Summary

- Happy 4th of July to all of you.

- I'm celebrating in Sarasota, Florida with relaxation, friends, and some reading.

- I'd also like to highlight top REIT picks including Rexford Industrial Realty, Agree Realty, VICI Properties, and Federal Realty.

tampatra

Happy 4th of July to all of you!

Here’s wishing liberty, justice, and a profitable portfolio to all my readers, no matter where you are.

Where I am, exactly, is Sarasota, Fla. Now that my kids are either fully grown and out of state or almost grown and far too cool to hang out with their dad, I decided to hit the beach on my own.

I do have some friends down here I’m catching up with. And, as usual, I’m mixing some business with pleasure, having scheduled a high-profile meeting or two before I head back home.

But again, today is for relaxing. That and catching up on my reading list.

There’s a stack I still need to get to.

Maybe you’re better than me in this regard. Perhaps you’re a page-turning machine, always on the look for the next great book you can get your hands on. Or maybe you’re just ready for a new read.

One way or the other, I’ll throw out a suggestion: Greatness Is a Choice by Ethan Penner.

Oftentimes, I know, if I’m not talking about my own books, I’m quoting ones that were written decades and decades ago, such as:

- The Intelligent Investor by Benjamin Graham

- The Millionaire Next Door by Thomas Stanley

- Investing in REITs by Ralph Block.

But this is a beach vacation, and that calls for something new. Something, perhaps, written just last year, like Greatness Is a Choice.

The foreword is written by Julius Irving. For those of you who aren’t basketball fans, “Dr. J” won three championships, four MVP awards, and three scoring titles during his time on the courts.

So if he’s recommending it, I clearly need to read it.

As for the actual author, Penner has decades’ experience in real estate debt. He was one of the creative minds behind the commercial mortgage-backed securities ('CMBS') market and was voted one of the U.S. real estate industry’s 100 icons of the 20th Century.

Here’s how Greatness Is a Choice is described on Amazon:

“… Wall Street legend Ethan Penner presents a jewel box filled with thoughts and ideas that challenge readers by stimulating a higher level of awareness and critical thinking… Each chapter is a guidepost for today’s challenging societal issues, but the words are also rooted in timeless thinking culled from Penner’s considerable personal and professional experiences. Greatness Is a Choice asks readers to consider new ideas and strategies as critical tools in the pursuit of a better life for themselves and their families.”

That’s my kind of read, and one I highly recommend so far.

Of course, it's more than 200 pages long, and I understand if you just don’t have that kind of time this 4th of July. Perhaps you have a family barbecue to attend, or the friends you’re hanging out with are super chatty and you won’t have more than five minutes to spare.

In which case, I do have a much quicker read to suggest. And you’re already partway through…

Rexford Industrial Realty (REXR) – Top-Tier SoCal Real Estate

Rexford Industrial Realty is one of our favorite REITs – across all REIT sectors.

While we acknowledge that California comes with political risks, Rexford has built an impressive business with advantages that others can only dream of.

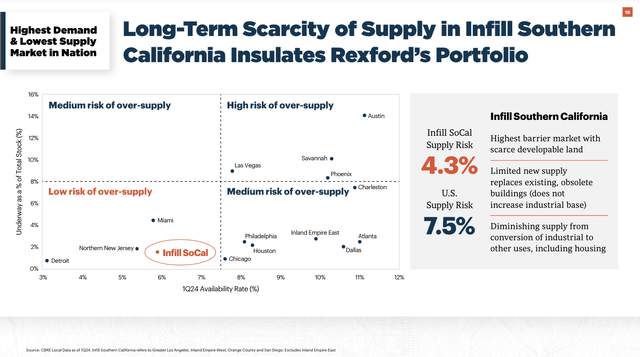

See, one of the biggest risks in the real estate sector is supply growth. Because real estate is a sector with low entry barriers, it often does not take long for new buildings to pop up when demand in certain areas is strong.

A great example of this is residential real estate in the Sunbelt, which saw exploding supply growth after the start of the mass-migration trend from “blue” to “red” states.

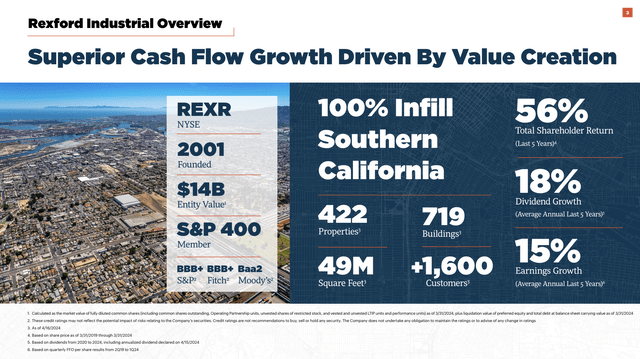

That’s where Rexford comes in, which owns industrial real estate in Southern California’s (“SoCal”) infill markets. In fact, all of its 422 properties are located in SoCal, where it serves more than 1,600 customers.

Rexford Industrial Realty

SoCal is home to two of the biggest ports in the world - Los Angeles and Long Beach, and is also one of the most attractive markets due to subdued supply growth.

Using the data below, we see SoCal has subdued supply growth and low availability rates. This provides a company like REXR with tremendous pricing power.

Rexford Industrial Realty

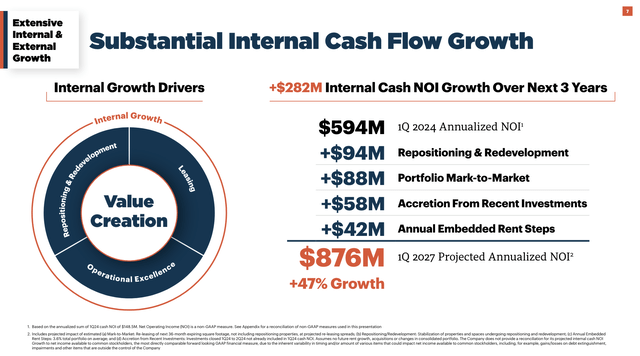

On top of protection against new entrants, this comes with internal growth opportunities.

Over the next three years, the company expects to increase its cash net operating income (“NOI”) by more than $280 million, which implies a 47% growth rate to $876 million.

This includes $88 million of incremental NOI from converting below-market leases to market rents over the next three years.

Moreover, the 3.6% embedded annual rent increases in the company’s current portfolio can add another $42 million over three years.

