Summary

- Old Dominion Freight Line, Inc. is a standout in the trucking industry with unique strengths in the less-than-truckload segment.

- Impressive growth, efficient operations, and strong financials have positioned Old Dominion Freight Line for continued success despite the recent stock price dip.

- Potential demand recovery could lead to strong returns and dividend growth, making Old Dominion Freight Line stock a promising investment opportunity.

ablokhin

Introduction

It's time to talk about Old Dominion Freight Line, Inc. (NASDAQ:ODFL), a company that has become one of my favorite dividend growth stocks on the market.

After covering the company for many years, this is my first article on the stock I'm writing as a shareholder, as I bought the company earlier this year, which I revealed in an article titled "A New Portfolio Addition! I Just Bought These 2 Dividend Growers."

My most recent in-depth article on ODFL was written on April 30, when I called it a "Dividend Growth Stock That Keeps On Winning."

Ironically, since then, shares are down 2.5%, lagging the 7.3% return of the S&P 500 (SP500) by a substantial margin.

The good news is that the current downtrend was the trigger for me to finally pull the trigger, as I now have an average entry of slightly less than $172 per share, roughly 25% below its all-time high.

Data by YCharts

Data by YCharts

In this article, I'll revisit my thesis, assess the risk/reward, and explain why ODFL remains one of my favorite holdings.

So, as we have a lot to discuss, let's get to it!

A Company With An Impressive Edge

Most readers may know that I don't really like the trucking industry. Trucking is competitive and prone to countless risks like labor shortages, inflation, railroad competition, and others.

