Summary

- Hemingway’s quote on bankruptcy reflects stock market risk: it builds gradually, then hits suddenly. Recent market volatility caught many by surprise, highlighting this pattern.

- Corrections are normal, occurring regularly. They offer opportunities to buy quality stocks at better prices. My "win-win" strategy benefits from both market rises and dips.

- I recommend careful stock selection, focusing on strong fundamentals. Avoid high-risk stocks and invest in companies with proven performance for a resilient portfolio.

Olena Yefremkina/iStock via Getty Images

(A Very Lengthy) Introduction

How did you go bankrupt?” Bill asked.

Two ways,” Mike said. “Gradually and then suddenly.”

The quote above is from the book "The Sun Also Rises," written by Ernest Hemingway in 1926.

I have to say, I think about this quote a lot, especially because there are many sayings that seem to be loosely based on what Hemingway wrote almost 100 years ago.

A similar saying often used on the stock market is "Risk Happens Slowly, Then All At Once."

Technically speaking, it's not entirely correct. After all, the "risk" of something happening is always present. When I eat spaghetti with a white t-shirt, the risk of getting a visible stain is always present. The risk does not rise the moment I get an actual stain.

The reason I'm bringing all of this up is because risk is often underestimated in the stock market. When stocks go up, it's smooth sailing, and people feel it's easy to make money.

That's usually when the fun abruptly ends.

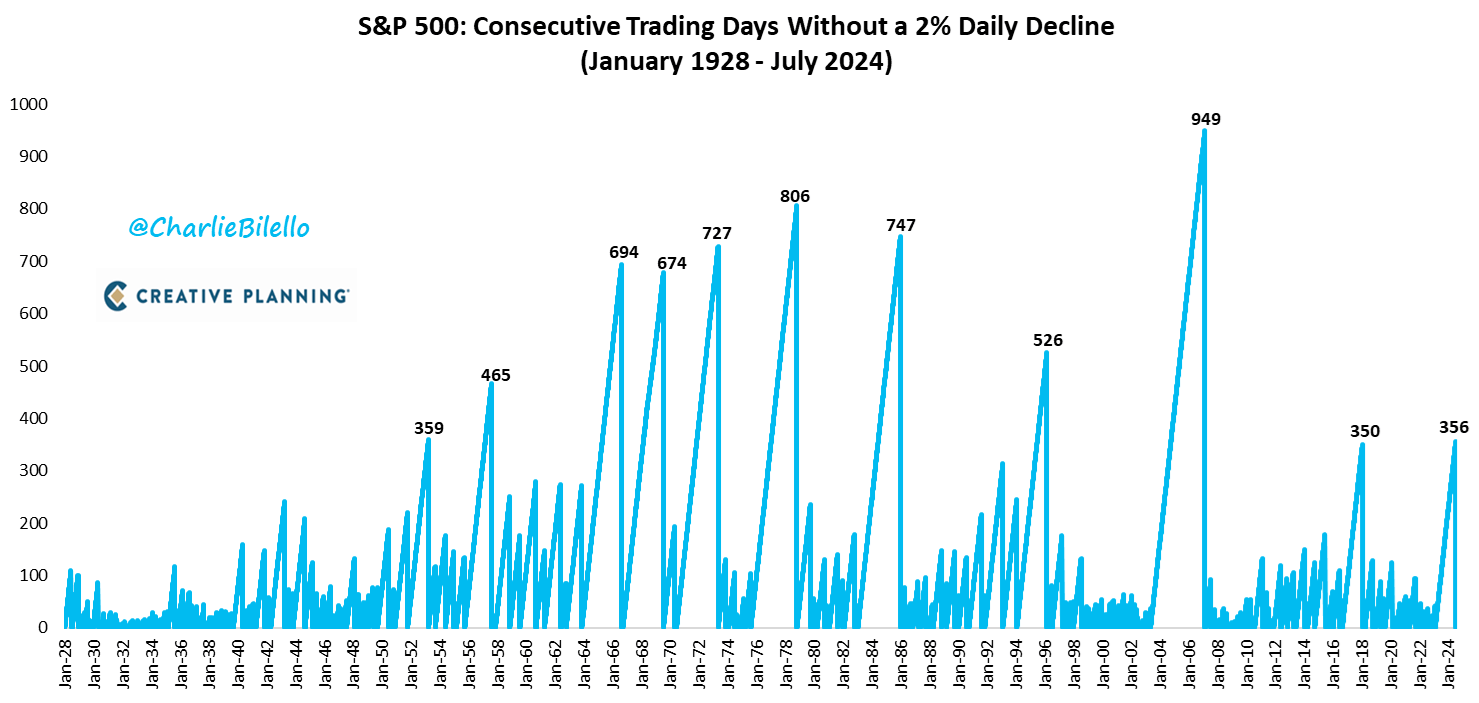

As we can see below, the stock market just had the longest streak without a 2% daily decline since the Great Financial Crisis. To be exact, it took 356 trading days before the market saw a 2% daily decline.

Before the Great Financial Crisis, that number was 949, which is truly mind-blowing. The calm before the storm was clearly something back then.

Creative Planning

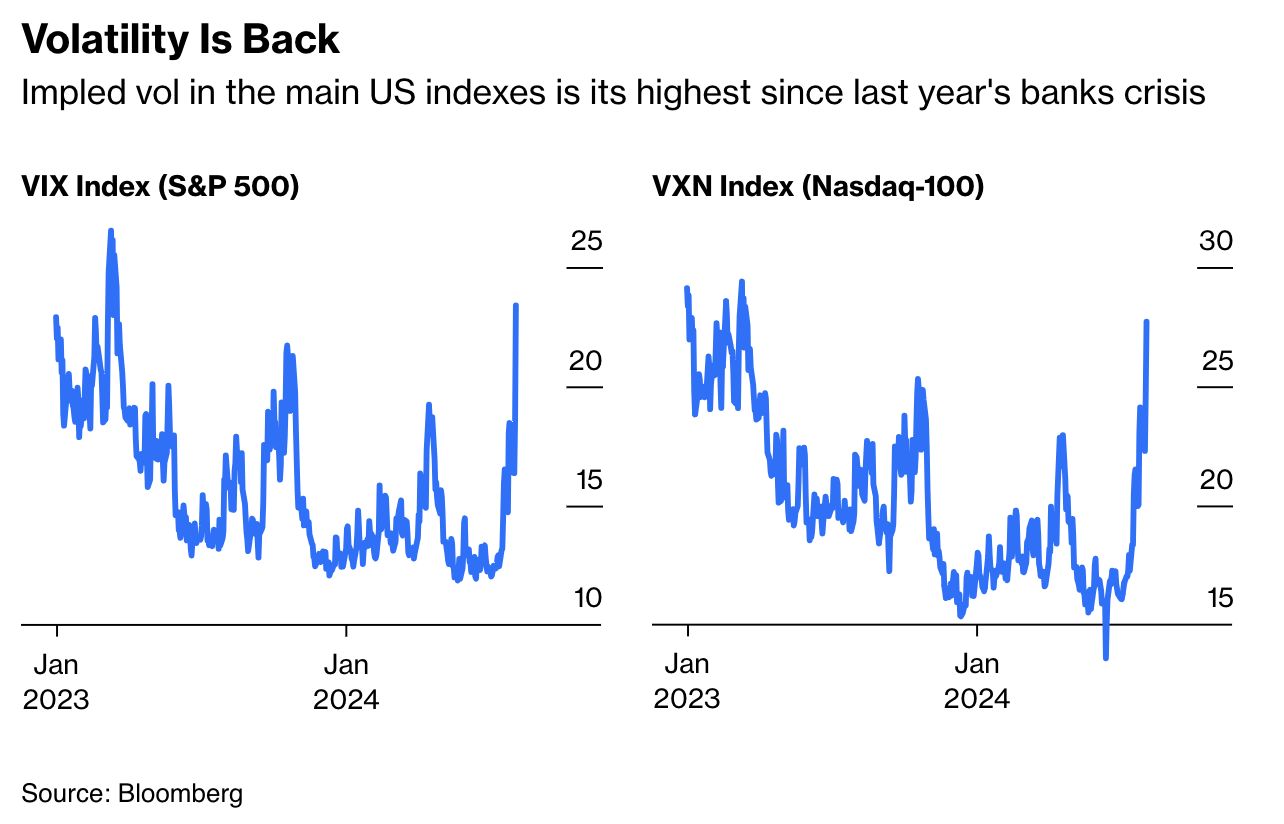

Earlier this week, volatility exploded when most did not expect it. This includes me. While I have been warning for a while that the S&P 500 valuation had become lofty and a rotation is likely, I did not expect volatility to rise so suddenly.