Rexford Industrial Realty

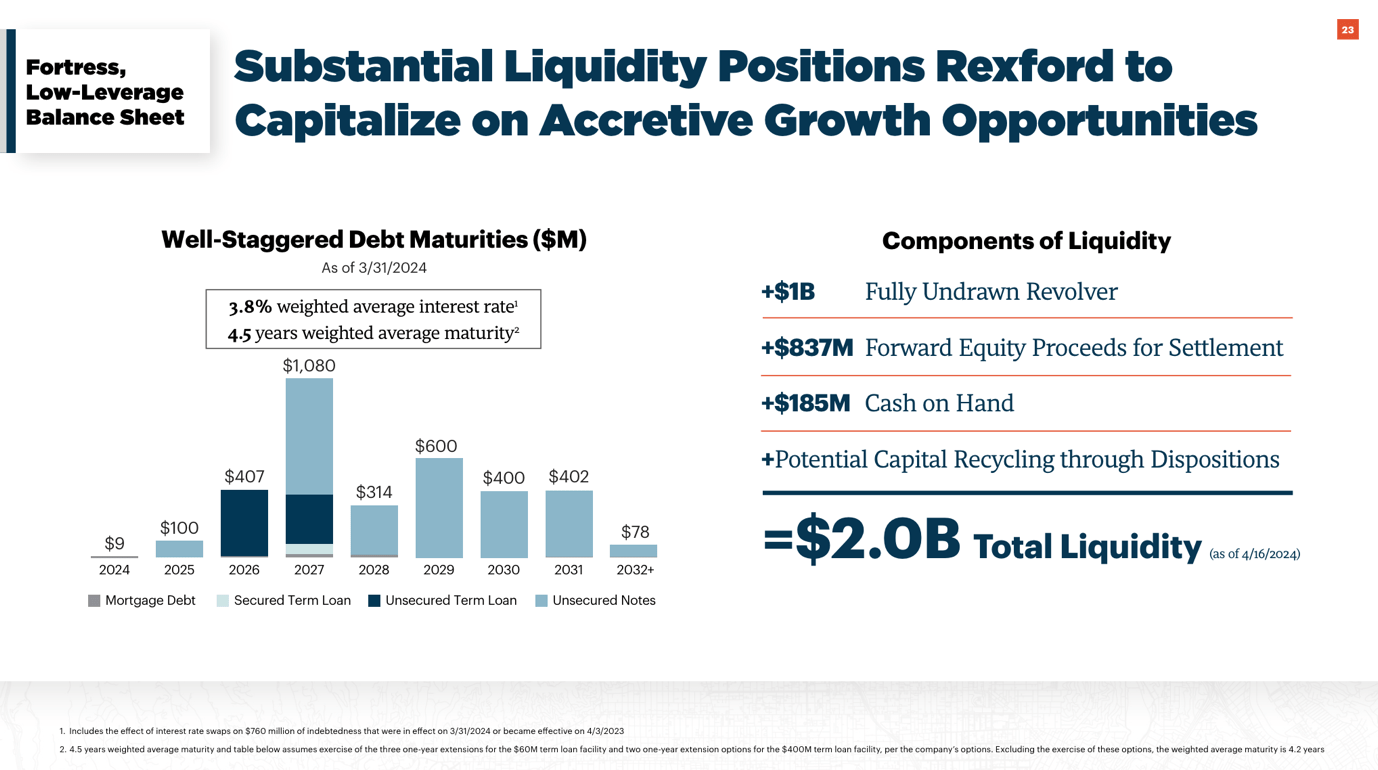

It also has a healthy balance sheet with a BBB+ credit rating, just one step below the A range. This balance sheet has a subdued net leverage ratio of 4.6x EBITDA and a weighted average interest rate of just 3.8%.

It also has $2 billion in liquidity and a weighted average debt maturity of 4.5 years, which buys a lot of time in this unfavorable environment.

Rexford Industrial Realty

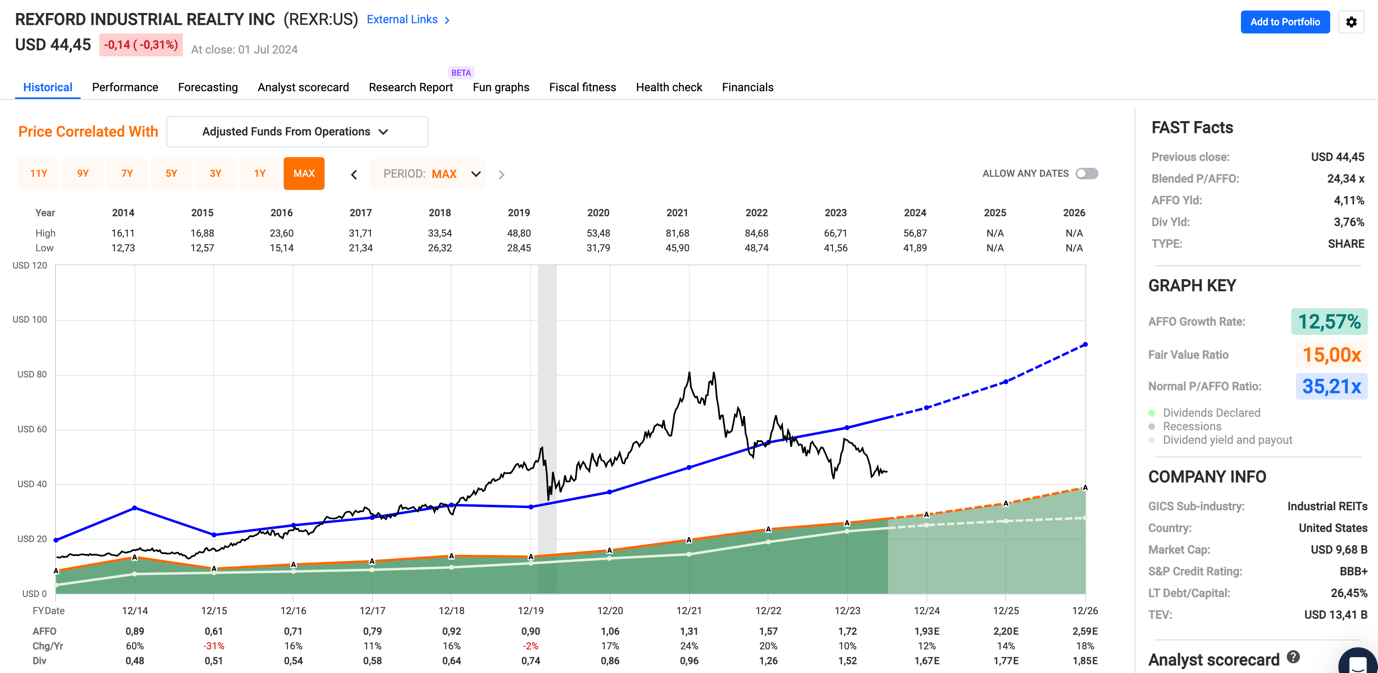

Moreover, analysts are upbeat about the company’s future.

Using the FactSet data in the chart below, the company is expected to grow per-share AFFO (adjusted funds from operations) by 12% this year, potentially followed by 14% and 18% growth in 2025 and 2026, respectively.

This makes it one of the fastest-growing REITs on our radar, which comes with a 3.8% dividend yield and a five-year CAGR of 18.2%.

FAST Graphs

Currently trading at a 24.3x AFFO multiple, the REIT trades a mile below its 35.2x normalized P/AFFO ratio.

While it will take a lot to justify a multiple that high, we expect REXR to return 15%-20% annually the moment the market sees a realistic path to lower rates.

Agree Realty (ADC) – Did Someone Say Net Lease?

Although Agree Realty has been a public company since the early 1990s, it has become a very popular REIT since the Great Financial Crisis.

Like its big brother Realty Income (O), Agree Realty is a triple net lease, meaning its tenants take care of insurance, maintenance, and taxes – on top of regular rent and utilities.