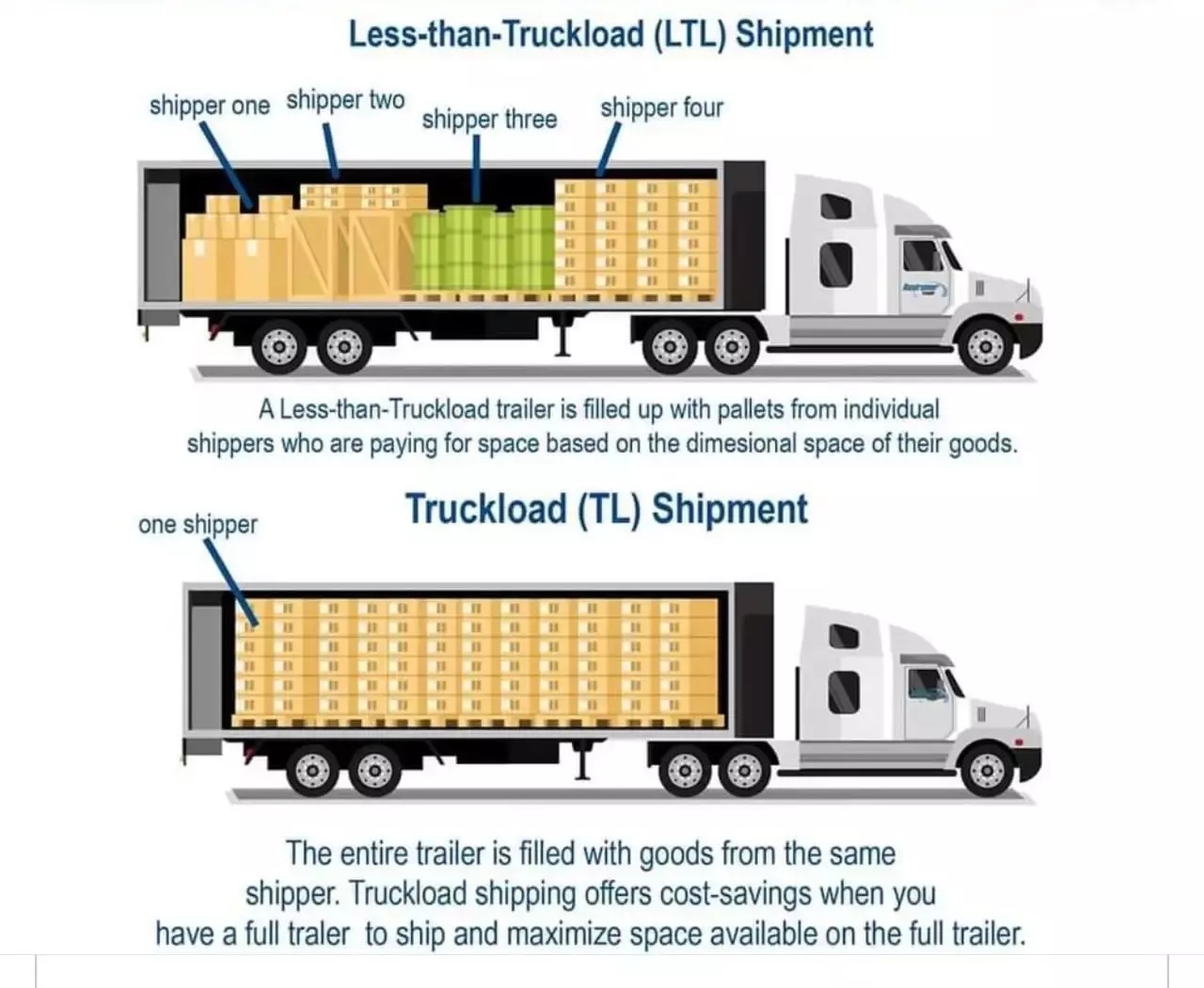

The good thing is not all trucking companies are the same. ODFL is an LTL (less than truckload) company, not a TL (truckload) company.

PACK & SEND

Unlike TL companies, LTL companies do not simply ship a load of goods from point A to point B for a specific customer.

LTL companies carry goods from multiple customers at the same time, which means they need to rely on very efficient planning.

The trucking industry is comprised principally of two types of motor carriers: LTL and truckload. LTL freight carriers typically pick up multiple shipments from multiple customers on a single truck. The LTL freight is then routed through a network of service centers where the freight may be transferred to other trucks with similar destinations. LTL motor carriers generally require a more expansive network of local pickup and delivery (“P&D”) service centers, as well as larger breakbulk, or hub, facilities. In contrast, truckload carriers generally dedicate an entire truck to one customer from origin to destination. - ODFL 2023 10-K (emphasis added).

ODFL has perfected the art of LTL trucking, as it has built an impressive network of (mostly owned) service centers and a strong company culture that has resulted in mind-blowing growth.