In general, most sell-offs come when it's least expected. That's what creates panic selling.

As we can see below, volatility exploded, impacting the Nasdaq-100 even more than the S&P 500.

Bloomberg

There are a few reasons why the stock market tanked.

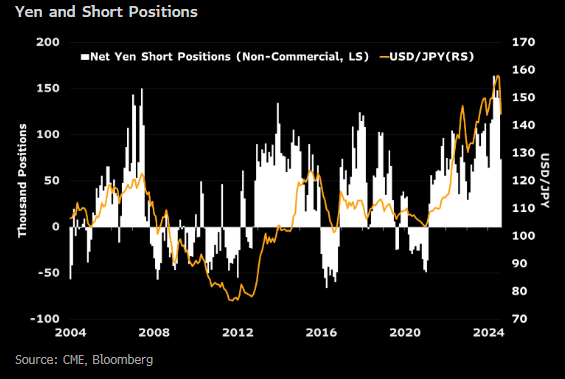

- The Japanese yen carry trade unwound. The market had used cheap rates in Japan, supported by a dovish Bank of Japan, to put money into riskier assets, including tech stocks in the United States. When this trade became crowded, it started to unwind very quickly, forcing people to close their positions.

Bloomberg

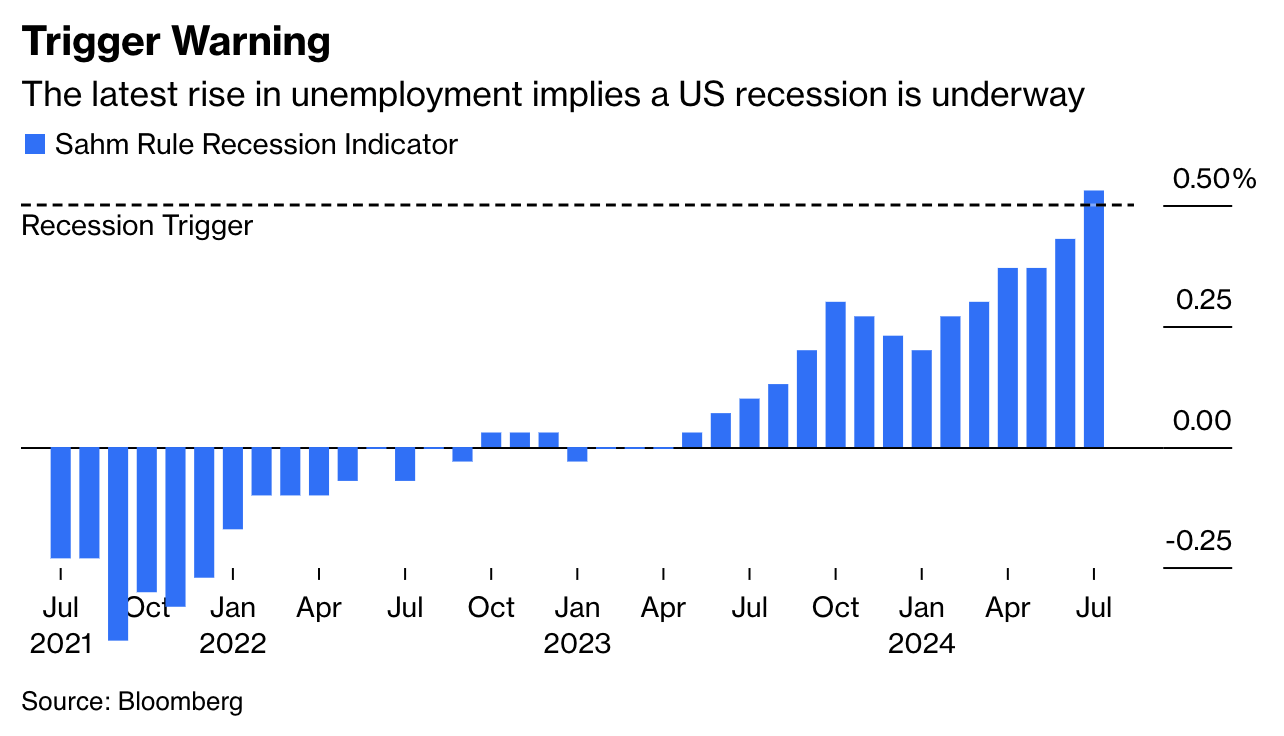

- Economic growth is weakening. Last week's labor market numbers have triggered the "Sahm Rule," which says that once the unemployment rate rises by 0.5 points from its 12-month low, a recession is likely. This is mainly based on even slight increases in unemployment having the ability to slow down the economy.

Bloomberg

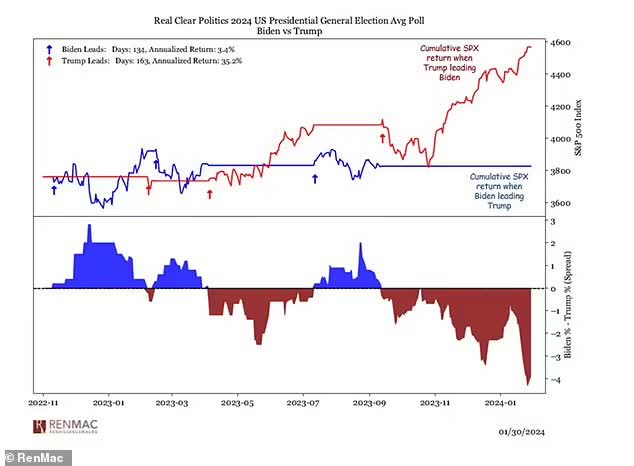

- The Harris factor could be another driver. While I won't turn this into a political article, some market participants have made the case that the surge of Harris in the polls is a bit bearish. I have to say, it took me a while, but I found some evidence that supports this. The (low-quality) chart below is from February 2024. It shows that in times when Trump was leading in the polls (versus Biden), the market did much better.

Renaissance Macro Research

Personally, I believe it's the mix of all the factors above. The market had gotten crowded, supported by a cheap Japanese yen. On top of that, economic growth is not in a good spot, and geopolitical pressure is rising. This includes the situation in the Middle East.

With that said, I did not lose a second of sleep this week. In fact, I wasn't even worried one bit - and that's not because the market quickly rebounded.

In all honesty, I believe the media and many market participants completely overreacted. Even European newspapers reported on the 2.5% decline in the S&P 500 as if it were a world-changing development.

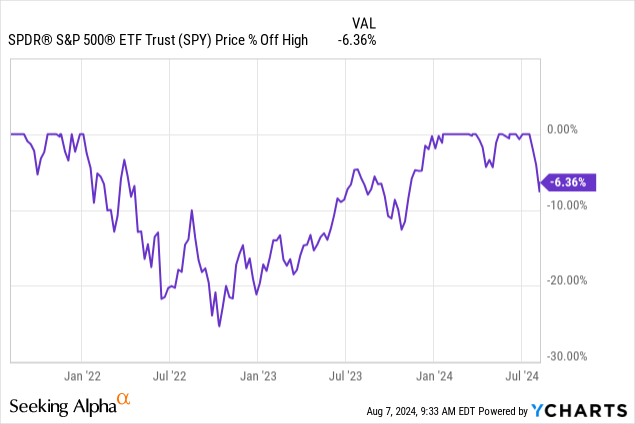

As we can see below, the market did not even drop 10%. Or, to put it differently, we did not even enter a correction.

