Summary

- Hedge funds have turned bearish on commodities, similar to 2016. Concerns about China’s growth and supply issues are affecting the market.

- Despite the bearish outlook, there's potential in Canadian energy stocks like Cenovus, which boasts strong assets and a commitment to returning cash to shareholders.

- Cenovus, with low costs and long reserves, is undervalued. Its focus on debt reduction and generous dividends makes it an attractive investment opportunity.

ImagineGolf

All financial numbers in this article are in Canadian dollars unless noted otherwise. Please note that oil and gas prices are always in U.S. dollars.

Introduction

"Nobody" is bullish on commodities anymore.

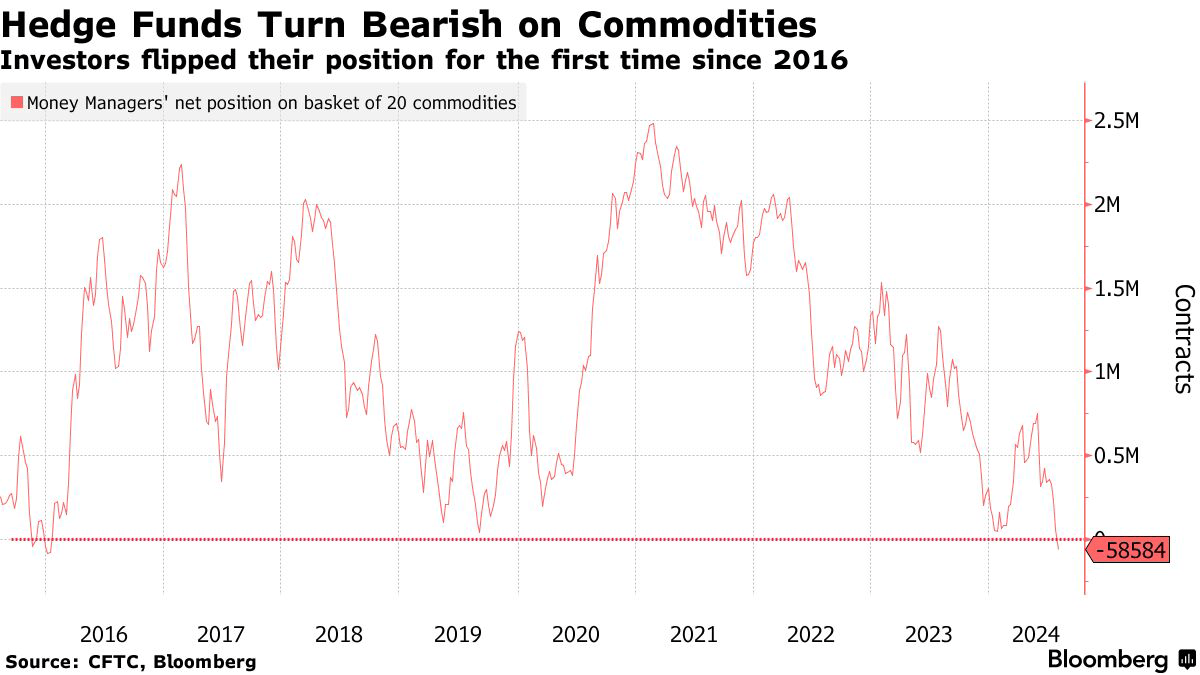

As reported by Bloomberg on August 2, hedge funds (money managers) have turned bearish on commodities for the first time since 2016. In this case, "bearish" is defined by having net short positions, as the chart below shows.

Bloomberg

This is absolutely fascinating, as 2016 was a horrible year for commodities, pressured by a global manufacturing recession, a very strong dollar, and a lot of political uncertainty.

According to Bloomberg, we are now dealing with similar issues (emphasis added):

The reversal underscores mounting concerns about economic growth in China, which has for decades been the top demand engine, and ampler supplies of key commodities including corn and nickel. That has weighed on investor sentiment even as conflicts in Europe and the Middle East and this year’s rally in US stock prices have limited the price downside. The move was exacerbated by an algorithmic selloff in the oil market. - Bloomberg

Speaking of oil, net positioning in energy commodities is even worse. Money managers haven't been this net short in decades!

X (@Josh_Young_1)

This happens despite major secular growth drivers, like rapidly slowing production growth in the U.S. shale industry, consistent long-term demand growth, and the (related) realization that the energy transition isn't going as smoothly as initially expected.

I discussed the biggest bullish drivers in a recent article on Canadian Natural Resources (CNQ), Canada's largest oil producer.

