Summary

- Gold is one of the top-performing assets in 2024, with a strong surge as the Japanese Yen crumbles.

- Gold miners, such as Agnico Eagle Mines, have performed well, outperforming peers Newmont and Barrick, which are seeing costs rise too quickly.

- Agnico's lower jurisdictional risk significantly benefits its peers, as the gold bull thesis largely implies increased political and economic unrest in developing countries.

- Based on an updated income estimate, I believe AEM's forward "P/E" today is closer to 12X to 13X.

- While I am neutral on most large gold miners, I believe AEM's advantage should continue in the long run.

Vitoria Holdings LLC

Gold is one of the top-performing assets in 2024, boasting a ~16% return YTD. Gold miners have also performed decently, with the gold miner ETF (GDX) rising similarly. As detailed recently regarding Newmont (NEM) and the large miner ETF GDX, I prefer gold ETFs such as (GLD) to miners. Although miners will likely rise with gold, their production costs are rising too quickly compared to gold, and many are not seeing equal profit growth.

My neutral outlook on miners primarily focuses on those with significant operations in developing countries, particularly in Africa and South America, experiencing increased labor, political, and economic unrest. Year after year, it seems more companies operating in these regions face worker strikes, outages, and other issues leading to higher operating costs. Should currencies in those regions continue to devalue at their current pace, or if energy commodities rise, then I expect all gains or more from higher gold and silver prices will go to increased costs or operating issues.

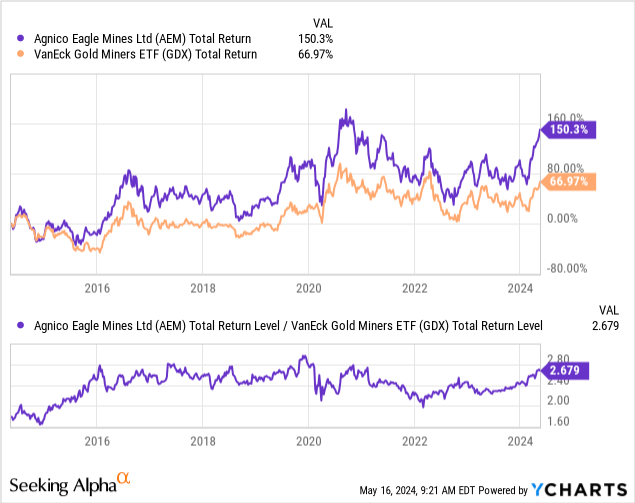

That said, mining companies operating in developed countries, such as Agnico Eagle Mines (NYSE:AEM), which is primarily focused on Canada but has some operations in Mexico, Finland, and Australia, seem to be performing better. AEM is up ~26% YTD, far more than its peers Newmont (4%) and Barrick (GOLD) (-4%). See below:

Data by YCharts

Data by YCharts

Agnico is on a very strong relative performance trend compared to the industry. It underperformed the gold mining index from 2020 to 2022 but has recovered since then, marking far superior returns as it has managed to keep its production costs from rising as quickly as its peers.

Fundamentally, I'd invest in gold miners rather than GLD because they have physical assets and usually offer some price leverage to gold. That said, gold miners with unstable production and skyrocketing costs are problematic, as their mines are not necessarily secured from the whims of the growing number of unstable governments in some regions. As such, I believe Agnico deserves closer inspection to assess its value potential.

Production Costs Rising, But Not So Quickly

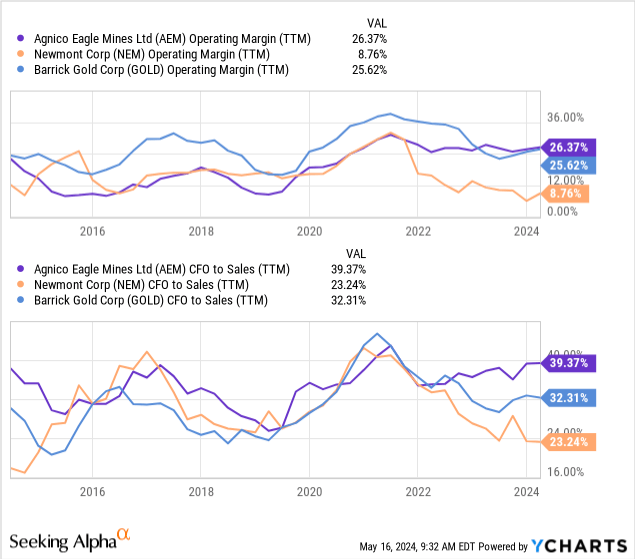

The critical issue with Newmont and Barrick is the rapid increase in their all-in-sustaining costs, "AISC." Newmont had an AISC in the mid-$900/oz in 2019 and reported that it expected to maintain that level through 2023. That did not go as planned, as its AISC was $1485/oz during Q4 of 2023, offsetting most gains from higher gold prices.

