Summary

- Barrick Gold Corporation reported strong Q3 financial results, with over one million ounces of gold produced and a significant increase in free cash flow.

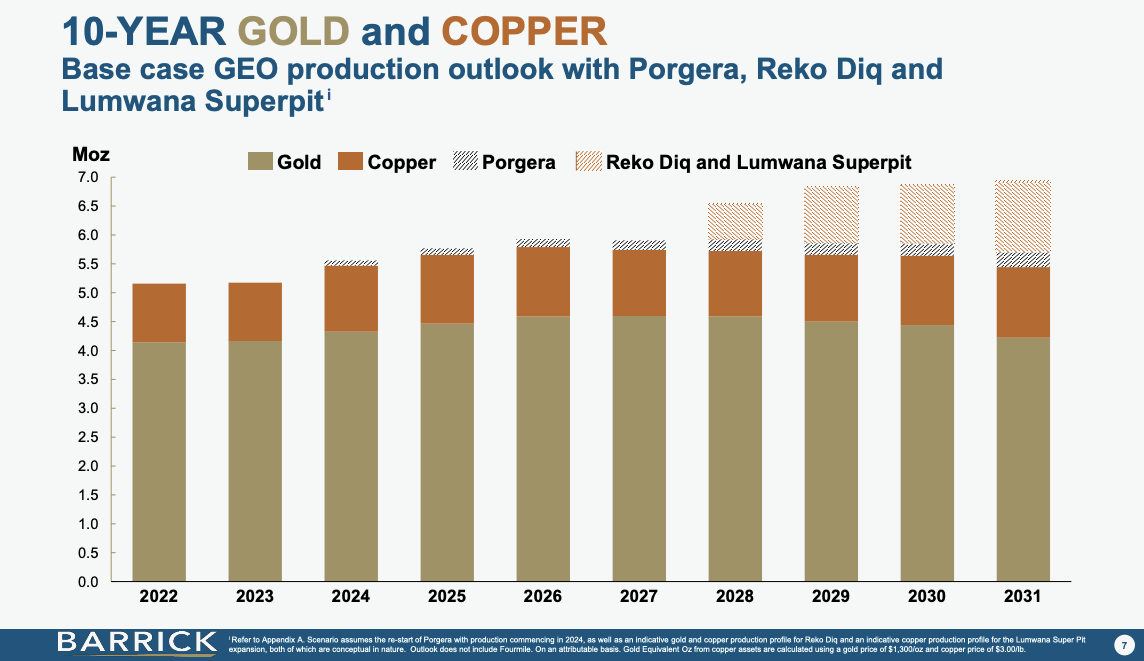

- The company is focused on substantial long-term growth, expecting a 30% increase in gold-equivalent ounces by the end of the decade.

- Barrick's Porgera mine in Papua New Guinea is expected to recommence gold production in early 2024, while the Goldrush underground mine in Nevada is set to begin production in the same year.

Oselote

Is Barrick Gold Ready To Shine In 2024?

This article is an update on Barrick Gold Corporation (NYSE:GOLD), one of the biggest gold miners in the industry by market cap. It recently disclosed its Q3 2023 financial results and announced an update on two key gold mines (Goldrush and Porgera).

Additionally, Barrick has been in the news lately, as Barron’s has listed Barrick as one of its top 10 favorite stocks for 2024. This is quite surprising, given that precious metals miners rarely make these kinds of lists, and Barrick is named alongside popular stocks like Berkshire Hathaway (BRK.A, BRK.B), Alphabet (GOOGL), and PepsiCo (PEP).

So, what has changed since my last update, and is Barrick stock still a buy? Let’s dig deeper.

Barrick’s Q3 Financial Results

Barrick Gold

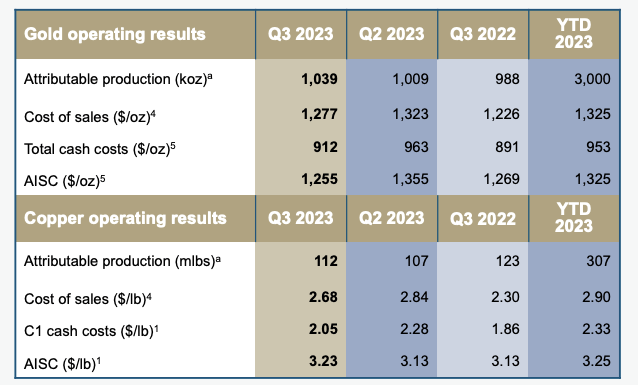

Barrick Gold's Q3 results last month highlighted a strong performance. The company produced over one million ounces of gold at an all-in sustaining cost of $1,255 per ounce. This cost is a $100 reduction from the previous quarter and slightly lower than Q3 2022, and, therefore, Barrick was able to generate substantial earnings and cash flow.

