Summary

- Best Buy's share price has risen this year despite the continued deterioration in its sales outlook, pointing toward potential overvaluation.

- The company may not have a large enough cash reserve to offset potential negative cash flows in a recession.

- Consumer stability trends continue to point toward lower spending on discretionary items, potentially for a prolonged period.

- Since BBY may be more exposed to critical economic risks today, short-selling may be a profitable way to hedge market risks.

- Best Buy's long-term potential remains unclear. I doubt its traditional store model will remain profitable a decade from now due to demographic differences in online vs. in-store preferences.

patty_c/iStock Unreleased via Getty Images

Toward the end of last year, I published "Best Buy: The Electronics Store Era Is Coming To An End," detailing my bearish outlook on (NYSE:BBY). I expected that BBY would lose value at that time, but I explained that I would not bet against it, due to its historically low valuation. Since then, BBY has risen by 25%, which is about the same as the S&P 500 over the same period. Accordingly, it is an excellent time to provide an updated analysis of the company, to determine whether or not, my previous view is wrong or that it may now be a short opportunity stemming from its higher valuation.

It is worth noting that my previous stance had both a long-term and short-term component. At that time, I was skeptical of its short-term performance, stemming from general weakness in the consumer discretionary sector. To that end, my view has not proven correct, mainly as its holiday sales figures were fine. Its cyclical exposure could change, if we consider the ongoing deterioration in that data.

Further, my long-term view remains that BBY may not find long-term competitive stability in the increasingly e-commerce-driven market. I do not expect a permanent decline in Best Buy's performance, until the cyclical trend turns over. In other words, once it faces a typical cyclical economic slowdown, I expect Best Buy may need to close many of its stores, as more consumer activity permanently shifts away from in-store electronics shopping. Then, we must consider BBY's valuation and ability to adapt to changing conditions, likely shifting towards smaller stores.

Best Buy's Cyclical Risks are Worsening

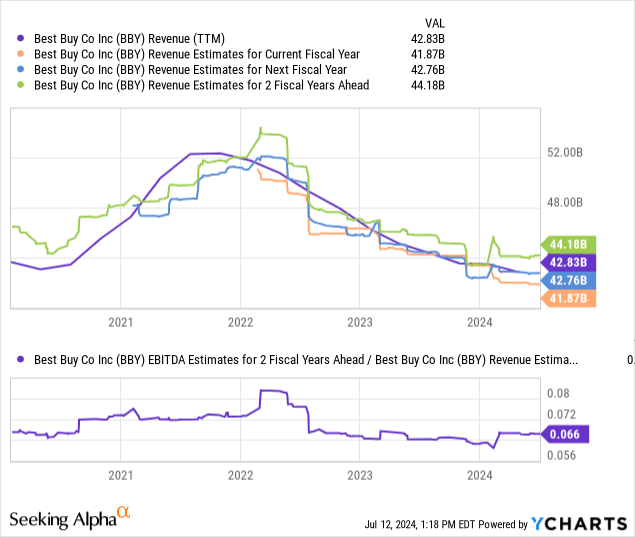

No doubt, BBY's gains, since I covered it, are strong. That said, expectations regarding its sales over the coming year or two have continued to deteriorate, although that has been offset by some improvement to its profit margin outlook. See below:

Data by YCharts

Data by YCharts

Since November 2023, Best Buy's TTM sales and estimates for 2024 and 2025 have continued to slide, albeit slower. That said, its two-year ahead sales estimate and its EBITDA margin outlook have improved slightly. Its sales outlook is also higher for the further-ahead data than the current fiscal year expectation, below its TTM sales. In other words, the analyst consensus indicates a difficult 2024-2025, followed by improvements through 2026.