Agnico's was also in the mid $900/oz range in 2019, but was only $1,117/oz in 2023 and ~$1,225/oz for its 2024 guidance. Thus, the company has far more stable production cost growth, giving it more significant profit margins and, more importantly, improved stability to its peers. See below:

Data by YCharts

Data by YCharts

Historically, because AEM is more focused on developed markets, particularly Quebec and Ontario, it has had lower margins due to higher labor costs. However, the opposite is true today, as its more centralized footprint and a more economically stable area have made its margins more stable and higher. In general, it is reasonable to expect this trend to continue, with AEM likely benefiting more than its peers from higher gold prices.

Higher gold prices usually mean fiat currencies are devaluing around the world. That is the case today, particularly in developing markets but also in other key markets like Japan. Should we see the wave of currency instability that many gold bulls expect, we will also see a wave of social and economic instability that inevitably comes from higher sustained inflation. I feel that gold miners often underappreciate jurisdictional risk, mainly when the gold bull thesis implies increased political risk. However, I think AEM's track record of AISC stability significantly mitigates this issue.

What is Agnico Eagle's Fair Valuation Today?

Fair value for gold miners can be tricky as it depends on the expected price and profitability of precious metals mining, with discounting for leverage and operational risk factors. Agnico deserves some premium from its peers due to its lower jurisdictional risk. Further, its net liabilities are around 21% of its Enterprise Value, compared to 34% for Barrick and 36% for Newmont. There are similar differences in other leverage measures, showing equity holders in AEM have a larger share of the pie than the other two.

Agnico's 2024 guidance gives it a 3.45Moz gold production outlook at a $1,225/oz AISC. Today's gold price of $2,375/oz implies a considerable margin of ~$1,150/oz. Assuming these levels remain, that equates to an expected pre-interest and tax profit of ~$3.97B. Significantly, that measure is based on its maintenance CapEx, not its appreciation, so it is non-GAAP but likely more reflective of its true expected sustained profit level.

Deducting $101M from net non-operating interest and assuming a 30% effective tax rate, we arrive at an expected non-GAAP profit of ~$2.71B. The company did earn an added ~$80M in revenue from byproduct sales of silver, zinc, and copper. While I could add some portion of that to its income, the net effect is likely immaterial and, if anything, offsets the likelihood that its AISC will be higher than expected (which is often the case). So, with gold prices where they are now, I value AEM based on a $2.71B expected forward income.

With a market capitalization of $34B, that gives AEM a low "P/E" of 12.5X. Technically, its forward "P/E" based on the consensus earnings outlook is 22.6X, with the market assuming a smaller earnings increase that will fade by 2027. Those estimates were likely made earlier this year, when gold was around $400 lower than it is today. The increase in gold prices has dramatically improved AEM's profit outlook.

The Bottom Line

Combined with its low leverage and its much lower jurisdictional risk, I like AEM and have a bullish outlook on it. To me, it is a much better risk-reward opportunity than Newmont and Barrick, mainly due to its more stable AISC, which I believe is a considerable risk factor as fiat currencies struggle compared to gold.

Now, this is not to say AEM is necessarily low risk. For one, as I discussed regarding GDX, gold is trading at a massive premium compared to its implied real interest rate price, which is around $1,200/oz. Usually, high real interest rates, or the net return on long-term Treasuries after inflation, are associated with low gold prices. Indeed, if fiat currency investments offer an excellent post-inflation return, gold should not be worthwhile as it does not promise to outperform inflation.

There are many reasons why this anomaly may have appeared. For one, China and other central banks are stockpiling gold tremendously. China, other central banks, and many wealthy people feel it is good to buy gold today to hedge against a potential future increase in global inflation. Indeed, although inflation has slowed, I argue that inflation will need to remain high for a sustained period with the US debt so high and its infrastructure aged. As such, the actual interest rate figure may be inaccurate, assuming inflation will spike again over the coming decade. Still, although I remain bullish on gold, I am preferential to silver (SLV) and Platinum (PPLT) because they lack this premium.

Aside from falling gold prices, Agnico is not immune to operational risk. Although its operating risks are lower than those of its peers, rising energy and labor costs may still affect its profitability. This is something to consider, but as long as crude oil does not spike dramatically, I am not too concerned by it. I am bullish on AEM and believe its fair value is around $42 per share, equating to a forward "P/E" of 15-16X based on my earnings estimates. Further, I think its upside to higher gold prices is greater than its peers, making it a superior long-term gold bull trade.

Comments