Summary

- Interest rates drive around 40% of Robinhood's net revenues, and a large recessionary rate cut would likely erase most of that revenue segment.

- Robinhood attracts speculative retail accounts, which see activity and flows ebb and flow more dramatically than peers with the overall stock market trend.

- Since individual investors lack prominent uninvested cash positions and recession odds are high, Robinhood's net revenues may also decline due to lower transaction-based sales.

- Assuming Robinhood's sales and income remain steady, the stock appears significantly overvalued, trading at a roughly 150% premium to IBKR.

- HOOD's bullish momentum is strong enough that it may not be a good short opportunity, but it may be a decent pair trade against its much more reasonably valued competitor, IBKR.

RichHobson

The popular retail brokerage Robinhood (NASDAQ:HOOD) has had tremendous performance over the past year, rising by around 90%. The past year has seen its greatest rebound since the end of its 2021 crash, though it remains around 35% below its IPO price and less than half of its post-IPO price.

Shortly after it went public, I was very bearish on HOOD due to its extremely high valuation and seemingly unstable business model. The stock crashed in value and remains 44% below its price then (September 2021). I updated my outlook to neutral in 2022. Though I remained neutral by 2023, I explained my positive outlook on its fundamentals in "Robinhood: Higher Revenue Expected Due To Federal Reserve Rate Hikes."

Since then, it has risen by 141%, warranting an updated analysis. My previous view was that the company's sales would increase markedly due primarily to higher interest rates, as the company generates a great deal of income from cash positions. Further, I thought improved customer quality with larger accounts would lead to more significant operating margins. Lastly, I was curious about the profitability of its credit card business, which has had a lackluster performance.

Speculative Market Momentum Slowing

I believe its Q2 earnings report, expected early next month, may be among its most important. The past year has seen a significant rebound in speculative market momentum, driven by the solid performance of many large technology companies like Nvidia (NVDA). Robinhood's core customer base is typically newer market participants, often younger and with smaller accounts. Thus, it tends to have very high exposure to changes in speculative momentum from that cohort, compared to Interactive Brokers (IBKR), which has a more stable customer base with larger accounts.

To me, the most significant issue with Robinhood is that investors value it without due regard for the cyclical nature of speculative market momentum. Imagine one group of stock market participants who are more long-term focused, either retirement investors or institutions. That group is stable, giving companies that cater to them, like IBKR, a slow-growing but strong-handed asset and customer base. The other segment of market participants usually looks more for short-term gains by trading market momentum. I believe Robinhood attracts that group more, giving it higher potential profits from trading volume and additional products (Robinhood gold, etc), but with less stability.

So, when we value Robinhood, I believe it is crucial to assume that its Assets Under Custody are more likely to decline during bearish or stagnant markets. Robinhood's exposure to that issue surfaced in 2021 as speculative momentum faded following the boom in "stimulus trading." We've seen a strong rebound in speculative trading over the past year, led by the most extensive stocks in the Nasdaq 100, but that, too, seems to be fading.

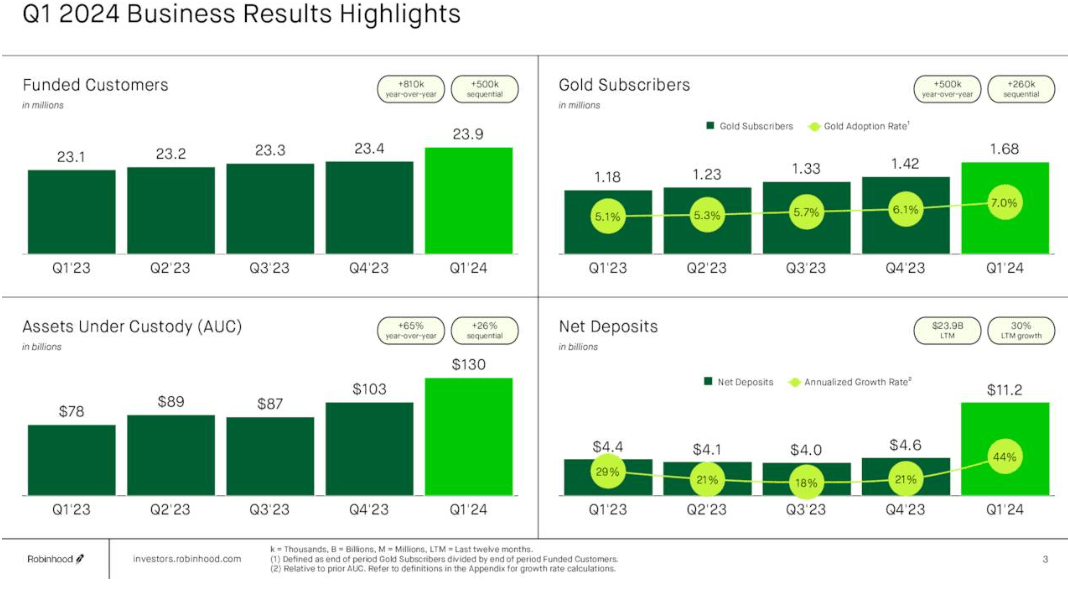

Still, looking backward, we can see Robinhood's significant improvements to its AUC, funded customer base, Gold Subscribers, and deposit base. See below:

Robinhood Business Highlights (Q1 Investor Presentation)

The increase in net deposits is likely due to higher interest rates. Further, the company has seen a rise in both the number and size of its accounts, partly driven by an increase in retirement accounts. At the end of Q1, it had $4.2B in its retirement account AUC, just 3.2% of its overall AUC, but this is still a positive trend as these accounts are typically larger and more stable.

The company also noted that its existing accounts are growing from deposits and that it's seeing far more accounts over $5K in size. Still, IBKR and Schwab (SCHW) have average account sizes of around $250K, meaning it's a long way before reaching that level. The fact is that younger generations are more often behind in saving for retirement today and are far less likely to own a home, giving them a low capacity for higher liquid net worths that drive brokerage account sizes.

HOOD has smaller accounts that likely have more "high beta" equity assets, based on the historical pattern of the top 100 stocks owned by HOOD accounts. Thus, the company is exposed to greater general market risks, as a stock market decline would lower its AUC and likely reduce inflows and account volumes. As detailed in many recent articles, I believe the US is headed into a standard recession based on consumer and employment trends. However, whether or not that results in a significant market decline remains unclear. Still, based on interest rate modeling, the odds of a recession are very high today. More importantly, individual investor cash allocations are meager, indicating low "sideline cash" that can be invested into equities. See below:

Data by YCharts

Data by YCharts

Often, but not always, stock market crashes occur when individual investors have smaller cash allocations. Stocks are fueled by liquidity, so stocks are less likely to rise if there is not enough cash to be invested. In 2022, investors turned cautious, and cash levels rose, hampering Robinhood's fundamentals. Since 2023, most of that cash has been redeployed back into stocks, significantly improving its fundamentals. Looking forward, it seems likely that low cash levels will hamper the stock market's performance and limit Robinhood's account fundamentals.

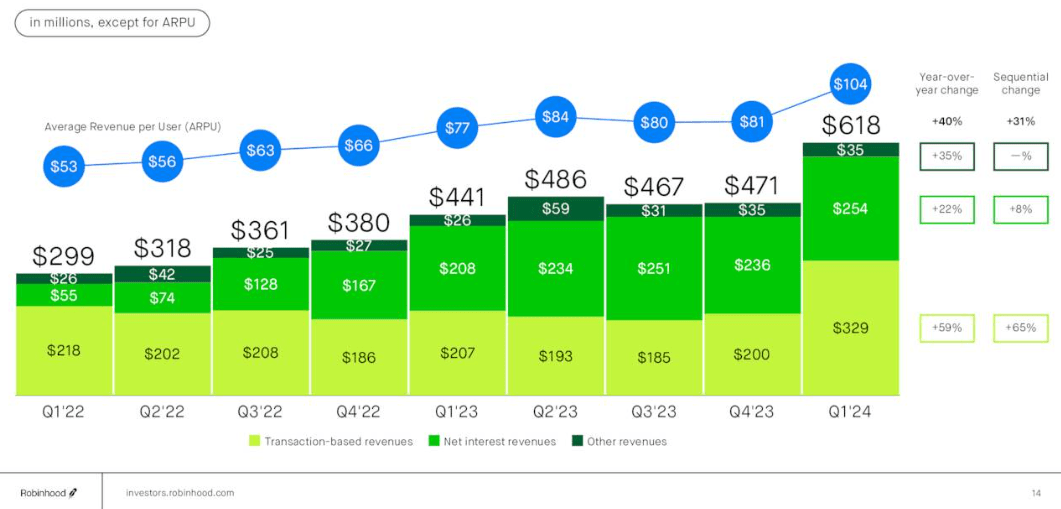

Transaction revenues shot up to $329M last quarter from ~$200M in previous quarters. A market correction could temporarily result in higher transaction revenues, but I expect a return below $200M over the coming year. A crash that pushes stocks below 2022–2023 minimums may cause transaction revenues to fall closer to $150M per quarter.

Lower Interest Rates Terrible For Robinhood

Many believe the expected interest rate cuts will benefit stocks and the economy. I disagree with that view. In past eras, high rates caused more cash savings, limiting consumption spending and investments. However, since the economy has become more import and QE-driven, interest rates have had a seemingly less direct impact on most companies. Indeed, personal savings have failed to improve despite high rates, while most large stocks have continued to rise.

Even then, Robinhood will not benefit from rate cuts because it derives a considerable portion of its sales from interest. See below:

Robinhood Segment Revenue (Q1 Investor Presentation)

Looking at the ultra-low rate era of early 2022, we can see that less than 20% of its sales were from interest. One of the main reasons my tone on Robinhood became more optimistic last year was the vast expected sales increase it would have from higher rates. Now, just over 40% of its sales are from interest. That segment is divided somewhat evenly between interest on its investments (primarily corporate cash securities), margin interest, interest on uninvested customer deposits, and, to a lesser extent, cash sweep, securities lending, and, negligibly, its credit card program.

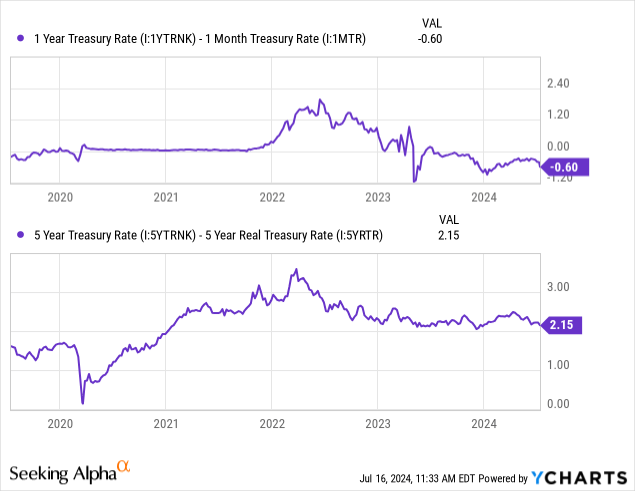

Based on the spread between the one-year Treasury rate and the 30-day rate, we can look toward a 60 bps cut over the next twelve months. That said, there's been a very sharp decline in that figure over the past week following disappointing economic data and lower inflation. The five-year inflation expectation rate is now near 2%, indicating no need for high rates based on current projections. See below:

Data by YCharts

Data by YCharts

In my view, the Treasury market is undershooting the potential impact of a recession. Historically, if the economy has a hard landing, that will quickly spur disinflation and potentially deflation. As I've detailed in many articles, I expect inflation will be high in the long run due to debt, demographic, and infrastructure issues (and potentially geopolitics). However, that sizeable temporary deflation is likely in the event of a significant rise in unemployment. I think household debt levels are too high compared to household savings, and even a small unemployment increase should cause a substantial decline in discretionary consumer spending.

While my outlook is speculative, I believe this sets the scenario for a "hard landing" followed by a temporary return to near-zero interest rates. Thus, I expect that Robinhood's sales from interest should fall back to $50M to $150M by 2025 (quarterly), with a wide range as it remains unclear if my aggressive rate-cut outlook will hold. I think a 400 to 500 bps rate cut is not off the table over the next year (potentially two), similar to the pattern seen around 2007-2009. Very few will agree with that view today. That said, even if we value Robinhood based on the more neutral projections of other analysts, it appears vastly overvalued.

Robinhood is Overvalued Without a Recession

Combining my outlook for transaction and interest revenues (keeping "other revenues" constant), I expect Robinhood's quarterly sales to be around $235M to $385M a year from now. That would push its sales back into the range seen before 2023 and potentially lower than they have been. If the US economy avoids a recession and a market slowdown with a "soft landing" and light rate cuts, its sales could remain over $500M quarterly and potentially higher if speculative trading activity remains as elevated as it has been.

Since I'm projecting a "hard landing" with lower rates, transaction volumes, and likely negative account growth, I expect a quarterly gross profit of around $175M to ~$300M by early 2025. That said, if the market has a soft landing or continues to rise, then Robinhood should see its TTM trend continue, though I find that quite unlikely based on my macroeconomic outlook.

Thus, I see a high uncertainty surrounding its sales and income, with the downside seemingly much more significant over the coming year. The company's quarterly adjusted OpEx was $398M in Q1, up from ~$360M during most of 2023. Robinhood could likely cut that figure to ~$300M, based on its lowest quarterly adjusted OpEx of $319M in Q4 2022. A prolonged recession or decline may see an even more considerable reduction in operating expenses, as much of its spending is on marketing and R&D, while only ~$100M is on G&A and operations.

Since the company's interest income is operational, its operating and net income are usually the same, aside from one-off events. Its tax rate is generally near zero due to its previous losses, though it is rising slightly. Still, given my economic and market outlook, I anticipate it will be seeing negative income of around -$125M to around $50M per quarter by 2025, or an annualized EPS of -$0.57 to $0.23.

My outlook disagrees with the analyst consensus, which predicts stagnation at its current EPS level of $0.50 per year for the coming three years (~$440M annual income). Most analysts are projecting that Robinhood will face stagnation due to lower rates, but are likely not accounting for the impact of a hard landing on transaction volumes with more rapid rate cuts. HOOD's 2026 projected EPS is also $0.50, giving it a "long-term" forward "P/E" of around 49X. To compare, IBKR's 2026 projected EPS is $7.15, giving it a "long-term" forward "P/E" of 17.3X.

I am bearish on HOOD because it appears overvalued, even based on the more positive outlooks of other analysts. My view differs because I am projecting along recessionary lines, but even if we assume stability, its price is high compared to peers.

Robinhood's superior income growth is mainly attributable to its interest income on uninvested cash, whereas Interactive Brokers and others do not typically profit from customers' uninvested cash. With Robinhood, you must pay a monthly fee to be eligible for market-level interest. So, a significant rate decline would likely hamper both its gold subscription income and interest revenues. In my opinion, Robinhood is not currently valued with the understanding that its income growth is primarily tied to the Fed funds rate.

It's core customer account growth is decent, but I still think IBKR's is better, given its larger account sizes. As a customer of numerous brokerages over the years, I feel Robinhood's platform is essentially a gamification of trading that will more often encourage serious investors to transition to platforms with more tools and fewer added costs (such as taking some interest from uninvested cash).

The Bottom Line

I see no reason why HOOD should trade at a hefty premium to IBKR when its cyclical risks are likely higher. In my view, HOOD should also trade at a similar long-term forward "P/E" to IBKR of ~17.3X, implying a 65% share price reduction to that target. HOOD would be worth ~$8.65 to have the same "P/E" valuation as IBKR. Both companies have around $4B to $5B in cash, but HOOD's is larger as a ratio of its market capitalization. HOOD's market capitalization should be slightly higher to account for this, giving me a target of $10. That is based on the net debt-to-market capitalization ratios of both firms. Though the calculation could differ depending on how we compare their balance sheets, the impact is not significant enough to justify HOOD's huge valuation premium.

That would be a far more reasonable price. That target may sound too low to many readers, but it traded at that price nine months ago. Again, that target is based on the relatively neutral outlooks of other analysts; if my view that the markets will face a "hard landing" scenario proves correct, then I expect IBKR to fall to an even lower price point.

Still, I would be cautious to bet against HOOD today, simply because it has a lot of positive momentum. Like many of the accounts in it, Robinhood tends to fall into the more speculative retail trading basket. I've learned that I do not like short-selling stocks that are trading too high above their fair value because very little stops them from rising even higher in a bubble. While I cannot justify its current price, its fundamentals today are much better than in 2021, when it traded at over $40 per share.

That said, I may bet against HOOD in a long IBKR pair trade. IBKR has also had decent momentum over the past year, rising by 47%. Although its speculative momentum is lower than HOOD's, its valuation gap is so large that I think the pair trade opportunity is decent. Interactive Brokers also has negative exposure to rate cuts, but not nearly to the degree as does Robinhood. Thus, the long IBKR short HOOD pair trade gives us a relatively straightforward bet on the impact of lower interest rates while hedging against the possibility that stock trading activity will remain abnormally high. Still, even the pair trade is precarious given HOOD's excessive momentum of late, which is a key risk that speculators may want to account for.

Comments