Summary

- Telephone and Data Systems preferred stock has outperformed the S&P 500 with a total return of 38% in about seven months and still offers a high dividend yield.

- The decrease in inflation and the outlook for interest rate reductions until 2026 provide a strong catalyst for preferred stocks like Telephone and Data Systems.

- The company's high debt load and weak business momentum pose risks to the preferred dividend, despite potential sale of the stake in US Cellular.

jamesteohart

About seven months ago, I rated the preferred stock of Telephone and Data Systems (NYSE:TDS.PR.V) as a "hold", as the stock was offering an exceptionally high dividend yield of 13.0% but it also had some material risks. Since my article, the stock has offered a total return of 38% and thus it has outperformed the S&P 500, which has gained 8%, by an impressive margin. The preferred stock of Telephone and Data Systems is still offering a remarkably high dividend yield of 9.7%. In addition, after such a steep rally, some investors may conclude that the risks have faded and hence they should buy the stock for its still attractive yield.

However, the rally has resulted from the decrease in inflation and the resultant outlook for many interest rate reductions until 2026, as lower interest rates provide a strong catalyst for preferred stocks. The risks related to the high debt load of Telephone and Data Systems remain in place, as evidenced by the last earnings report of the company, in early November. Investors should be well aware of these risks before deciding to lock in the outstanding yield of the preferred stock.

Interest rates

There has been a significant improvement in the outlook of interest rates and the policy of the Fed since my aforementioned article. Until late October, inflation had proved somewhat sticky and thus there were many "experts" who were making forecasts for many more interest rate hikes by the Fed this year. The CEO of JPMorgan Chase (JPM) projected interest rates of 7% at some point this or next year.

However, the aggressive policy of the Fed finally began to bear fruit. Inflation has decreased from a 40-year high of 9.1% in the summer of 2022 to 3.1% now. As the interest rate hikes of the Fed take about a year to have a cooling effect on the economy, it is only natural that the policy of the Fed has finally begun to bear fruit. Thanks to the steep decrease in inflation, it is reasonable to expect inflation to revert to the target zone of 2.0%-2.5% of the central bank at some point this or next year.

This helps explain the recent shift of the Fed to a more dovish policy. Last month, the Fed provided guidance for three interest rate reductions this year, four reductions in 2025 and another three reductions in 2026. If the central bank executes as per its guidance, it will restore interest rates to its long-term target of 2.0%-2.25% in 2026.

Such a development will provide a great catalyst for the preferred stock of Telephone and Data Systems. Despite its recent rally, the stock is still trading at a 38% discount to its par value of $25, largely due to the 16-year high-interest rates prevailing right now. High interest rates enable investors to identify high yields in many securities and hence they exert pressure on the prices of preferred stocks. Therefore, if interest rates decrease as per the guidance of the Fed over the next three years, they will provide a strong tailwind to the preferred stock of Telephone and Data Systems and will help the stock retrieve a significant portion of its losses over the last two years.

Liquidity risk

If interest rates were the only determinant of the future path of the preferred stock of Telephone and Data Systems, I would attach a "strong buy" rating to the stock. However, a material portion of the deep discount of the stock to its par value has resulted from the excessive debt load of the telecommunications company.