Data by YCharts

Data by YCharts

Does this mean we're out of the woods?

No, it does not mean we're out of the woods at all. And to be honest, that's OK.

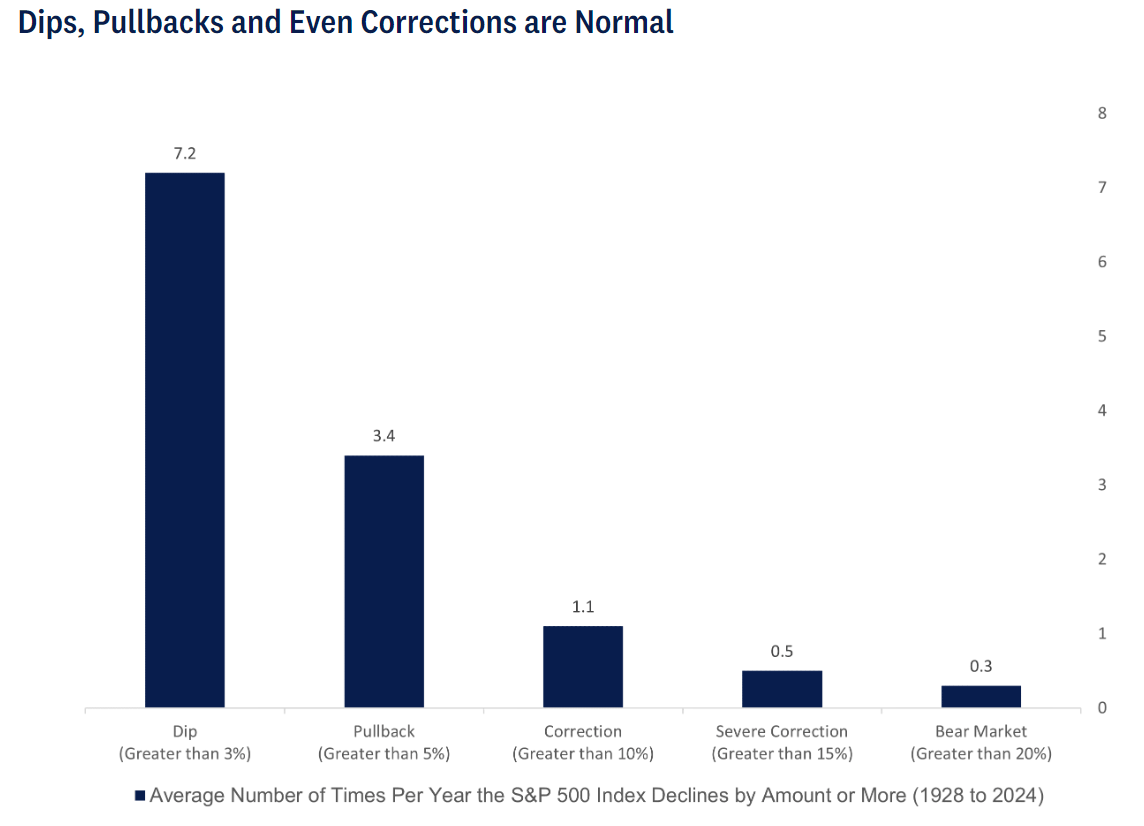

Corrections are very normal.

- On average, the market drops at least 10% every single year.

- The average year sees more than three pullbacks of more than 5% and seven pullbacks of more than 3%.

- Every two years, a 15% correction happens. Again, on average.

- The average year sees 0.3 bear markets of more than 20%. This implies we get a bear market every 3.33 years.

LPL Financial

Stocks go down, which is good. After all, who doesn't like buying stocks at a discount?

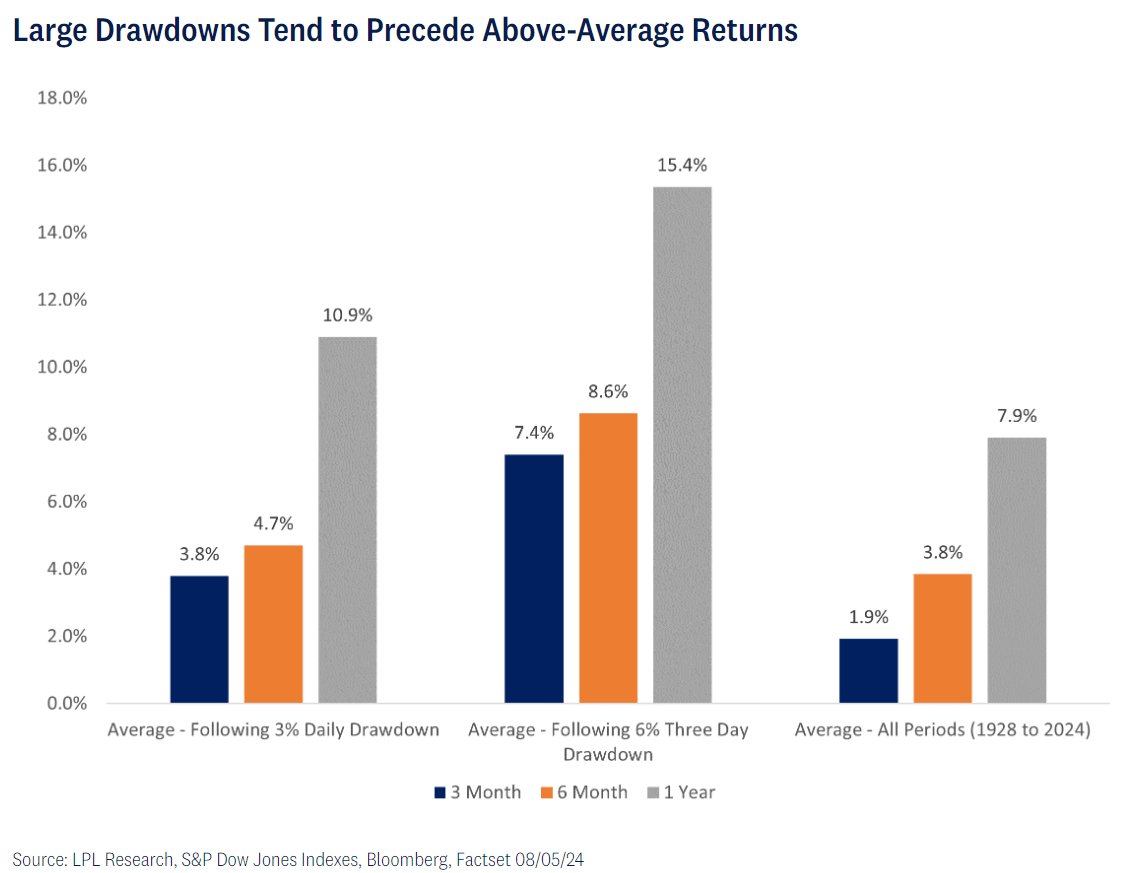

Statistically speaking, "dips" are great buying opportunities. Using the data below, we see the average 6% three-day decline was followed by a 15.4% return over the next 12 months. After three months, stocks had risen by 7.4%.

LPL Financial

As reported by Bloomberg:

We would characterize the recent market pullback as a textbook correction, after months of low volatility so far in 2024,” said Carol Schleif at BMO Family Office. “The lack of volatility before the past few weeks is unusual, and our current correction is actually quite normal, especially during August, which historically is a volatile time for markets given lighter trading volumes and the summer doldrums.”

After having said all of this, I'm not writing this article to push anyone in the market. The main message is that dips happen. We have been through many, and we will see many more.

That's why I have what I like to call a "win-win" strategy. Although it may sound silly, it is actually something, I always have in the back of my head when I research investments.

It's simple.

- When stocks rise, I win. This one is obvious.

