Summary

- National Fuel Gas has underperformed the S&P 500 due to milder winter weather and a bearish outlook on the natural gas industry.

- The company has reduced its sensitivity to natural gas prices and offers a low forward price-to-earnings ratio and high dividend yield.

- National Fuel Gas has steady production growth, a strong reserve base, and promising prospects for future earnings growth.

Pgiam/iStock via Getty Images

In 2020, shortly after the onset of the coronavirus crisis, I recommended purchasing National Fuel Gas (NYSE:NFG) for its robust business model, its promising growth prospects, and its attractive dividend. Since then, the stock has offered a total return of 40%. Almost three months ago, I reiterated my bullish thesis but the stock has declined 4% since that article and thus it has underperformed the S&P 500, which has gained 1%. The recent underperformance has been caused by milder-than-normal winter weather and the latest outlook of the Energy Information Administration [EIA] on the natural gas industry, which is bearish.

However, National Fuel has solid growth potential ahead while it has reduced its sensitivity to the prevailing price of natural gas. In addition, the stock is trading at a nearly 10-year low forward price-to-earnings ratio of 9.1x, offering a nearly 10-year high dividend yield of 3.9%. Therefore, investors should not be discouraged by the unfavorable weather outlook. Instead, they should remain patient until business conditions improve and the market rewards the stock with a more reasonable valuation level.

Business overview

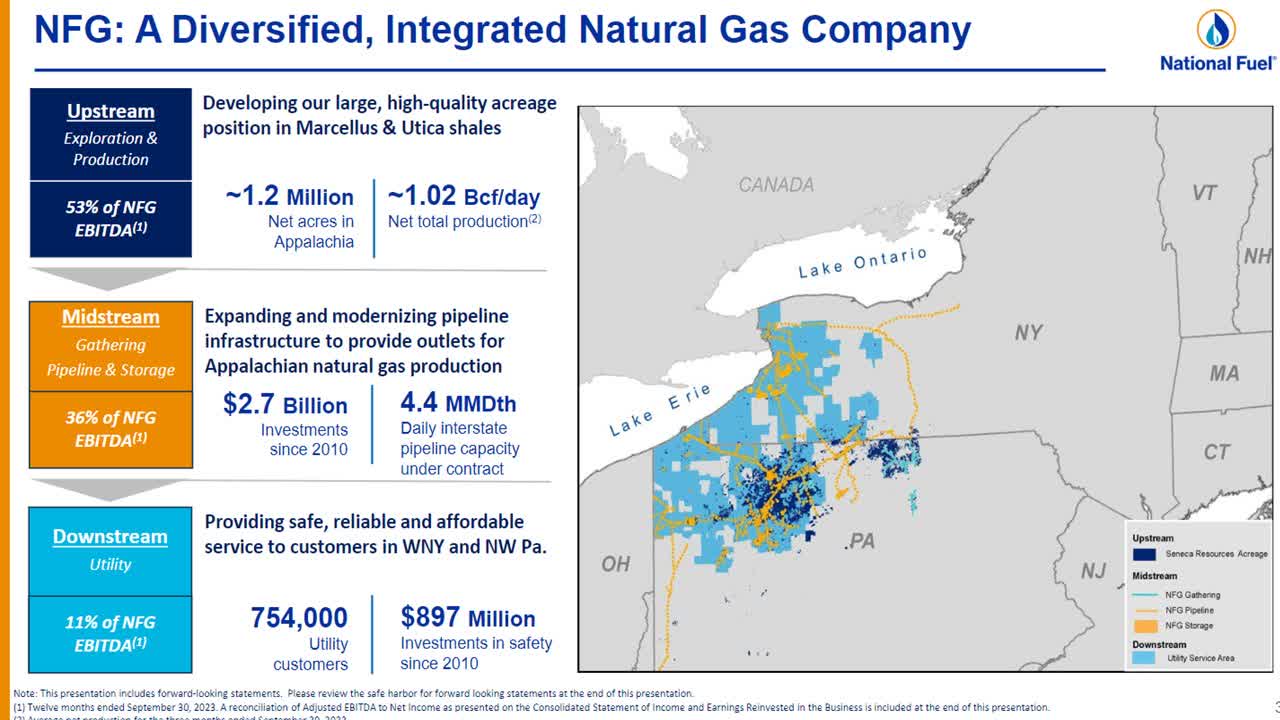

National Fuel Gas is a highly integrated energy company that is focused on the natural gas industry. It was founded in 1902 and has an upstream (exploration and production), midstream (gathering and storage), and downstream segment.