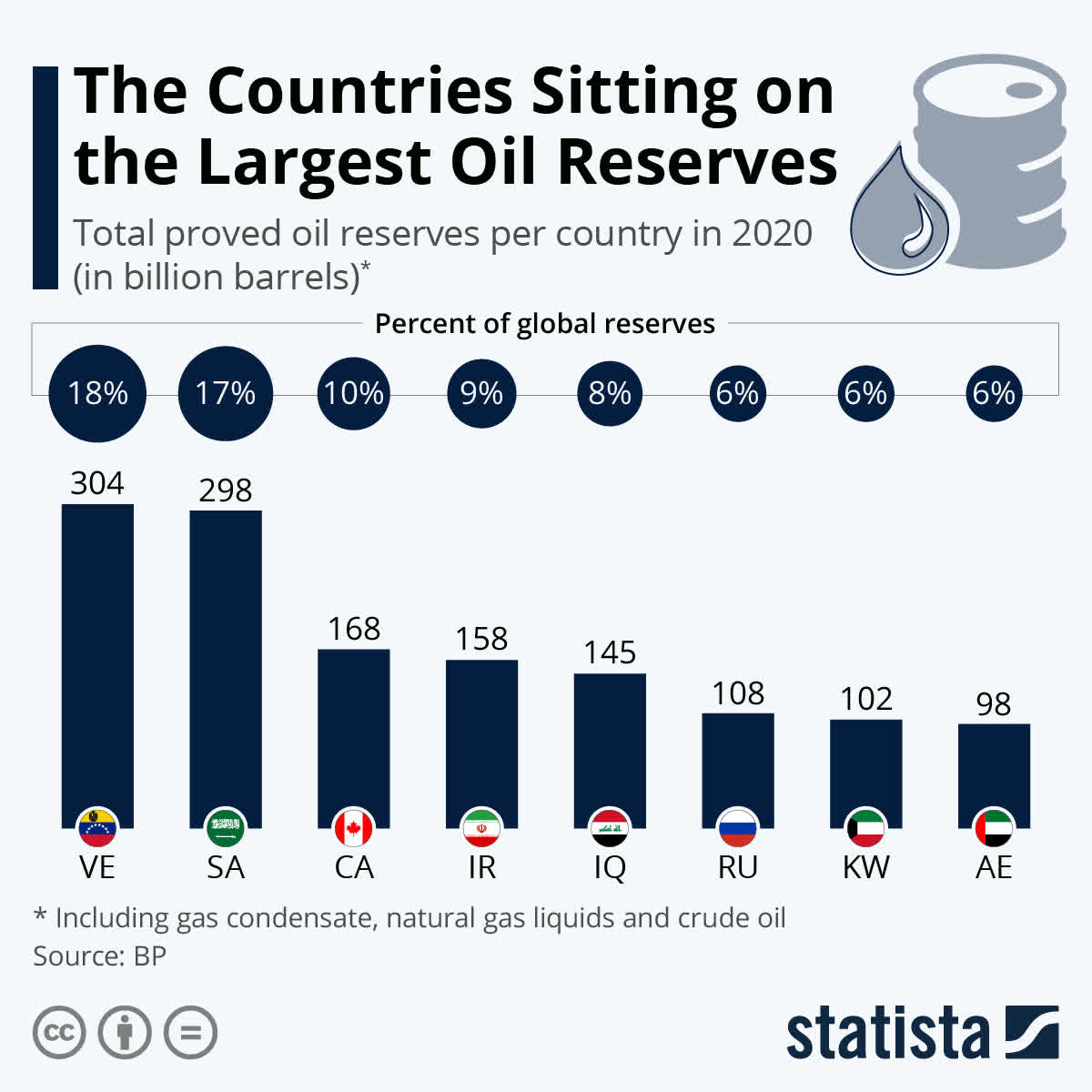

The short version is that production growth headwinds in the United States have shifted pricing power back to OPEC and made Canada, with its massive oil and gas reserves, a more important player in the global energy sector.

In 2020, it was estimated that Canada was home to 10% of the global oil reserves, more than Iran, Iraq, Russia, and other major oil producers.

Statista

Hence, as the market has turned its back on energy (again), I continue to look for attractive investments. In addition to my investment in Canadian Natural, I like Cenovus Energy (NYSE:CVE), a company I called a "Cash Flow Gusher" in my most recent article, written on May 12.

Since then, shares have declined by 13% due to a new wave of economic growth fears that have - as we just discussed - caused the market to avoid cyclical stocks again.

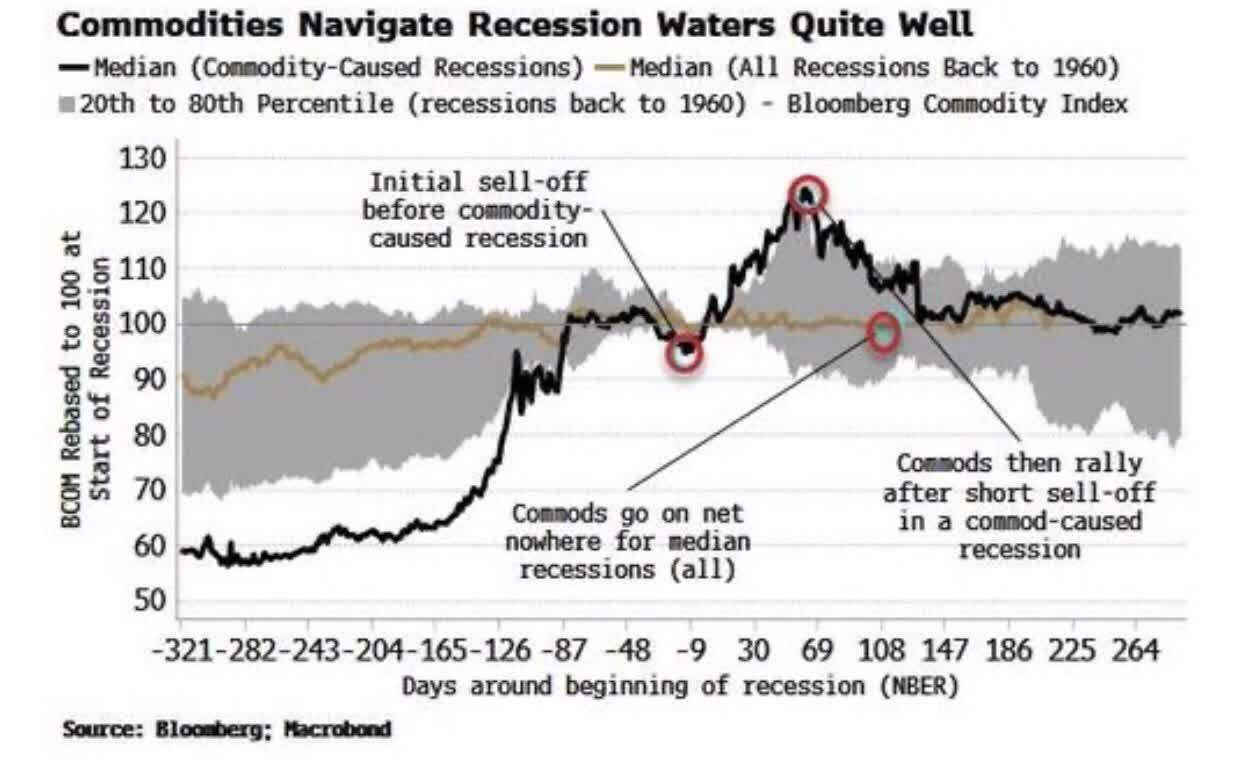

The good news is that historically speaking, commodities tend to rise through recessions, only selling off in the early phases of a recession. While this does not mean they are protectors against recession (oil is still cyclical), when underlying fundamentals are strong, sell-offs in commodities tend to offer great buying opportunities.

Bloomberg, Macrobond

Hence, in the remainder of this article, I'll update my Cenovus Energy thesis and explain why I continue to believe this Canadian stock is a great, undervalued energy play.

So, let's get to it!

There's Deep Value In Cenovus

In the past, I never cared much for Cenovus. Like Exxon Mobil (XOM), the company is an integrated oil and gas company with refinery assets to turn oil into value-added products.

