Arithmetic returns

- Expected return for a bet is the simple probability-weighted average of outcomes.

- If there is a 50% chance of a bet making 21% and a 50% chance of it returning 19% this it’s a good bet that is also not volatile. You expect to make 20% on average (despite the fact that you can’t ever make that on any single bet since you can only earn 19% or 21%).

- Your expected terminal wealth after a single trial is 1.2x what you started with.

- Since we took a simple average of the outcomes we computed an arithmetic mean return of 20%

Compounded returns

For multi-period investing where we do not take any distributions or “money off the table” we cannot use simple arithmetic means to compute an expected return.

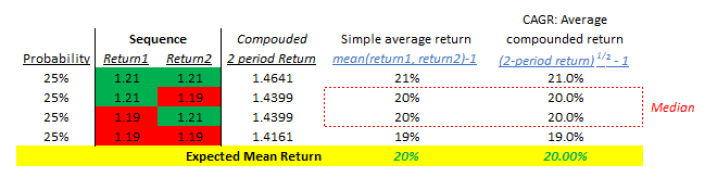

Consider the same bet after 2 trials. These are the 4 possibilities each equally likely:

- Best return, best return

- Best return, worst return

- Worst return, best return

- Worst return, worst return

If we look at the summary table, there is no difference between the mean expected return and the median.

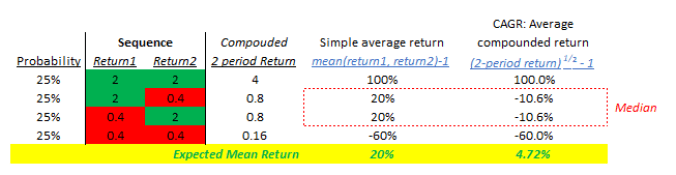

Let’s keep the mean return the same but raise the volatility. An investment that is equally likely to:

- go up 100%

- fall by 60%

Even though this is more volatile than the first investment, the mean expected return is still 20% per trial. You can compute this in 2 ways:

50% * +100% + 50% * -60% = 20%

or

Terminal wealth = 50% * 2 + 50% * .4 = 1.2 or 20% return

But let’s see what happens when we look at the compounded scenario where we fully re-invest the proceeds of the first period into a second period.

Now the mean compounded return has dropped from 20% to just 4.72% and the median outcome is a loss of 10.6%!

The divergence between mean and median returns comes from the compounded effect of volatility.

Investing Is a Multiplicative Process

When it comes to investing, we are usually re-investing rather than taking our profits off the table each year. We hope to grow our wealth year by year like this:

1.10 * 1.10 * 1.10 … or 1.10^n where n is the number of compounding intervals (typically years).

Therefore, we want to look at compounded not mean rates of return. To compute them we simply take the n-th root of our terminal wealth where n is the number of years.

If you doubled your money in 5 years then your CAGR = 2^(1/5) –1 = 14.9%

Note that if you took the naive average return you could say you earned 100% in 5 years or 20% per year. But this defies reality where you re-invested a growing sum of capital every year.

CAGR is a median return

It’s important to note that the expected mean return of these investments is still 20% per year. It’s just that the median is much lower. In the high volatility example, your lived experience usually results in a loss of 10.6% but the mean 2-period return is still positive 4.7%. The complication is that the avergae is driven by the 25% probability that you double your money in 2 consecutive year. In every other scenario, you lose money.

Volatility is altering the distribution of your outcomes not the mean outcome.

Mathematically the median is the geometric mean. In a multiplicative process, you care more about the geometric mean. After all, you only get one life.

A note on log returns

A logreturn is a compounded return where we assume continuous compounding. So instead of every year, it’s more like every second. Of course, if our wealth grows from $1 to $2 in 5 years but we assume tiny compouding intervals, then the rate per interval must be small. After all the start and end of our journey ($1 to $2) is the same, we are just slicing it into smaller sections.

