Summary

- Lockheed Martin Corporation has shown remarkable performance, outperforming the S&P 500 by 60 points over the past decade.

- The company's recent 2Q24 earnings report revealed strong revenue growth, an impressive backlog, and progress in the F-35 program.

- Lockheed Martin's raised guidance, stock buybacks, and commitment to R&D indicate renewed momentum and potential for sustainable long-term gains.

inhauscreative

Introduction

It's time to talk about Lockheed Martin Corporation (NYSE:LMT), a company that was my biggest holding until I bought the Texas Pacific Land Corporation (TPL) this year.

During the pandemic, I started accumulating LMT stock for a number of reasons, including its anti-cyclical business model, its position at the very top of the NATO defense supply chain, and the fact that due to pandemic and government budget-related headwinds, the stock was simply irresistible (read: cheap).

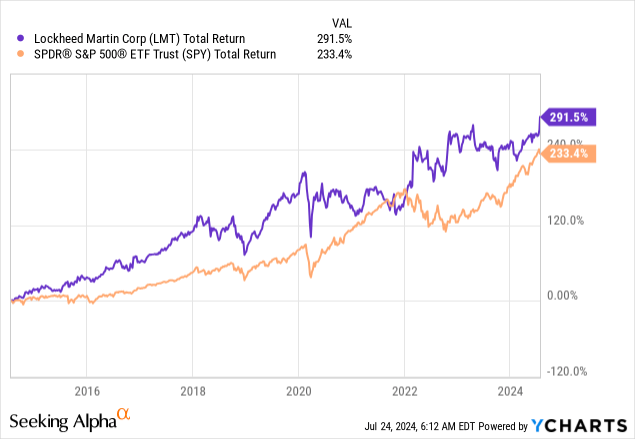

Despite these challenges, Lockheed Martin has returned 292% over the past ten years, outperforming the tech-heavy S&P 500 by roughly 60 points.

Data by YCharts

Data by YCharts

This is a remarkable performance, as the giant has been struggling since 2021, pressured by ongoing supply chain headwinds, defense budget uncertainties (i.e., continuing resolutions), and issues with new F-35 updates.

As a result, earnings during the past 2-3 years were often mixed.

Fortunately, that has now changed.

The just-released 2Q24 earnings were absolutely fantastic, as it saw growth across the board, high demand, and higher guidance.

Since my most recent article on May 20, titled "Seeking Alpha? Lockheed Martin Is The Place To Be," the stock is up 8.1%, beating the 4.7% return of the S&P 500 by a decent margin.

The stock was up more than 5% after its earnings.

In this article, I'll update my thesis and explain why the just-released earnings are a game changer.

So, as we have a lot to discuss, let's get to it!

Lockheed Is Back!

