Summary

- Verizon's Q2 revenue miss has wiped out its ~8% YTD gains all at once, taking the stock's choppy performance this year back to square one.

- Yet the company has continued to deliver favourable progress on its three pillars - namely, wireless service revenue growth, adjusted EBITDA expansion, and FCF growth.

- Postpaid wireless net adds have also returned to the positive side, with increasing adoption of its premium myPlan and myHome offerings coupled with comparatively limited churn.

- Taken together, we view the stock's latest pullback as the final boarding call for close-to-7% dividend yield, as Verizon's fundamentals are poised for better days in 2H24 alongside greater valuation correlation to rising Treasuries amid impending rate cuts.

hapabapa

Verizon Communications Inc.'s (NYSE:VZ) year-to-date gains have been wiped out after its second quarter earnings were disappointing, highlighting the stock's choppy run this year. The stock's elevated volatility continues to reflect its strong correlation to long-end Treasury performance, as we had previously discussed, which has fluctuated due to rising rate cut expectations later this year. And Verizon's underwhelming report this week has only exacerbated the fundamental-driven component of the stock's valuation prospect.

Down to the fundamentals specifically, Verizon has delivered consistent positive progress in shoring up earnings and cash flow growth, with wireless service maintaining stand-out performance in recent quarters despite the broader revenue miss. Specifically, persistent momentum in gross postpaid phone additions at Verizon of +12% y/y, despite limited net adds, continues to be a key growth driver alongside accretive ARPA expansion during the quarter. This is largely in line with anticipated favourable contributions from a "full quarter's impact of recent pricing actions" implemented earlier this year. Reduced churn also highlights Verizon's consistent delivery of an improving value proposition, which was further resonated through its recent rebrand with "customer-first programs".