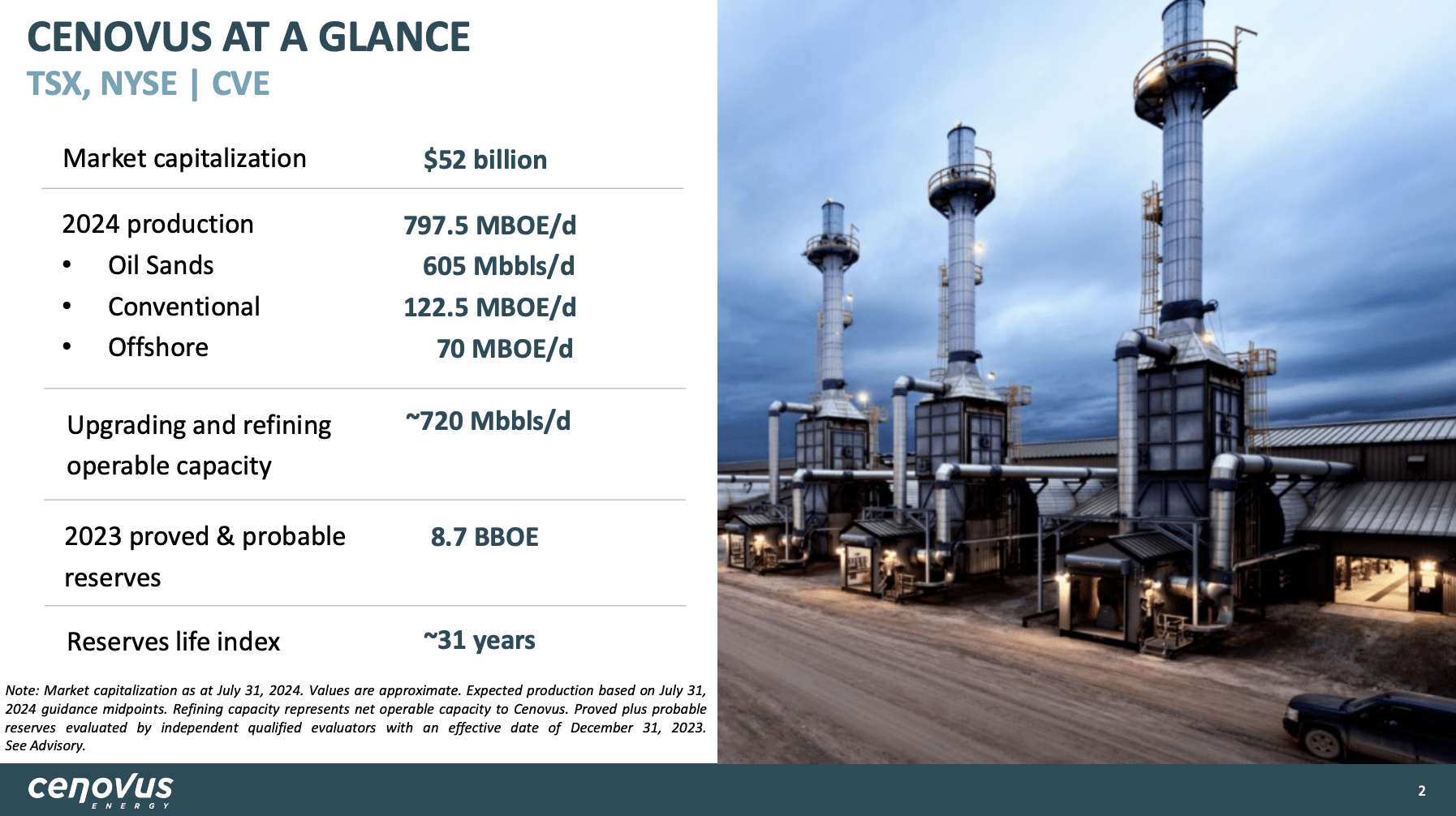

This year, the company is expected to produce close to 800 thousand barrels of oil equivalent, most of it in Canada's oil sands, which have zero decline rates and low breakeven prices. They are bad for the environment, but great places to be for investors when a lot of shale producers in the U.S. struggle to maintain Tier 1 reserves.

These assets have a reserve life of more than 30 years (excluding any new discoveries), which is a fantastic number. The total refining capacity is 720 thousand barrels per day.

Cenovus Energy

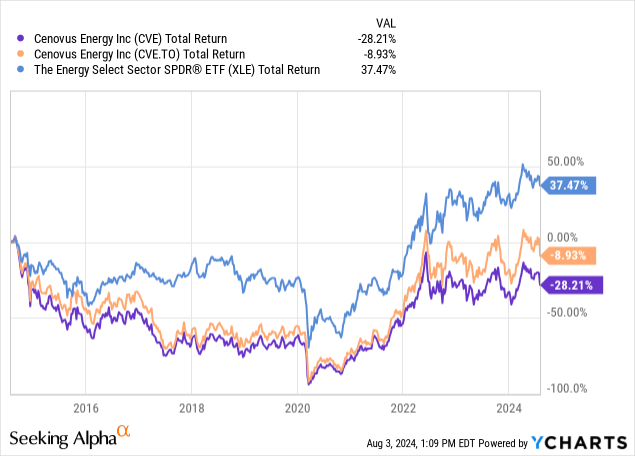

The company also has an abysmal performance. Over the past ten years, Toronto-listed CVE shares have returned negative 9%. The Energy Select Sector ETF (XLE) has returned 37%, which isn't great, either.

New York-listed CVE shares have returned a negative 28%, as the U.S. dollar/Canadian dollar currency pair was a headwind for non-Canadian investors over the past decade.

Data by YCharts

Data by YCharts

Hence, I picked Canadian Natural. That company has no refining assets (I wanted to buy a pure-play upstream company), a much better track record, and a balance sheet that allows it to return 100% of its free cash flow to shareholders.

The reason I'm bringing this up is because CVE has one huge benefit that CNQ does not have: recovery potential.

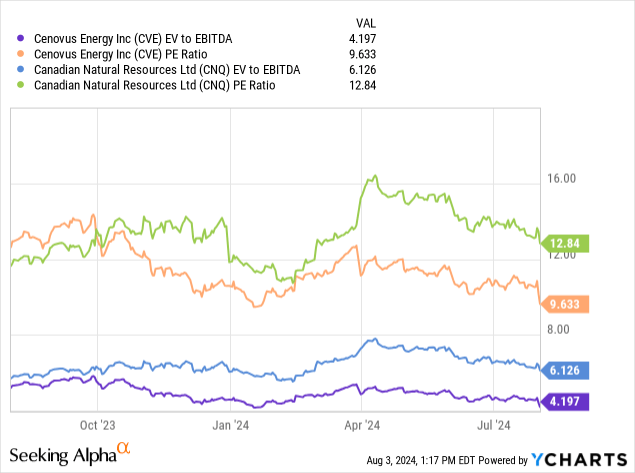

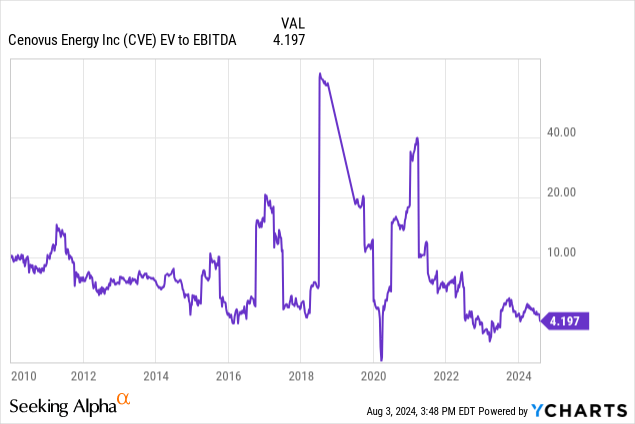

Cenovus trades at 4.2x earnings and 9.6x EBITDA. Canadian Natural trades at 6.1x earnings and 12.8x EBITDA.

Data by YCharts

Data by YCharts

If Cenovus is able to show investors it is able to reduce debt, run an efficient integrated oil and gas business, and return cash to shareholders, it could have a lot of capital gain potential - on top of its 3% dividend.

That's what the bull case is based on.