- When stocks fall, I am able to buy more of my favorite investments at better prices. I win again.

Unlike investors who rely on index ETFs, this strategy requires careful investment selection. After all, if investors buy the "wrong" stocks, they will continue to add to losing investments, creating an ever-growing financial liability.

That's why I put so much emphasis on a careful stock selection. Although I make mistakes, most of my picks are companies with wide-moat business models, stellar balance sheets, a focus on shareholder distributions, and attractive valuations.

I usually avoid companies with heavy competition, products that may or may not turn into blockbusters, and other investments with unfavorable risk/reward ratios.

Even if I miss some of the high-flying stocks, I believe avoiding the need to participate in every "hype" and investing in proven dividend growth stocks is one of the best ways to build wealth.

Hence, in the second part of this article, I'll present a few stocks that I expect to be fantastic plays for a "win-win" strategy without the constant worry one may be betting on the wrong horse.

Fantastic Sleep-Well-At-Night Stocks

On August 6, Seeking Alpha reported that Bank of America ("BofA") securities had published a list of 42 S&P 500 holdings with low betas to help investors sleep better at night.

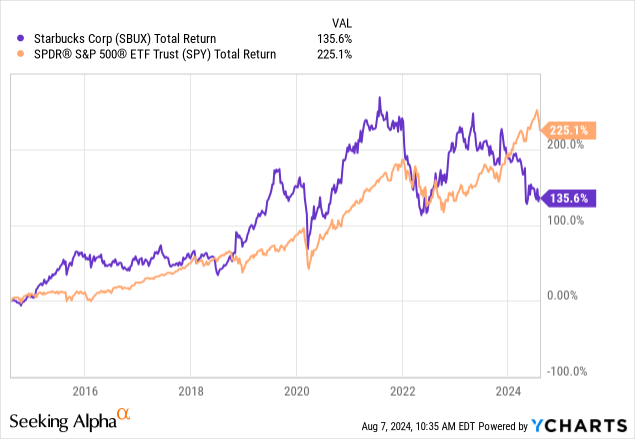

As much as I respect BofA, I don't agree with all of these picks. For example, I would not necessarily put Starbucks (SBUX) on that list, mainly because of its dependence on middle-class consumers in an ever-increasingly competitive environment.

Again, SBUX is NOT a bad company. I just would not put it in the ultimate sleep-well-at-night category. Especially in recent years, it has gotten quite volatile, failing to outperform the S&P 500.

Data by YCharts

Data by YCharts

There are stocks I like a lot.