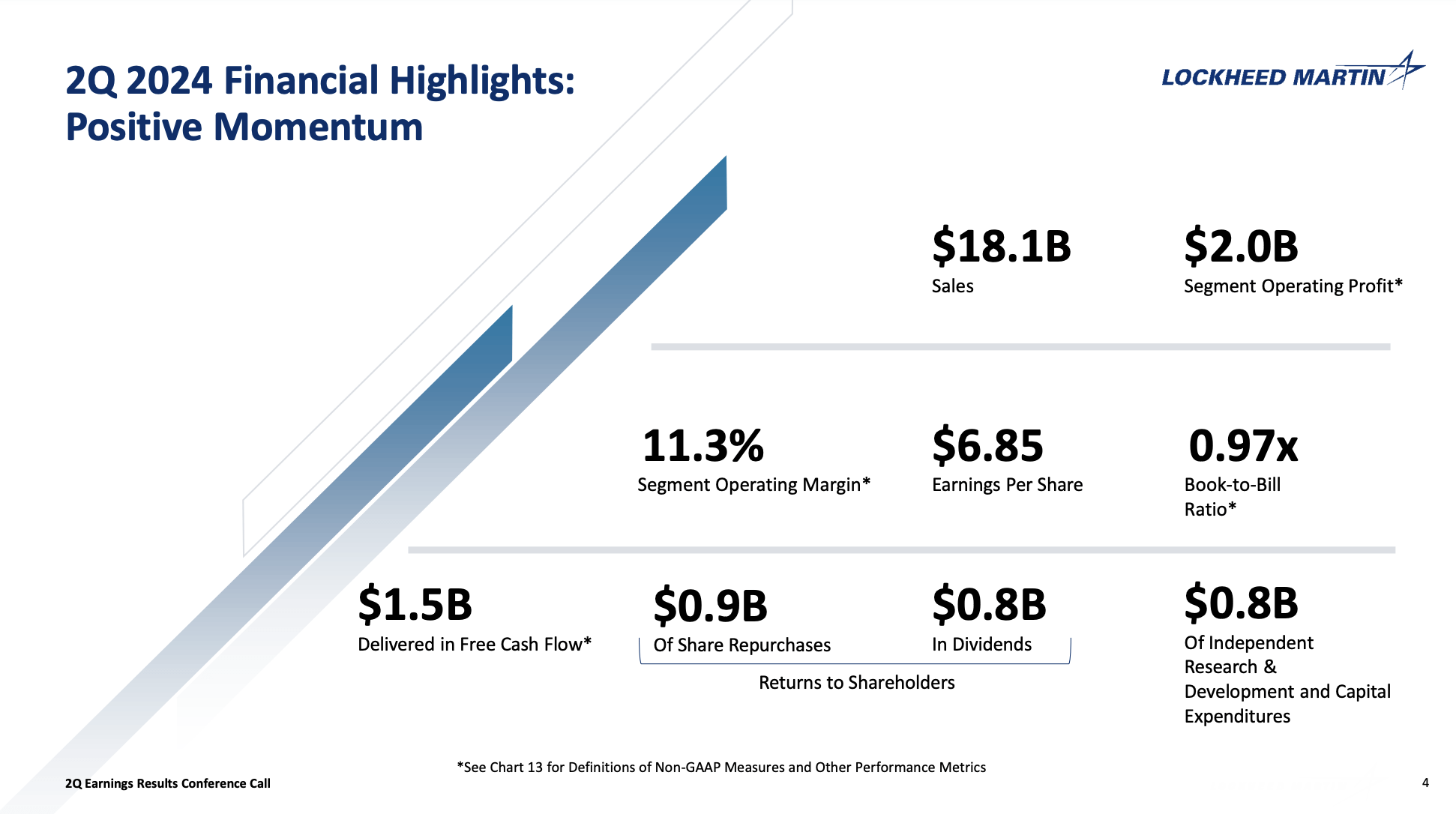

In 2Q24, Lockheed reported adjusted EPS of $7.11, beating estimates by $0.66. Revenue came in at $18.1 billion, roughly $1.1 billion higher than expected.

Total revenue growth was 9% on a year-over-year basis and 5% on a sequential basis.