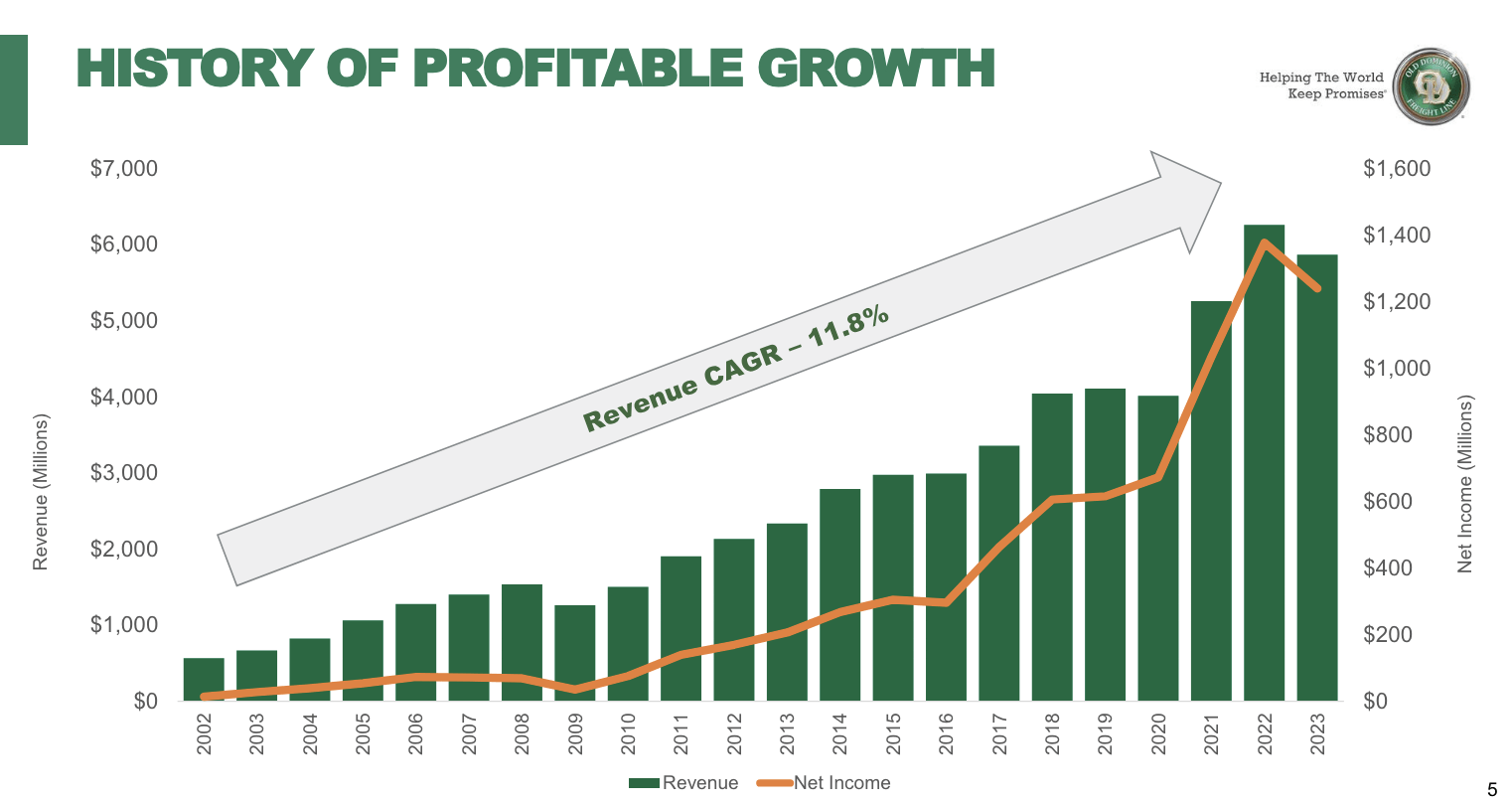

In the 2002-2023 period, the company has grown its revenues by 11.8% annually - almost entirely organic. During this period, it has grown its market share from roughly 3% to 12%.

Old Dominion Freight Line

During its first-quarter earnings call, the company noted that despite industry challenges like excess capacity and competitive pressures, it is using its strategic advantages to outperform, which includes the bankruptcy of the Yellow Corporation.

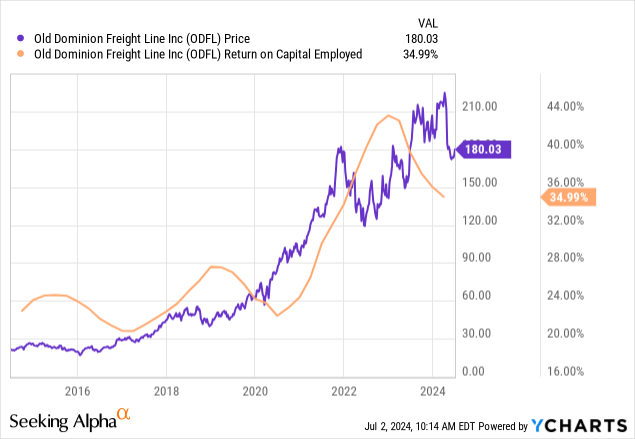

Moreover, the giant has a return on invested capital of more than 30%, which is a blowout number and one of the reasons why the stock price went up more than 660% over the past ten years.