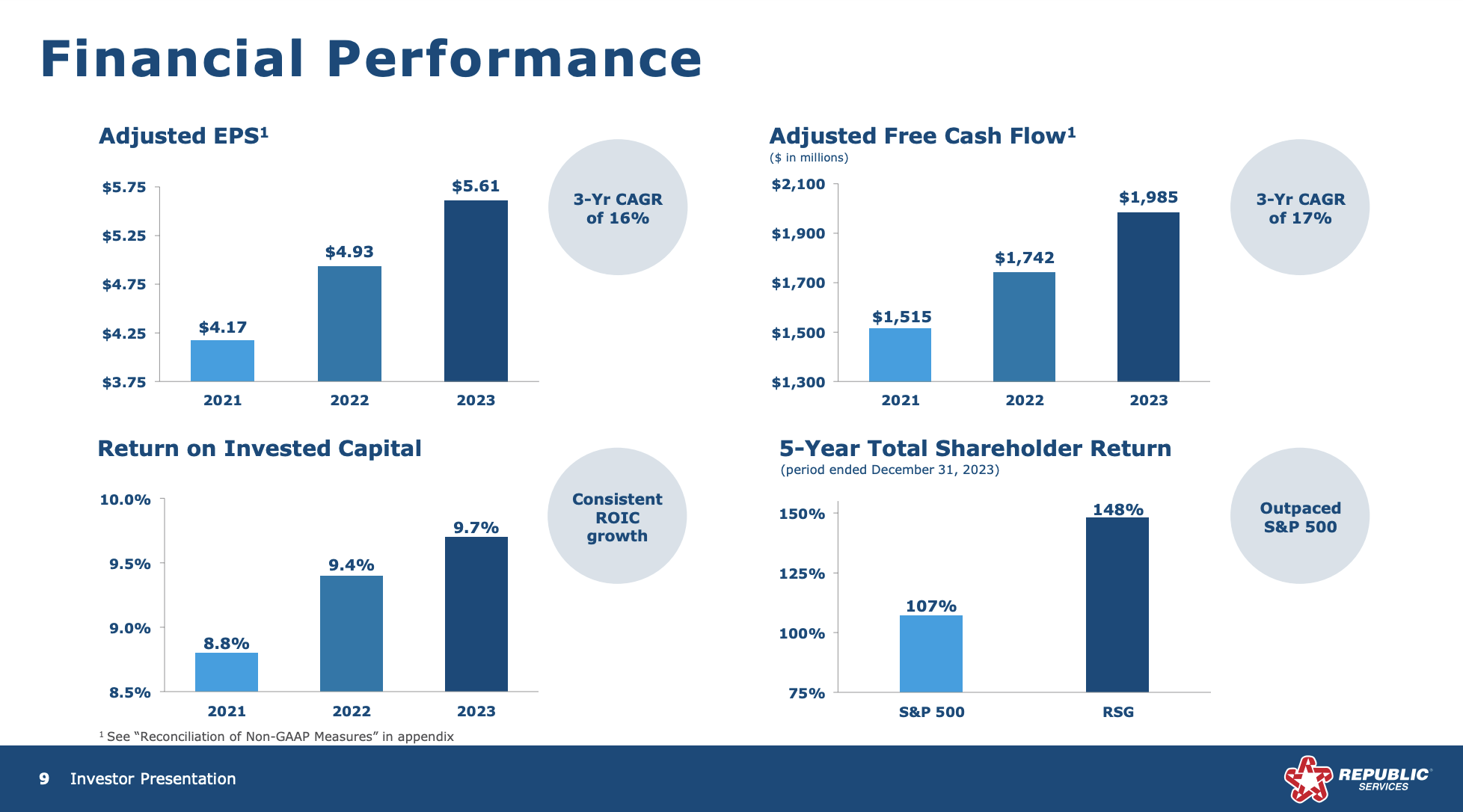

Republic Services (RSG) - Anti-Cyclical Dividend Growth

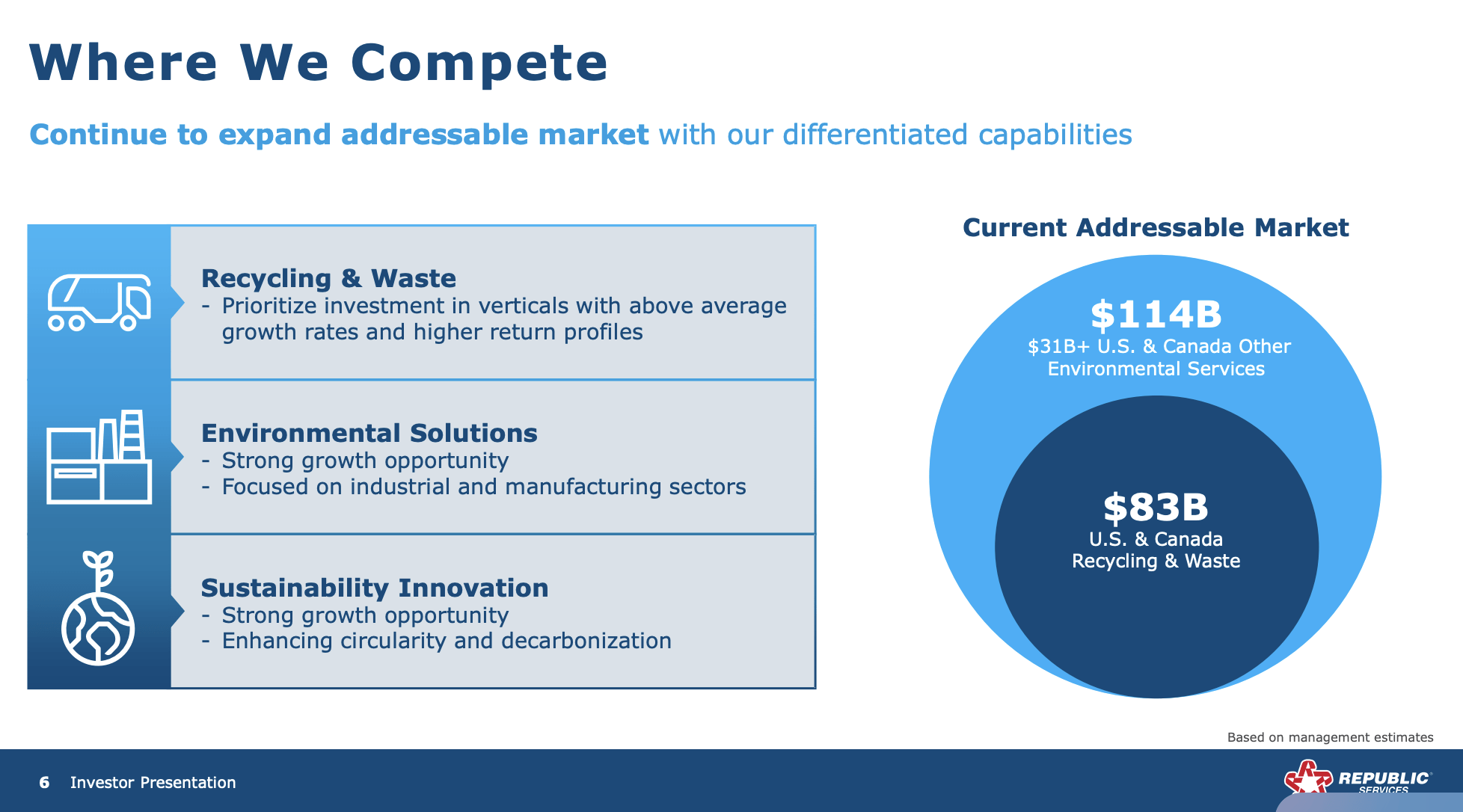

RSG is the second-largest waste management company in North America. It provides services in an industry with a total addressable market of $114 billion. Although the trash business has a cyclical aspect, it's mostly an anti-cyclical industry that comes with 80% annuity-type revenues for Republic Services.

Republic Services

The collection business represents roughly 70% of its income. Meanwhile, its business model consists of almost 200 business units with individual income statements.

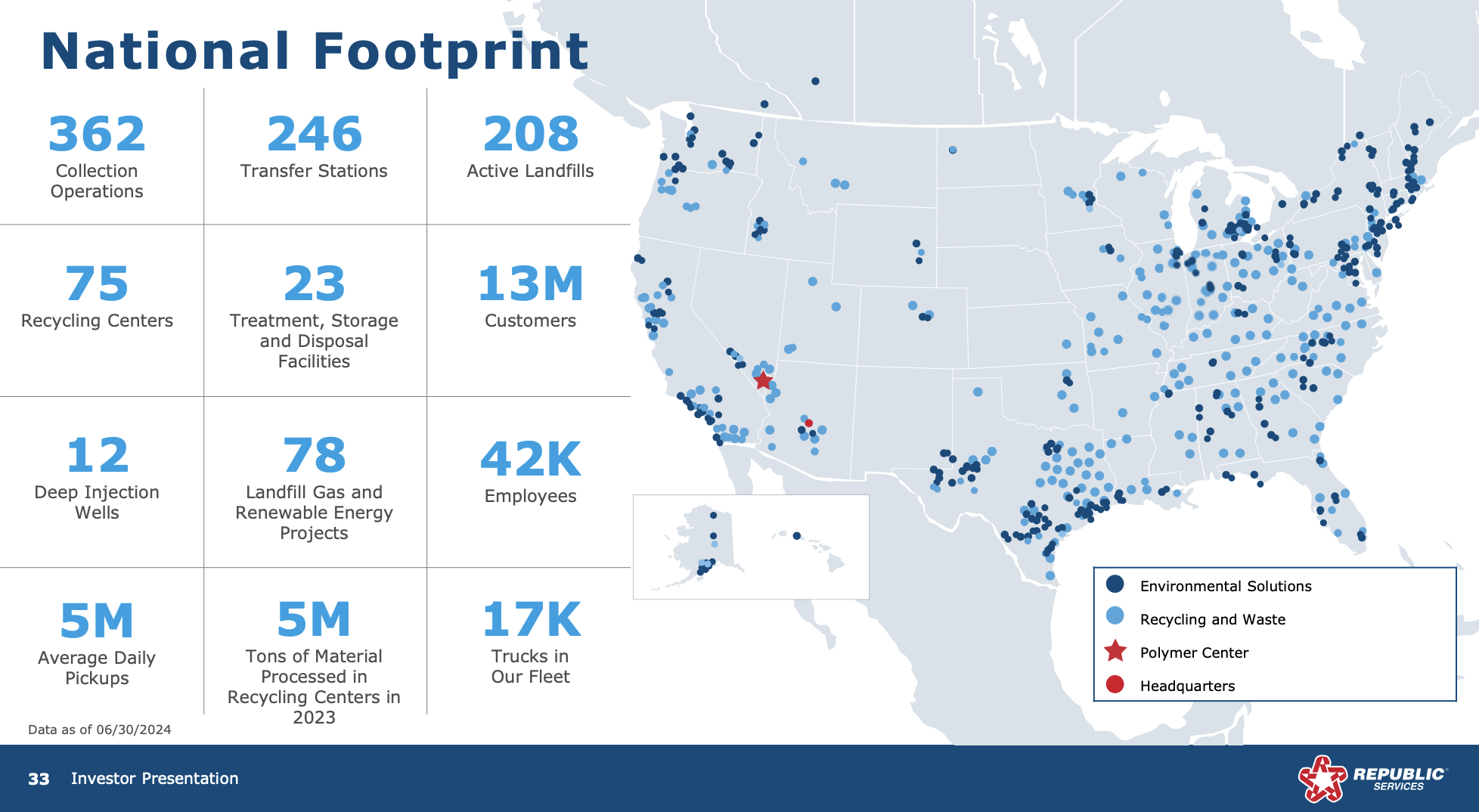

It has a footprint of 75 recycling centers, 208 landfills, and countless other assets that serve roughly 13 million customers in the United States and Canada.