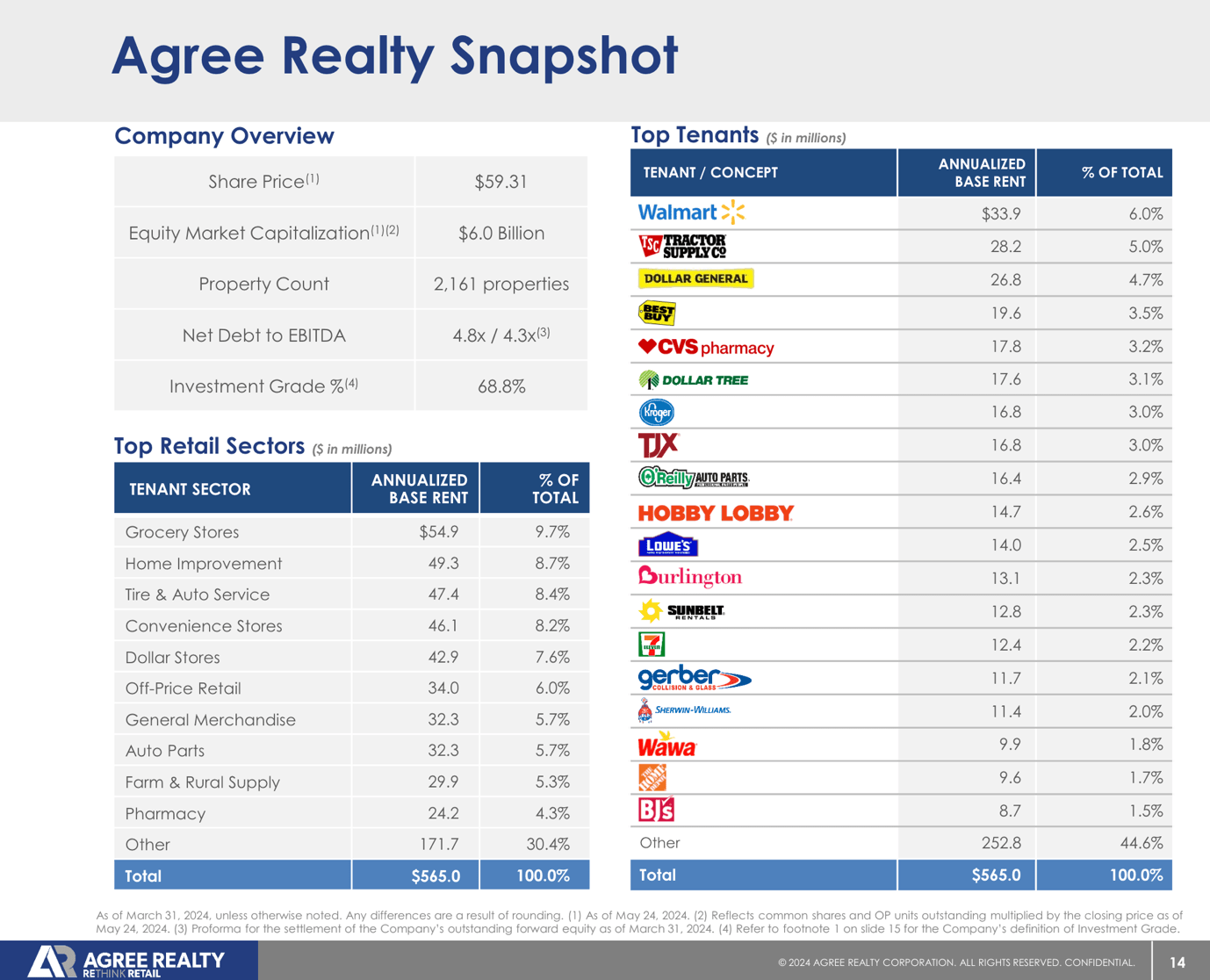

What sets Agree Realty apart in its industry is its fantastic portfolio that caters to some of the most sought-after tenants, including Walmart, Tractor Supply Company, Dollar General, Best Buy, CVS, and Home Depot.

Roughly 69% of its tenants have an investment-grade credit rating, which is unmatched by any of its peers. The company itself also has an investment-grade balance sheet with a sub-5x net leverage ratio.

Agree Realty

During the first quarter, the company invested $140 million in 50 high-quality retail net lease properties, achieving a weighted average cap rate of 7.7%.

Moreover, investment-grade retailers accounted for 64% of the annualized base rents that were acquired, further supporting a healthy tenant base.

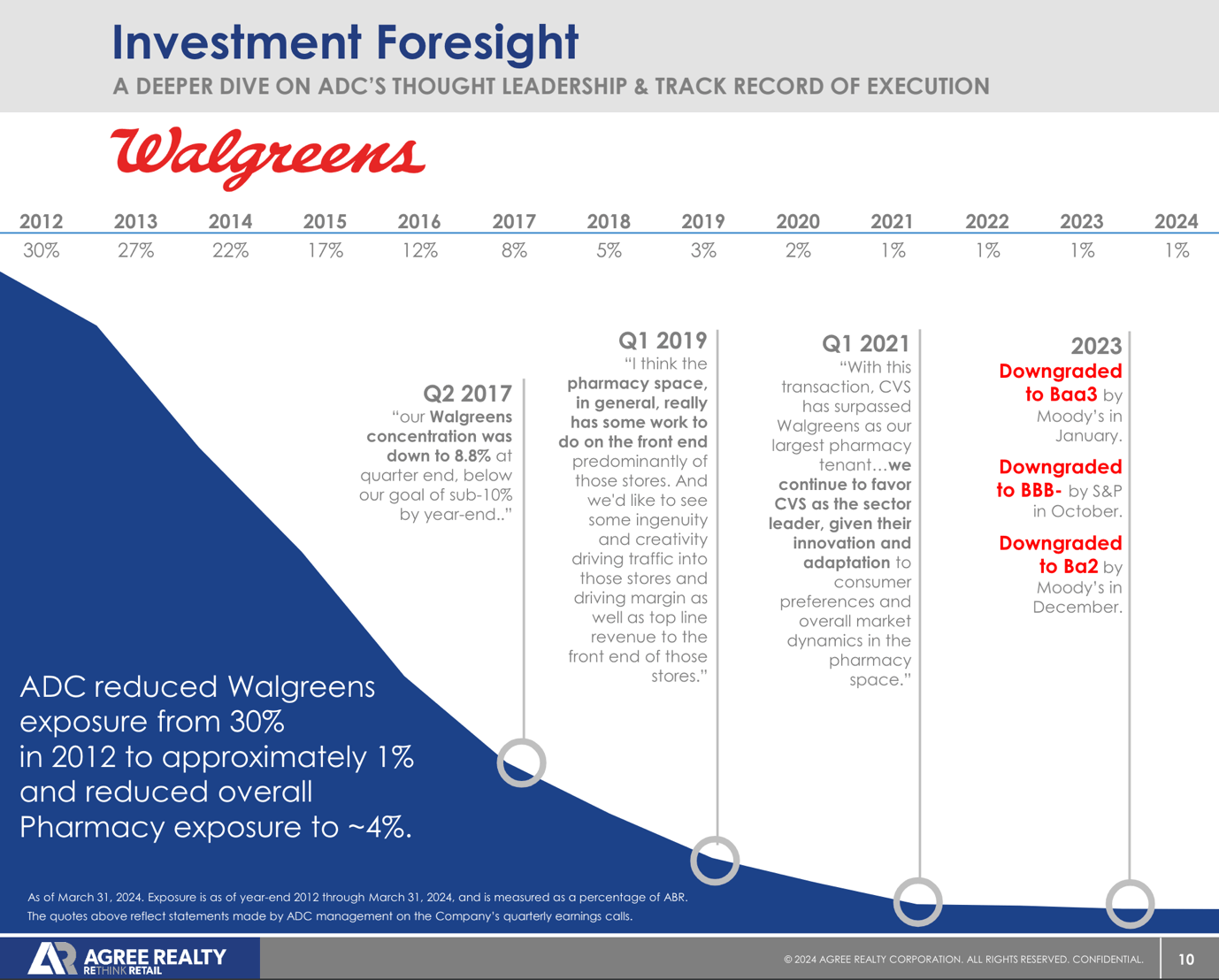

In general, the company’s proactive management is working out well as it reduced its exposure to struggling pharmacy giant Walgreens way ahead of the company’s financial downgrades and mass-closing announcements.