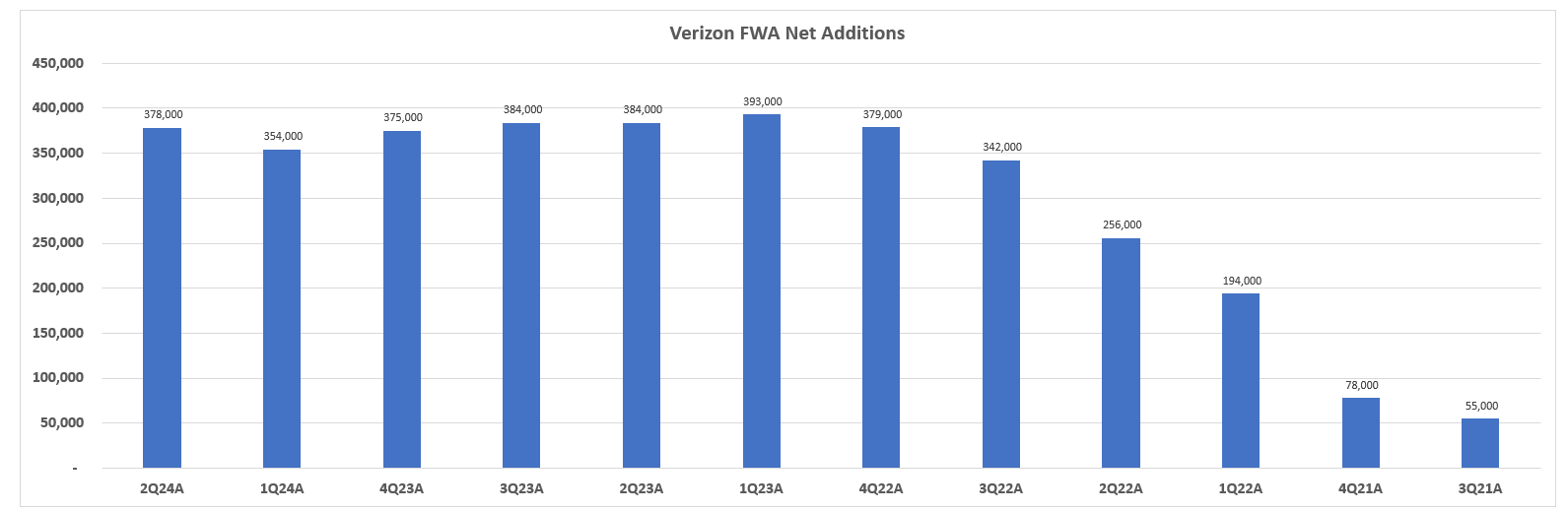

Persistent strength in wireless mobility also complements resilient demand for Verizon's broadband offerings, especially fixed wireless access ("FWA"). Specifically, Verizon reported 378,000 FWA net adds during Q2, up from 354,000 in Q1, with the revenue stream upholding its broadband segment subscriptions. Verizon's recent introduction of the myHome internet bundle plan is likely to further reinforce its broadband market share gains. The newly introduced home internet bundle is expected to imitate the success of its equivalent in wireless mobility - namely, myPlan - in amplifying ARPA growth at Verizon, and contributing to a higher premium revenue mix.

Despite Verizon's Q2 revenue miss, its latest results continue to reinforce confidence in its near- and longer-term FCF growth trajectory critical to its ongoing deleveraging efforts and industry-leading dividend payout. It also assuages earlier concerns over near-term cost headwinds stemming from lower capitalized interests amid an elevated borrowing cost environment, given the near-complete deployment of Verizon's C-band spectrum licenses. Verizon's improved 1H24 performance provides a strong foundation for incremental operating tailwinds in the latter half of the year. They include a resilient demand environment reinforced by seasonality, as well as favourable prospects of an AI-driven mobile device upgrade cycle that could spur incremental uptake of premium plans. This will likely bolster Verizon's near-term valuation gains with tangible fundamental strength, while also compensating for an anticipated dividend yield reduction as impending rate cuts materialize.

Regaining Momentum in Consumer Wireless

Despite being the largest mobile carrier in the U.S., Verizon has been challenged by intensifying competition as it grapples with sporadic market share losses in recent years. Yet the company's pivot towards a risky premium strategy, with the roll-out of its myPlan campaign, continues to pay strong dividends. Specifically, myPlan, which encourages sign-ups on higher-priced unlimited plans by offering discounted add-on perks like popular streaming services, has benefitted from robust adoption. Up from 20% in Q1, myPlan subscriptions currently account for 30% of Verizon's postpaid phone base. This continues to show consistent positive progress in Verizon's newfound focus on driving wireless service growth.

Strong myPlan uptake also coincides with the first full quarter's impact of recent price increases implemented earlier in the year. Recall that Verizon had implemented a $4/month increase to its premium 5G plans at the beginning of March. Yet wireless retail postpaid phone churn has remained at low levels of 0.89% during the initial implementation of recent pricing actions in Q1, with further improvement to 0.85% exiting Q2.

The results continue to underscore Verizon's strong value proposition to the consumer end-market despite intensifying competition. Meanwhile, Verizon has also maintained a measured approach to recapturing market share, ridding itself of the competitive pricing strategy implemented in the past, which had burdened its profits and cash flows.

Specifically, the company's recent rebrand also solidifies emerging tailwinds in the back half of the year. Verizon's recent roll-out of new "customer-first programs" resonates well with the inherently price sensitive retail vertical, in our opinion, especially given ongoing macroeconomic uncertainties and their adverse implications on consumer end-markets.

As mentioned in the earlier section, myHome represents Verizon's latest offering aimed at bolstering its value proposition to price sensitive consumers looking to do more with their monthly subscriptions. With a home internet base plan that starts at $35/month, myHome allows subscribers to select "add-on perks" for an additional $10/month that span popular streaming services like Netflix, Inc. (NFLX) with ads, Warner Bros. Discovery, Inc.'s (WBD) Max with ads, and/or The Walt Disney Company (DIS) bundle that includes Disney+, Hulu and ESPN+; lifestyle benefits like Walmart Inc.'s (WMT) Walmart+; and pay-TV services like Fios TV or Alphabet Inc.'s (GOOG) (GOOGL) YouTube TV. The roll-out of myHome is not only expected to help maintain sustainability in Verizon's broadband growth momentum, primarily in FWA, but also become incrementally accretive to wireless ARPA. We believe the roll-out of myHome will also complement Verizon's recent expansion of its C-band coverage to suburban and rural areas in driving the near-term FWA broadband base to 5 million.