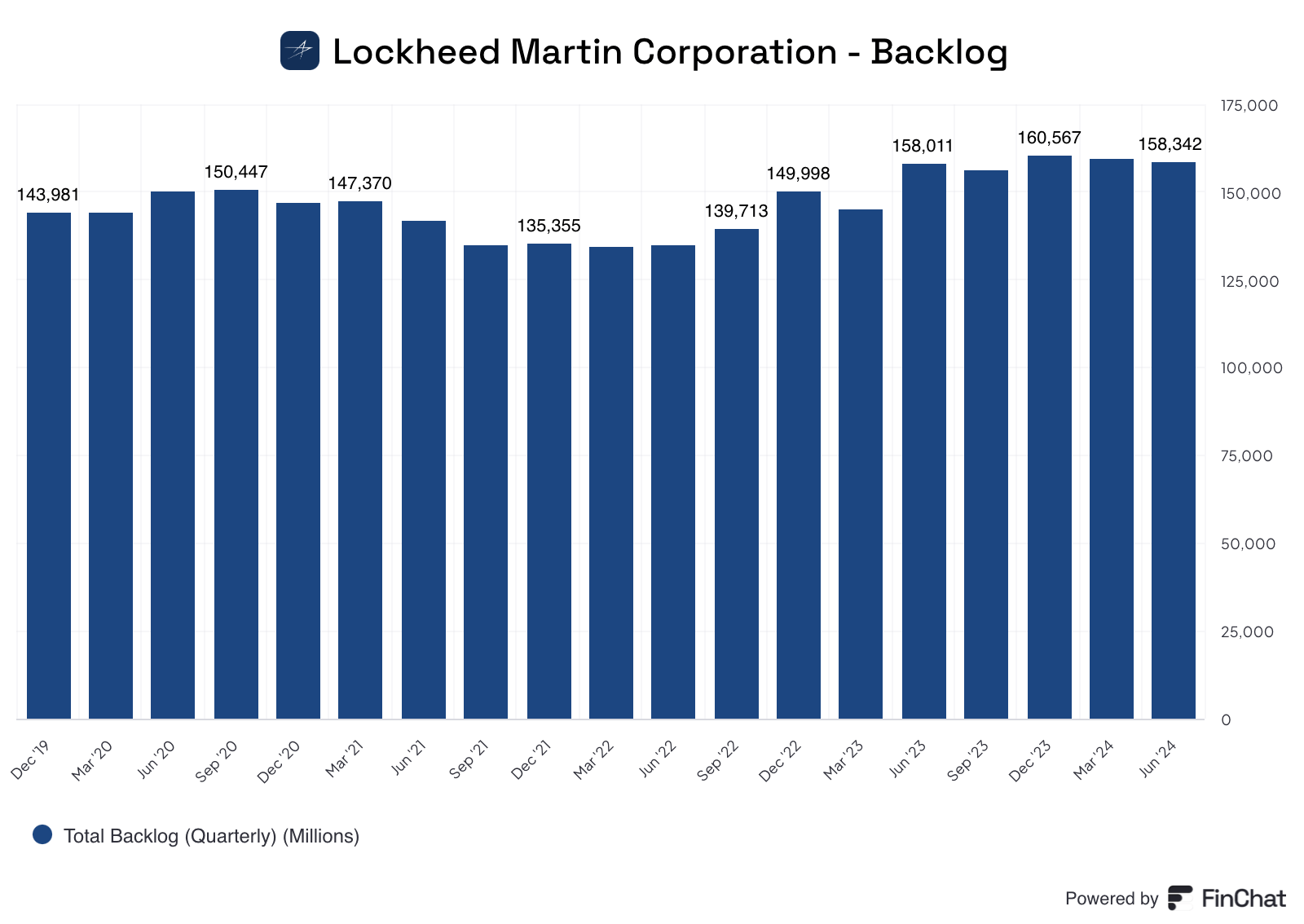

This was supported by an impressive backlog of almost $160 billion, which is more than twice the company's annual revenue.

FinChat

After securing more than $17 billion in new deals, the total book-to-bill ratio is roughly 1.0, indicating that new orders and production are in line.

Lockheed Martin

Moreover, Lockheed Martin has shown improved operational efficiency, which is reflected in its segment operating margins of 11.3%, a 20 basis points increase compared to the previous year's second quarter.

Before we dive into more financial numbers, one very important thing that stood out is the company's progress in updating the F-35 program, which includes the Technology Refresh 3 (TR-3) upgrade.

This program had many issues in the past. In my most recent article, I used the quote from Bloomberg below:

The first fully capable TR-3 jets were supposed to be delivered in July 2023, but the program has been dogged by problems with the new software and a new integrated core processor for combat missions. The plane needs the full upgrade before it can carry more long-range precision weapons, gather more information on enemy aircraft and air defenses and operate more effectively with other aircraft. - Bloomberg

Now, there's good news, as the company gave great F-35 production guidance. I added emphasis to the quote below:

We continue to produce at a rate of 156 aircraft per year and expect to deliver 75 to 100 aircraft in the second half of 2024. Over 95% of TR-3 capabilities are currently being flight-tested, and we look forward to delivering full TR-3 combat capability to the customer. In addition, we expect deliveries of F-35 aircraft to exceed production for the next few years. - LMT 2Q24 Earnings Call

The "exceed production" part of the quote above was key, as the F-35 accounted for about a quarter of the company's total sales last year.

Moreover, speaking of the F-35, the company secured new deals, including Israel's expansion of its F-35 fleet and new potential deals with Greece and Romania. Israel is key, as the nation is at war and looking to add a third squad of F-35 jets, potentially increasing their total fleet by 50%.

The Times Of Israel

The company is also collaborating with partners like the Australian Department of Defense on the Joint Air Battle Management System and German defense giant Rheinmetall for the Global Mobile Artillery Rocket System ("GMARS"), a program that could not come at a better time, given strong defense spending growth among European NATO members.

This [GMARS] is a highly interoperable 2-pod launcher system intended to fire the MLRS-based munitions. Combining these combat-proven systems will help address the growing demand for long-range rocket capabilities in Europe and elsewhere. - LMT 2Q24 Earnings Call