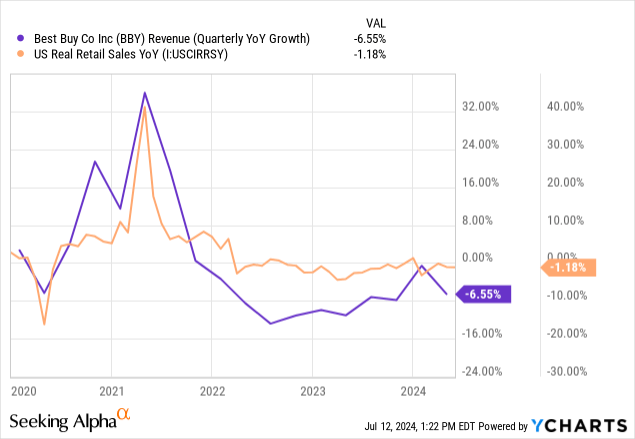

Best Buy's products are, to a great extent, discretionary items, some representing larger consumer purchases. Thus, the cyclical exposure to its sales is relatively high, particularly when considering lower discretionary spending capacity amongst many people. Its sales growth is well-correlated to changes in US retail sales adjusted for inflation. See below:

Data by YCharts

Data by YCharts

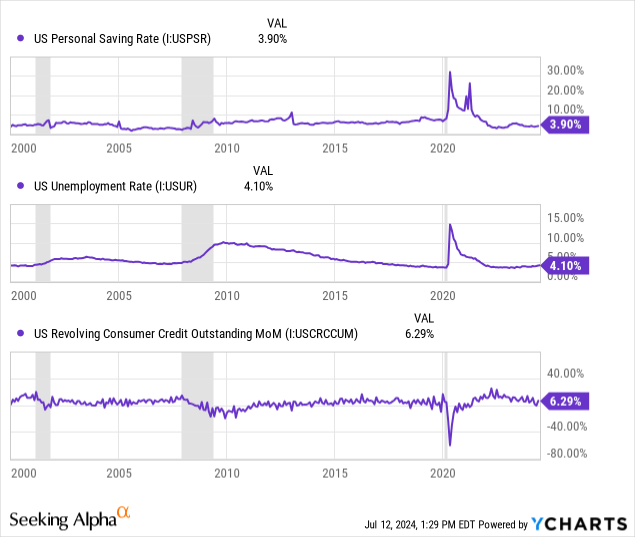

Historically, electronics are not as inflation-sensitive as most consumer goods, with the electronics CPI usually in a state of deflation; however, it is not totally representative of Best Buy's goods basket. Of course, people will reduce spending on electronics if they lack spending capacity, due to rising prices on other items. Thus, changes in excess incomes drive Best Buy's sales outlook and general US retail sales. We can determine that trend by considering personal savings, unemployment, and changes in credit card debt usage:

Data by YCharts

Data by YCharts

The lockdowns and stimulus of 2020 saw unprecedented changes to consumer stability, initially causing significant excess savings, despite unemployment (or because of it, as some saw incomes rise on unemployment). Around 2022, as excess demand caused prices to rise while incomes normalized, personal savings crashed to an abnormally low level (which remains true), causing more consumer activity to be driven by credit cards. Starting in 2024, we've seen a notable rise in unemployment and a negative trend in credit card spending, indicating a potentially negative pattern in consumer spending capacity. As I've explained in some recent articles, the employment trend is likely worse than the unemployment figure, if we also account for underemployment, dual employment, and weakening labor participation.

Opinions on this matter will differ, but to me, it looks pretty evident that the consumer spending trend is negative and is likely to worsen before it improves. I disagree that interest rate cuts will alleviate this trend, as we'll only see substantial rate cuts if we also see negative changes to employment and prices. Further, the theory that rate cuts improve consumer spending is likely incorrect in the modern economy. That may be true for businesses, but considering personal savings levels have declined while rates have risen, there is little reason to expect rate cuts will cause a further reduction in savings (promoting spending).

While not all of this data is available, it seems that retail-centric firms like Best Buy have become somewhat dependent on consumer credit card spending to offset lower excess spending capacity, which now appears to be reaching a limit.

