlights progress in its AI strategy, in addition to normalizing optimization trends in the industry. Recall that AWS remains the market leader in the provision of cloud-computing services. It currently commands about a third of the global cloud computing market, and is the primary cloud service provider for close to a fifth of the enterprise cloud spending segment.

RBC Capital Markets

And AWS’ recent deployment of competitive AI offerings – spanning its foundation model marketplace “Bedrock,” as well as hardware such as “Trainium” and “Inferentia” aimed at facilitating AI workloads – has likely leveraged its expansive cloud-computing market share, driving the gradual realization of adjacent revenue growth through total addressable market ("TAM") expansion enabled by the nascent technology trend. This is in line with management’s acknowledgement of adoption momentum in AWS’ generative AI solutions, especially amongst existing customers such as adidas AG (OTCQX:ADDYY, OTCQX:ADDDF) and United Airlines Holdings (UAL).

The tailwind is further corroborated by Amazon’s recent investment in AI start-up Anthropic, best known for its Claude chatbot. The company announced in late September that it has entered into an agreement with Anthropic that entails investments of up to $4 billion into the start-up. Amazon’s latest investment in the AI start-up – a viable rival to OpenAI – likely overtakes Anthropic’s existing partnership with Google, which puts AWS’ key rivals on notice. As a result of the arrangement, the availability of Anthropic’s innovations will now prioritize Amazon and its customers through solutions such as Bedrock, with the start-up also making AWS its primary cloud service provider. Anthropic has committed to training its future foundation AI models on Amazon’s proprietary Trainium accelerator and Inferentia AI chip as well. Taken together with AWS’ recent outperformance, the latest development is likely to make Amazon’s AI one-stop-shop all-the-more competitive to rivals’ offerings, such as Google’s Vertex AI and Microsoft’s Azure OpenAI Service.

Advertising Step-Up

Advertising revenue, albeit still a nominal growth and profit contributor at Amazon, remains a resilient corner for the company. The segment’s sales grew 26% y/y in Q3, accelerating sequentially. Amazon’s advertising strengths have remained a bright spot in the industry over the past year, while its competitors reel from the inherent sensitivities to broader macroeconomic challenges. Specifically, continued advertising sales growth at Amazon at robust double-digits suggests a combination of increasing ad load as well as improving pricing power despite the measured ad spending environment. Recent industry checks have also highlighted the demise of retailer Bed, Bath and Beyond as a tailwind for the company, as aggregators “move most/all of that ad spend over the Amazon” in recent quarters.

We believe Amazon continues to present itself as a growth leader in the retail media advertising format, which currently represents one of the strongest ad distribution avenues, in line with recent industry observations:

…retail media networks continue to be a bright spot in our business growing at 80% this year.

Source: DoubleVerify (DV) 2Q23 Earnings Call Transcript.

From an advertising perspective, retail media is something that’s really taken off over the last two years, It’s no coincidence that the growing interest in retail media coincides with growing advertiser focus on authenticated ad environments. With retail media, advertisers can start with precise authenticated data, whether that data is based on purchase history or loyalty data. From there, the advertiser can target based on what they know and then do more accurate data-driven modelling to expand targeting segments with greater precision.

Source: The Trade Desk (TTD) 2Q23 Earnings Call Transcript.

This is further corroborated by recent industry findings, which show demand for retail media formats already represents 30% of total spending on search ads. And relevant demand is expected to grow 22% in 2023 and 17% in the following year, making retail media a key driver in total search/commerce ad sales growth of close to 10% in 2024. While looming weakness in the consumer spending backdrop could potentially restrict the advertising budgets of retailers and hamper near-term demand for retail media formats, we expect Amazon’s advertising segment to remain resilient. We point to Amazon’s several competitive advantages on retail media advertising, including its market leading trove of first-party data on key consumer purchasing trends and behavior critical to targeting and measurement, as well as its extensive reach to drive conversion.