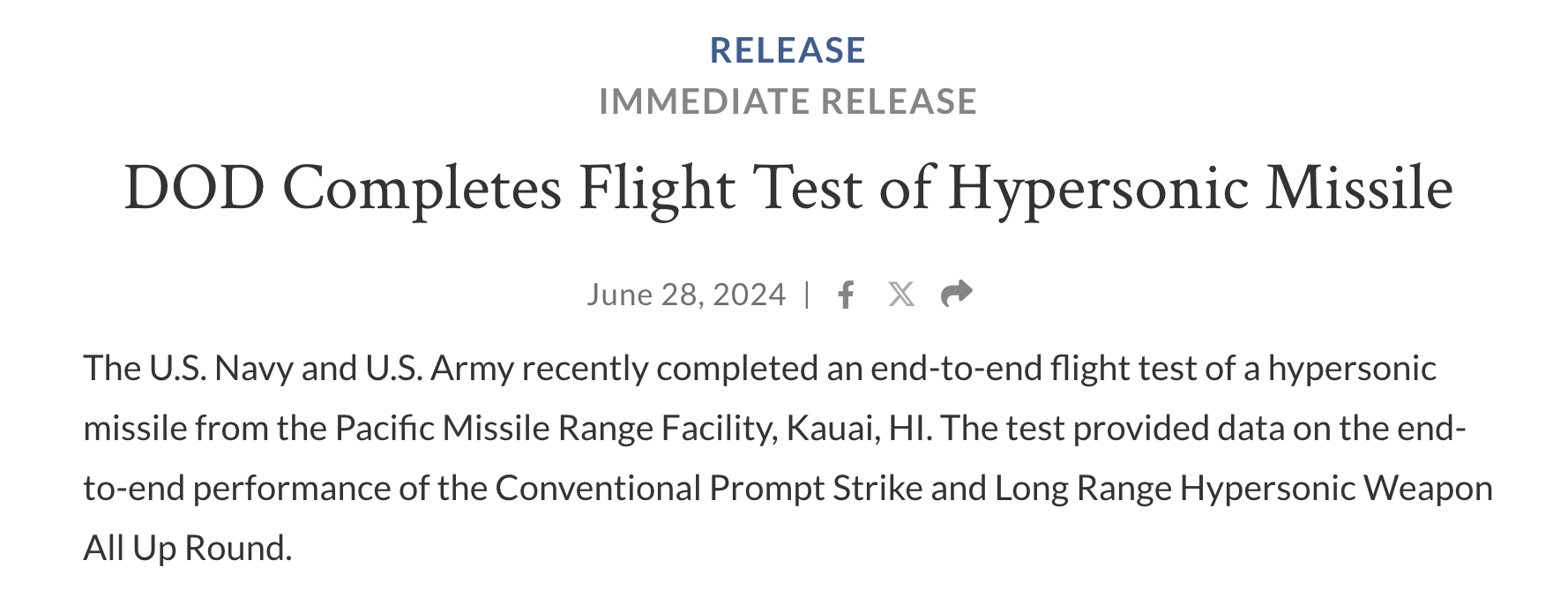

Lockheed also sees progress in defense technology with successes in hypersonic strike capabilities and AI-driven autonomous flight operations.

The recent successful tests of the U.S. Navy's Conventional Prompt Strike and the U.S. Army's long-range hypersonic weapons programs are great examples of key programs with bright futures when it comes to demand.

Department of Defense

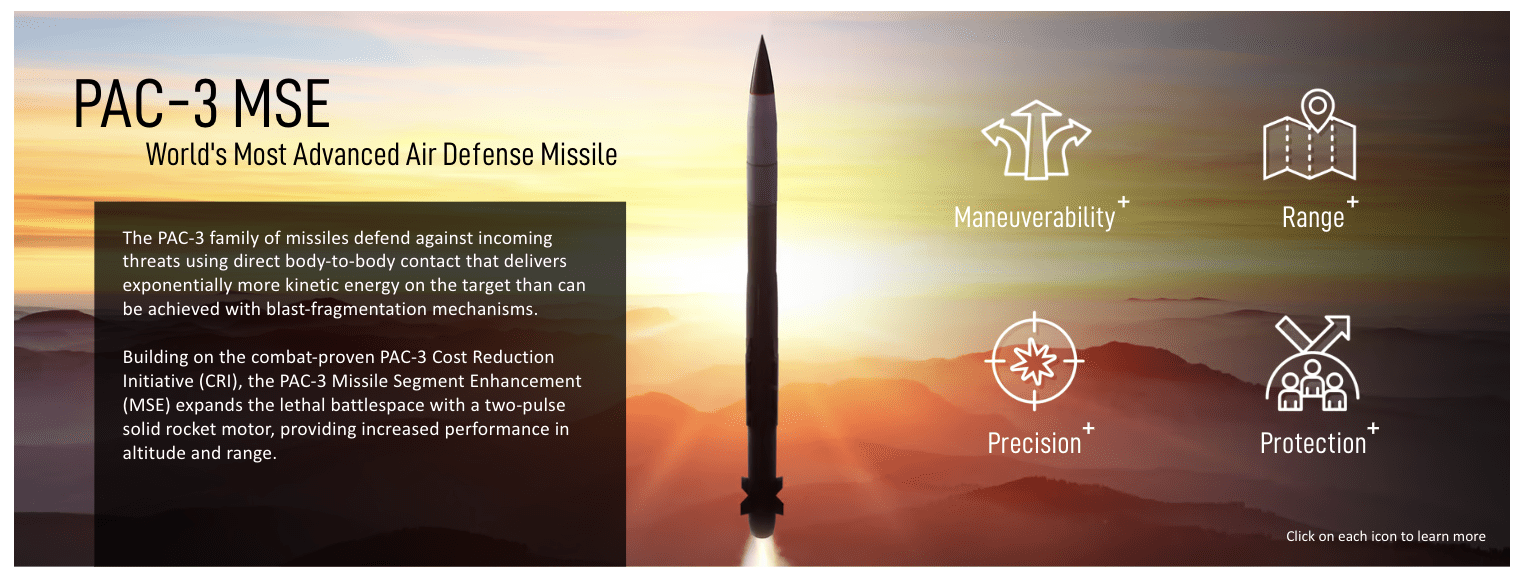

Based on this context, and with regard to the demand picture, the company's Missile & Fire Control segment saw a book-to-bill ratio of more than 2.0, which indicates that demand is coming in twice as fast as it has the ability to finish products.

