Summary

- SilverCrest Metals Inc. maintains strong production and cost efficiency, with Q3 results reflecting increased production and well-managed costs.

- The company's valuation metrics, such as EV/EBITDA ratio and price-to-net asset value, position it as an attractively priced stock in the silver mining sector.

- SilverCrest's active share buyback program and status as a prime M&A candidate further enhance its appeal to investors.

alexis84

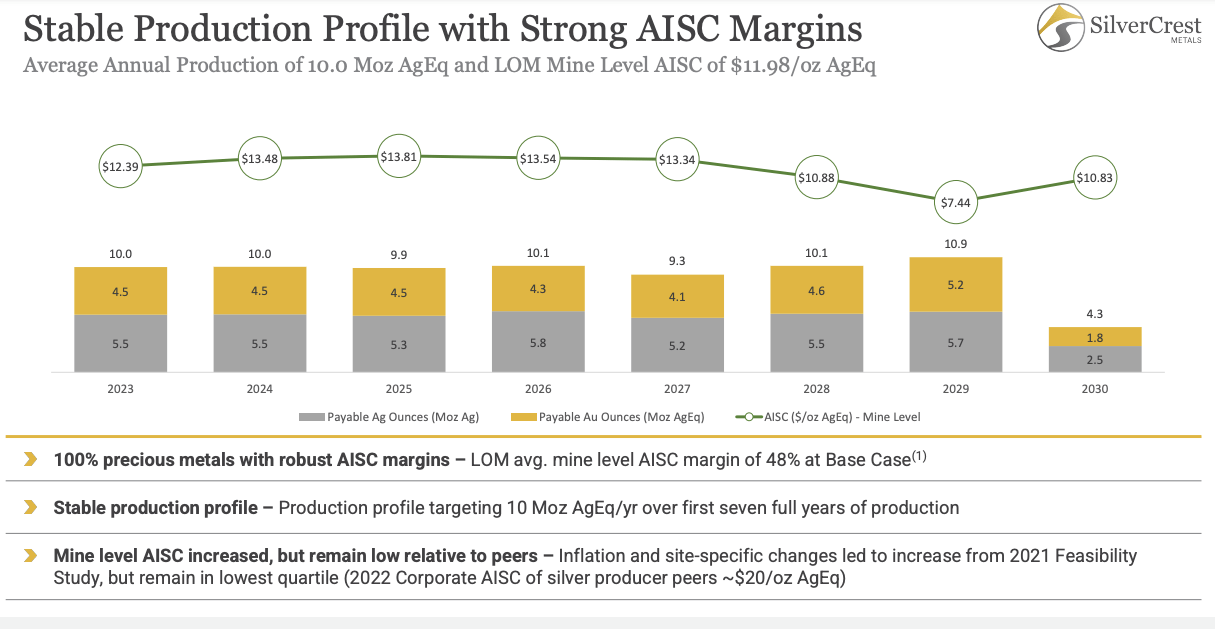

SilverCrest Metals Inc. (NYSE:SILV) is a high-grade silver and gold producer that's averaging around 10 million silver equivalent ounces of production annually at its Las Chispas mine in Mexico.

Despite the general struggles faced by silver mining stocks in 2023, SilverCrest has recently marked a significant turnaround with one of the most impressive quarterly earnings in the gold and silver mining sector for Q3. This success is attributed to decreasing all-in-sustaining costs and steady production levels at the Las Chispas mine.

Looking ahead, SilverCrest maintains its 2023 production and cost projections. The company confidently expects to sell between 9.8 to 10.2 million ounces this year, with all-in sustaining costs ranging from $12.75 to $13.75 per ounce of silver equivalent (compared to spot silver prices of ~$23).

Financially, SilverCrest is also standing on solid ground, boasting nearly $82 million in cash and equivalents and the notable absence of any debt. This combination of strong production, substantial profits, and a healthy balance sheet not only underscores SilverCrest's resilience, but also enhances its appeal as a potential M&A target in the precious metals space.

Finally, and perhaps most importantly to investors, I think SilverCrest's stock valuation remains attractive. Even after a 9.20% rise over the past month, the shares don't appear overvalued, making it an interesting option.

Here's a closer look at SilverCrest's Q3 and my updated thoughts on the stock.

SilverCrest Metals: Impressive Production, Cost Efficiency

SilverCrest Metals

SilverCrest Metals is set to maintain its strong performance in the coming years, as detailed in its technical report. The company is expected to consistently produce around 10 million silver equivalent ounces (SEOs) annually.

Here's a quick summary of Q3 results:

In Q3 2023, SilverCrest recovered 15,700 ounces of gold and 1.49 million ounces of silver, or 2.74 million AgEq ounces. It ended up selling 14,500 ounces of gold and 1.53 million ounces of silver at average prices of $1,931 per ounce for gold and $23.41 per ounce for silver, totaling 2.68 million AgEq ounces sold.