Agree Realty

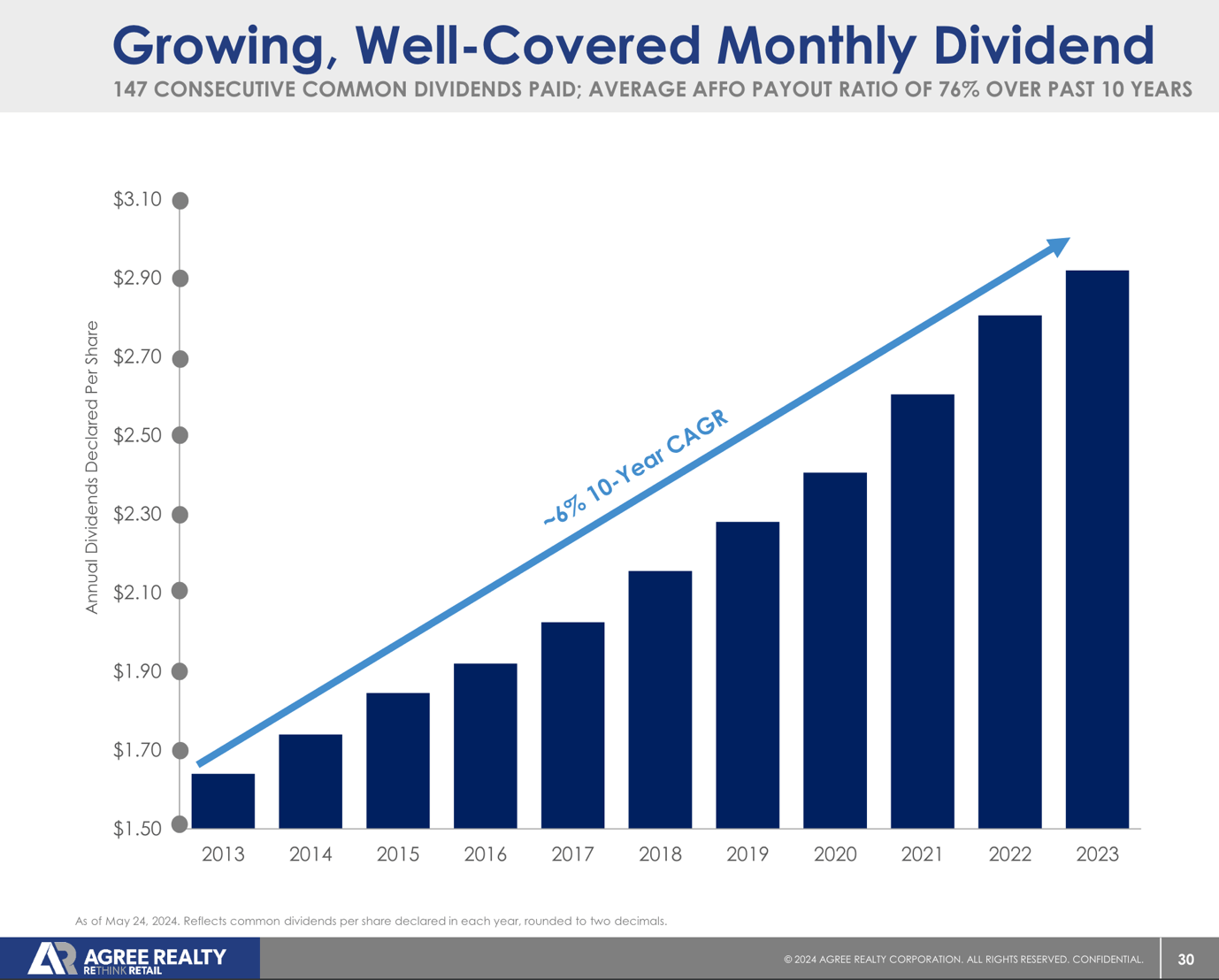

Moreover, with a growing (five-year CAGR of 6.2%) dividend that yields 4.9% and a well-covered 72% AFFO payout ratio for the first quarter, investors can expect a stable and growing income stream.

Agree Realty

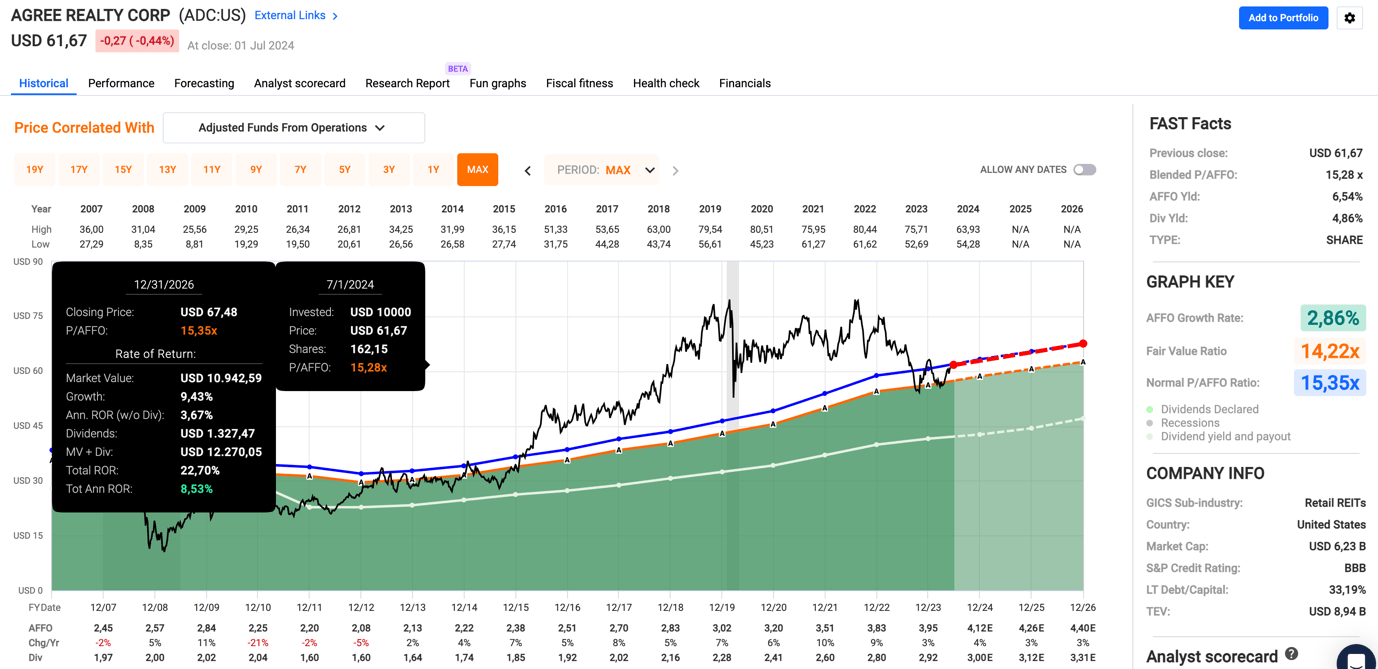

With regard to its valuation, ADC trades at a 15.3x AFFO multiple, in line with its long-term average.

As analysts expect 3%-4% annual per-share AFFO growth through at least 2026, we get an annual return outlook of 8%-9%, which could be substantially higher if the market prices in a lower-rate environment.

FAST Graphs

With that said, there’s another net lease REIT on our radar we have grown quite fond of.

VICI Properties (VICI) – Owning The Strip Comes With Benefits

Managed by Ed Pitoniak, who we have interviewed a few times in the past, VICI has become the largest gaming REIT in the United States.

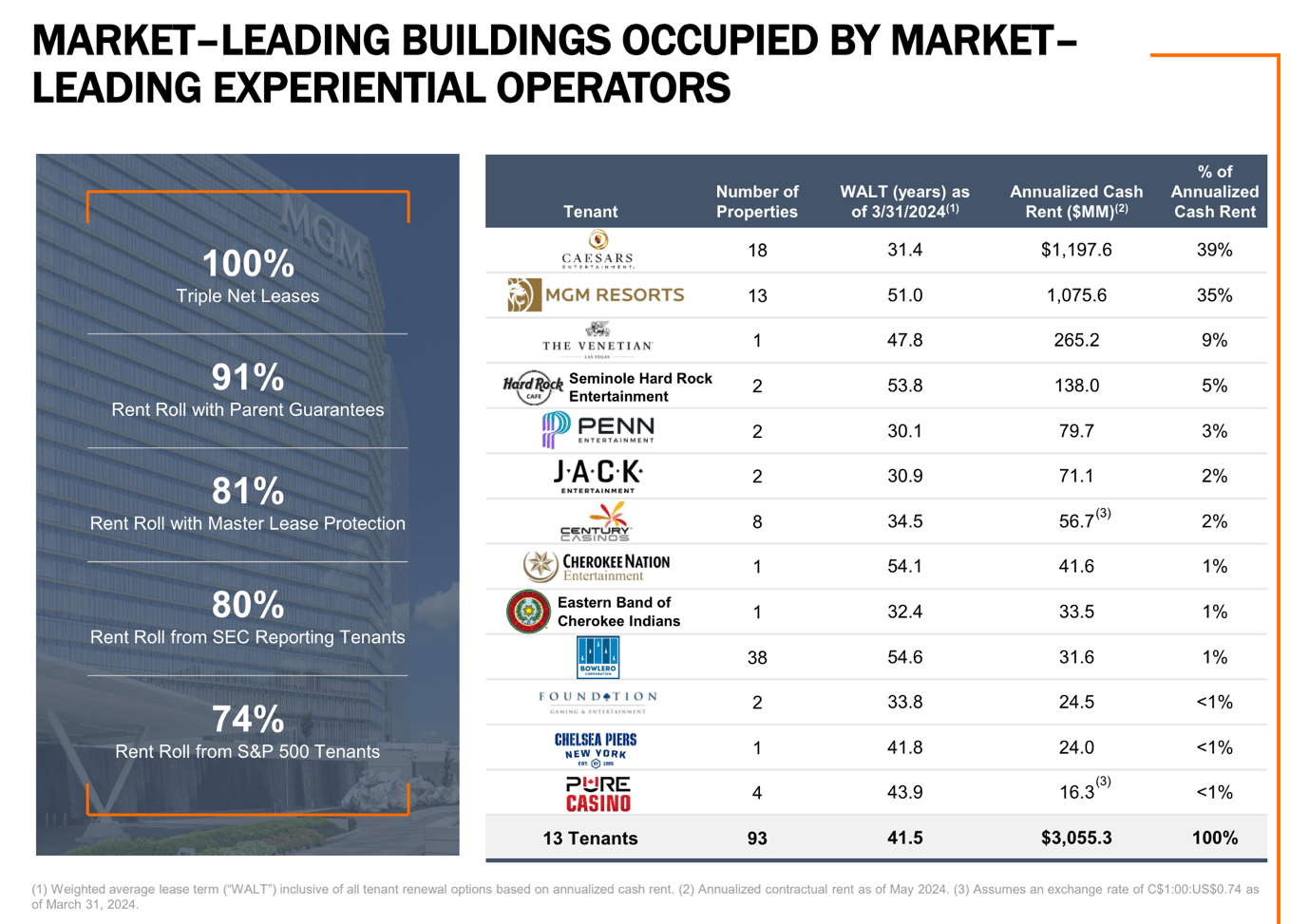

The company, which has its roots in the 2017 bankruptcy of Caesars Entertainment, acquired MGM Growth Properties in 2021 to create a giant that owns more than 90 properties and generates roughly $2.5 billion in annual rent from its biggest three tenants: Caesars, MGM Resorts, and The Venetian.