This is boosted by multi-billion demand for its PAC-3 (interceptor) missiles and 400 JASSM-ERs (air-launched cruise missiles) for Poland.

Lockheed Martin

Beyond the F-35 and advanced missiles, the company also saw growth in the F-16 and C-130J program.

The F-16 initially launched in 1978 and is still one of the world's most capable jets. This year, Lockheed targets 20 deliveries. The C-130, which was launched in 1957, 12 years after the Second World War, is also expected to see 20 deliveries.

Meanwhile, NASA picked Lockheed to develop its next-gen weather satellite constellation.

Lockheed Martin

So, what does this mean for shareholders?

Great News For Shareholders

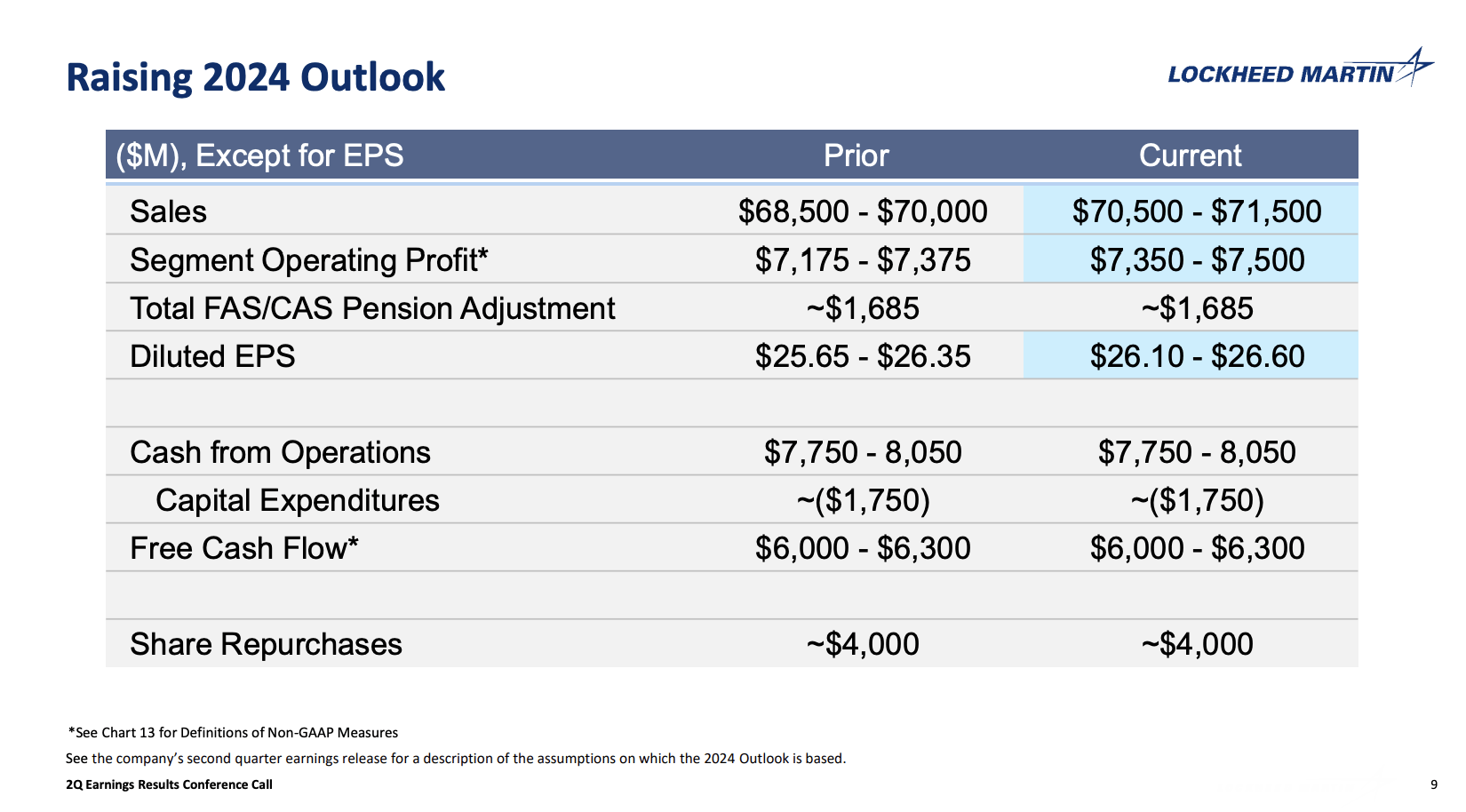

Thanks to great financial results, the company raised its guidance, increasing its 2024 sales forecast by $1.75 billion, resulting in a new sales range of $70.50 billion to $71.50 billion.