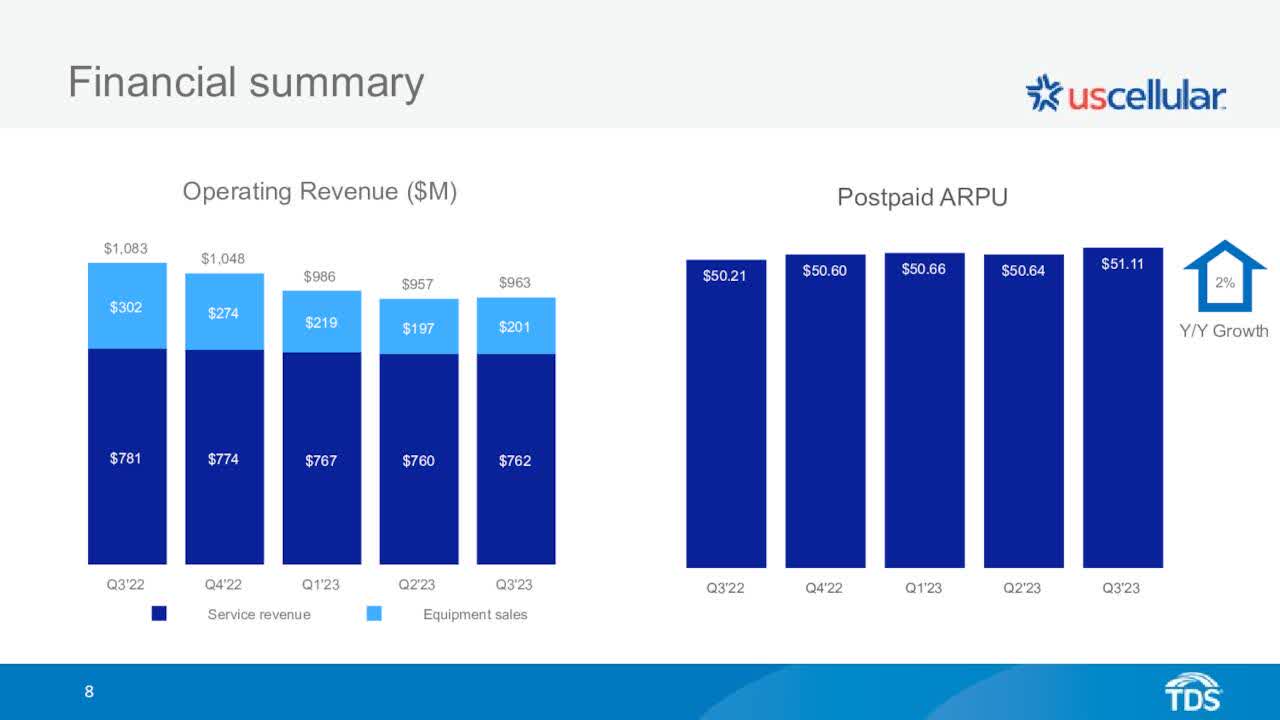

Telephone and Data Systems offers cellular and landline services, wireless products, cable, broadband, and voice services to about 6 million customers across the U.S. The company owns approximately 83% of US Cellular. This part of the business generates 74% of the total operating revenue of the company and hence it is paramount for the entire company.

Telephone and Data Systems is going through a rough period, partly due to intense competition. The revenue of US Cellular has steadily declined in each of the last four quarters while its postpaid average revenue per user has barely grown.

US Cellular - Financial Summary (Investor Presentation)

In the third quarter, Telephone and Data Systems saw its revenue decrease 8% over the prior year's quarter and posted a loss per share of -$0.16. The company has posted losses for five consecutive quarters and has missed the analysts' estimates by a wide margin in each of these quarters. This performance does not bode well for a potential turnaround anytime soon.

It is also important to note that Telephone and Data Systems carries an excessive debt load on its balance sheet. Its net debt (as per Buffett's formula: net debt = total liabilities - cash - receivables) is currently standing at $6.6 billion. This amount is 3.3 times the market capitalization of the stock and hence it is undeniably excessive.

The impact of the weak balance sheet is clearly reflected in the income statement of the company. Interest expense has exceeded operating income by a wide margin in each of the last two years. Moreover, the company will have to refinance a significant portion of its debt in the upcoming years. As it will refinance its debt at nearly 16-year high interest rates, its interest expense is likely to increase even further.

