Summary

- Meat commodity prices have stabilized in 2023 after experiencing extreme volatility from 2020 to 2022 but remain generally elevated.

- Investors should expect the possibility of prolonged negative profit margins for Tyson due to labor shortages and rising input costs.

- Tyson faces a significant debt maturity in 2024, likely increasing its interest costs materially due to higher interest rates.

- I believe Tyson Foods is materially overvalued today and has a fair value closer to $30 based on income projections discounted by its risk.

Anna Moneymaker/Getty Images News

After facing extreme volatility from 2020 to 2022, meat commodity prices generally stabilized in 2023. Beef and poultry commodity prices have seen moderate declines since their 2022 peaks but remain typically elevated compared to pre-COVID price levels. On the other hand, consumer prices for most meat products have risen this year, albeit at a much lower rate than over the two years prior. That said, major meat companies such as Tyson Foods (NYSE:TSN) have faced significant declines this year as profit margins on their products reverse dramatically after being very high in 2021.

I covered Tyson Foods in July in "Tyson Foods: Meat Market Crisis Points To 'Lower For Longer' Profit Margins." At that time, I had a bearish outlook for various reasons. Fundamentally, I believed the company's profit margins would continue to decline and stay low as meat commodity prices remained high, causing the company to fail to pass input costs onto consumers. This issue has been further aggravated by growing labor woes and reduced farm animal production levels, which may be due in part to what I view to be Tyson's short-term business strategy.

Since that article was published, TSN has lost only around 3.5% of its value. However, it had lost about 14% in value by October but reversed most of those losses in recent weeks. This rally arrived after a relatively poor Q3 report and flat revenue guidance for its FY 2024 outlook. Even more, the company has faced some pressure regarding labor practices. This is potentially a public image issue. It also shows how Tyson is potentially cutting corners to maintain its flailing profit margins.

Despite its rally, Tyson has generally faced negative news over recent months. The recent rebound appears triggered by its decision to raise its dividend by 2%, giving it a yield of ~3.8% today, which is lower than the risk-free rate. Given this, I believe it is an opportune time to take a closer look at the company to determine its valuation and risk potential today. In particular, we must determine whether or not Tyson raised its dividend because of an improved outlook or to encourage investment despite its negative fundamental trend.

Negative Profit Margins Will Continue

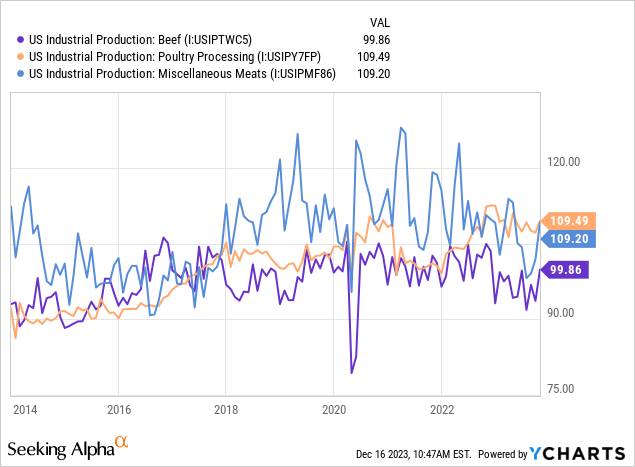

In 2020, there was a massive increase in consumer prices for meat products. Tyson's revenue is most costly tied to consumer prices for its meat products, while meat commodity prices are a significant cost factor. The company has some vertically integrated farms but generally buys meat from farmers. Beef prices have been exceptionally high since COVID due to a combined labor shortage on farms and a 1,200-year record dry spell in the Southwest. US production and exports for beef and veal have been stagnant. That said, there has been a slight positive turn in meat production levels, particularly in poultry, which has filled the gap created by beef. See below:

Data by YCharts

Data by YCharts

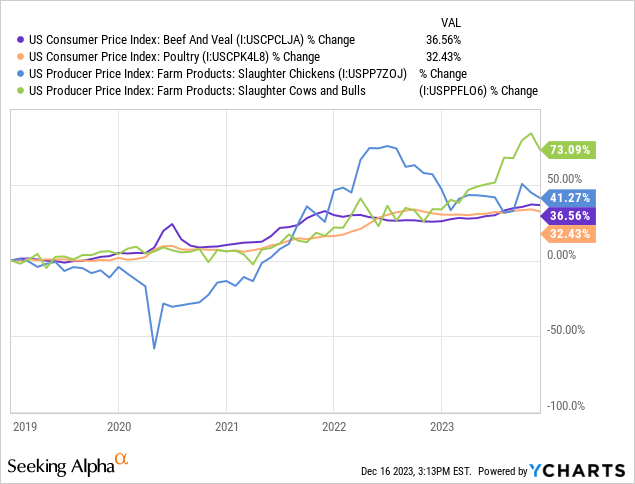

The increase in chicken production has had a more clear negative impact on chicken prices. Specifically, this is the price received by chicken and cow farmers, not the consumer price paid in the store. Thus, lower animal prices are a positive factor for Tyson Foods. See below:

Data by YCharts

Data by YCharts

Notably, cows and chickens are still much more expensive than in 2020. The declines in chicken prices have a slight positive impact on Tyson but are still not necessarily large enough to shift Tyson's margins. Further, cow prices remain very high compared to pre-COVID levels. That said, the slight negative price trend combined with increased production is a positive factor for Tyson's cost outlook.

On the revenue side, we're seeing comparative moderation in the rise of meat prices at grocery stores. Beef has become more expensive while poultry has stagnated, likely stemming from increased chicken production and lower chicken farm prices. Altogether, I believe this points toward a continuation of the profit levels we've seen in Tyson over the last two quarters. It is certainly possible that beef and poultry farm prices fall while consumer prices do not, but farm prices remain as high after COVID points toward a prolonged shift in the market's supply and demand outlook.