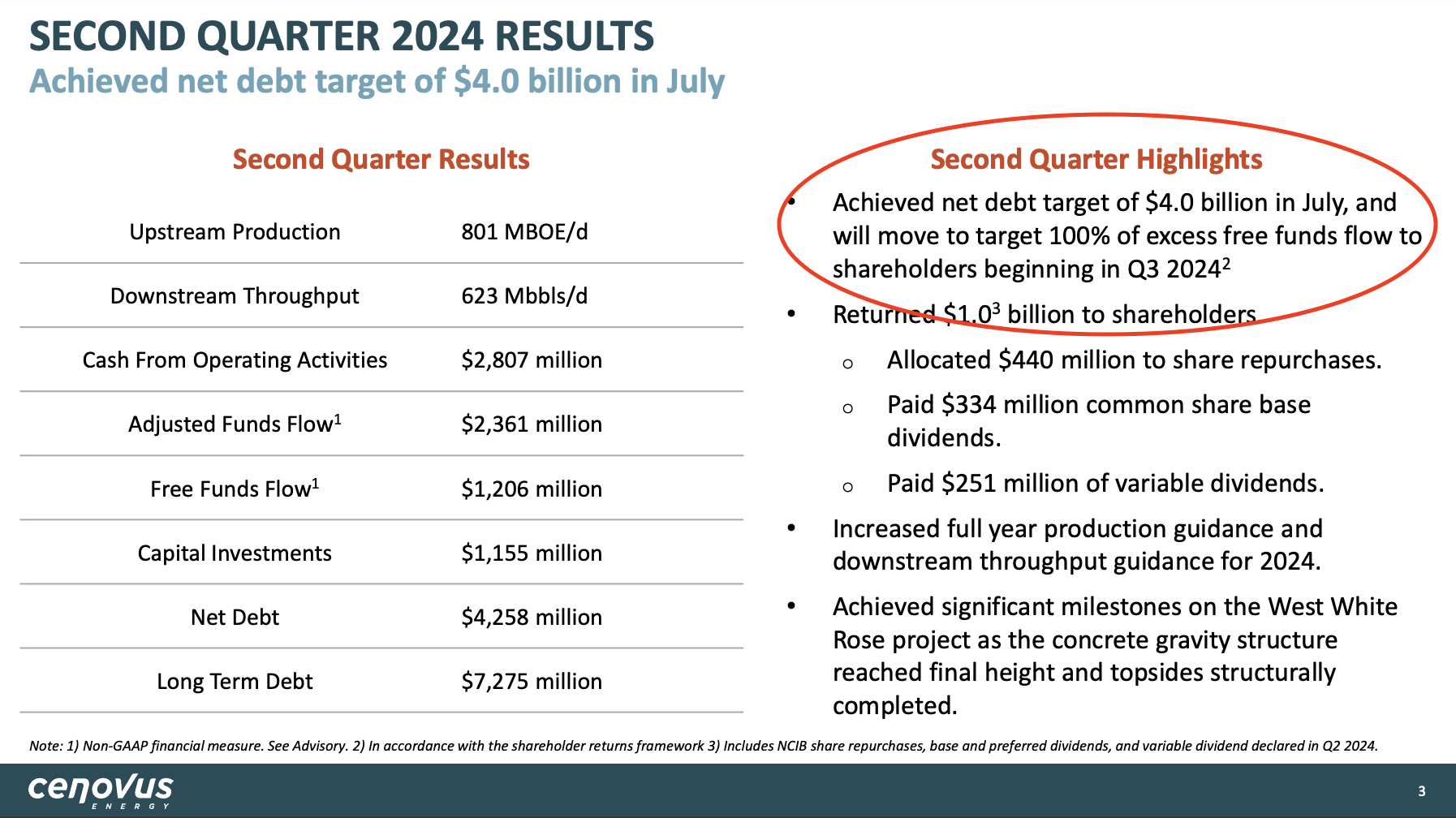

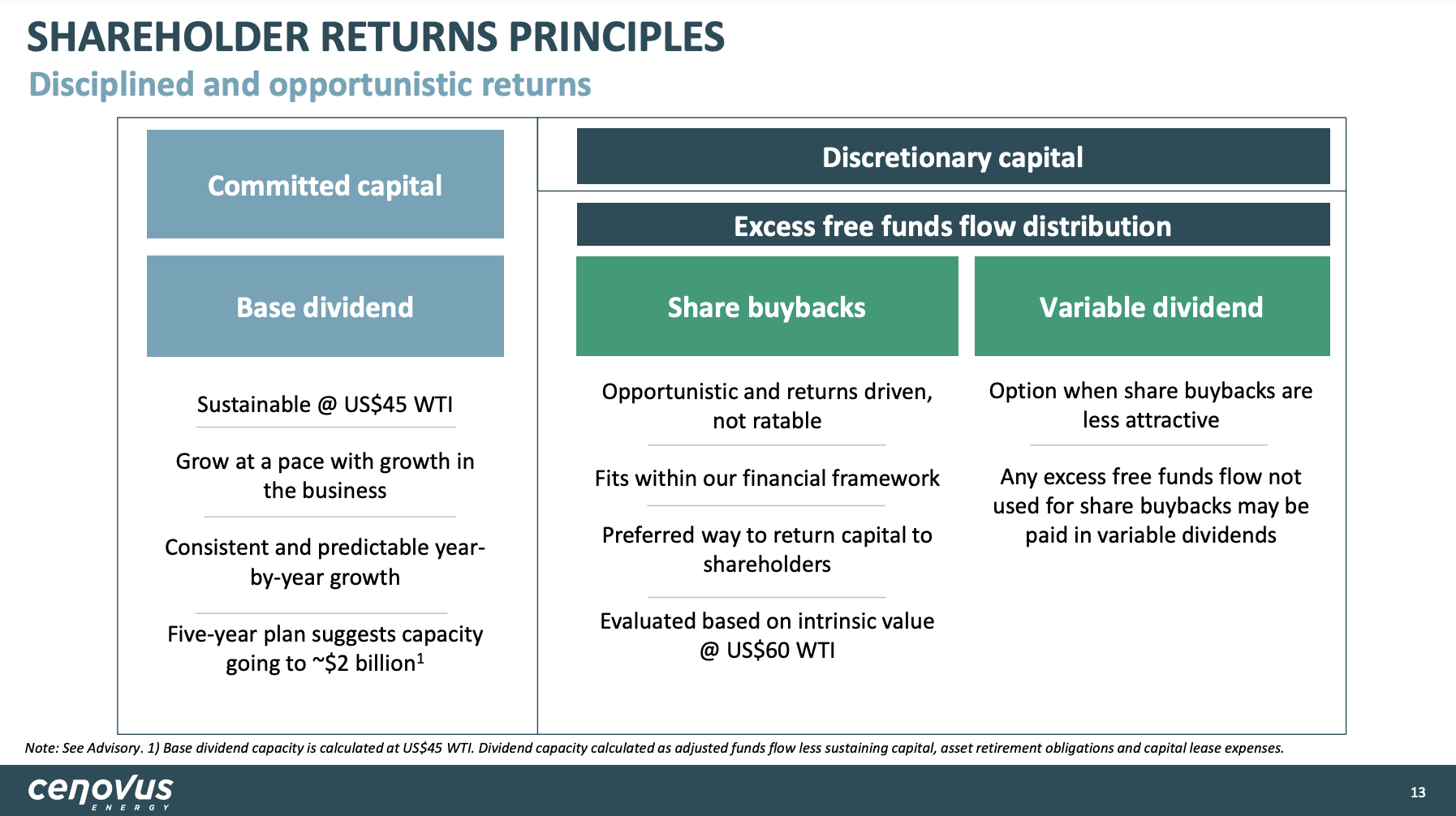

Having said all of this, like its bigger "brother" Canadian Natural, Cenovus Energy has hit its ($4 billion) debt target, which will allow it to return 100% of its free cash flow to shareholders, starting in the third quarter of this year.

I highlighted this in the overview below.

Cenovus Energy

In the second quarter, the company distributed more than $1 billion to shareholders. This translates to 2.2% of its market cap, which is a lot for a single quarter.

