Summary

- Speculative growth stocks rebounded in 2023 after declines in 2022 as retail investors sought to buy growth companies at discounted valuations.

- DoorDash, Inc. stock has doubled in value this year but remains unprofitable, with notable dilution due to high stock-based compensation.

- DoorDash faces economic risks such as a potential decline in demand, labor shortages, and lower net pay for drivers, which may impact its profitability.

- The company's valuation appears relatively high with a 2027 forward "P/E" over 18X, particularly given the risk it fails to achieve this goal.

hapabapa

After experiencing tremendous declines in 2022, many speculative growth stocks have rebounded this year. Last year, the prospects of higher interest rates lowered the fair value of many pre-profit companies by increasing financing costs and reducing the present value of future cash flows. At the same time, many speculative investors from 2021 raced to take profits on the top-performing stocks, causing the boom to become a bust. However, renewed hope in 2023 has benefited most of these firms, some of which have become more profitable amid lower economic volatility.

One notable example is DoorDash, Inc. (NASDAQ:DASH), which has doubled in value this year, rising to just over $100 today. From its 2021 peak of around $250 to its 2022 trough of ~$50, the stock had lost roughly 80% of its value over about a year. Amid chronically negative net income, some likely believed the company might fail, as its short interest rose to around 7% of outstanding shares. That is not an exceptionally high figure, but it does point to a fair amount of bearish speculation on the stock, which has since slipped to 5.3% today.

DoorDash remains unprofitable but nearly broke even last quarter and is expected to earn a profit in 2024. Of course, the firm generates relatively strong operating cash flows due to tremendous stock-based compensation ("SBC"), totaling around $1B per year TTM. Investors should account for this factor because it could cause significant dilution should DASH decline in value.

Still, from a liquidity standpoint, DoorDash does not appear to be at risk of insolvency in the foreseeable future. That said, I believe its business model remains unproven, particularly in a prolonged consumer spending slowdown, which some evidence suggests is beginning today. Further, even if DoorDash becomes profitable, its valuation may be too high today, given its competitive risks.

Economic Risks Facing DoorDash

DoorDash's popularity skyrocketed during the COVID period but has continued to grow. The average delivery service customer is now spending around $407 per month, with Millennials spending an average of $575 per month. In some instances, the cost of delivery fees can be more than the cost of the food; however, usually, these service fees make up around 36% of total food delivery costs. Thus, the added convenience premium is likely around $100 to $200 monthly for most food and grocery delivery customers. Although ample, it is generally a substantial added value for most customers. Further, with around a third of American work occurring at home (with a strong skew toward white-collar workers), the ability to outsource such errands is very economical.

I believe DoorDash's most significant risk is not demand, though that will be an issue; white-collar incomes continue to decline compared to inflation. I think its most significant risk is a prolonged shortage of drivers or related labor issues. As mentioned in the last investor call, 90% of "Dashers" work fewer than 10 hours per week, with over 80% having full-time jobs. Dashers usually earn a revenue of around $18.5 per hour. Very rough estimates point toward drivers going about 12 miles per hour of work. Theoretically, it costs about $0.72 per mile to operate and maintain a new vehicle based on the government's 2022 estimates, reducing driver pay by about $8.65 in an estimated one-hour period. After this net of ~$10 per hour, we could also account for healthcare and payroll tax costs that come with contracted work, theoretically pushing net pay close to zero for many drivers (based on 2020 estimates).

Thus, for most drivers, almost all net income will ultimately come from tips, likely declining with consumer spending power. On the one hand, the low net pay for Dashers explains why the company's revenue and subscriber growth have been so substantial; it is a sizeable economic saving for many people who value their time over a minimal amount per hour. More recently, amid growing driver complaints surrounding no-tip orders, the company has begun to warn customers of delays for no-tip orders. DoorDash does not publish data on driver tip earnings, but in my view, this campaign may be one indication that the company is facing issues with drivers amid lower net pay.

Some may argue that net pay is far higher than my estimates because many drivers use older vehicles with much lower costs. That is undoubtedly true, and for many drivers, this fact will artificially boost perceived net profit. However, a full-time driver will likely add around 25K to their car per year, giving the vehicle a life expectancy of about four years, assuming it has nearly 100K. We could also account for the fact that "stop and go" inner-city driving miles usually wear a car out much faster. Of course, vehicles over the 100K mark usually have an occasionally high maintenance cost as they age. This is a very rough estimate, but my point is that many drivers may need to quit as time passes and their cars become inoperable. Driving for DoorDash with far more expensive new vehicles will likely reduce the labor economics further.

Rising vehicle costs, maintenance costs, and (until recently) gasoline also contribute to lower net pay for workers. Of course, while these inflationary factors make DoorDash a worse employment option, it also increases the number of people falling behind financially. It may need to resort to DoorDash to fill the pay gap. In an era of growing labor backlash, a shift in social or economic dynamics could reverse this trend, particularly given the tremendous pay growth for most blue-collar jobs, likely being a far better long-term alternative for workers pushed out of white-collar jobs.