Overview of National Fuel Gas (Investor Presentation)

Source: Investor Presentation

As the upstream division generates 53% of the total EBITDA of National Fuel Gas, it is evident that the company is sensitive to the price of U.S. natural gas. However, the midstream and the downstream divisions offer resilient and reliable cash flows and hence they provide a strong buffer during periods of low gas prices. The company also hedges a great part of its production and thus it somewhat mitigates the effect of gas prices on its earnings.

The Energy Information Administration recently provided a bearish short-term outlook on the natural gas market. Due to high production of natural gas and expectations for a milder-than-normal winter, the EIA expects the U.S. natural gas inventories to stand 21% above their 5-year average level at the end of the heating season, in March. The price of natural gas has declined 21% this month, from $3.64 to $2.88, mostly due to the bearish outlook of the EIA and the mild winter weather so far.

However, weather has always been volatile and unpredictable and hence investors should not base their investing thesis on short-term or mid-term weather trends. More importantly, National Fuel Gas has remarkably reduced its sensitivity to the price of natural gas in recent years thanks to its highly diversified and integrated business model as well as its price hedging strategy. To be sure, in its fiscal 2023, which ended in September, the average price of natural gas plunged 45% over the prior year but the adjusted EBITDA and the earnings per share of the company dipped only 5% and 12%, respectively. This is certainly an impressive performance for a company engaged in the natural gas industry.