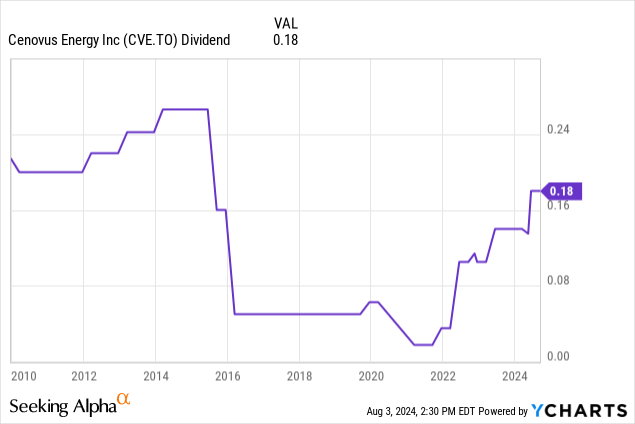

Currently, the company pays $0.18 per share per quarter. This is its fixed quarterly dividend. It hiked the dividend by 28.6% on May 1.

Data by YCharts

Data by YCharts

This dividend translates to a base yield of 2.9%. It also paid a variable dividend of $0.135 (0.5%).

Now, the question that's probably on your mind is how the company plans to distribute its free cash flow in the future.

You're not the only one, as this is what Manav Gupta from UBS asked during the 2Q24 earnings call (emphasis added):

[Question] Just trying to understand a preference between buyback and variable dividend. Should we continue to see a combination of those? Or you have a very strong preference for one of those? Definitely, buybacks were variable, but if you could talk about that.

[Answer] So you're going to continue to see us ratably, predictably grow the base dividend over time. We've typically done that kind of in that April, May time frame. Obviously, driven by the Board discretion. But as the business grows, you're going to continue to see us target, let's say, double-digit growth in the base dividend over time.

That's the first thing. I think the second is, as I said, given where the share price is today and what we see is value and intrinsic value and the return on acquiring our shares back, we see that as an attractive value proposition. So the variable dividend we paid in May was more a function of we underallocated our shareholder returns in the first quarter.

And so that's not a reflection, I would say, the value that we see in the buyback. So going forward, to the extent that you continue to see an attractive share price, which we do, you should expect most, if not all, of our return -- excess returns will be done in the form of share repurchases.

In other words, the company will likely maintain double-digit annual growth in its base dividend. It will also prioritize buybacks over special dividends due to the attractive intrinsic value of its business.

Cenovus Energy

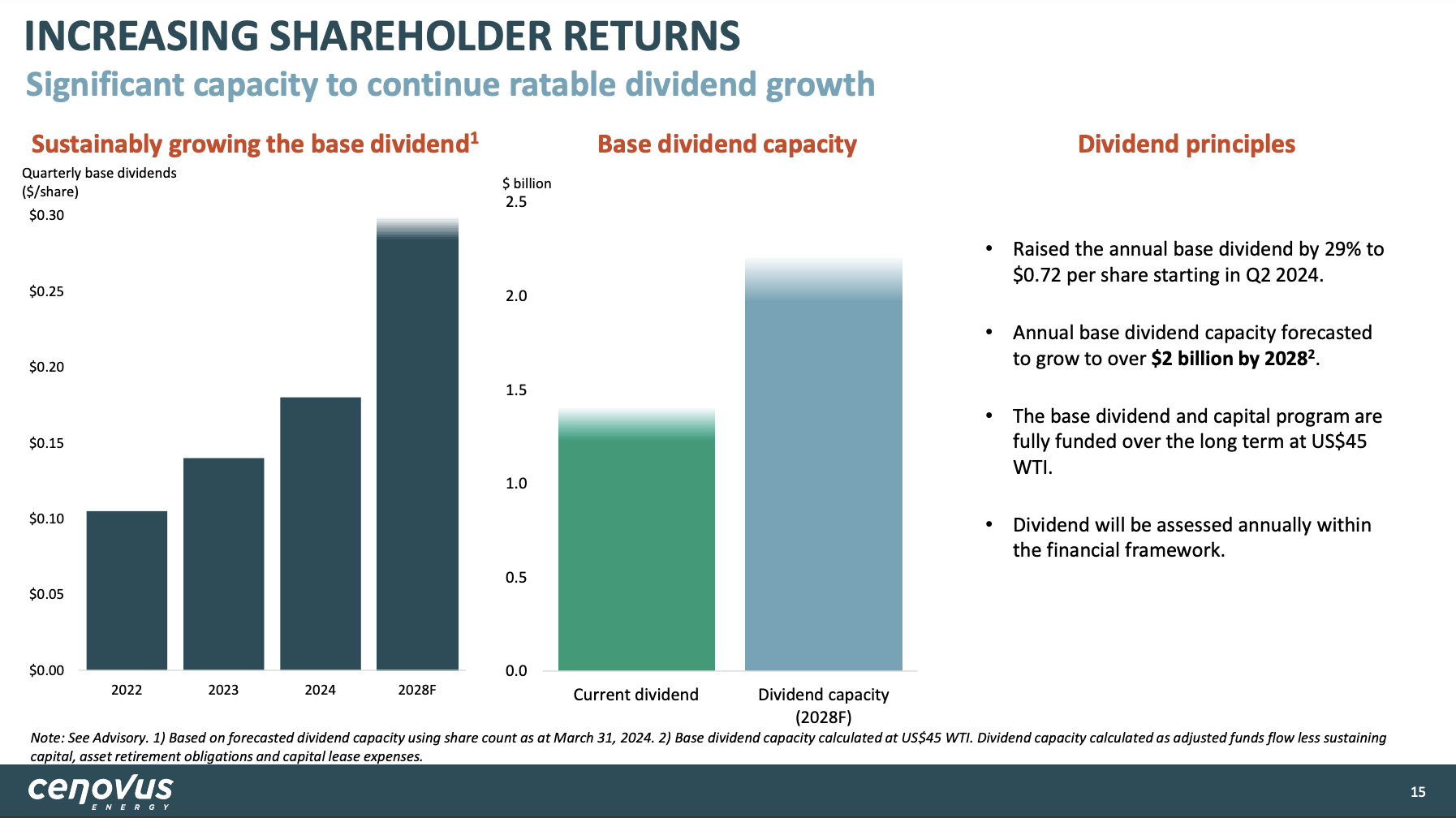

Moreover, the company has made clear that it aims to grow the base dividend to more than $2 billion by 2028, which could indicate a $0.30 per share base dividend. That would be a 4.8% yield on cost (current stock price).

Cenovus Energy

The base dividend is expected to be protected at US$45 WTI, which is a great number and a result of its efficient operations.