VICI Properties

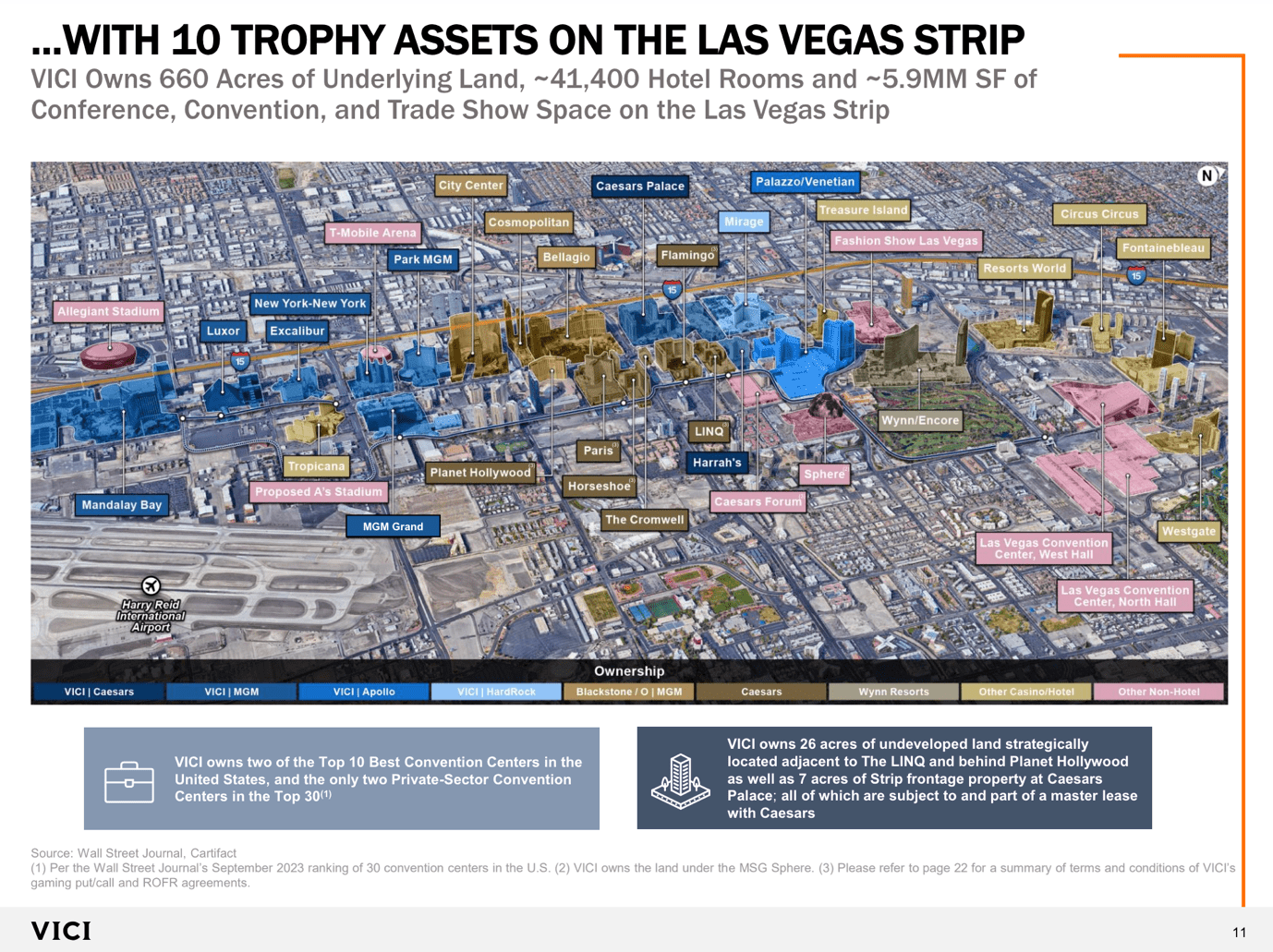

As we can see below, these assets cover a big part of the Strip, where the company generates roughly half of its annual base rent. This includes Mandalay Bay, Luxor, New York-New York, the MGM Grand, Park MGM, and Caesars Palace.