As such, I believe Best Buy's current sales and EBITDA outlook will likely be incorrect. In particular, I doubt its sales and income will recover by 2025-2026, as it seems more likely that they should continue to deteriorate, as more people reduce credit card spending, particularly if they're facing unemployment (or underemployment).

A Long-Term View of Best Buy's Valuation

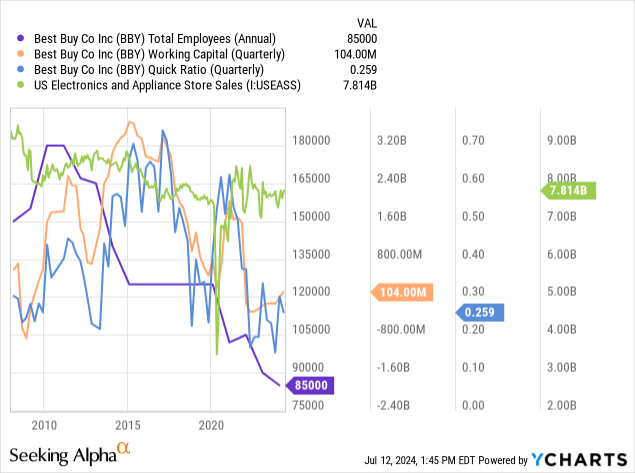

At this point, there is little Best Buy can do to offset the impact of a typical consumption and employment-driven recession. That said, for many years, the company has shifted away from pursuing growth toward improving efficiency and profitability at its existing stores. Its store count has declined consistently over the past decade, and its employee count has fallen even faster, particularly since 2020. This relates to the general weakness of US electronics and appliance store sales. That said, Best Buy's liquidity position is not as strong as I'd prefer, heading into a potentially difficult period. See below:

Data by YCharts

Data by YCharts

I've argued that Best Buy's sales over the 2010s are somewhat misleading regarding its overarching trend, because the company has benefited from the failure and bankruptcy of many of its large competitors. This is what I call the "last man standing" bias. Considering overall US electronics store sales, particularly if we adjust that figure for rising consumer prices, there is an evident long-term negative trend in that sector. By and large, consumer electronics spending is shifting towards Amazon.

Now that Best Buy lacks direct competitors (like Fry's Electronics, Circuit City, etc.), it faces most of the declines in the broader in-store electronics and appliance market. To me, this issue remains underappreciated, as Best Buy has only recently made a more significant effort to adapt to this roughly twenty-year-old trend. A decent amount of its overall sales are online. Still, it failed to grow that segment enough to improve its total sales, causing the company to reconsider investing in its physical stores.

In my view, there is a future for physical electronics and appliance stores. I imagine most people would prefer to interact with an electronic item rather than buy it online. That said, people are not necessarily willing to pay a considerable premium. Best Buy also faces issues stemming from the need for more labor, rent, and utilities overhead from operating large stores.

Further, while the company has partially avoided the growing retail theft trend, those measures can also detract from the in-store shopping experience. I do not know many people who prefer to wait for an employee to open cases; I prefer to shop online to avoid that nuisance. I am curious regarding the age demographic differences in this pattern, as some studies suggest that older people prefer physical stores. Hence, Best Buy is likely focusing more on the older generation, which also has more wealth. Still, I think that this demographic may make the "e-commerce shift" more rapidly, if the in-store experience deteriorates.

One solution may be a shift towards smaller "experience stores." The company has worked on this model since at least 2022 and has begun to open these stores at a much faster pace, with some focus on the Canadian market. I will be curious to see how these stores perform in the long-run, as they may have an advantage compared to Best Buy's traditional large store model. That said, shifting all its stores to this model would likely be costly (considering its leases on large buildings and more) and may not recoup its previous sales.