Computing an expected logreturn is simple. Using the volatile example:

.5 * ln(2) + .5 + ln(.40) = -11.2%

Note that this is slightly worse than the geometric mean return (aka median) we computed earlier of -10.6%

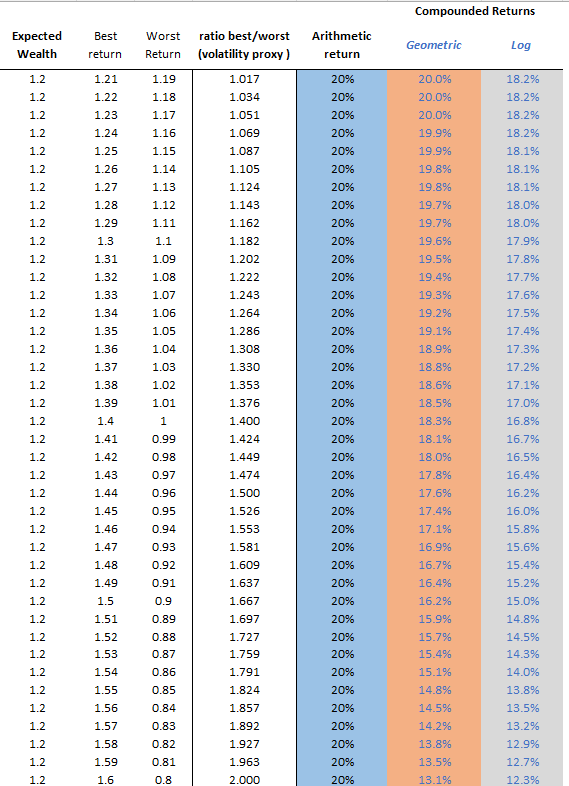

Volatility’s effect on compounded returns

The following table presents different investments that each have an expected arithmetic return of 20%. Just like the examples above. But the various payoffs are altered to proxy different levels of volatility. An investment that can earn 21% or 19% is much less volatile than one that can return 100% or -60% even though the average return is the same.

We use the simplest measure to represent the volatility — the ratio of the best return to the worst return.

The stable investment volatility proxy is 1.21 / 1.19 = 1.017

The volatile investment above is 2 / .4 = 5.00

Table snippet:

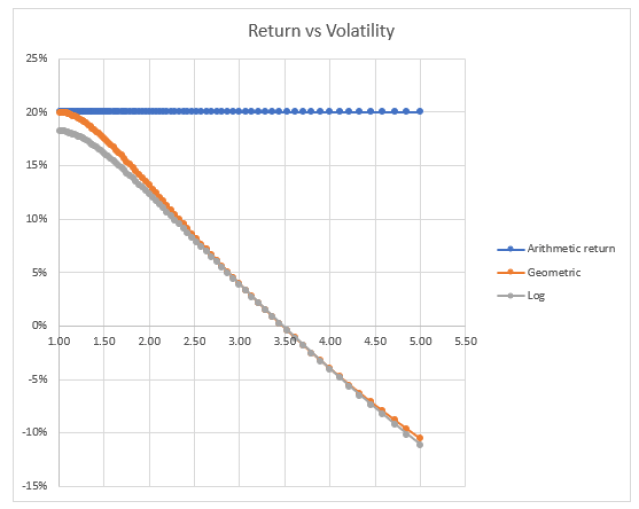

These charts show the divergence between arithmetic and median returns as we increase the volatility (the ratio of the best return to the worst return):

An investment that is equally likely to return 60% as it is to lose 20% has a 20% expected return but if you keep re-investing your long-term median outcome is closer to a 12–13% CAGR.

What if we raise the volatility further to a ratio of 5 (terminal wealth of 2x vs .4x):

At a ratio of 3.5 (1.87x vs .53x) our median result is zero. At a ratio of 5, the average return remains 20% but the median return is losing 10%. Almost all the paths are losing they are just being counterbalanced by the unlikely event that you keep flipping heads.

Takeaways

- Investing is a multiplicative process so we want to look at compounded or log returns not simple returns

- Compounded returns ask “what growth rate when multiplied from period to period gets us from the start point to the end point?”

- Compounded and logreturns are always less than arithmetic returns

- Compounded and log returns are better measures for what you expect to find in your bank account after volatility has taken its toll. Remember if you lose 50% on an investment you need 100% to get back to even. If you earn 50% on an investment you only need to lose 33% to be back at even.

- If there was no volatility there’d be no promise of return, but volatility is a quadratic drag on returns. The sweet spot for your portfolio likely falls in the realm of the volatility of broadly diversified portfolios. By rebalancing you can reduce concentration risks that threaten to turn your entire nest egg into a coin flip. Even if this coin has positive expectancy, remember you can’t eat theoretical edge.

Comments