Author, with data from verizon.com

Author, with data from verizon.com

In addition to myHome, Verizon's consumer end-market also benefits from the recent introduction of a "guaranteed trade-in program", which promises a payout no matter the condition of the swapped device under myPlan unlimited tier subscriptions. Taken together, the continued ramp of Verizon's recently introduced value-added services to the consumer wireless end-market is expected to reinforce expectations for a sustained, albeit modest, topline growth alongside margin expansion at scale. This would be critical to sustaining Verizon's FCF trajectory, which underpins ongoing deleveraging efforts, its industry-leading dividend program, and most importantly, its valuation prospects.

A Balanced Approach to Cash Flows

Verizon has also continued to undertake a more balanced approach than its rivals when it comes to sustaining its pace of margin expansion and resulting cash flow growth. This includes a measured pace of device- and equipment-related spending, which have typically been attributable to aggressive promotions and discounts.

Specifically, Verizon's measured equipment cost trajectory in recent quarters has been a key driver in enabling margin expansion of 80 bps during Q2 and, inadvertently FCF growth through 1H24. Admittedly, lower wireless equipment upgrades in recent periods have played a role in this. This has unfortunately been coupled with incremental pressure on its topline growth, as wireless equipment revenue accelerated its decline to -13% y/y during Q2, worsening from -6.9% y/y in Q1. But the company's disciplined spending management is also apparent in its day-to-day operations.

This is consistent with Verizon's recent "guaranteed trade-in program" introduced as part of its rebrand, which differs from a comparatively more aggressive approach from rivals like AT&T. Specifically, AT&T has taken "pre-emptive" measures ahead of the anticipated upgrade supercycle unleashed by Apple Inc.'s (AAPL) upcoming AI-enabled iPhone 16 with the launch of its "AT&T Next Up Anytime" add-on plan feature. The Next Up Anytime feature comes at an extra $10 per month and allows AT&T's premium plan subscribers to upgrade their device as many as three times a year as long as they have paid off one-third of the existing device's cost. In addition to encouraging early upgrades, AT&T also provides the highest trade-in subsidy amongst the Big Three U.S. carriers of as much as $1,000 per qualified device.

In contrast, Verizon's maximum device trade-in subsidy is capped at $840. Its recently introduced trade-in program also promises myPlan subscribers a guaranteed trade-in subsidy, regardless of the condition of the device - spanning smartphones, smartwatches, tablets, and other digital accessories. Not only does the strategy preclude Verizon from margin dilution risks related to aggressive promotions and rebates, but it also helps to upsell its premium myPlan offering in the consumer wireless business by providing consumers with an added incentive.

Looking ahead, Verizon could potentially introduce a more competitive promotional offering as Apple's new smartphone rolls out in September, while also taking advantage of the coinciding back-to-school season. However, we expect Verizon's prudently measured approach to device subsidies in recent quarters to continue, which is in line with management's expectations for continued growth and FCF expansion through 2H24.

Another cash flow accretive lever for Verizon this year includes the potential sale of some of its mobile tower inventory. Recent reports are estimating that Verizon has earmarked up to 6,000 mobile phone towers for sale this year, which could generate proceeds of more than $3 billion. Management has refrained from commenting on the matter during Verizon's 2Q earnings update, but instead turned its focus towards their steadfast commitment to driving cash flow. Yet tower sales have been a frequent cash-generating strategy implemented across U.S. telco carriers - and this would not be Verizon's first rodeo either. The company generated $5 billion in proceeds to support its 5G capex cycle in 2015 from the sale of "rights to lease and operate" 11,300 wireless towers to American Tower Corporation (AMT). Given Verizon's continually pressing capital allocation priorities, which include aggressive deleveraging and a commitment to consistently raising annual dividends, a sale of some of its mobile phone tower inventory could be potentially accretive to its FCF target this year.

Final Thoughts

Verizon's Q2 results show that it is continuing to regain market share slowly, but surely. This organic fundamental strength stemming from its core operations will be complementary to its reduced capital expenditures following the 5G build cycle, and help offset the imminent impact from lower capitalized interest on relevant investments as well. And ensuing strength in FCF growth expected through 2H24 will be critical to its deleveraging efforts, dividend program, and most importantly, valuation prospects as the stock's correlation with Treasuries potentially reduces yield for Verizon's income-focused investor base later this year.

Comments