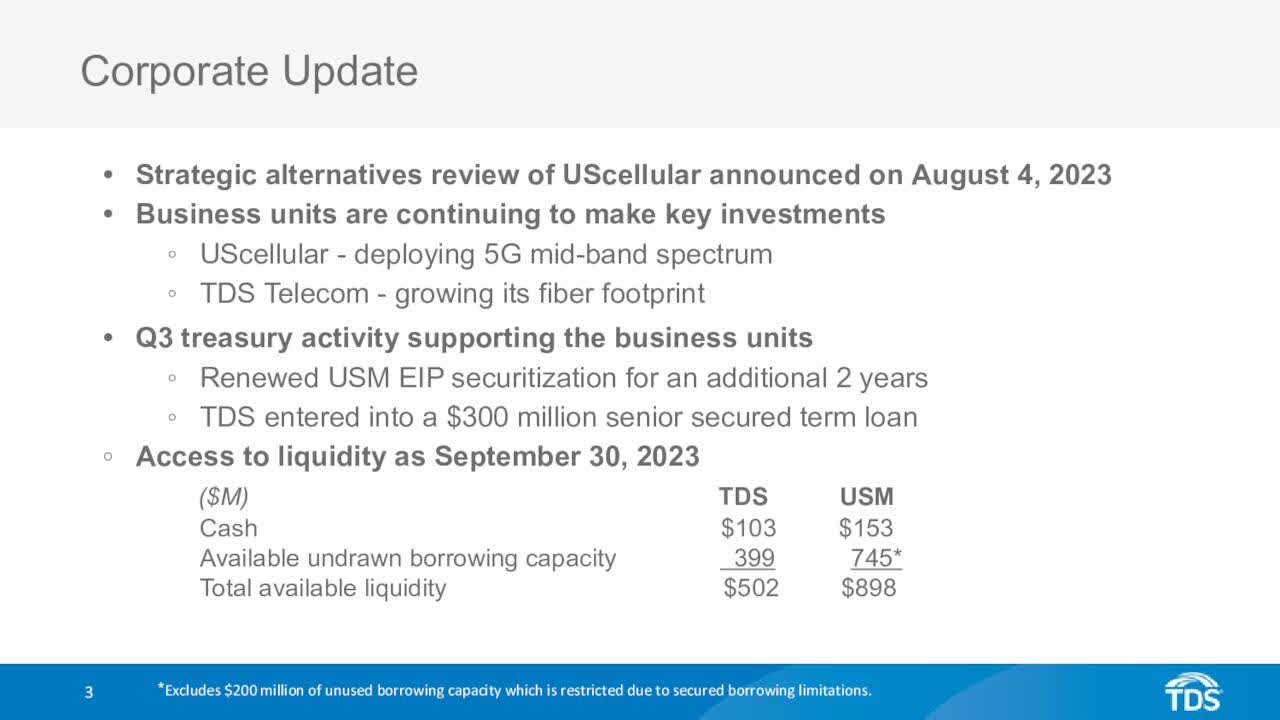

It is also worth noting that Telephone and Data Systems stated that it had a total available liquidity of $502 million in the first slide of its latest earnings call presentation.

Telephone and Data Systems - Investor Update (Investor Presentation)

When a company provides liquidity metrics in the first slide of its presentation, it sends a strong signal to investors that it struggles to meet its financial obligations. Investors should definitely receive this message from the above presentation.

Analysts have certainly taken note of the weak business momentum and the high debt load of Telephone and Data Systems. They expect the company to post material losses per share in every single year between 2023 and 2026. If they prove correct, the company will post a loss for a fifth consecutive year in 2026.

At this point, investors should be aware that the preferred dividend is much safer than the common dividend of Telephone and Data Systems. The company cannot cut its preferred dividend unless it first eliminates its common dividend. It is also impressive that Telephone and Data Systems has raised its common dividend for 49 consecutive years. Unfortunately, given the recurring losses of the company and its high debt load, the common dividend is likely to be cut sooner or later. On the other hand, the common dividend may not be eliminated and hence the preferred dividend has a meaningful margin of safety.

Even better, on November 10th, Telephone and Data Systems announced that it had managed to attract interest for its stake in US Cellular. Verizon (VZ), AT&T (T), T-Mobile (TMUS), and some private equity firms showed interest in acquiring the towers of Telephone and Data Systems. This is a positive development in reference to the debt load of the company. That's why the preferred stock jumped 18% on August 4th, when the company first reported that it would try to find strategic alternatives for its stake in US Cellular.

Given the interest of many companies in the towers of Telephone and Data Systems, the company has a good chance of selling its stake in US Cellular and thus greatly reducing its debt load. However, it is impossible to predict the financial capacity of the resultant company, which will have much higher liquidity but will also be a much smaller company, with poor business momentum. Overall, the preferred dividend of Telephone and Data Systems appears safer than it was a year ago thanks to the high odds of a sale of the stake in US Cellular but there is still high uncertainty over the value of a potential deal and the financial strength of the resultant company.

Final thoughts

The 9.7% preferred dividend of Telephone and Data Systems is much safer than the common dividend of the stock, particularly after the aforementioned efforts of the company to sell its stake in US Cellular. Nevertheless, it is impossible to predict whether this sale will materialize and at what price. The company has not mentioned any potential amounts regarding this sale. Therefore, given the high debt load of the company, investors should be aware that the preferred dividend is not safe.

Comments