Data by YCharts

Data by YCharts

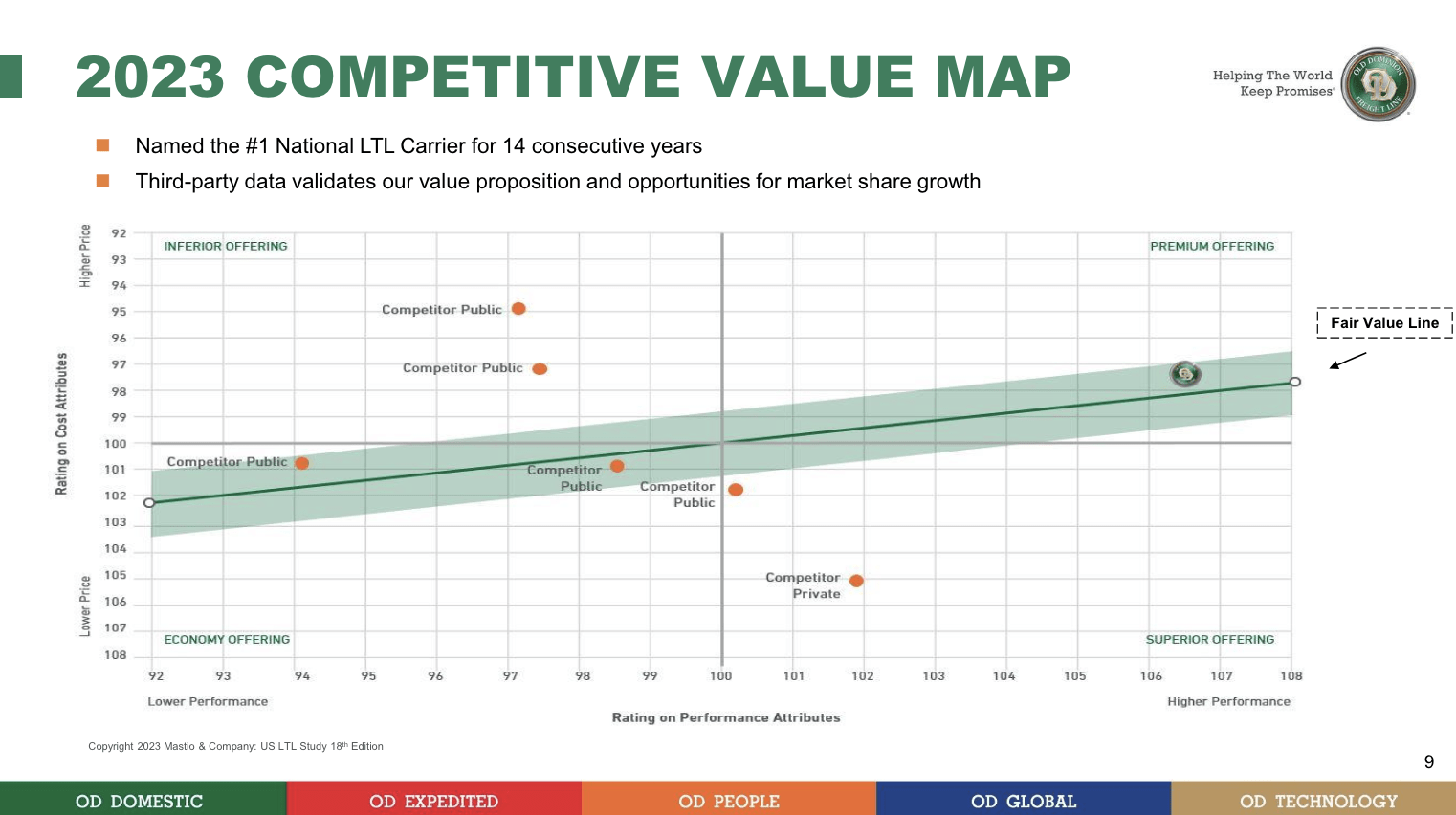

Another thing I need to mention before we dive into more recent results is the fact that all of this was made possible by a great mix of service quality and pricing.

Even LTL trucking is highly competitive - just less competitive than TL transportation.

ODFL has managed to provide superior service quality, which provides the company with a narrow moat (that's unique in its industry) and pricing power.

Old Dominion Freight Line

Especially in times when others are struggling (like the aforementioned Yellow bankruptcy), the company can use pricing power to grow, which is one of the reasons why it has a low 70% operating ratio.