Its mining rates rose by 11% from Q2 to Q3, averaging 911 tonnes per day. The company stated that this boost was due to more long-hole stopes being available than planned, alongside higher localized dilution in the Babicanora Main Vein. The Q4 mining rates are anticipated to range between 800 to 900 tonnes per day. Daily mill throughput also exceeded expectations, reaching 1,245 tonnes per day.

Impressively, cash costs were only $6.53 per AgEq ounce sold, and all-in sustaining costs were just $12.23 per AgEq ounce, both below the lower end of the H2 2023 guidance.

The company reported $63.8 million in revenue against a cost of sales of $26.4 million, yielding a mine operating income of $37.5 million - a substantial 59% operating margin.

Net income came in at $29.9 million, or $0.20 per share. SilverCrest also generated a net free cash flow of $33.4 million, or $0.23 per share.

The company invested $7.1 million to repurchase and cancel its own common shares.

SilverCrest concluded the quarter without any debt and with total cash and cash equivalents totaling $81.7 million, which includes $70.0 million in cash and $11.7 million in gold and silver bullion. This marks a remarkable ~$17 million increase from the previous quarter.

So, what to make of this quarter? Clearly, SilverCrest Metals' Q3 results reflect a company that is not only increasing its production but also managing its costs very well.

With robust production figures, exceptional cost control, and a strong balance sheet marked by significant cash reserves and zero debt, SilverCrest is solidifying its position as one of the strongest silver miners in the industry.

SilverCrest's Valuation Update

SilverCrest Metals

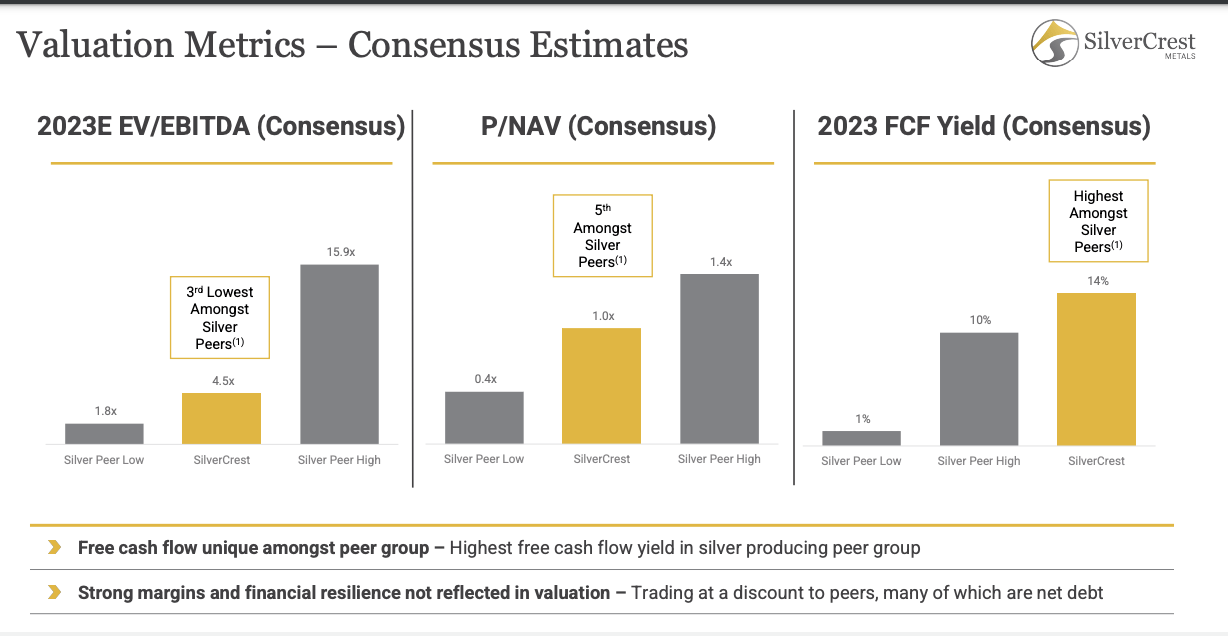

SilverCrest Metals stands out as an attractively priced stock in the silver mining sector when using various valuation metrics.

For example, the company's estimated EV/EBITDA ratio is just 4.5x, positioning it as the third most affordable among its selected peer group, which includes Aya Gold & Silver Inc. (OTCQX:AYASF), Coeur Mining, Inc. (CDE), Endeavour Silver Corp. (EXK), First Majestic Silver Corp. (AG), Fresnillo plc (OTCPK:FNLPF), Fortuna Silver Mines Inc. (FSM), Gatos Silver (GATO), Hecla Mining Company (HL), MAG Silver Corp. (MAG), Pan American Silver Corp. (PAAS), and Silvercorp Metals Inc. (SVM).

In terms of price-to-net asset value ("NAV"), SilverCrest ranks fifth lowest among its peers, suggesting that its stock is priced favorably relative to the company's net assets.

Supporting this view of undervaluation, Seeking Alpha has given SilverCrest a valuation grade of B+, indicating it as one of the more modestly valued stocks in the precious metals domain. This is further exemplified by its price-to-earnings ("P/E") ratio of 9.54, which is significantly lower than the peer group's median of 16.42, based on available data.

SilverCrest Metals

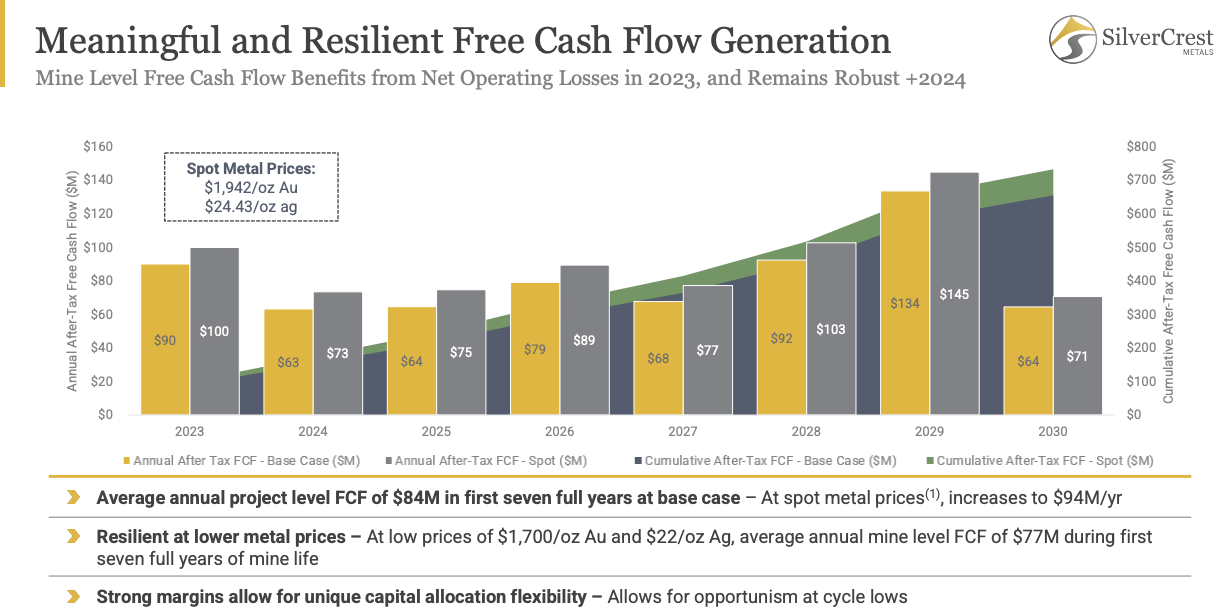

SilverCrest Metals shows great promise in generating strong earnings and cash flow in the coming years.

The company expects to make, on average, about $84 million each year in free cash flow for the first seven years, based on the base-case prices for gold and silver. If we consider today's higher metal prices, this yearly cash flow could increase to around $94 million. With higher metals prices, $100+ million annual cash flow becomes a real possibility.

What's really impressive is that if things go as planned and metal prices stay steady or rise, SilverCrest could make almost $700 million in total cash flow after taxes by 2030. This is a big deal, especially when you compare it to the company's current enterprise value of about $720 million.

For investors, this means SilverCrest is looking like an even more attractively valued stock.

SilverCrest's Share Buybacks: A Game Changer?

One possible benefit of investing in SilverCrest Metals is its active share repurchase program, a rarity among precious metals producers.

Through its Normal Course Issuer Bid, or NCIB, SilverCrest is authorized to buy back up to 7.36 million of its common shares, which represents about 5% of the 147.2 million shares currently in circulation.

As of now, the company has already bought back 20% of the total shares it's allowed to repurchase under this program.

SilverCrest believes that the market doesn't always accurately reflect the true value of its shares, considering its future growth potential and the cost to develop similar mining projects.

This perspective makes a lot of sense, because buybacks are most effective when they're used to repurchase shares that are undervalued - which certainly seems to be the case here with SilverCrest. I think these buybacks could be a significant driver for the stock's performance in 2024.

SilverCrest: Prime M&A Candidate

YCharts

SilverCrest stands out as the sole 100% owner of a top 10 primary silver mine, making it a particularly attractive asset.

I believe that the combination of its low cash costs, impressive profitability, and a mine life extending beyond 8 years makes it an appealing target for larger players in the industry.

Companies like Hecla, Coeur, Pan American Silver, and SSR Mining Inc. (SSRM) may consider SilverCrest a strategic fit for acquisition in the near future.

The bottom line: While higher gold and silver prices in 2024 would certainly be beneficial to SilverCrest, the stock price of ~$5.50 currently presents great value. My assessment remains that SilverCrest is a BUY for investors looking for solid performance in the precious metals sector.

Comments