Summary

- Ventas, a healthcare REIT, has underperformed the market due to the pandemic and high interest rates.

- The company is starting to recover, with strong demand for its properties and favorable supply-demand fundamentals.

- Analysts expect Ventas to grow its FFO per unit by 7% per year, and the stock is reasonably valued with upside potential.

Funtap

Almost four years ago, I recommended purchasing Ventas (NYSE:VTR) for its promising growth prospects and its attractive dividend yield of 5.5% back then. Unfortunately, a few months later, the coronavirus crisis emerged and severely hurt the REIT. In addition, Ventas has been negatively affected by the surge of interest rates to 16-year highs, as its interest expense has significantly increased. As the company has yet to recover from the pandemic and the sky-high interest rates, it has pronouncedly underperformed the broad market since my article, with a total return of -5% (vs. +45% of the S&P 500). Nevertheless, the worse seems to be behind Ventas, which also enjoys secular growth drivers and is reasonably valued. Therefore, investors should consider purchasing the stock around its current price.

Business overview

Ventas is one of the largest healthcare REITs in the U.S., with about 1,400 properties in the U.S., Canada, and the United Kingdom. As a healthcare REIT, Ventas is supposed to be resilient to downturns but it proved vulnerable to the pandemic. To be sure, its funds from operations [FFO] per unit in 2022 were 22% lower than they were before the pandemic, in 2019.

Most REITs were hurt by the coronavirus crisis in 2020 but they recovered in the following years. The primary reason behind the absence of a recovery in the case of Ventas is the unfortunate timing of its $4.0 billion of investments in 2019, just before the pandemic, and the resultant high debt load.

Due to the surge of inflation to a 40-year high last year, the Fed has been raising interest rates at an unprecedented pace since early last year. Consequently, interest rates have climbed to 16-year highs this year. As Ventas carries a material amount of debt, its interest expense has increased 22%, from $438 million in 2021 to $536 million in the last 12 months. Interest expense currently consumes 86% of the operating income of the REIT. Therefore, it is easy to understand why Ventas has not yet fully recovered from the pandemic.

Fortunately, the healthcare REIT has finally begun to recover. In the third quarter, it experienced strong demand for its properties, with the move-ins in its senior housing portfolio exceeding the pre-pandemic levels. As a result, the REIT grew its same-store net operating income by 8% and its FFO per unit by 6% over the prior year’s quarter, from $0.71 to $0.75.

Moreover, Ventas benefits from a strong secular trend, namely an aging population. More than 70 million individuals (about 20% of the U.S. population) will be 65 or older by 2030. The number of U.S. citizens above the age of 80 is expected to grow 24% over the next five years. These demographic trends provide a strong tailwind to the business of Ventas, which relies on the tendency of elderly people to spend great amounts on their healthcare.

It is also important to note that management recently stated that the supply-demand fundamentals in senior housing are the most favorable Ventas has ever experienced in its markets. The development of new properties is at cyclical lows and is likely to remain depressed due to the sky-high interest rates prevailing right now, as high interest rates greatly reduce the amounts spent on new investments. In fact, this is the exact reason behind the aggressive interest rate hikes implemented by the Fed to cool the economy.