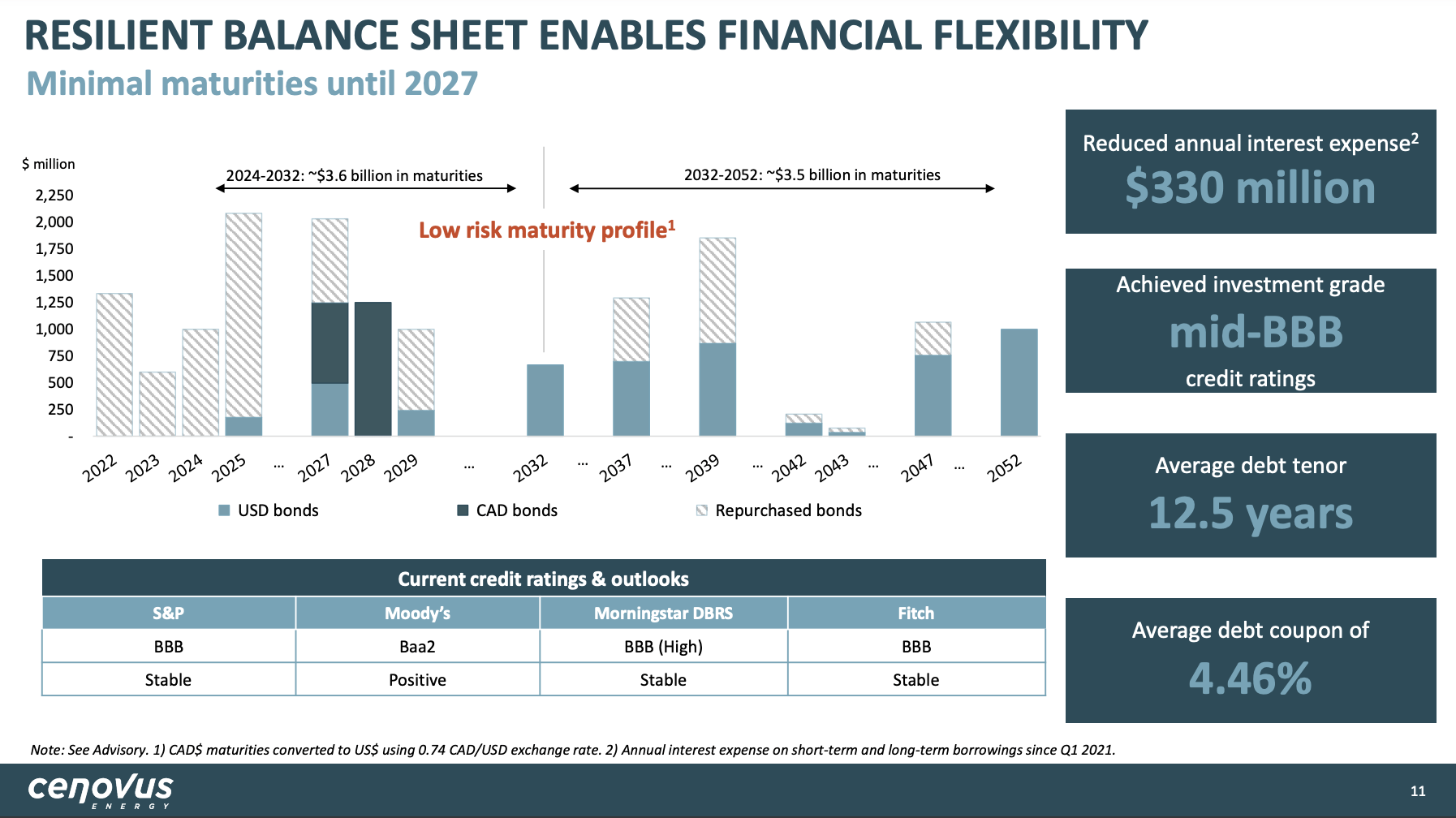

Speaking of low risks, the company has also de-risked its balance sheet. On top of hitting its debt target, it has repurchased most bonds that mature through 2026, resulting in a highly favorable maturity profile with a weighted average duration to maturity of 12.5 years.

It has reduced annual interest expenses by $330 million since 2021 and achieved an investment-grade BBB (or equivalent) credit rating from all major rating agencies.