Fundamental and Valuation Update

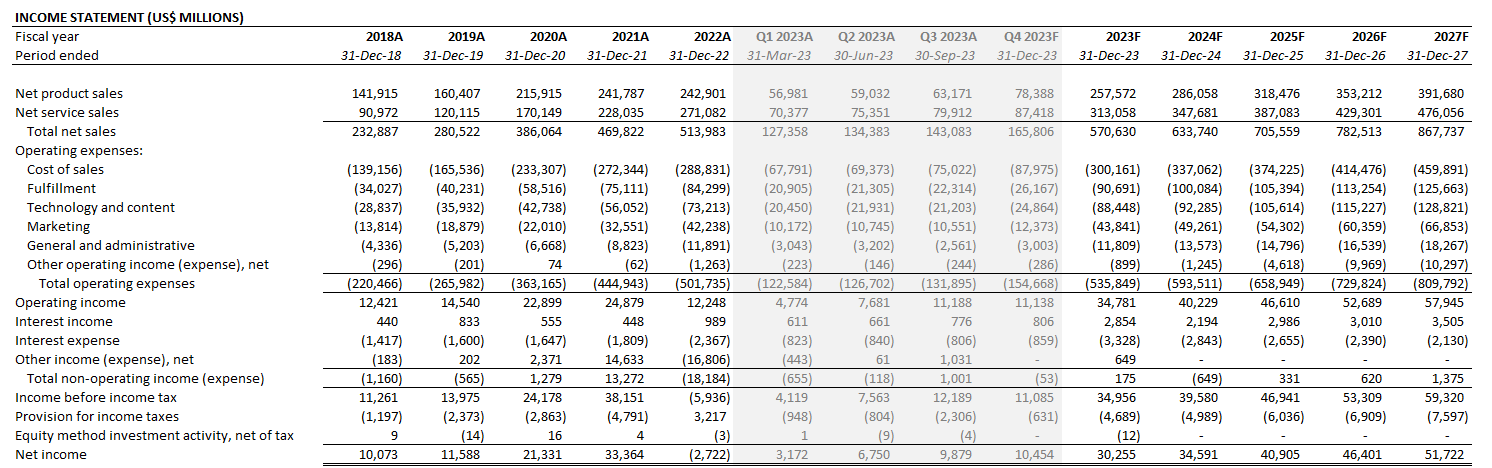

Adjusting our previous forecast for Amazon’s actual Q3 performance and forward growth prospects discussed in the foregoing analysis, we expect full-year 2023 revenue to expand at 11% y/y to $570.6 billion. North America revenue is expected to exit the fourth quarter with 11% y/y growth, resulting in full-year expansion of 11%, approaching prior year levels. Meanwhile, international revenue is expected to re-emerge in growth of 9% for full-2023 as well, given improvements in online stores, 3P seller services, subscription services, and advertising services revenue growth in recent quarters. AWS is expected to finish the year with 14% y/y growth in Q4, in line with expectations for continued sequential acceleration as optimization headwinds trough and its AI strategy picks up.

Author

On the cost front, operating margins are expected to benefit further from fulfilment efficiencies realized in Amazon’s core U.S. e-commerce business, as well as improved growth and ensuing scale at AWS, its profit driving segment.

Author

Amazon_-_Forecasted_Financial_Information.pdf.

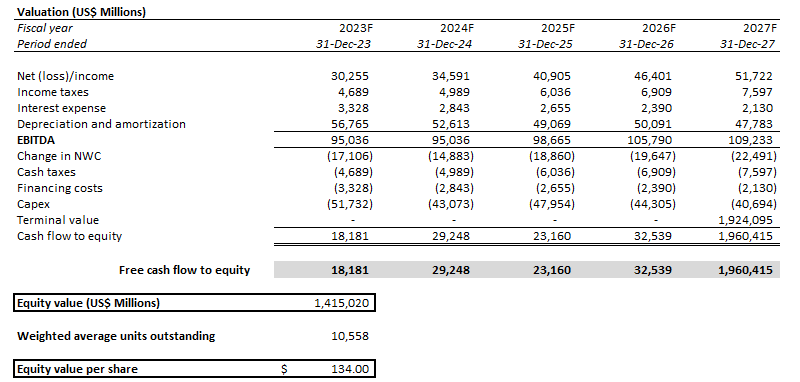

We are maintaining our base case price target of $152 on AMZN stock.

Author

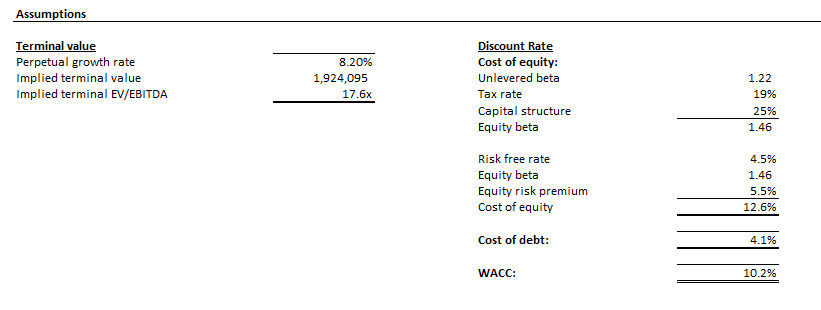

The price target is computed under the discounted cash flow method, which applies a WACC of 10.2% (vs. previous 10%) to account for Amazon’s capital structure and risk profile relative to the elevated risk-free benchmark, and an estimated perpetual growth rate of about 8%, or terminal multiple of 17.6, in line with the company’s longer-term cash flow prospects driven primarily by AWS. The perpetual growth rate applied implies 20x 2024 EBITDA, which is in line with the stock’s historical average as well as its placement among Amazon’s comparable mega-cap internet peers.

Author

Author

Final Thoughts

Amazon likely represents one of the most prone stocks, among its comparable mega-cap Internet peers, to the impact of ongoing macroeconomic uncertainties, given its highly cyclical e-commerce business and market leading exposure to the restrictive enterprise spending environment. This is reflected in the stock’s laggard performance to peers, despite the recent flight to safety tailwind for mega-caps with robust fundamentals amidst renewed risk-off market sentiment in response to the Fed’s call for a “higher for longer” rate environment.

Yet the company’s consistent outperformance in Q3 highlights company-specific strengths in weathering the industry-wide challenges. The results also implies that Amazon’s long-time e-commerce and cloud-computing moat remains intact despite signs of weakness over the past year. And upside surprises over the past two quarters also highlight the expertise of Amazon’s management, as well as their unwavering focus on driving value to the company’s stakeholders.

With Amazon.com, Inc. stock still trading at levels that trail its comparable Internet mega-cap peers, which is likely reflective of the underlying business’ elevated exposure to cyclical risks, the latest two consecutive quarters of fundamental outperformance are likely to alleviate some of this downside pressure and unlock incremental pent-up value from current levels.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments