Summary

- B. Riley's stock has fallen by 71% since I wrote a bearish opinion in 2021, as its income has declined while its balance sheet risks have grown.

- The company's future seems uncertain as short interest reaches 30%, making it among the most short-sold stocks today.

- Fundamentally, the company is operating too many segments, failing to develop a competitive edge in most, leading to low margins.

- B. Riley's securities lending business stands out compared to peers but could result in notable risks due to the potential undercollateralization of these loans in the event of a large market decline.

- Although B. Riley's risk exposure appears high, its performance may recover depending on macroeconomic circumstances. Further, its short interest is high enough that it has high short-squeeze potential.

AmnajKhetsamtip

In 2021, I published "B. Riley Financial: Declining Deal Volumes And Balance Sheet Leverage May Spell Trouble," detailing my bearish outlook on the investment bank, B. Riley (NASDAQ:RILY). At that time, most analysts had a bullish outlook on RILY due to its strong performance in the stimulus binge of 2020. Since then, RILY has fallen by 71% as its income has collapsed negatively due to its weak balance sheet and poor investment banking activity.

When I last covered it, I felt the company was overvalued and exposed to turbulence in the IB sector. Today, its situation appears even worse than I had predicted, as its market capitalization continues to hemorrhage, and short interest on the company piles on to a staggering 30%, making it one of the most short-sold stocks today.

Indeed, some investors may wonder if B. Riley may become the next Bear Stearns, given its staggering losses and strains in its capital markets segment. Of course, there are many differences between B. Riley's situation today and then. That said, investors should keep an eye on investment banks, as they often see significant declines ahead of others, given that they're typically dependent on high M&A activity. Globally, M&A activity has been extremely low lately, likely due to widespread economic stagnation and antitrust sentiment, causing the FTC to block many deals.

The coming quarters will be crucial for B. Riley's survival, as it cannot remain on its current trend for much longer. Of course, should its focus improve, the stock may prove discounted, trading far below its five-year average price. That said, RILY is not significantly below its pre-2020 price range, potentially implying it only lost the immense overvaluation it found that year.

Overview of B. Riley's Operating Segments

B. Riley operates through six significant segments. Based on data from its Q1 report, its capital markets segment is its most prominent, with $90M in sales but very volatile expenses due to varying trading P&Ls. That segment includes its investment banking segment, which has had some pressures but is more stable than its trading activity. Its capital markets segment had a negligible net income of $445K in Q1, but that could have been $30M if not for trading losses.

The company's second-largest segment is Wealth management, with ~$52M in Q1 sales but a low segment income of ~$1.68M. Wealth management often has stable revenues based on client assets, but with many investment banks focusing on this segment, its profit margins are weak after SG&A expenses.

Next is its auction and liquidation segment, which is focused on selling (primarily but not exclusively) physical assets for clients with financial challenges. This segment delivered $5.7M in total revenues at a $2M segment income, making this smaller segment one of its most profitable.

Its financial consulting segment had $35M in sales with a segment income of $2M, again pointing to low margins after paying its employees. B. Riley's communications segment is more attractive, with $82M in sales and a $8M segment income. That segment focuses on subscription services through its acquisition of United Online. Seemingly, that segment has little to do with its core business but is among its best-performing, though it lacks a clear growth trend.

Its final segment is consumer products, primarily through its acquisition of the computing product company Targus (which makes popular phone cases, etc). That segment had $51M in sales but posted a $3.4M loss, indicating difficulty competing. In my view, this may be a troublesome segment because cheaper Chinese companies increasingly dominate the consumer electronics accessory market. I am not alone in thinking this deal was unwise. Even if its valuation was low, I think it is relatively straightforward that most accessory-type items will be undercut by overseas competition.

I believe B. Riley is spread far too thin for its smaller size. It manages consumer-facing companies (lacking strategic value) and many different capital markets, investment banking, and other financial services. Today's financial services environment is extremely competitive because deal volumes are lower, so B. Riley's lack of economic scale leads to low margins.

Looking at its segment profitability, its employees are earning the most would-be profits. I believe that is a significant issue with investment banks as equity investments. Investment bank's greatest assets are their employees, not their capital base (since they don't do much traditional banking), so equity investors should not expect to reap the rewards of most financial services activity. In other words, high-value employees will gravitate toward financial services companies with the best pay, eroding profitability potential.

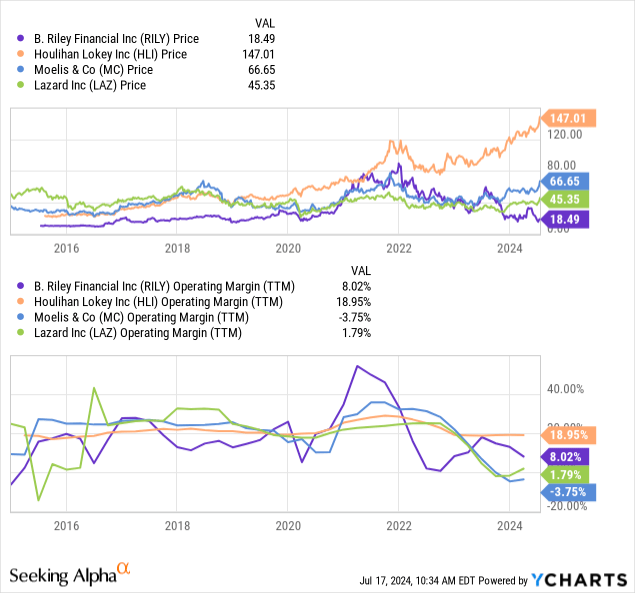

All of the boutique investment banks have differing business models, but for the most part, the current environment does not offer solid margins for most in the industry. Compared to peers, B. Riley's operating margins are particularly volatile, though its consumer-focused acquisitions give it better margins than Lazard (LAZ) and Moelis (MC). Houlihan Lokey (HLI) has far more stable margins due to its focus on financial restructuring, giving it an anti-cyclical hedge in today's rising corporate bankruptcy environment. See below:

Data by YCharts

Data by YCharts

I believe B. Riley's operating margins would be in a much more difficult spot if not for its communications segment, which is not closely tied to its core business. However, its core financial services business is more volatile than its peers, partly stemming from its heavier balance sheet. Compared to its peers, it is more focused on capital market activity, with a huge securities-based lending business focusing on lending to customers with unrealized investment profits.

While many other financial services companies may underserve this segment, I expect it will prove riskier. Last quarter, it posted ~$60M in securities lending interest income against $35M in related interest costs. Customers lend their securities to B. Riley for cash (at interest) to get liquidity without the tax event of realization. B. Riley then lends these securities back onto markets, likely to short-sellers who borrow them at interest.

This business can deliver significant profits on the related margins without significant capital requirements because it is not traditionally banking. That said, I believe it exposes the company to market risk. Customers can borrow 50-95% of their securities value as collateral, so if those securities lose value (potentially as low as 5%), then B. Riley may face lending losses on undercollateralized loans. This is a risk that investors may want to research more, as the potential related losses are difficult to estimate because they may become very asymmetric given a market crash. The company briefly mentioned this risk factor in its annual report, stating:

When we allow customers to purchase securities on margin, we are subject to risks inherent in extending credit. This risk increases when a market is rapidly declining and the value of the collateral held falls below the amount of a customer’s indebtedness. If a customer’s account is liquidated as the result of a margin call, we are liable to our clearing firm for any deficiency.

That is true for all firms engaged in securities lending and borrowing. However, my concern is how significant those assets and liabilities are ($2B to $3B) compared to its $530M market capitalization. B. Riley's assets to equity ratio is 22X, but its tangible equity value is negative due to its significant intangible assets. In my view, this exposes B. Riley to many solvency and liquidity risks in the event of a combined economic downturn (hampering its core business) with a market correction or crash that could surface critical risks in its capital market balance sheet.

The Bottom Line

I am bearish on RILY today, but I would not bet against it. Fundamentally, I think the company is spread too thin, focusing on far too many segments, and lacks considerable profitability in most. It does not help that the general capital markets and investment banking industries have been much weaker since 2022. Indeed, if IB activity improves and the economy returns to a growth trajectory without seeing considerable financial market turbulence, we may see a decent recovery in B. Riley's profitability. Further, in improved circumstances, the company may be able to sell its non-core assets, though I feel it is unlikely to see a gain on Targus.

RILY is also among the top-short-sold stocks, giving it a very high short-squeeze risk. RILY rose dramatically on Wednesday as part of the ongoing rotation trade, which may be related to the higher odds of Trump winning., who has a record of favorable corporate decisions such as the tax cut. Still, I don't see its fundamentals improving without indicating an economic turnaround.

As detailed in my recent articles, I believe the economic fundamentals point to a downturn that should result in a stock market decline due to the apparent overvaluation of many large-cap stocks. While the actual impact is nearly impossible to predict, B. Riley's balance sheet appears to have high-risk exposure to excessive market turbulence due to its securities lending business.

Overall, I think RILY's future is somewhat binary. If financial markets and the economy stabilize or grow, RILY should retain its current price and may see a decent rebound. However, if turbulence returns as I expect, I think RILY's downside risk is very high, depending on its ability to deleverage quickly enough and sell its non-core assets.

Comments