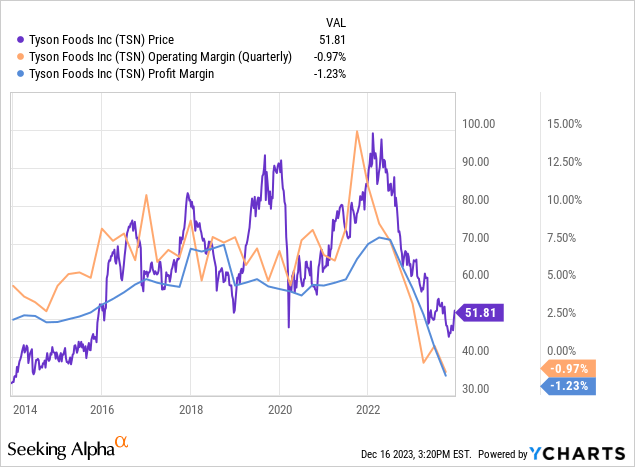

In my view, investors should expect prolonged negative profit margins. Tyson's operating margins have collapsed to nearly 1% amid the growth of input costs. The most significant factor is likely burgeoning production costs due to labor shortages and older factory plants that are being closed. While the company is fighting to handle its cost growth, it is struggling, mainly because people are starting to buy fewer meat products in response to rising prices. See below:

Data by YCharts

Data by YCharts

I think many investors underestimate the potential for this situation to last for over a year or two. Many view this change as stemming from the shock in the meat market created during the COVID lockdowns. That said, this change may be more entrenched in the company's business, as labor issues in farms are pushing material input costs up while labor issues in meat processing are pushing Tyson's other costs higher. The fact may be that meat processing cannot remain as profitable due to growing economic power for specific segments of workers.

What is TSN Worth Today?

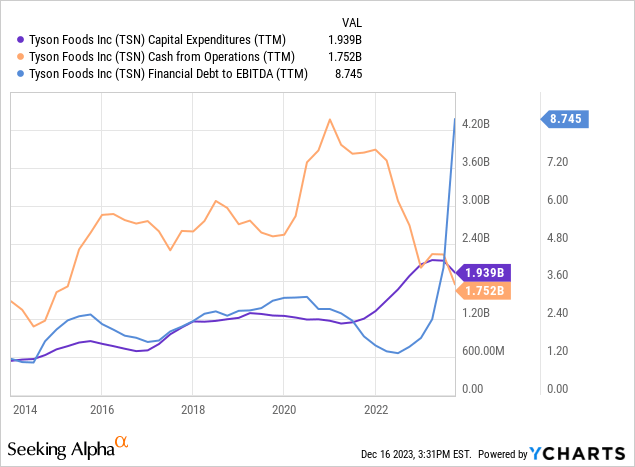

Tyson is an old company and has been operating securely for many years. However, as its cash flow dwindles and its capital expenditures rise due to needed capital upgrades, its debt-to-EBITDA appears extremely alarming. See below:

Data by YCharts

Data by YCharts

Tyson's leverage ratio would not be so problematic if its EBITDA were not compressed by its profit margin issues. That said, the company faces a $1.25B refinancing due in 2024, likely increasing its expected net interest costs by 23% to ~$400M (from in net interest expense $325M TTM). In response to this issue, Moody's recently cut Tyson's credit outlook, opening the door to potential downgrades that could increase its refinancing costs further. At this point, Tyson appears to have sufficient liquidity to enter a prolonged negative free cash flow period. Still, I expect the company will eventually need to reduce its dividend if its prospects fail to improve.

The analyst consensus currently places Tyson's EPS outlook for 2024 at $1.92, rising back to $4.4 by 2026. This gives TSN a forward "P/E" of around 11.7X to 27X. That said, I believe these estimates may not account for the potential that the meat commodity market does not normalize and that Tyson continues to struggle with labor cost growth. Thus, I see a distinct possibility that TSN's 2024-2025 profits will remain negative, potentially resulting in a dividend cut and potential balance sheet deterioration. Given that, I continue to believe TSN is materially overvalued today.

The Bottom Line

Overall, I am bearish on TSN and expect the stock to continue to lose value over the coming year. Fundamentally, I believe the company's issues are more deeply rooted than many may expect, stemming from aggressive expansion and consolidation of the meatpacking industry over recent decades, creating dislocations in the farming industry that supplies it. Further, because meat prices are rising at grocery stores, people are buying less, directly hitting Tyson's profitability. Tyson's margins are usually so thin that a small decline in meat sales and a slight rise in input costs could push the firm's margins chronically lower.

Following its recent slight rebound, I believe TSN could be an excellent short opportunity today. I expect it will return to the $45 level and potentially lower as its price adjusts for a lower long-term profit outlook. Personally, I value the company at roughly $30, giving it a three-year ahead forward "P/E" of ~7X based on analysts' outlooks, which I see as being too high. Further, such a low valuation is necessary to offset my expected loss outlook for 2024 and possibly 2025. TSN's short interest is low at ~2%, as are its borrowing costs (roughly zero), while its implied volatility is at normal levels of ~24%.

Risks in shorting TSN are numerous. For one, the company's operational efforts may indeed reduce costs and improve margins, as the firm hopes. Further, farm poultry and beef prices may reverse their trend, directly improving TSN's profit margin outlook for 2024. Personally, I do not believe the upside potential on TSN is excellent even if that occurs; however, because the stock was so popular in 2021, it could theoretically return in popularity today. Still, in my opinion, it is more likely that these margin pressures will continue and may be potentially exacerbated by credit downgrades or a dividend cut in 2024.

Comments