Goldman Sachs is once again recommending straddle options, a strategy where investors buy both call and put options. Goldman believes that with U.S. stocks reaching new highs this year, options might be a more attractive alternative to owning the stock outright.

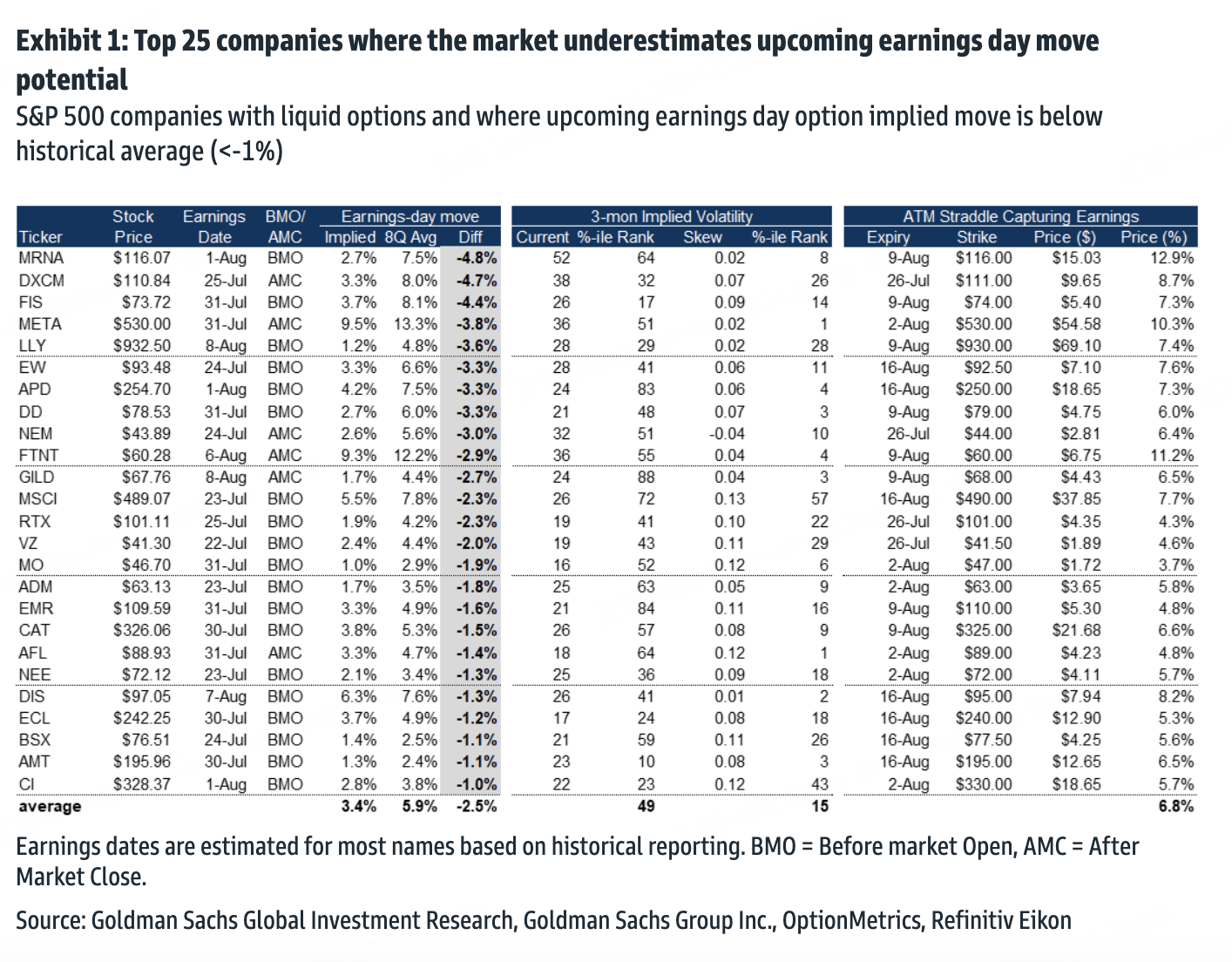

Goldman Sachs identified 25 companies where they believe the implied volatility (IV) underestimates the potential stock price movement on earnings day, making straddle options appealing. Among these, notable picks include $Meta Platforms(META)$ $Eli Lilly(LLY)$ and $Marathon Digital Holdings Inc(MARA)$

Meta Platforms (META): With earnings set for July 31, Goldman suggests buying straddles before IV spikes. The implied earnings day stock movement is +/-9.5%, below the average of +/-13.3% over the past eight quarters. They recommend purchasing at-the-money straddles expiring on August 9.

Due to Meta's competition with Trump Media & Technology Group (DJT), the stock has lagged behind other tech giants, making direction hard to predict. However, significant volatility is expected.

Goldman also recommends two direct Buy Call options:

Microsoft (MSFT)**: Ahead of its July 30 earnings, Goldman suggests buying August 9 call options with a strike price of $450, anticipating a rise in volatility.

GE Vernova Inc. (GEV)**: A spin-off from GE, Goldman sees GEV benefiting from the energy transition, particularly in power and electrification sectors, making it a top earnings pick.

Goldman has often recommended straddle options during earnings season. This strategy bets on volatility rather than price direction, profiting from significant stock price movements regardless of direction.

Other specific names on the list include:

Before, I introduced two types of straddles: Straddle and Strangle:

Straddle, also known as saddleback, involves buying call and put options with the same strike price and expiration date, typically close to the current price (ATM). This strategy's main advantage is speculating solely on volatility without predicting direction. However, if the stock price doesn't move significantly, the risk lies in the inability to offset the cost of buying two options.

Strangle is an asymmetric straddle option, also known as a wide straddle. Unlike Straddle, it involves buying call and put options with different strike prices but the same expiration date, typically out-of-the-money (OTM). Profits can be made when the price breaks through a certain range (whether up or down), betting on volatility. This strategy is suitable for stocks with highly volatile prices, typically growth or tech stocks.

Straddle options are more expensive than buying individual call or put options because they involve buying two contracts. Therefore, the biggest risk is if the volatility falls short of expectations, and one side's gains are insufficient to cover the cost of both sides, resulting in a loss. However, as an option buyer, the maximum loss is limited to the premium of the two contracts.

To summarize, straddle options are a volatility play, a direction-neutral strategy. By purchasing them a week before earnings and benefiting from the significant stock price fluctuations after the earnings release, investors can achieve excess returns. They can also sell for profit on the day before earnings when option IV reaches its peak. For specific details, please refer to the two articles mentioned above.

Comments