VICI Properties

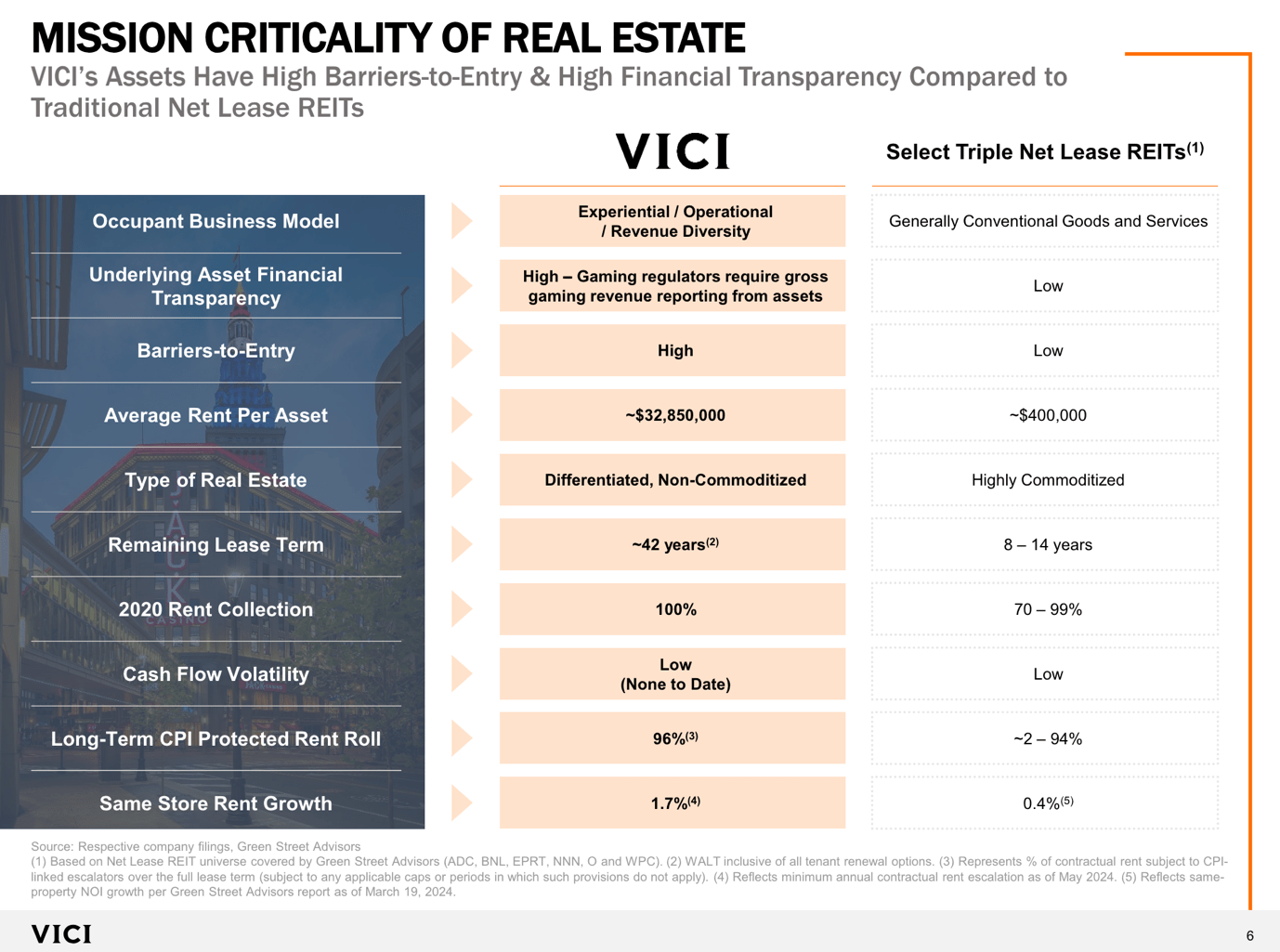

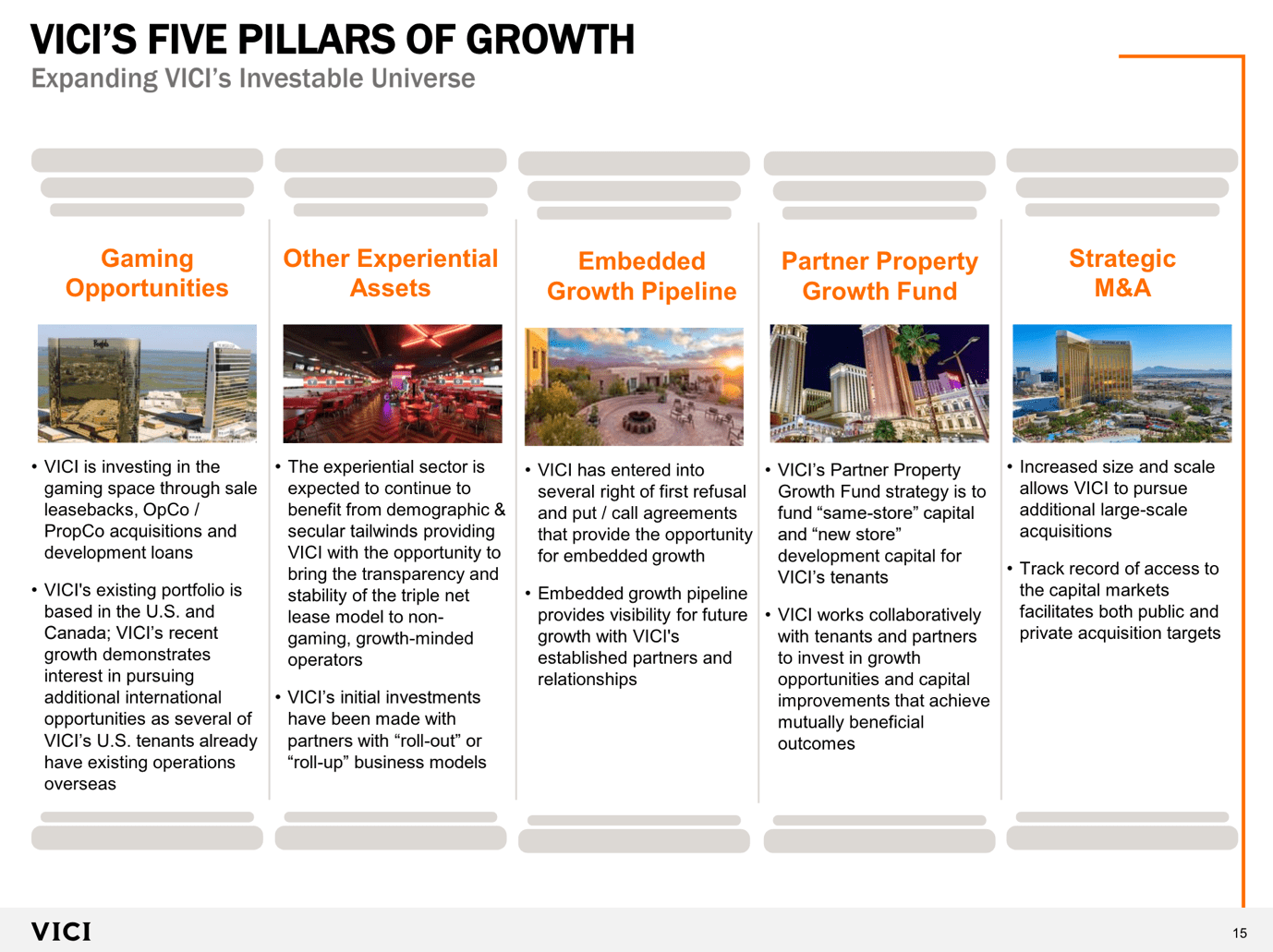

Although it will be hard for the company to grow by adding Vegas-like properties, it has built a portfolio of non-commoditized net lease assets, which sets it apart in the no-moat net lease industry.

It also has an average remaining lease term of more than 40 years, close to 100% CPI-protected rents, and tenants who absolutely depend on the “uniqueness” of their buildings to stand out.

VICI Properties

In order to grow, the company is adding desired entertainment/leisure assets, including its investment in Homefield Kansas City, which is a leading sports training complex that will soon feature a Margaritaville resort.

According to the company, this investment aligns with its initial move into the sports and recreation sector with the 2023 acquisition of Chelsea Piers.

Additionally, VICI’s opportunity to invest up to $700 million in The Venetian in Las Vegas through the Partner Property Growth Fund is a great way to enhance the customer experience and keep these assets highly desired objects for customers and tenants.

VICI Properties

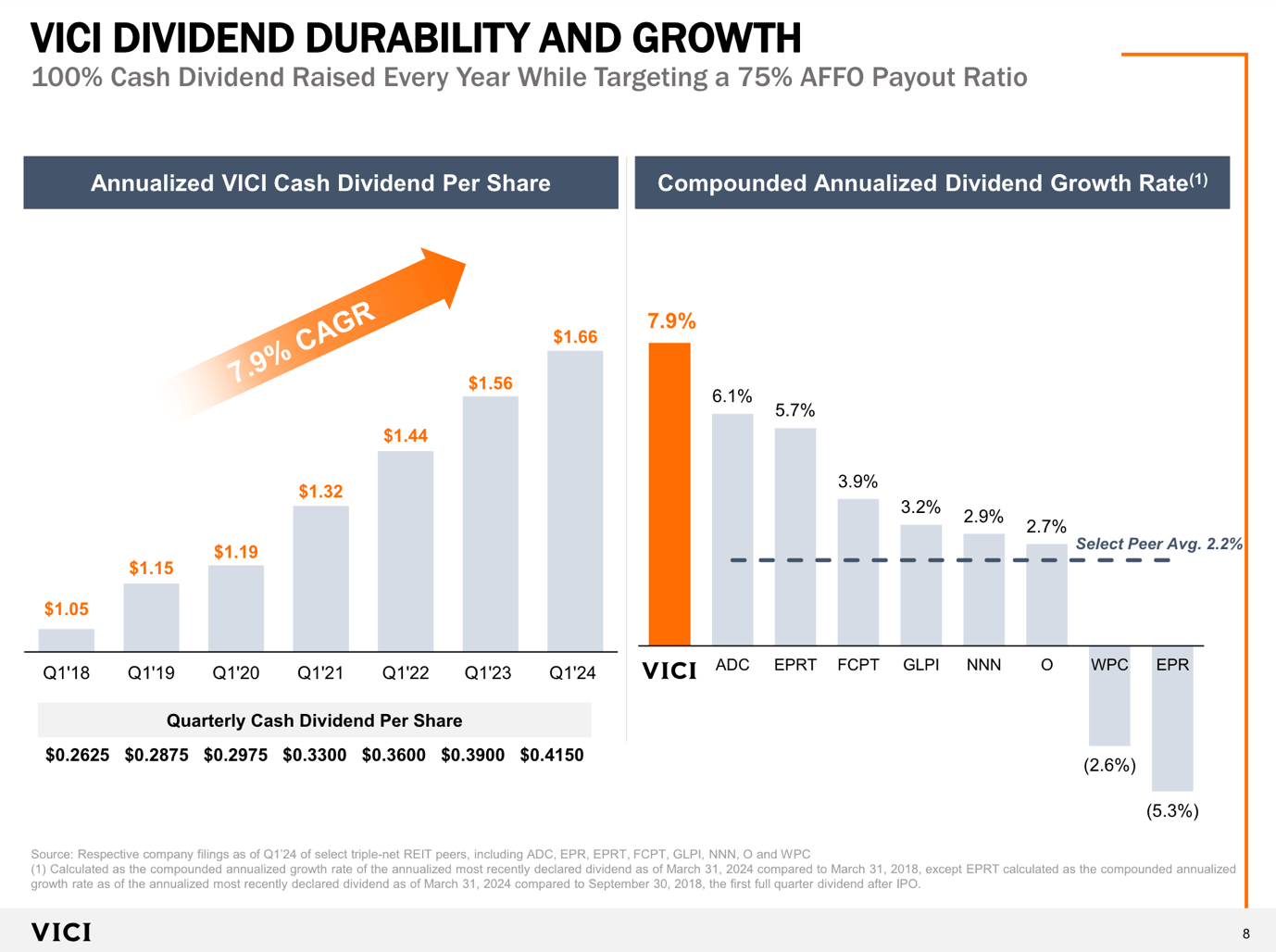

It also comes with a fantastic dividend, which has a CAGR of 7.9% since its IPO in 2018.