Moreover, to quote my prior article, it started to pay a dividend in 2017 and has a pristine balance sheet:

- It has a pristine balance sheet. The company ended the first quarter with roughly $500 million in net cash (more cash than gross debt). Analysts expect the company to boost that number to $1.5 billion by the end of 2026.

- The company has bought back 16% of its shares over the past ten years, as a healthy balance sheet and successful operations have created a lot of excess cash.

- In 2017, the company started paying a dividend. Although its 0.6% dividend yield is not exciting for income-focused investors, it comes with a five-year CAGR of 36% and a payout ratio of just 15%. This bodes well for future dividend growth.

Data by YCharts

Data by YCharts

Having said all of this, the question is:

Has ODFL Bottomed?

On June 5, ODFL released a second-quarter update, which was very upbeat.

- Revenue per day increased 5.6% compared to May 2023 due to a 1.5% increase in LTL tons per day and an increase in LTL revenue per hundredweight.

- The change in LTL tons per day was attributable to a 2.3% increase in LTL shipments per day, which was partially offset by a 0.7% decline in LTL weight per shipment.

- On a quarter-to-date basis, LTL revenue per hundredweight and LTL revenue per hundredweight, excluding fuel surcharges, increased 4.2% and 4.7%, respectively. That's on a year-over-year basis.

In other words, both stronger volumes and pricing!

This is how Marty Freeman, President and CEO of the company, put it:

Our revenue results for May include increases in both our volumes and yield. We are pleased with the ongoing improvement in our LTL revenue per hundredweight, which reflects our consistent, cost-based approach to pricing as well as stability in the overall pricing environment.

These improvements make sense, as TruckingDive reported that LTL was performing much better than TL at the end of May.

LTL rates made year-over-year gains in April, with the Bureau of Labor Statistics’ Producer Price Index for LTL long-distance trucking increasing 8.2% year over year. - TruckingDive.

In general, we are seeing structural improvements as prices are rising faster than capacity. This is a clear indication of fading excess capacity and more industry pricing power.

All else being equal, that's bullish.