Cenovus Energy

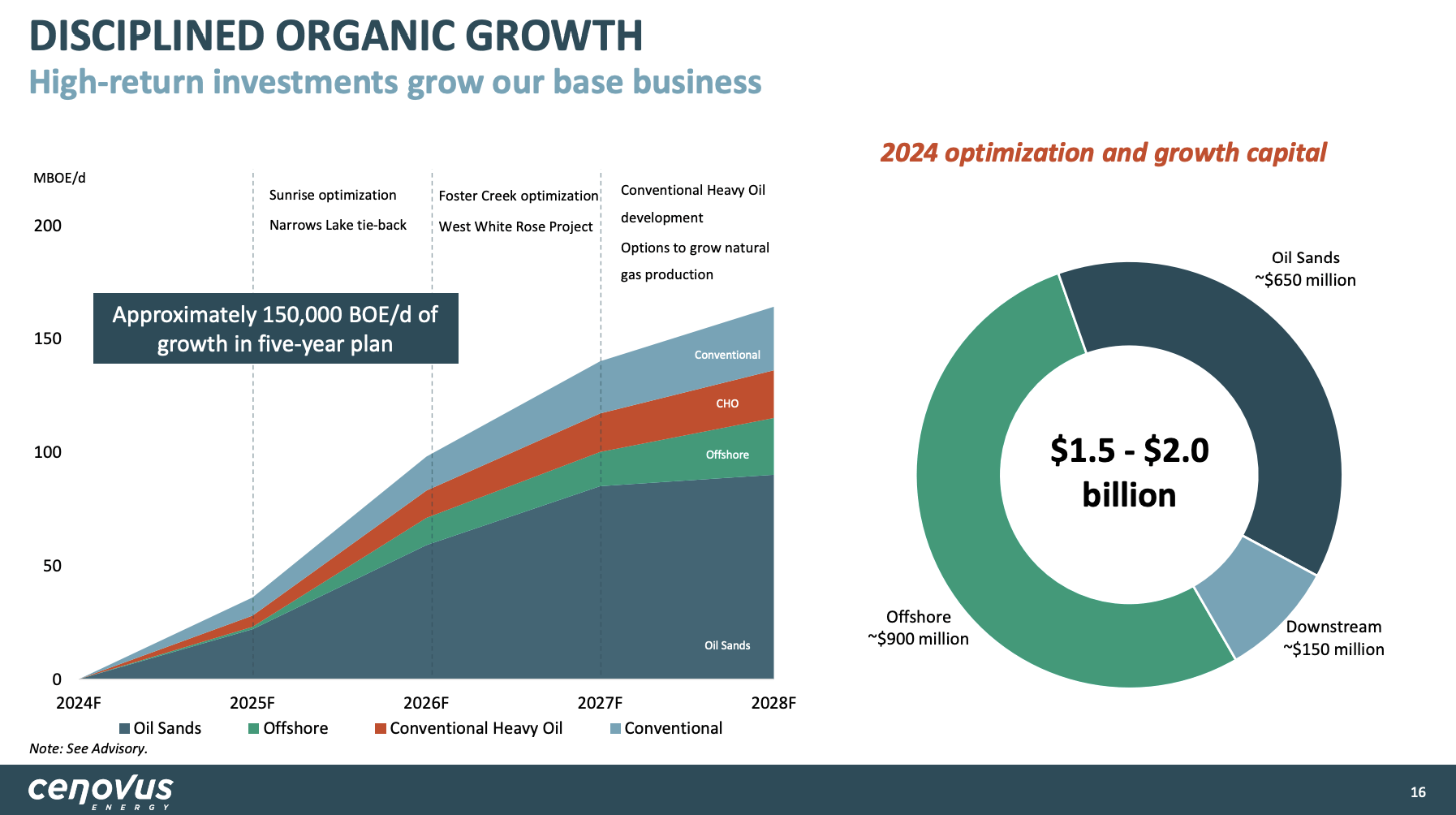

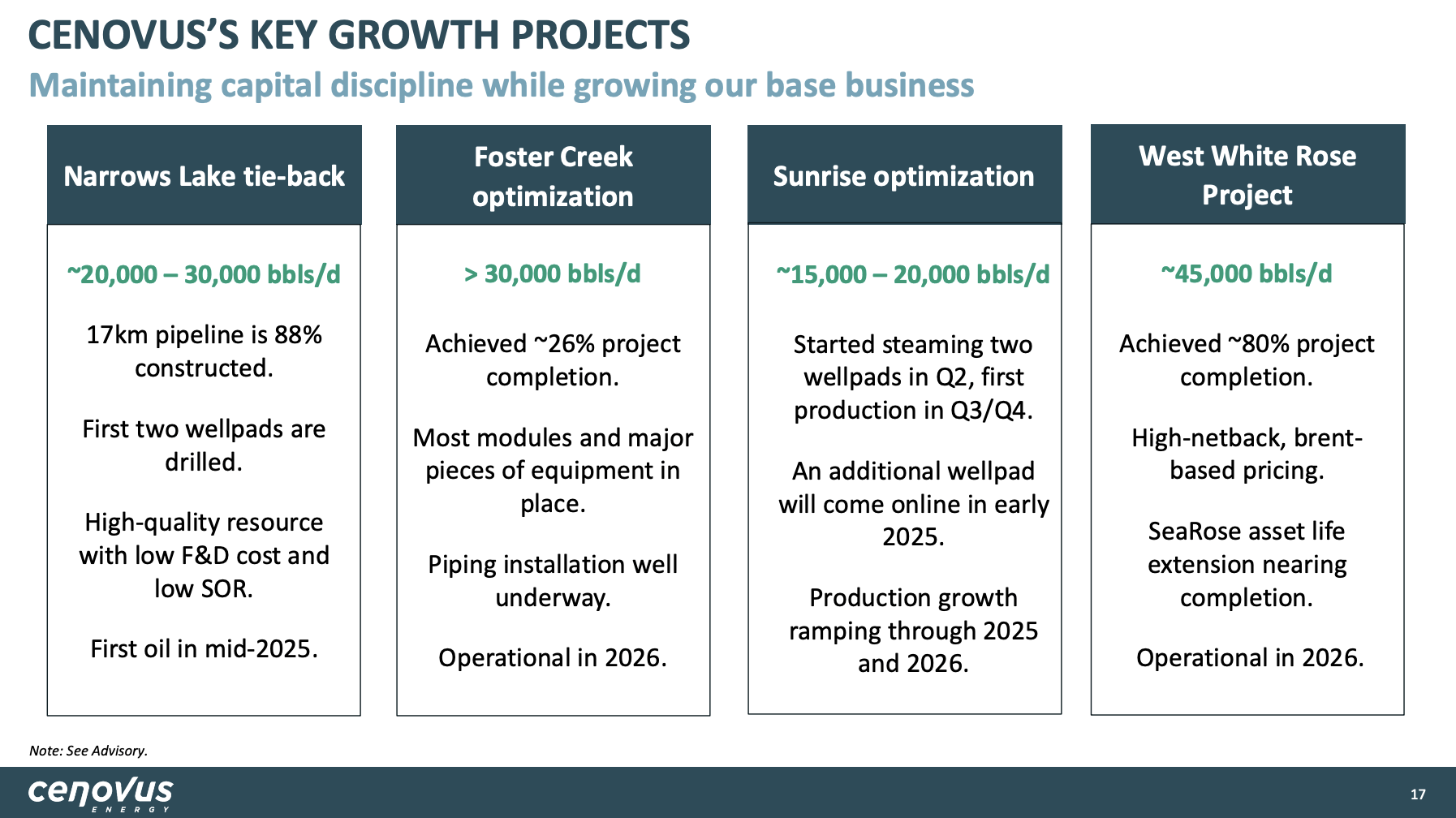

With that in mind, other tailwinds are production growth.

As projects like the Foster Creek optimization are going according to plan (expected to be online in 2016), the company is looking to add more than 150 thousand barrels per day in production by 2028, mainly supported by its oil sand operations.

Cenovus Energy

Meanwhile, in its offshore operations, Cenovus has made significant progress as well, with the West White Rose project reaching 80% completion and on track for the first oil output in 2026.

The SeaRose FPSO, which is undergoing regulatory maintenance, is expected to resume production in the fourth quarter of this year, further supporting the company's offshore production capacity.

Here's a full overview of the company's current growth projects:

Cenovus Energy

So, what about its valuation?