Admittedly, I can't estimate its income and sales ten years into the future, because it is difficult to say how Best Buy's model will change by then. I doubt that its existing model will remain by then, considering the rapid acceleration in retail issues since 2020. Further, recessions, particularly prolonged ones (unlike 2020), tend to accelerate secular trends. In other words, in the event of a significant decrease in consumer discretionary spending, I expect a permanent change in consumer spending habits toward e-commerce, particularly considering a recession would exacerbate theft-related issues. I believe this risk factor remains vastly underappreciated by the market.

The Bottom Line

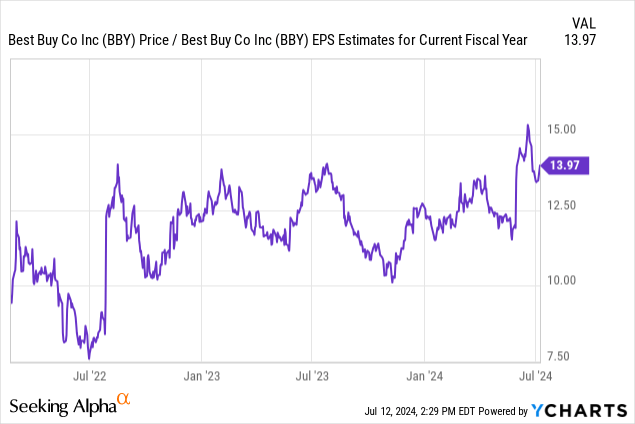

Last November, I was bearish on BBY, but would not short it due to its discounted valuation. Since then, analyst expectations on its future sales have continued to deteriorate. My outlook has also declined, given the recent rise in unemployment signals makes its recession exposure likely greater. Even more, its forward "P/E" valuation has risen markedly since November of 2023. See below:

Data by YCharts

Data by YCharts

In my view, a ~14X forward "P/E" is far too high for BBY, considering its negative sales trend. Its profit margins are also low, so it could easily face losses in the event of a decline in consumer spending. As noted earlier, its liquidity position is also not ideal, particularly its smaller cash reserve that may leave it in a poor place, should consumer demand turn over.

It is not guaranteed that consumer demand will decline. I've had a generally negative consumer spending outlook since 2022. Real retail sales have declined since, but not as fast as I had expected. That said, because we're now seeing an unemployment increase, the consumer spending trend may worsen more rapidly, particularly for discretionary items, such as most sold by Best Buy.

I do not have a specific price target on BBY because I think there is a wide range in how a recession may impact its valuation. A slight recession should cause its price to decline, but perhaps only back to late 2023 levels. However, I feel a much more significant economic decline could create serious challenges for Best Buy, given its secular issues and lacking cash reserves. At this point, I am confident that consumer spending will fall, but the extent of that issue remains unclear.

Of course, it is also possible that consumer strength will return, perhaps under dovish Federal Reserve decisions. It is also possible that new technologies will drive more excellent sales for Best Buy. Though I do not expect either, that is a significant risk in short-selling BBY.

BBY has moderate short interest at 6.4%, indicating some agree with my outlook and are willing to bet on it. That said, BBY's borrowing costs are not elevated. BBY's implied option volatility is also below its typical level, potentially making put options an attractive way to bet against BBY with defined risk. For me, as a macro-focused long/short investor and speculator, a traditional short bet is best, as I see BBY as a great short bet to hedge other long positions. In other words, I believe BBY carries far greater cyclical risk exposure than most stocks today. Thus, by betting against it, I feel it will fall asymmetrically in a recession, compared to my long positions.

If there is no recession (or a decline in consumer spending), then my argument will be fruitless. My views on BBY are predicted by my long-term outlook for retail stores and my cyclical outlook. Between the two, the cyclical outlook likely has more weight on BBY's stock price changes over the coming year. Thus, I do not necessarily expect BBY to lose value, if the economy remains stable. Still, at its current valuation, in light of its long-term risks, I do not think its upside is significant, even if the economy returns to a growth trajectory.

Comments