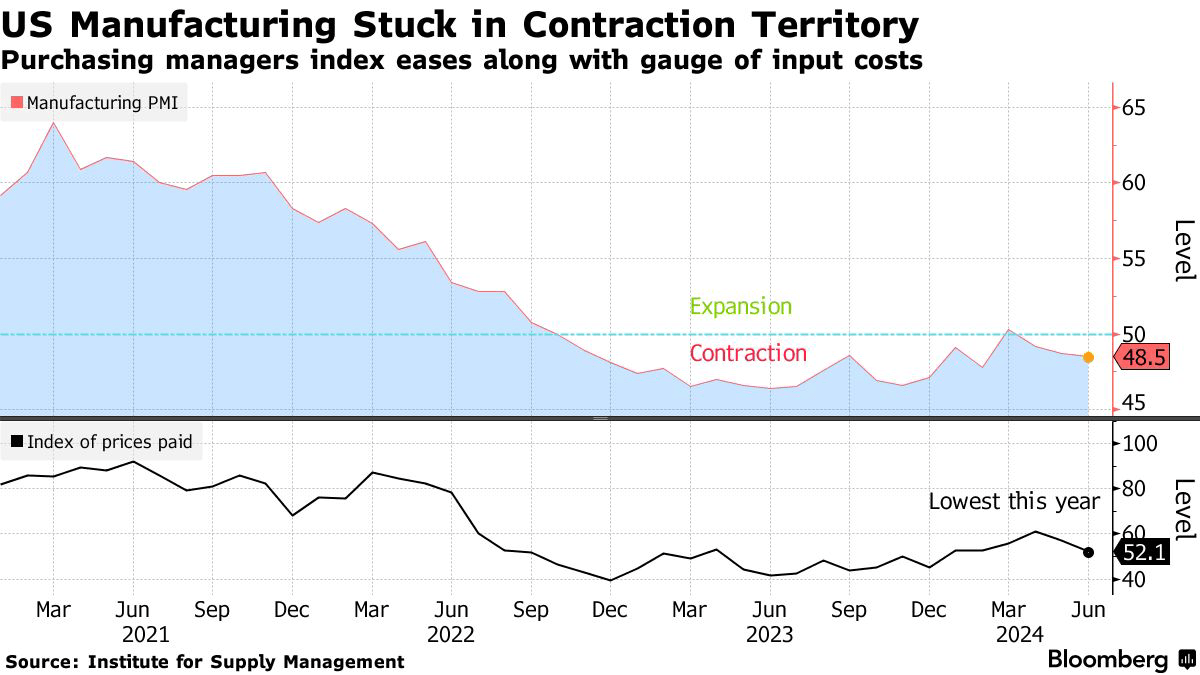

Logistics Managers' Index

Unfortunately, the latest data from the ISM Manufacturing survey (see below) hints at renewed weakness in the manufacturing sector, which could keep a lid on the general recovery in freight demand (LTL is dependent on industrial output).

Bloomberg

Nonetheless, the developments in LTL are promising and likely hint at stronger underlying demand, which could translate to higher orders if companies are indeed almost finished with inventory de-stocking.

If that happens, ODFL expects to push its operating ratio below 70%.

This is based on a number of factors, including investments in growth. This year, ODFL is expected to invest $750 million in growth, slightly down from $757 million in 2023.

These investments have resulted in roughly 30% excess capacity in its service centers.

In other words, the moment demand improves, it can service this demand without needing to boost investments in growth. This is highly beneficial for the next upswing - especially because it still kept its operating ratio at just 73.5% in 1Q24.

Higher demand without the need to boost costs will almost certainly result in a decline in the operating ratio.

In the Q&A session of its 1Q24 call, the company explained it aims for a sub-70% operating ratio. It achieved this in 2022 and will likely achieve it again if demand improves.

Given the company's recent price action, it seems the market is slowly starting to bet on a bottom.

Unfortunately, the stock seems to be bottoming at a somewhat lofty valuation, as ODFL is trading at a blended P/E ratio of 31.0x, above its long-term normalized P/E ratio of 22.7x.

Its ten-year average P/E ratio is 26.3x.