Valuation

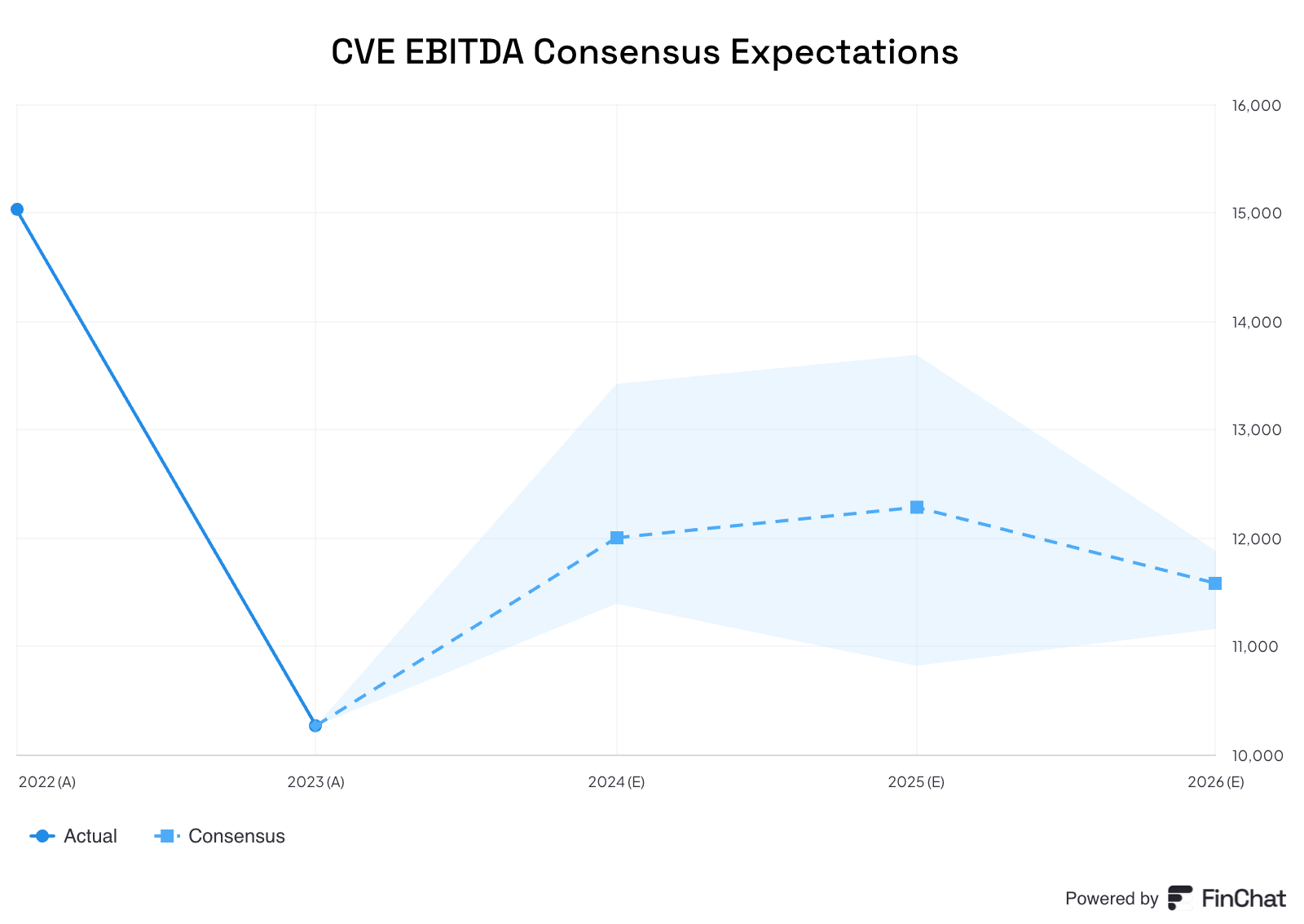

Valuation-wise, the company is expected to generate $12.3 billion in EBITDA by 2025. I believe that's a very conservative estimate based on current market conditions.

FinChat

Even if we apply a subdued multiple of 6x to that number, we get an expected market cap of roughly $70 billion (assuming $4 billion in net debt). That's more than 50% above the current number.

Data by YCharts

Data by YCharts

If we incorporate a rebound in oil prices, aggressive buybacks, and production growth, I believe CVE has room to double in the 2-3 years ahead.

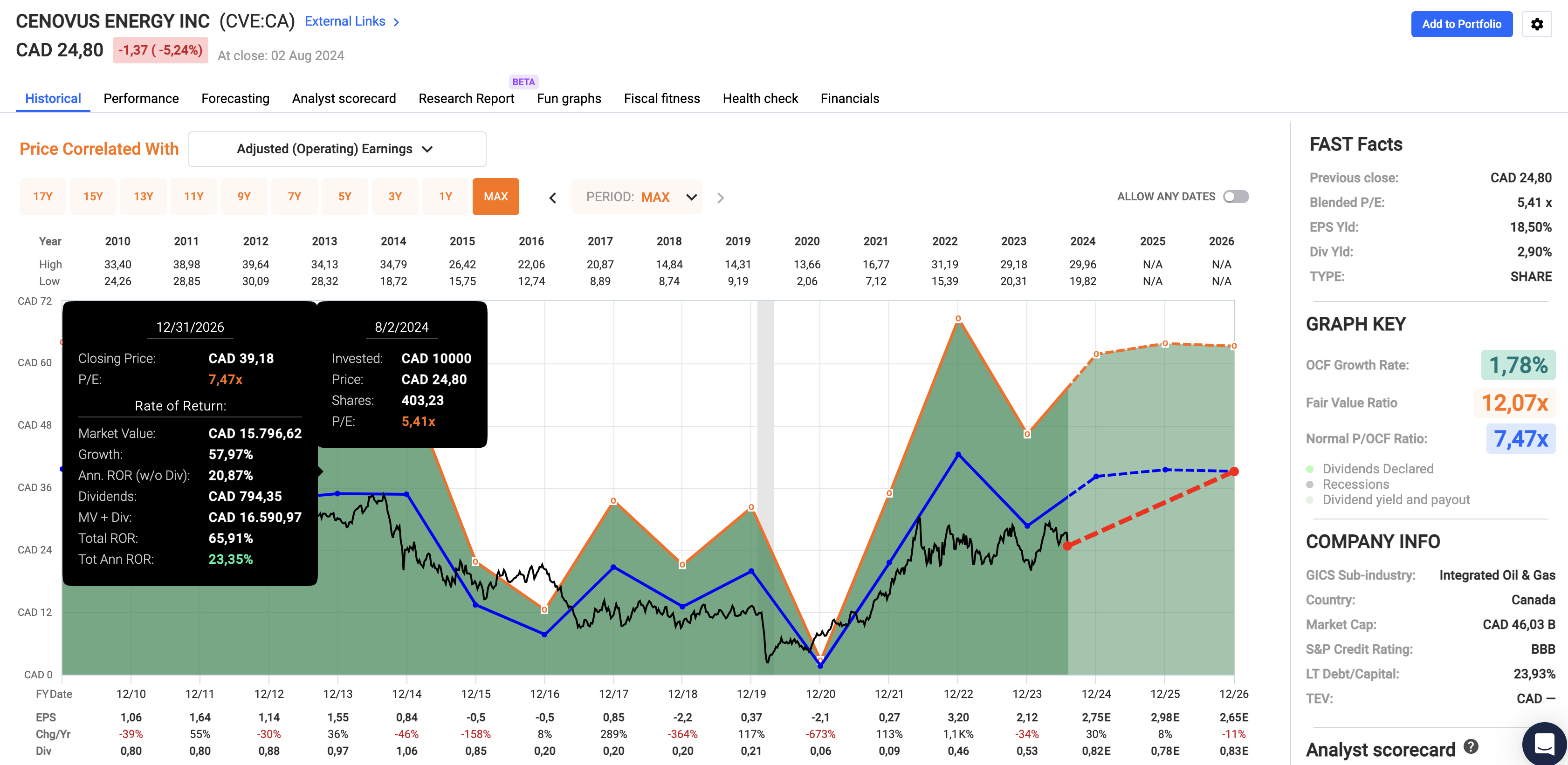

Moreover, I arrive at the same conclusion when using the company's operating cash flow. By 2026, per-share operating cash flow is expected to be $2.65. Applying a conservative 7.5x multiple gives the stock a fair price target of $39, 57% above the current price.

Fast Graphs

As such, I maintain a Strong Buy rating.

Takeaway

Despite the current bearish sentiment in the commodities market, I see significant potential in Cenovus Energy.

The company's solid asset base, strong dividend growth outlook, and strategic focus on buybacks position it well for a recovery. This includes its 100% free cash flow return commitment.

With its long reserve life and subdued breakeven costs, in addition to improving financials and planned production growth, I believe Cenovus is undervalued and offers a compelling investment opportunity.

Hence, I maintain a Strong Buy rating, expecting a substantial upside once the market turns to commodities again.

Pros & Cons

Pros:

- Strong Asset Base: CVE has deep reserves with long life and low decline rates, providing stability and reliable cash flow potential.

- 100% Free Cash Flow Commitment: The company is committed to returning 100% of its free cash flow to shareholders, which is a significant advantage for income-focused investors.

- High Dividend Yield: CVE offers a consistent and attractive dividend yield, supported by a strong balance sheet.

- Favorable Market Position: With U.S. shale growth slowing, CVE benefits from Canada's rising importance in the global energy market.

Cons:

- Environmental Concerns: The company's operations in Canada's oil sands raise environmental concerns, which could come with additional political risks.

- Dependency on Oil Prices: CVE's financial performance is closely tied to the price of oil, making it vulnerable to fluctuations in commodity markets.

- Withholding taxes: non-Canadian investors need to be aware of the additional tax complexities that may come with investing in Canadian stocks.

Comments