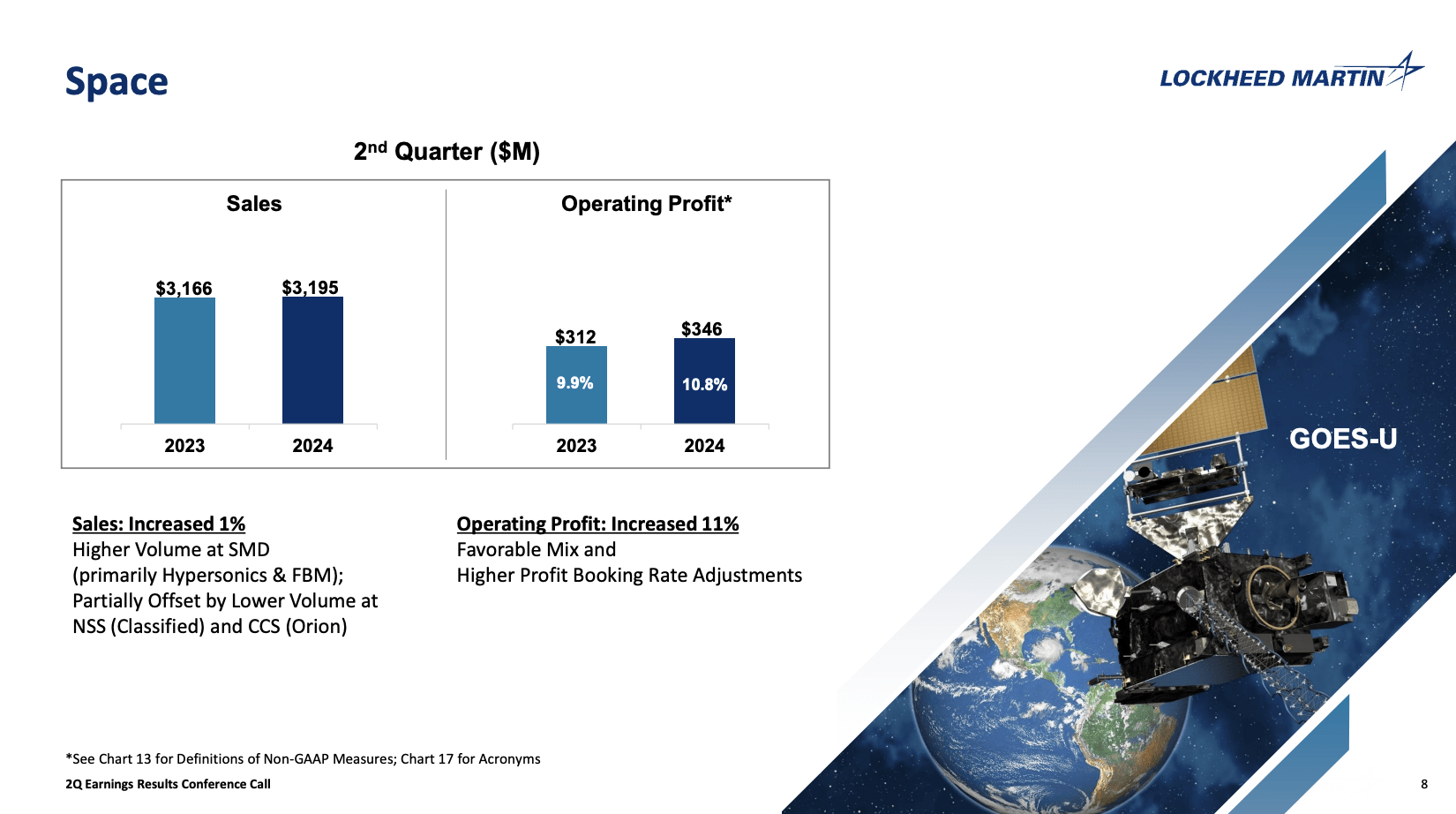

This adjustment reflects a solid 5% growth rate compared to last year, driven by improvements across all four business areas: Aeronautics, Missiles and Fire Control, Rotary and Mission Systems, and Space Systems.