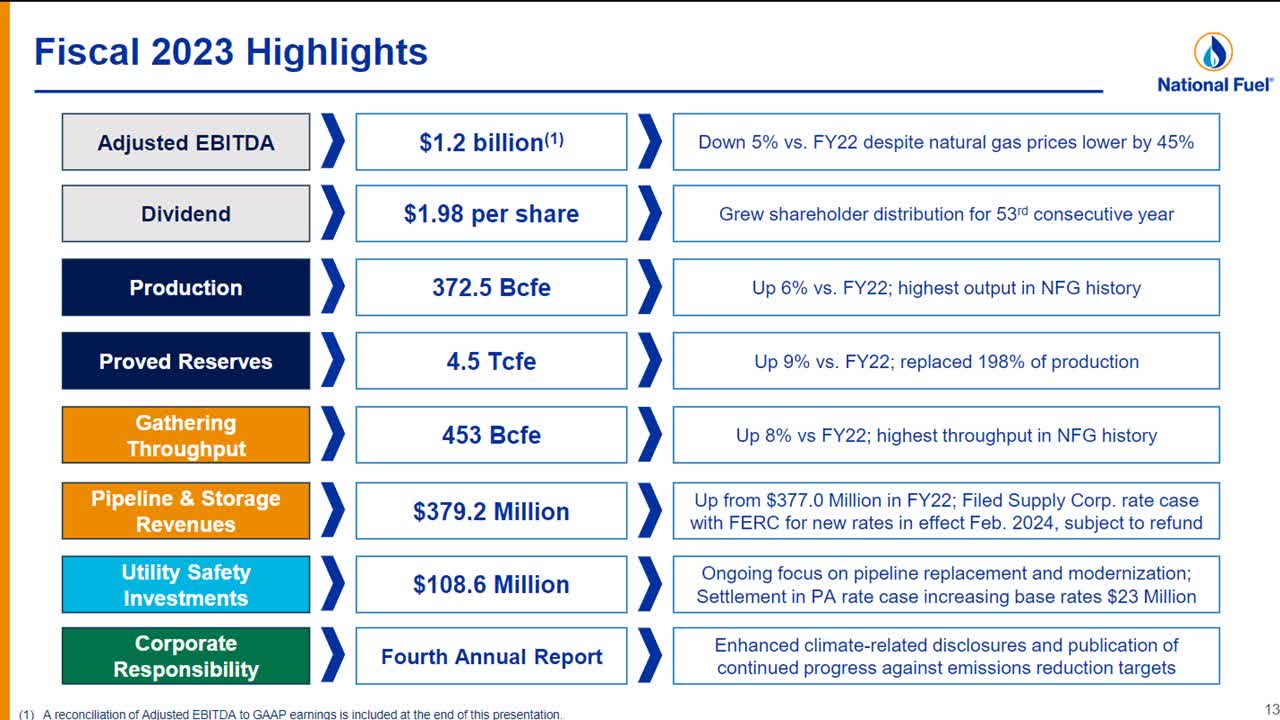

Another reason behind the resilient performance of National Fuel Gas is its sustained production growth. The company grew its production by 6% in fiscal 2023, to a new all-time high.

National Fuel Gas - Fiscal 2023 Highlights (Investor Presentation)

Source: Investor Presentation

Even better, National Fuel Gas posted an eye-opening reserve replacement ratio of 198%, and thus it grew its total proved reserves 9%, to a new all-time high of 4.5 trillion cubic feet. The reserve replacement ratio and the growth rate of the reserves of National Fuel Gas are among the highest in the entire energy sector and undoubtedly bode well for future production growth.

National Fuel Gas has steadily grown its production and its reserve base for several years in a row. The consistent and reliable growth of the proved reserves of the company results from its focus on the exceptionally rich resource areas of Utica and Marcellus. As these areas have excessive amounts of natural gas, National Fuel Gas is likely to keep growing its production for many more years. Analysts seem to agree on the promising prospects of the company, as they expect it to grow its earnings per share by 9% in fiscal 2024 and by another 23% in fiscal 2025.

Valuation

As mentioned above, National Fuel Gas is currently trading at a nearly 10-year low forward price-to-earnings ratio of 9.1x. This earnings multiple is much lower than the 5-year average of 13.0 of the stock. It is also remarkable that the stock is trading at only 7.4 times its expected earnings in 2025. The cheap valuation has probably resulted from the negative market sentiment, which has been caused by the unfavorable winter weather and the aforementioned bearish outlook of the EIA.

However, it is reasonable to expect the weather to become favorable at some point in the future while it is also important to keep in mind the improved resilience of National Fuel Gas to modest natural gas prices. Whenever weather conditions become favorable for National Fuel Gas, the valuation of the stock will probably expand toward its historical average. When that happens, the stock will have up to 43% upside potential (=13.0/9.1 – 1) merely thanks to the normalization of its valuation.