On top of that, VICI currently yields 6%, which is one of the most attractive yields in the REIT space – especially because it’s backed by an investment-grade balance sheet and a 76% AFFO payout ratio.

VICI Properties

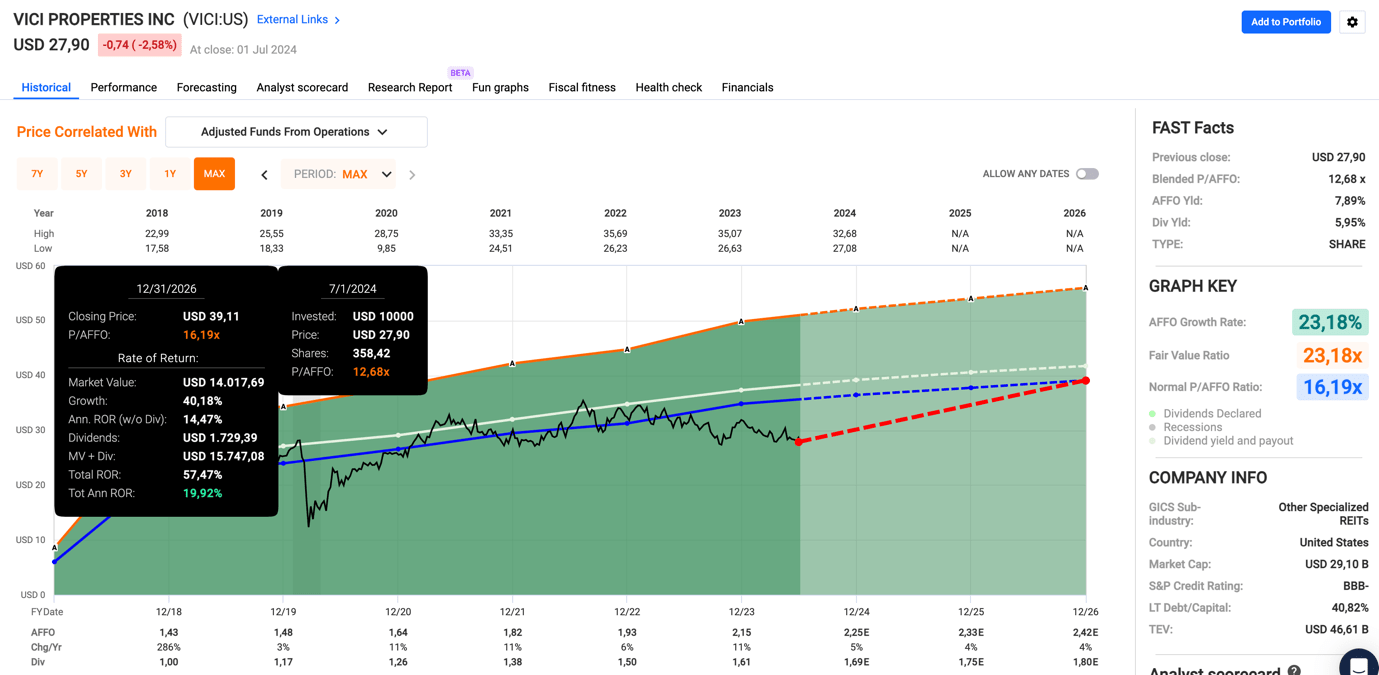

VICI is also one of the most attractively valued REITs on our radar, trading at a blended P/AFFO ratio of just 12.7x. This is a mile below its normalized P/AFFO ratio of 16.2x and further supported by 4%-5% annual per-share AFFO growth through at least 2026.

FAST Graphs

While it will likely require lower rates to unlock a higher multiple, we do not believe VICI should be trading below $40 on a longer-term basis, which is more than 40% above the current price.

The next pick is even cheaper – relatively speaking.

Federal Realty (FRT) – A Dividend King With A Great Price Tag

- The 1973 oil embargo.

- 1980s inflation.

- Emerging market financial crisis.

- Great Financial Crisis.

- The pandemic.

What do these things have in common?

None of them prevented Federal Realty from hiking its dividend.

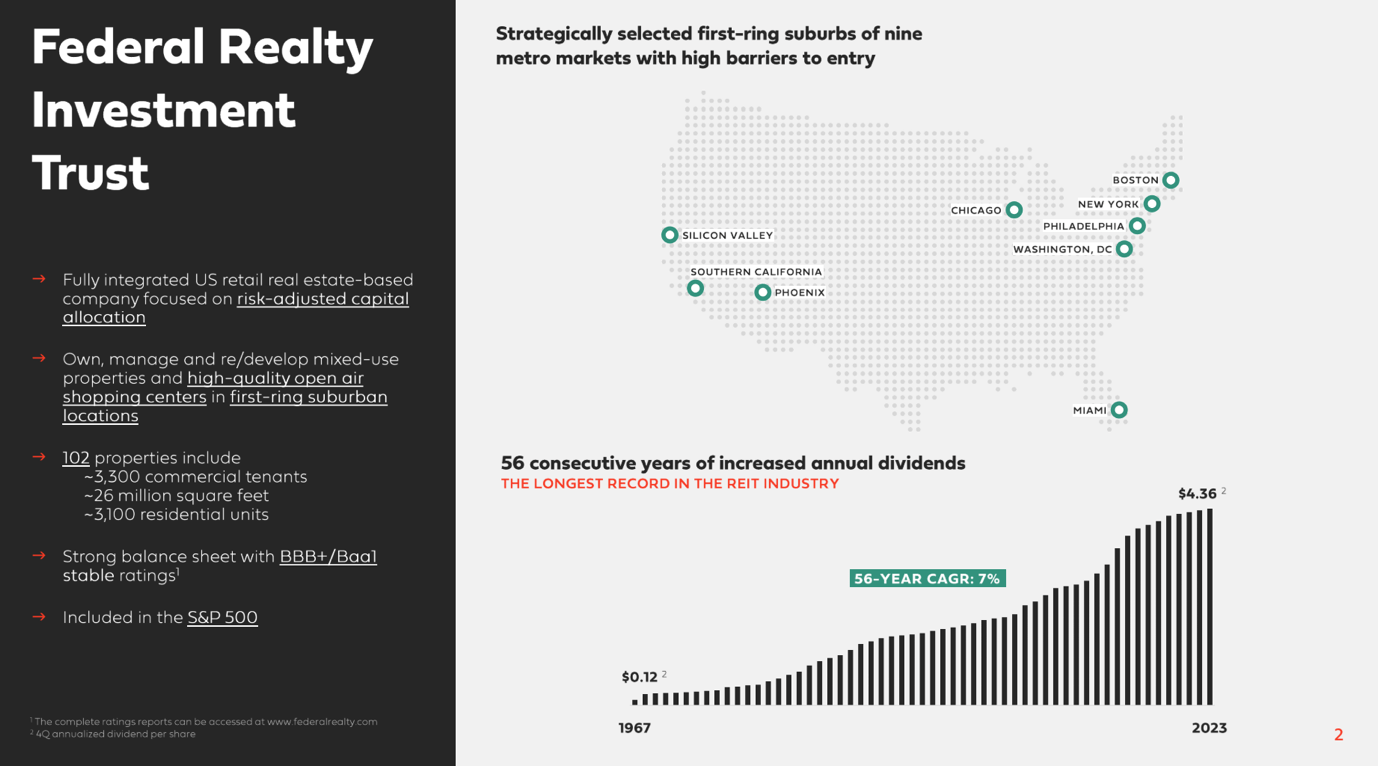

Since 1967, the company has hiked its dividend every single year, making it one of the few Dividend Kings in the REIT space.

Currently yielding 4.3%, the dividend has a 64% payout ratio and a five-year CAGR of 1.3%.

Federal Realty

This S&P 500 member is a fully integrated U.S. retail real estate entity focused on high-quality open-air shopping centers in first-ring suburban locations.

Its 102 properties include roughly 3,300 commercial tenants on 26 million square feet and roughly 3,100 residential units, which is a part of the company’s diversification.

Unlike other strip malls, the company stands out for two reasons:

- It enjoys extreme population density when it comes to its assets.