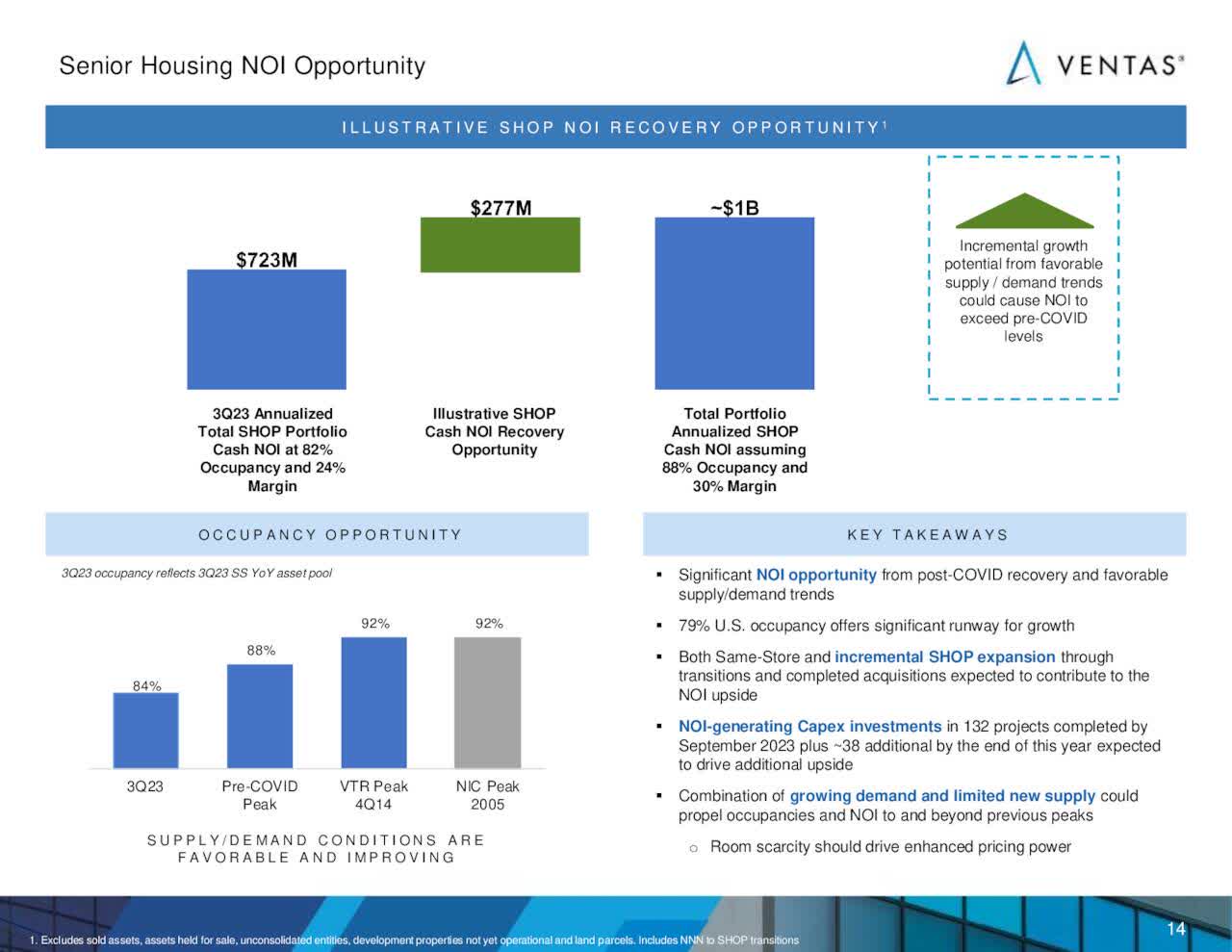

Growth Potential of Ventas (Investor Presentation)

Source: Investor Presentation

The lack of new starts in senior housing properties is likely to provide strong pricing power to Ventas in the upcoming years. As a result, the REIT believes that it has entered a multi-year growth cycle.

Furthermore, Ventas has promising growth prospects thanks to its low current occupancy rate. The REIT posted an occupancy rate of 84% in the latest quarter. This is much lower than the pre-pandemic peak of 88% and the peak of 92% in 2014.

Ventas: Growth Potential From Occupancy (Investor Presentation)

Source: Investor Presentation

Therefore, as long as Ventas continues to recover from the pandemic and reaches the peak occupancy levels it enjoyed before the pandemic, it is likely to significantly grow its FFO per unit.

Analysts seem to agree on the promising growth potential of Ventas. They expect the REIT to grow its FFO per unit by 7% per year over the next three years, from $2.98 this year to $3.66 in 2026. While some investors try to identify stocks with higher growth rates, a 7% growth rate is certainly attractive for a REIT, particularly a healthcare REIT, which is fairly resilient to recessions.

Valuation

Ventas is currently trading at a price-to-FFO ratio of 15.1. This FFO multiple is only slightly higher than the 10-year average price-to-FFO ratio of 14.7 of the stock. It is also important to note that the stock is trading at only 12.3 times its expected FFO in 2026. Therefore, if Ventas meets or exceeds the analysts’ estimates in the upcoming years, its stock will have significant upside.

Investors should also be aware that REITs are among the most sensitive securities to interest rates. High interest rates greatly increase the interest expense of REITs and simultaneously compress their valuation, as they render their dividends less attractive. Thanks to the aggressive policy of the Fed, inflation has cooled from a 40-year high of 9.2% in the summer of last year to 3.2% now. Whenever it reaches the target range of 2.0%-2.5% of the Fed, the central bank is likely to begin lowering interest rates. Given the high sensitivity of REITs to interest rates, lower interest rates are likely to provide a strong tailwind to the valuation of Ventas.

If Ventas meets the analysts’ estimates in 2026 and trades at its 10-year average price-to-FFO of 14.7 in that year, it will have 20% (=14.7/12.3 – 1) upside potential over the next three years. Given also its current dividend yield of 4.0%, the stock can offer a 32% total return over the next three years or a 9.7% annualized total return. This is certainly an attractive expected return for conservative income-oriented investors.

Dividend – Debt

Ventas is currently offering a dividend yield of 4.0%, with a healthy FFO payout ratio of 60%. This payout ratio is slightly lower than the median payout ratio of 63% of the REIT sector and is a nearly 10-year low level for Ventas. Therefore, the dividend seems to have a material margin of safety.

On the other hand, investors should note that Ventas cut its dividend by 43% in 2020, due to the coronavirus crisis, and has kept its dividend constant since then. In addition, the REIT has a somewhat high debt load. Its interest expense is consuming 86% of its operating income while its net debt (as per Buffett’s formula: net debt = total liabilities – cash – receivables) is standing at $14.2 billion. This amount is 78% of the market capitalization of the stock and hence it is material. On the other hand, most REITs have net debt levels near or above 100% of their market cap. Therefore, the debt level of Ventas is not excessive and is likely to prove manageable in the absence of a severe downturn. Overall, the 4.0% dividend of Ventas appears fairly safe, particularly given the promising growth prospects of the REIT.

Risk

Most stocks are vulnerable to recessions but this is hardly the case for Ventas, as people do not reduce their healthcare expenses even under the fiercest economic conditions. As a healthcare REIT, Ventas is fairly resilient to recessions.

On the other hand, Ventas is vulnerable to an environment of persistently high interest rates. As mentioned above, the Fed is likely to begin reducing interest rates whenever inflation falls to the target zone of the central bank, most likely next year. If inflation proves much stickier than currently expected, interest rates are likely to remain excessive for a considerable period. In such an adverse scenario, Ventas will be negatively affected via high interest expense and pressure on its valuation level. Therefore, only the investors who can wait patiently for interest rates to moderate should consider purchasing Ventas.

Final thoughts

Ventas has underperformed the broad market by a wide margin over the last four years and thus it has fallen out of favor in the investment community. However, the REIT has begun to recover and has promising growth potential while its valuation is reasonable. Therefore, it is likely to offer attractive returns off its current price, especially if interest rates decrease significantly in the upcoming years.

Comments