Dividend

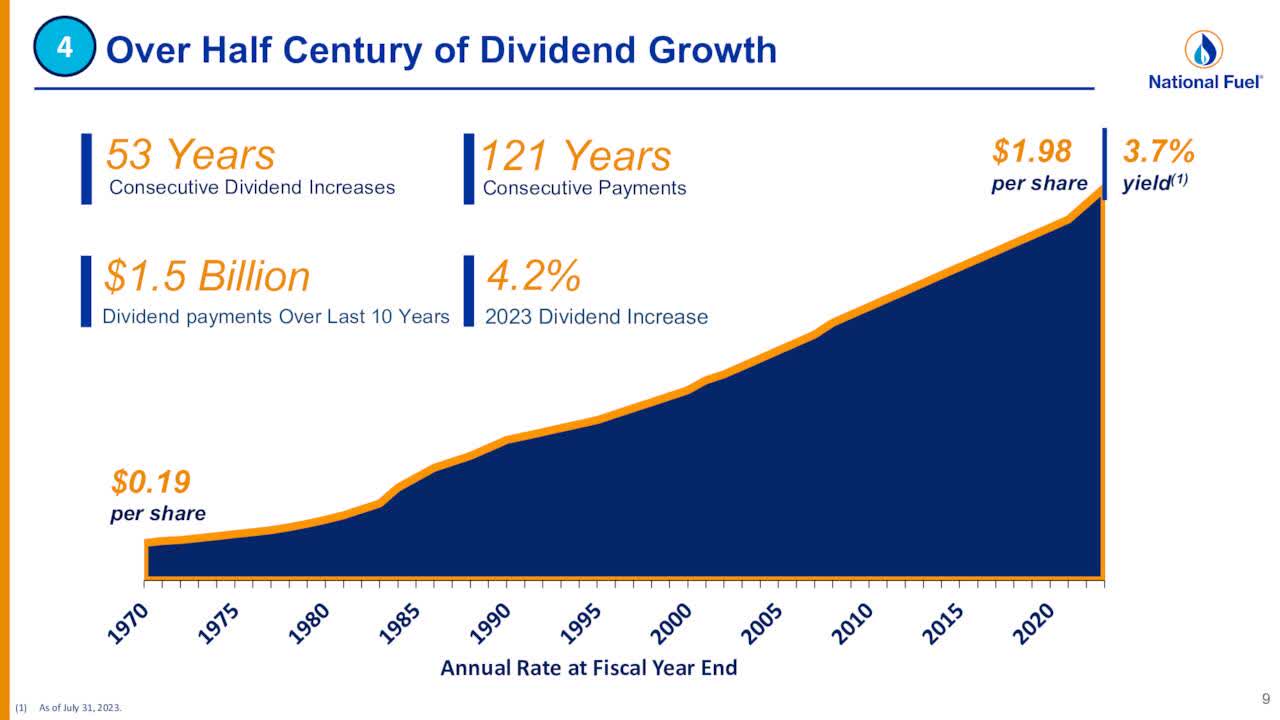

The resilient business model of National Fuel Gas is clearly reflected in its outstanding dividend growth record. The company has raised its dividend for 53 consecutive years and hence it has the longest dividend growth streak in the entire energy sector.

Dividend Growth of National Fuel Gas (Investor Presentation)

Source: Investor Presentation

It is also currently offering a nearly 10-year high dividend yield of 3.9%, with a solid payout ratio of only 38%. Moreover, National Fuel Gas has a healthy balance sheet. Its interest expense consumes just 17% of its operating income while its net debt (as per Buffett’s formula: net debt = total liabilities – cash – receivables) is standing at $5.1 billion. This amount is approximately 10 times the annual earnings of the company and 109% of its current market capitalization hence it is not negligible but it is certainly manageable, particularly given the reliable growth trajectory of the company. Overall, National Fuel Gas has the longest dividend growth streak in its sector and is likely to continue raising its dividend for many more years.

Risk

The primary risk for National Fuel Gas is the adverse scenario of depressed natural gas prices for a prolonged period. Such an unfavorable scenario could materialize due to the secular transition of most countries from fossil fuels to renewable energy sources. However, natural gas is viewed as a much cleaner fuel than oil products. As a result, the vast majority of countries aim to drastically reduce their consumption of oil products but not the consumption of natural gas. Therefore, the business of National Fuel Gas seems resilient to the ongoing transition towards green energy sources.

Depressed gas prices could also result from persistently adverse weather, i.e., mild winter weather. However, experience has proved that extreme weather conditions do not last for more than a few months. Therefore, if the stock of National Fuel Gas remains under pressure due to mild weather, its shareholders just need to be patient until weather reverts to normal.

Final thoughts

Despite its consistent performance, its reliable growth trajectory, and its exceptional dividend growth record, National Fuel Gas passes under the radar of most investors, who prefer to avoid the cyclicality of the natural gas industry. However, thanks to its integrated business model, the company is much less cyclical than most oil and gas companies. Given also its attractive valuation, the stock is likely to highly reward patient investors off its current price.

Comments