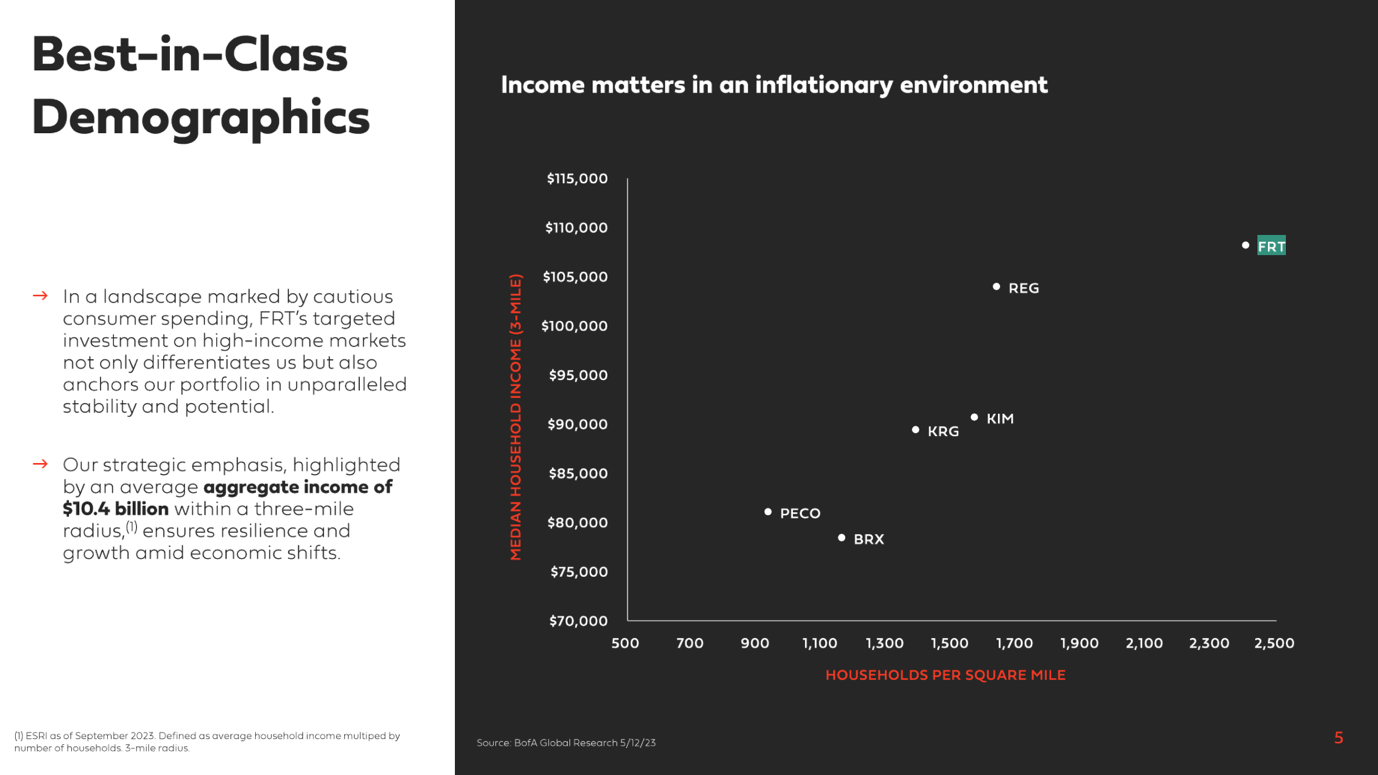

- The median household income in its operating areas is much higher compared to its peers. This adds some resilience.

Federal Realty

The average household income of its markets is $152,000 with relatively high barriers to entry. This includes markets like New York, Southern California, the San Francisco Bay Area, Boston, Philadelphia, and others.

In these markets, it's landlord to highly-desired tenants, with mostly investment-grade balance sheets. Even better, none of them account for more than 2.7% of annual base rent.

Federal Realty

Right now, these markets come with strong demand, as the company signed 117 commercial leases in the first quarter, totaling more than 775,000 square feet.

This included record retail leasing and significant office space leases, such as the 141,000-square-foot lease to PwC at One Santana West.

The leasing success is further supported by the increase in small shop lease percentage to 91.4% and anchored lease percentage to 95.8%, indicating a healthy occupancy rate and room for further growth.

Federal Realty

As part of its growth strategy, the company is focusing on acquiring larger shopping centers with potential for redevelopment and higher rents, mainly in markets that have shown significant post-pandemic strength. This includes Phoenix, Central and South Florida, and Northern Virginia.

It also has a healthy balance sheet with no debt maturities until 2026, a BBB+ credit rating, 86% fixed-rate debt, and $1.3 billion in liquidity.

Federal Realty

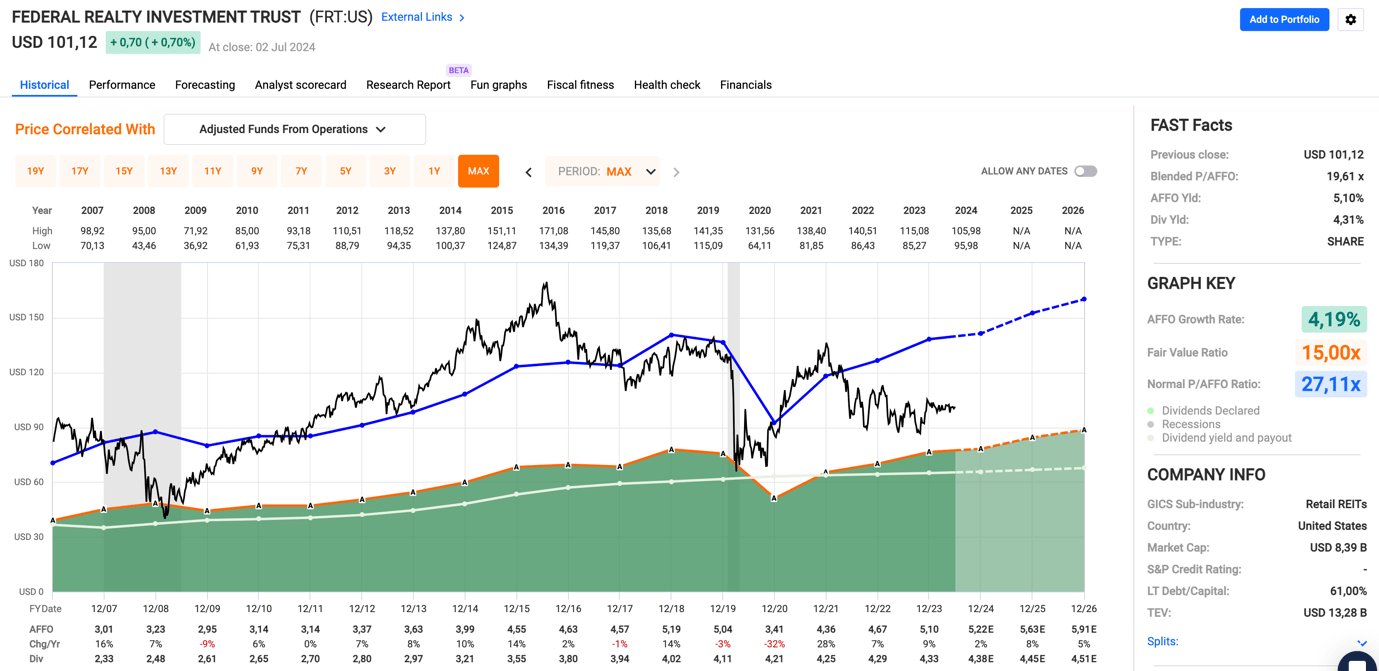

Valuation wise, FRT trades at a blended P/AFFO ratio of 19.6x, which is below its normalized 27.1x multiple.

This year, analysts expect 2% per-share AFFO growth, potentially followed by 8% and 5% growth in 2025 and 2026, respectively.

FAST Graphs

Although it will likely require lower rates to achieve a higher multiple, we believe this stock has room to rise at least 30% in the years ahead, without including its dividend.

In Closing

I'm looking forward to the weekend, and these four picks will allow me to enjoy my time off without worrying about my portfolio.

Rexford Industrial Realty, Agree Realty, VICI Properties and Federal Realty Trust all have strong portfolios and robust balance sheets, and we expect to see significant capital appreciation in the future as market conditions become more favorable for REITs.

As always, thank you for reading and commenting. Have a great 4th of July!

PS: Special thanks to Leo Nelissen who helped me coproduce this article.

Author's note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.

Comments