Moreover, as we can see below, the company also adjusted its segment operating profit expectations to a range of $7.35 billion to $7.50 billion.

Lockheed Martin

Full-year EPS is expected to be in the $26.10 to $26.60 range, with free cash flow expected to remain in the $6.0 billion to $6.3 billion range.

FCF guidance was not hiked because the company wants to give itself some room in case of deferred payments for F-35 deliveries. I agree with that decision, as F-35 deliveries are still its biggest bottleneck.

If deliveries go smoothly, we'll likely see an FCF guidance hike in the next 1-2 quarters.

For shareholders, all of this is great news, as the company plans to buy back stock worth $4 billion this year - in addition to spending $3 billion on R&D and capital investments.

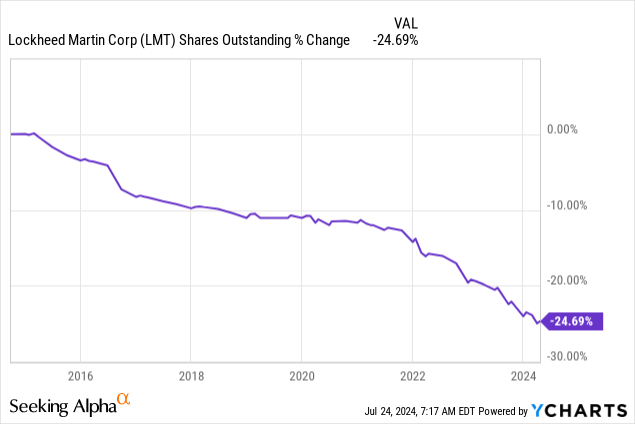

These buybacks are roughly 3.4% of its current market cap. Over the past ten years, LMT has bought back a quarter of its shares, which significantly contributed to its favorable total return during this period.

Data by YCharts

Data by YCharts

Moreover, the company, which returned more than 100% of its free cash flow to shareholders in the second quarter, pays a very reliable dividend.

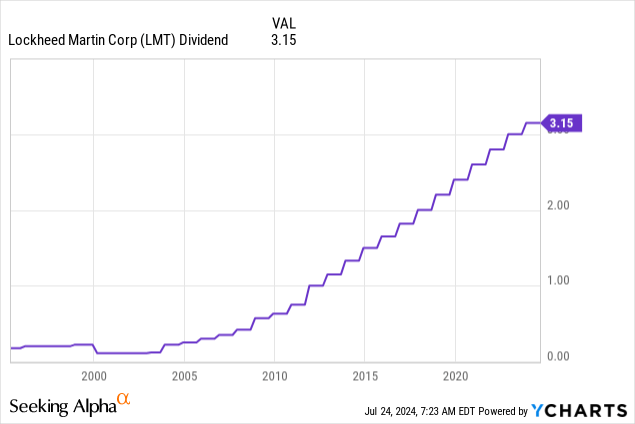

Currently yielding 2.5%, the dividend has a 47% payout ratio, a five-year CAGR of 7.7%, and a track record of 21 consecutive annual hikes.

Data by YCharts

Data by YCharts

It also helps that despite its recent stock price surge, the valuation is still attractive.