Republic Services

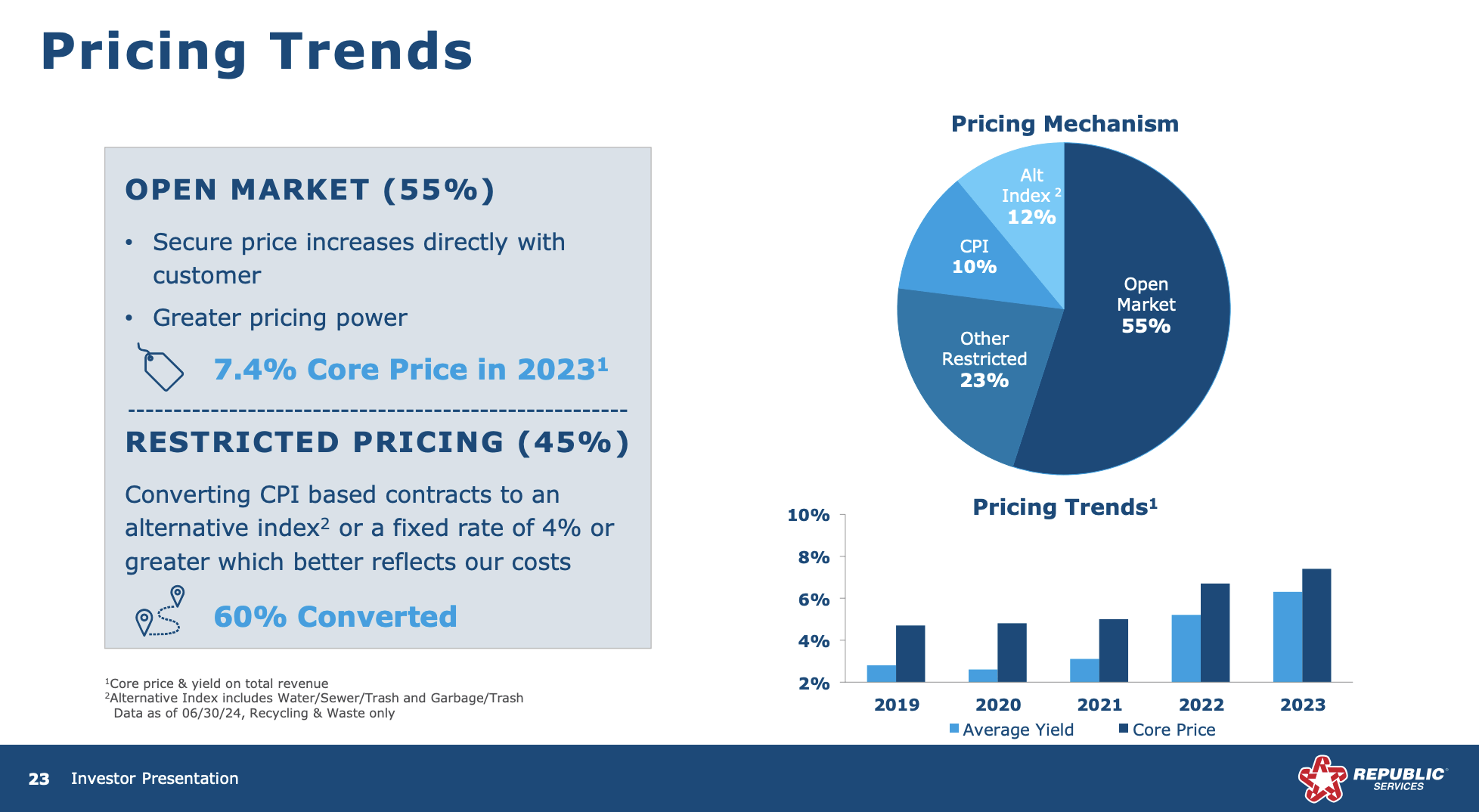

On top of that, the company has strong pricing power, as more than half of its contracts are priced on the open market. The remainder of its contracts are tied to the consumer price index, alternative inflation indices, or fixed at 4%.

Republic Services

The company is currently aggressively investing in automation, customer satisfaction, and next-gen operations like recycling and producing gas from waste.

It also benefits from the aforementioned pricing power.

Over the past three years, it has grown its EPS by 16% per year, which allowed it to return close to 150% in the five years ending December 31, 2023. This beats the S&P 500 by 41%.

Republic Services

Currently yielding 1.2%, the dividend has a payout ratio of 36% and a five-year CAGR of 7.4%. The dividend has been hiked for 20 consecutive years.

Data by YCharts

Data by YCharts

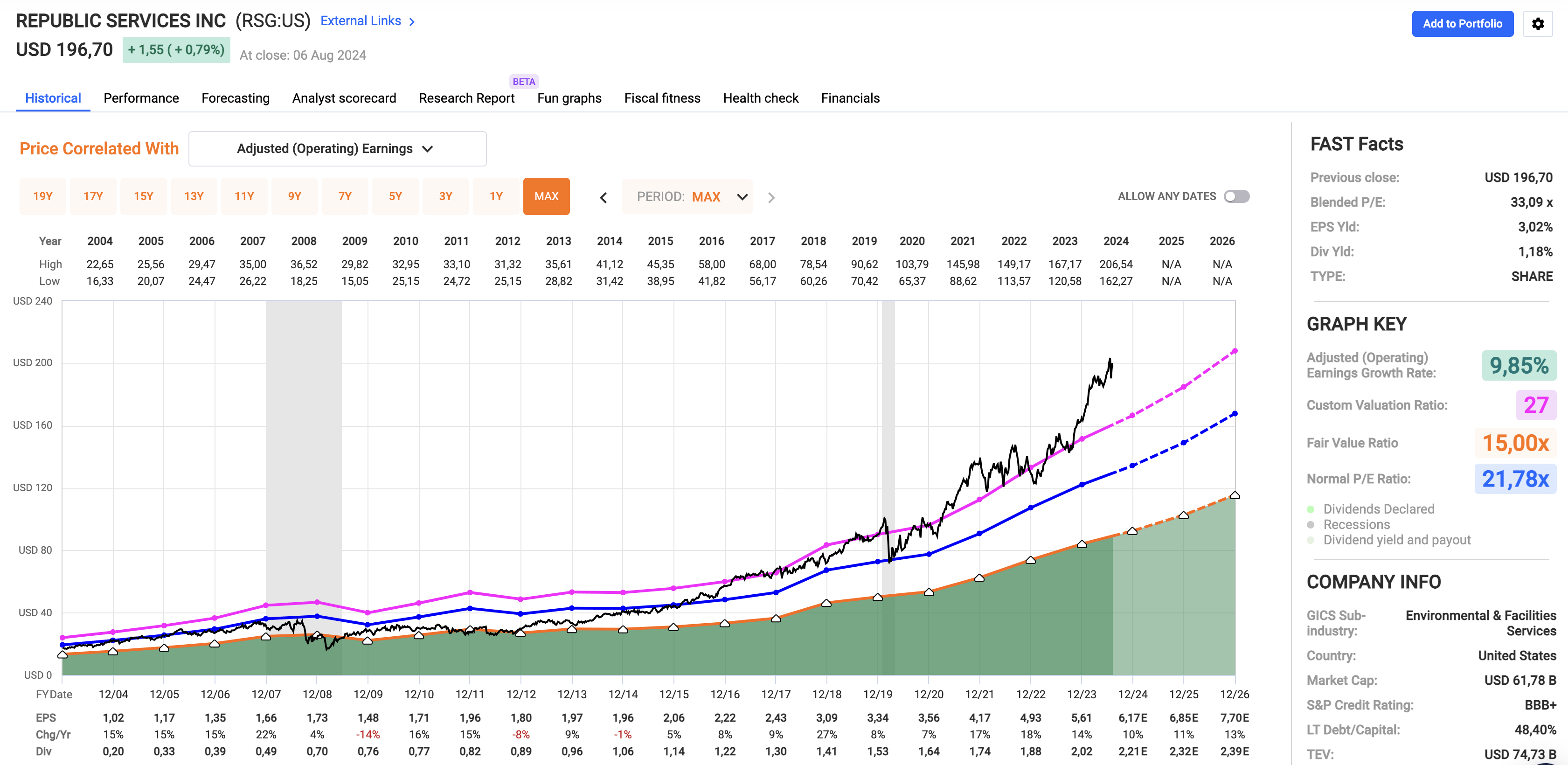

The only problem is that RSG isn't cheap. Trading at a blended P/E ratio of 33.1x, it trades a few points above its five-year average P/E ratio of 27.0x.

Using the FactSet data in the chart below, the company is expected to accelerate EPS growth from 10% in 2024 to 13% in 2026. This gives the stock a fair price target of roughly $210, 7% above its current price.

FAST Graphs

Hence, I give the stock a Buy rating and hope to buy it on the next dip, which also depends on my cash situation.

All things considered, RSG is definitely one of the best dividend growth stocks on the market, a stock I expect to survive any future recession and market crash.