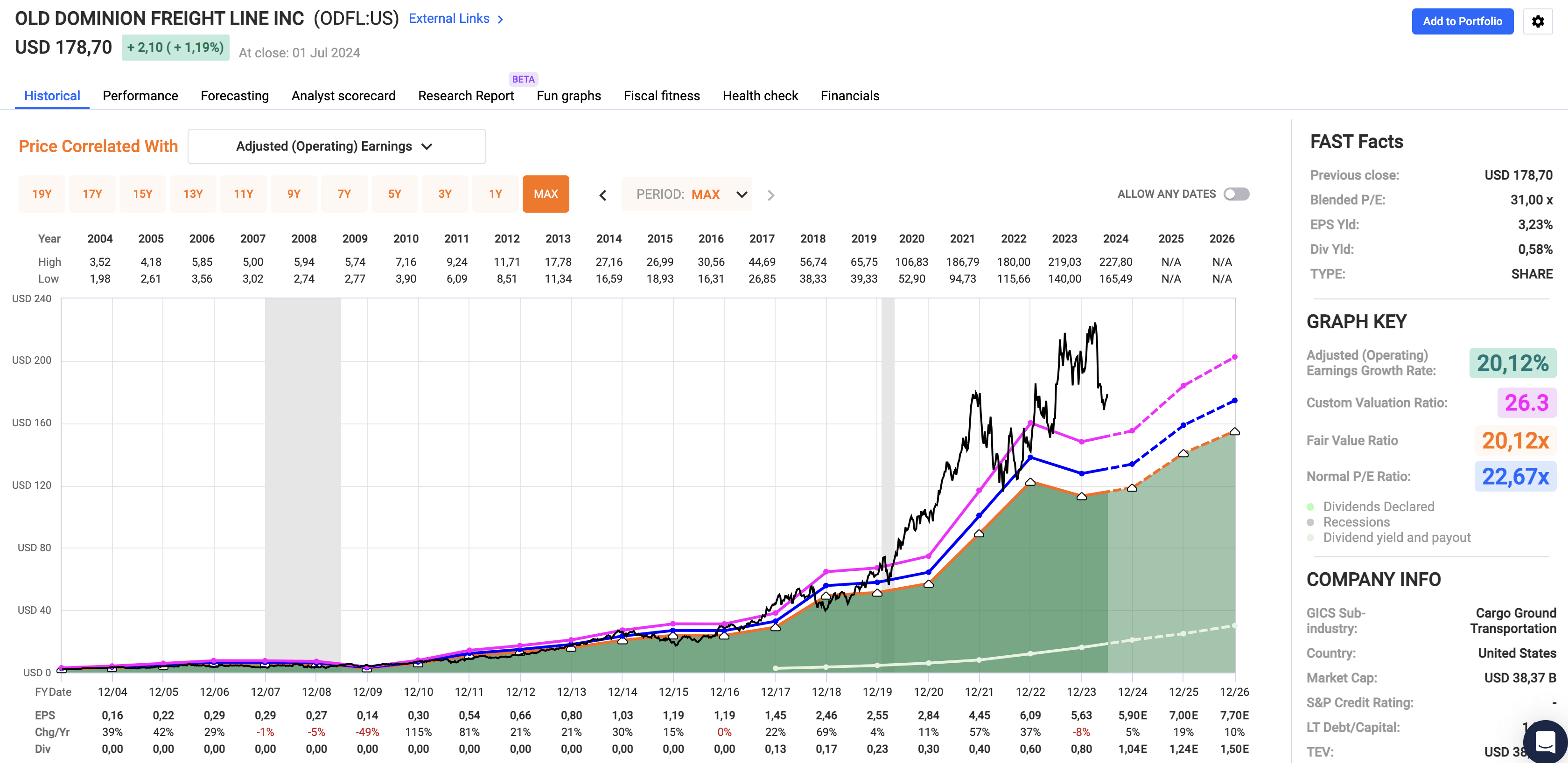

However, I still decided to buy it, as the company's ability to grow is impressive. Even in the current environment, FactSet numbers in the chart below show an expected EPS path to $7.70 by 2026. This implies a $202 stock price using its 10-year average P/E ratio (13% above the current price).

FAST Graphs

If we get an upswing in demand, I have little doubt this stock can continue to return 10-15% per year and grow its dividend at an even higher rate due to its current 36% payout ratio.

While ODFL is likely the wrong stock for income-focused investors, I believe it's a very promising company with a very bright future ahead.

Now, all eyes are on the potential recovery in freight demand, which could come with a wave of analyst EPS upgrades if it comes to fruition.

Takeaway

After closely following Old Dominion Freight Line for years, I've now joined its shareholders, taking advantage of the recent dip in its stock price.

Despite a slight downturn, ODFL's unique strengths in the less-than-truckload segment make it a standout in the trucking industry.

Its impressive network, efficient operations, and strong financials have driven significant growth, even in challenging conditions.

While the stock's current valuation is far from "deep value," the company's attractive growth prospects and strategic investments position it for continued success.

With potential demand recovery on the horizon, I'm very confident in its ability to deliver strong returns and dividend growth over the long haul.

Pros & Cons

Pros:

- Strong Growth: ODFL has delivered impressive revenue growth of 11.8% annually since 2002, growing its market share from 3% to 12%.

- Efficient Operations: Its low 70%-range operating ratio and ability to leverage pricing power set it apart in the competitive LTL industry.

- Financial Health: With a pristine balance sheet and net cash position, ODFL is well-positioned for future growth.

- Dividend Potential: Despite a modest yield, the 36% five-year CAGR and a low payout ratio promise significant dividend growth.

Cons:

- High Valuation: ODFL's current P/E ratio of 31.0x is above its long-term average, suggesting a less favorable valuation. However, in light of growth potential, I think it's a "good deal."

- Economic Sensitivity: Depending on industrial output, any prolonged manufacturing slowdown could negatively impact demand.

- Competitive Industry: Despite its strengths, ODFL operates in a highly competitive industry (yet less competitive than truckload transportation).

Comments