To me, delivery driving is a transition job that is not sustainable at current pay levels for most people. Since 2020, many people have sought transition jobs amid economic and social changes. Still, considering so few work for DoorDash full-time, the company is at risk of tremendous labor turnover should that trend end.

DoorDash May Never Be Profitable

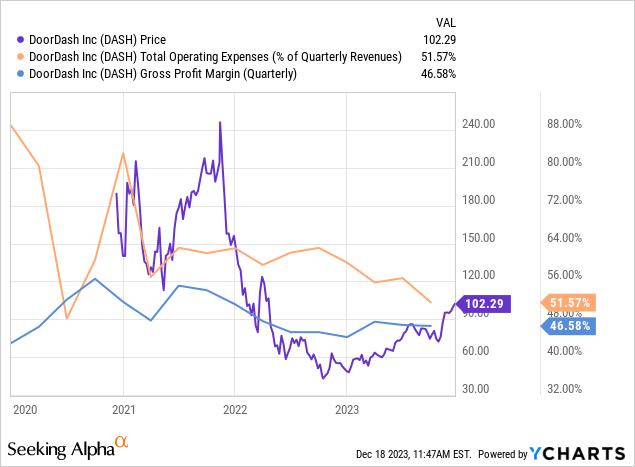

At this point, my view is not demonstrated in DoorDash's data, as it continues to have a growing number of total drivers, but some profit data points toward labor cost strains. The company's gross margins have declined since 2021, indicating potentially higher driver costs than sales. However, the firm's decline in Opex-to-sales has increased, resulting in improved operating losses. See below:

Data by YCharts

Data by YCharts

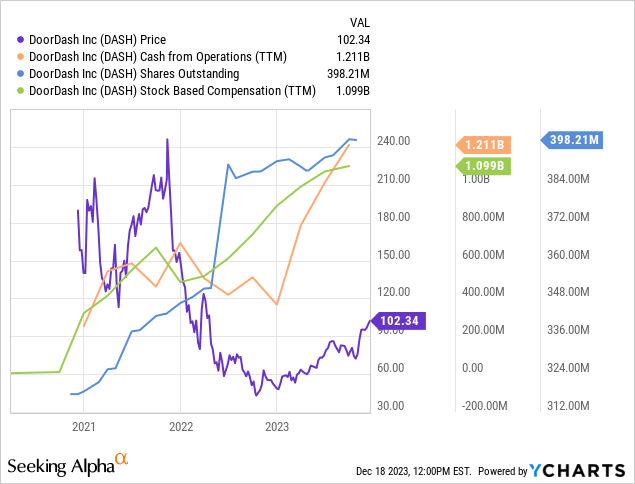

We must keep in mind that since 2020, DoorDash has operated in a tremendous environment with excellent customer demand and many people needing side-income gigs. Despite that, the company has never earned a positive operating profit outside of one quarter in 2020. Still, DoorDash does have solid operating cash flows because over $1B of its annual revenue goes to stock-based compensation. See below:

Data by YCharts

Data by YCharts

Investors should be mindful of the company's high stock-based compensation. Currently, this is diluting shareholders at a rate of about 2.75% per year, given its market capitalization. That is not a high figure, particularly given this practice keeps DoorDash in a cash-flow-positive situation. Still, if its market capitalization declines, it would dilute its equity value faster. The company has just over $2.1B in positive working capital and no long-term financial debt, giving it low solvency-related risks in the foreseeable future.

While the prospect of profits in 2024 may have encouraged investment in DASH, I fundamentally believe competition between food delivery companies will make it difficult to sustain those profits. Customers will always gravitate toward the lowest-cost service, while drivers will gravitate toward those with the highest pay. Without any moat, there is no reason to expect profits to be sustainable, given basic economic laws.

Still, even if we consider the consensus profit outlook for DASH, it does not appear fairly valued today. Analysts expect the company's EPS will rise to about $5.6 annually by the end of 2027, giving it a forward "P/E" of 18.3X based on that long-term outlook. That valuation is based on four years ahead of EPS expectations, which is usually low given the time and risk horizon. That is a very high valuation, particularly given it is uncertain (and, to me, unlikely) that DASH will ever achieve a $5+ EPS level.

The Bottom Line

Overall, I am bearish on DoorDash, Inc. shares due to a variety of factors. For one, I believe the stock is overvalued by around 50% to 100% and, therefore, should trade at a price of about $51 to $68, which would give it a much more reasonable "2027" forward "P/E" of 9.1X to 12.1X. To me, that valuation range better accounts for the company's risk and the time value of money. Still, stocks can continue to rise in value even if overvalued.

In my view, it is generally unlikely DASH will continue to rebound in 2024 due to the high probability of economic shifts that either lower demand or reduce the company's active driver count. To me, that is a significant enough catalyst to make me bearish on the stock, but it is not so strong that I am willing to short-sell it today. While I fundamentally believe the company's business model will never deliver stable profits, it has strong liquidity and decent investor interest that can offset that issue for a long time. However, if its operating cash flow dwindles, I may be more willing to bet against DASH directly.

Comments