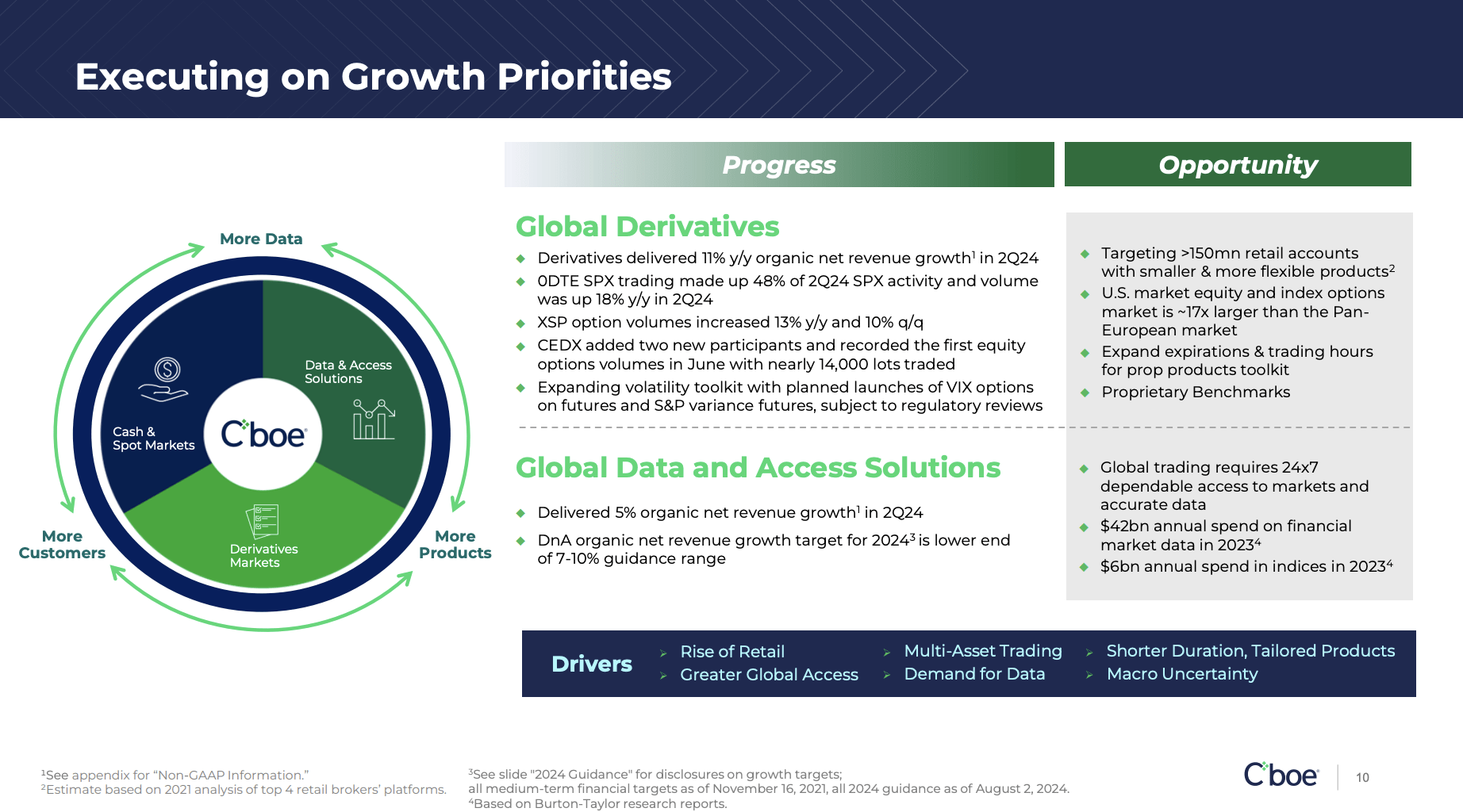

Cboe Global Markets (CBOE) - Make Volatility Your Friend

Cboe is another perfect stock for any market environment. It's also a company I recently covered in an in-depth article on August 6.

Headquartered in the beautiful city of Chicago, Cboe is one of the biggest exchange operators in the world.

Cboe Global Markets

The company operates the biggest option exchange in the United States, it's the third-largest stock exchange operator in the United States, and it owns one of the largest stock exchanges in Europe, Cboe Europe.

It also owns clearing houses and trading venues in Asia, among many other operations.

In addition to benefiting from secular growth due to increasingly attractive options, the company benefits from periods of elevated volatility. Even if the Cboe stock price declines during weak economic periods, "panic" on the stock market usually boosts the company's revenue.

Furthermore, what's interesting is that Cboe is moving away from M&A-fueled growth to internal growth. After years of aggressive M&A (see the overview above), the company is expanding its existing footprint, including APAC nations, where the company wants to increase access to popular American equities.

Cboe Global Markets

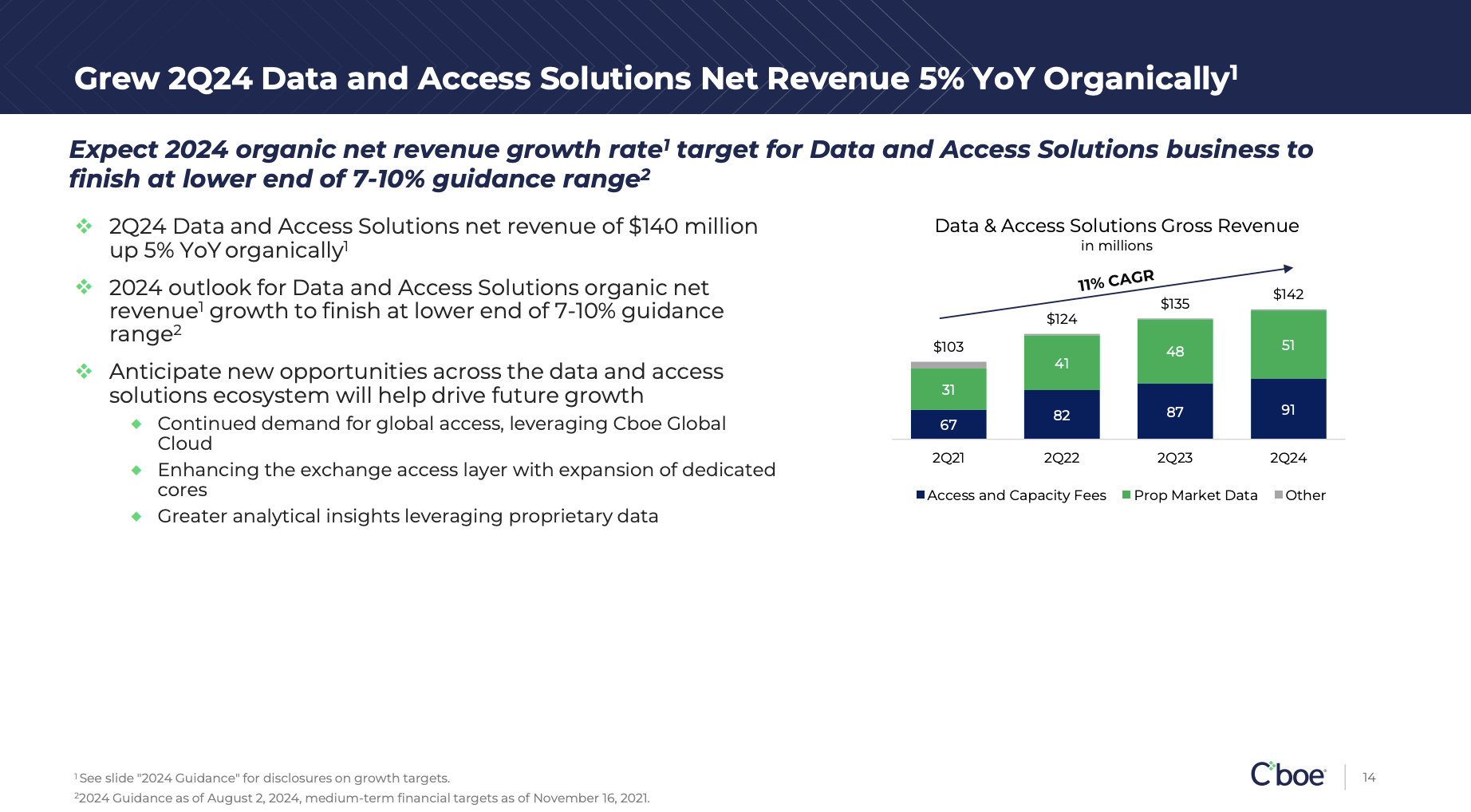

This also includes non-transaction revenue like its Data and Access Solutions segment, a part of the company that has grown by 11% per year since 2Q21.