Barrick achieved net earnings of $368 million, translating to $0.21 per share, which is a $0.04 increase from the previous quarter. Impressively, the company also reported a significant increase in free cash flow, reaching $359 million.

Also during the quarter, notable mine improvements were seen in key mines such as Cortez, Turquoise Ridge, and Kibali. Progress was also made in the Environmental Impact Statement for the Goldrush project, with a formal notice published on October 27.

One negative update in Q3: The Pueblo Viejo mine's ramp-up has been slower than expected, and the company is actively addressing equipment issues there. Despite these challenges, Pueblo Viejo is anticipated to produce over 800,000 ounces in 2024.

Barrick’s Excellent Growth Profile

Barrick Gold

Looking ahead, Barrick is focused on substantial long-term growth, expecting a 30% increase in gold-equivalent ounces by the decade's end to nearly 6.5 million gold equivalent ounces.

Major growth projects like the Reko Diq mine in Pakistan and the Lumwana mine expansion in Zambia appear to be advancing steadily, with both projects aligning construction and production timelines.

Barrick is also enhancing its copper portfolio, with Reko Diq projected to be a top global copper producer and Lumwana expected to yield 240,000 tonnes annually.

In addition, the company's financial health remains robust, with Barrick finishing the quarter with $4.26 billion in cash and cash equivalents, compared to $4.77 billion in debt - therefore, giving it a net debt position of $514 million, which is conservative for a company of its size. These strong financials support Barrick’s investment in growth projects.

Barrick’s Latest Mine Updates

Porgera Mine

Barrick Gold Corporation recently announced that its Porgera mine in Papua New Guinea is gearing up to restart operations later this month, with the expectation of recommencing gold production in early 2024. This development comes after finalizing the terms of the Porgera Project Commencement Agreement, which included establishing a new ownership structure for the mine.

Mark Bristow, Barrick's president and CEO, recently expressed optimism about the mine's future, highlighting its alignment with the company's successful host-country partnership model, previously implemented in Tanzania and the new Reko Diq project in Pakistan.

Barrick Gold Corporation holds high expectations for the Porgera mine, projecting it to reach the status of a world-class producer and potentially become a part of its prestigious Tier One gold mine portfolio.

To achieve this status, according to Barrick Gold the Porgera mine is expected to meet specific criteria:

- It should have a lifespan of at least 10 years;

- Produce a minimum of 500,000 ounces of gold annually;

- Maintain all-in-sustaining costs per ounce that are among the lower half in the industry. This would have obvious benefits to Barrick’s earnings and cash flow.

This ambitious goal set by Barrick reflects their confidence in the Porgera mine's potential to deliver significant and efficient gold production.

It should also generate huge benefits for Papua New Guinea, with Barrick estimating $7 billion in value creation over 20 years (assuming a gold price of $1,800/oz).

Goldrush

The US Bureau of Land Management's approval of Nevada Gold Mines' (“NGM”) Goldrush underground mine is another bullish development for Barrick Gold’s stock.

The mine, located in Nevada’s Cortez Complex, is set to begin production in 2024 and is expected to significantly increase its output, reaching an estimated 400,000 ounces annually by 2028.

Barrick, a major operator of NGM, has already invested over $370 million in Goldrush, with total expected investment nearing $1 billion, according to the company.

This development is bullish for Barrick’s stock for several reasons:

- Increased production. The ramp-up to 400,000 ounces per year substantially boosts Barrick's gold production volume.

- Growth potential. The addition of Goldrush to Barrick's portfolio, already boasting three Tier One mines, underscores the company's potential for continued expansion and growth, making it an attractive option for investors looking for long-term value in the mining sector.

- Local economic benefits. According to Barrick, approximately 500 construction jobs and 570 operational jobs will be created, positively impacting the local economy and potentially fostering community support and stability for the project.

Overall, the approval and progress of the Goldrush project signal a strong growth trajectory for Barrick.

Barrick Gold: The Bottom Line

As the year draws to a close, Barrick Gold emerges as a strong contender in the mining sector, with its strong earnings, a healthy balance sheet, and significant production growth coming from two key mines. The company is poised for impressive growth, with an estimated production increase of around 30% in the next 5-7 years.

Another crucial advantage for Barrick lies in its leverage to rising copper prices, thanks to substantial production at its mines. This aspect could become increasingly valuable, considering the anticipated copper supply deficit in the coming years.

Financially, Barrick stands on solid ground with a manageable net debt of just $514 million. While its valuation isn't the lowest in the mining sector, I think Barrick Gold Corporation remains attractive when considering the high quality of its assets and growth potential. This supports my continued BUY recommendation for 2024.

Comments