Valuation

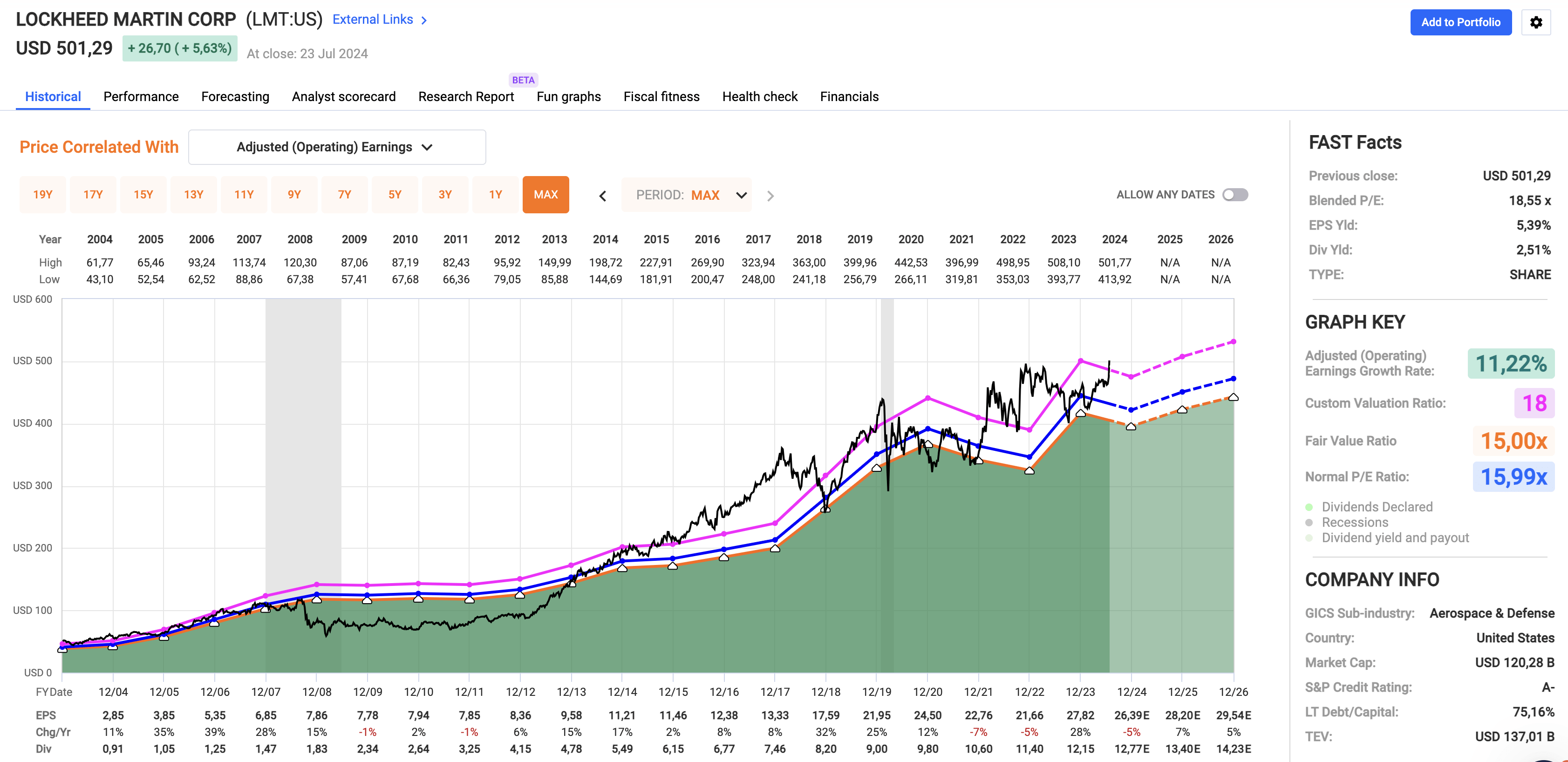

Lockheed has a normalized P/E ratio of 16.0x. However, in recent articles, I have used a 17.7x/18.0x multiple, which is its ten-year average.

Using the FactSet data in the chart below, we see Lockheed had four years of negative EPS growth since 2020, including 2024E.

2025 and 2026 are expected to see mid-single-digit EPS growth, giving the stock a fair stock price of roughly $531, 6% above the current price.

FAST Graphs

While 6% upside potential is not spectacular, the company is likely on a path to elevated long-term growth, benefitting from consistent budget growth, high demand (including from international customers), fewer supply chain constraints, successful F-35 updates, and secular growth in space and missile defense.

As such, I believe the current breakout is for real (sustainable), likely paving a path to outperforming long-term gains.

Takeaway

Lockheed Martin's earnings reveal a major turnaround, showing strong revenue growth, an impressive backlog, and important F-35 program progress.

With an 8.1% stock increase since my last article, it's clear that the company's strategic moves are paying off.

The raised guidance, substantial stock buybacks, and commitment to R&D support Lockheed's renewed momentum.

Moreover, the stock's valuation remains appealing, and with increasing demand and fewer headwinds, I believe Lockheed Martin is poised for sustainable long-term gains, making it a fantastic dividend growth stock.

Pros & Cons

Pros:

- Strong Recent Performance: Lockheed Martin's 2Q24 earnings were stellar, with revenue up 9% year-over-year and impressive growth across all segments.

- Robust Backlog: A backlog of almost $160 billion highlights solid future revenue visibility and operational strength.

- F-35 Program Recovery: Significant progress in the F-35 program and optimistic delivery forecasts support future growth.

- Attractive Valuation: Despite recent gains, the stock's valuation remains appealing.

- Shareholder Returns: The company is aggressively buying back stock and maintains a reliable dividend with a history of consistent hikes.

Cons:

- Ongoing Supply Chain Issues: Despite improvements, supply chain challenges and F-35 delivery bottlenecks still pose risks.

- Mixed Recent Earnings: The past 2-3 years have seen earnings volatility, reflecting broader industry uncertainties.

- Global Defense Spending Risks: Geopolitical tensions and defense budget shifts could impact future growth.

- High Valuation Multiples: While the current valuation is attractive, it's slightly above the long-term average, potentially limiting short-term upside if it encounters new headwinds.

Comments