Cboe Global Markets

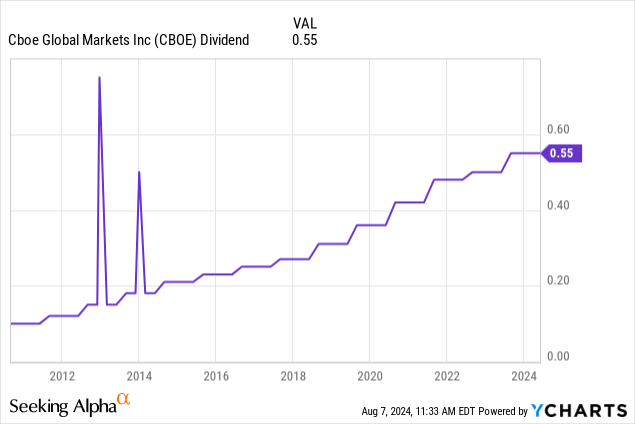

Unfortunately, like Republic Services, Cboe does not have an elevated dividend yield.

The good news is that its 1.1% yield comes with a payout ratio of 26%, a five-year CAGR of 12.2%, and 13 consecutive annual dividend hikes since it initiated its dividend.

Data by YCharts

Data by YCharts

Moreover, while the company has repurchased just 1.4% of its shares over the past three years, it will likely accelerate shareholder distributions due to its focus on organic growth instead of M&A.

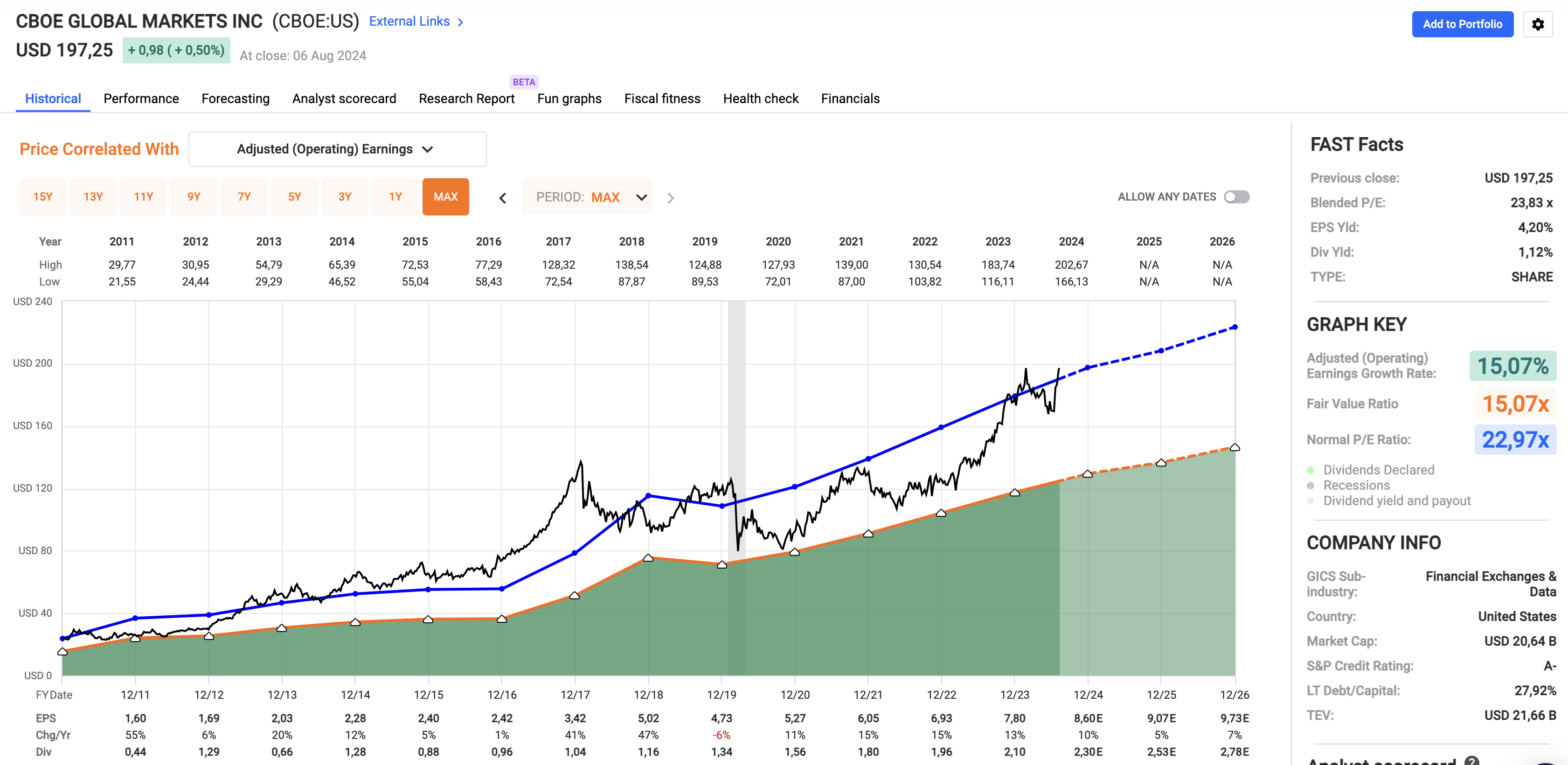

Valuation-wise, I (obviously) stick to what I wrote in my article a few days ago:

That said, with a blended P/E ratio of 23.6x, the stock trades slightly above its long-term normalized P/E ratio of 23.0x.

This implies an annual return of 7-10%, including its 1.1% dividend yield.

As such, I remain bullish and believe the company is in a great spot to beat the market on a prolonged basis.

FAST Graphs

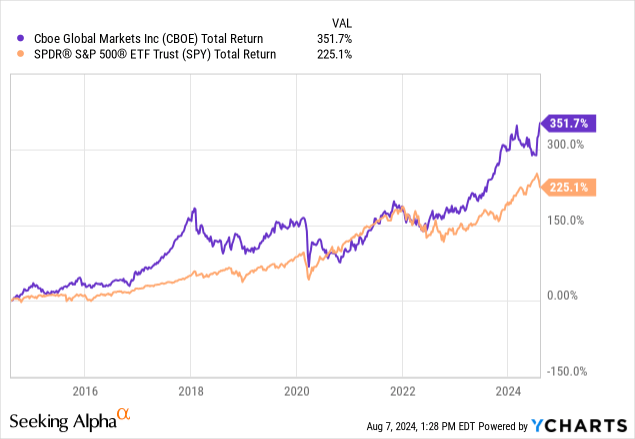

Over the past ten years, CBOE has returned 352%, beating the S&P 500 by a wide margin.

Data by YCharts

Data by YCharts

The third pick has a slightly higher yield and an even more anti-cyclical business model.

Lockheed Martin (LMT) - Still Attractive And (Literally) Very Defensive

I have to be honest. I did not want to include defense stocks. That's mainly due to the fact that I discuss these companies a lot on Seeking Alpha. While I will never get tired of discussing my investments, I want to avoid too much coverage, as it may seem I'm promoting my own investments.

That said, Lockheed was one of BofA's picks I could not ignore.

My most recent in-depth article on Lockheed was written on July 24, when I went with the simple title "Lockheed Martin Goes Boom."

Lockheed isn't just America's largest pure-play defense company, but also one of the most anti-cyclical companies in the world, as it generates roughly all of its revenue from government contracts.

Like the other two picks in this article, it has a wide-moat business model. In fact, I would say it has an ultra-wide moat business model. This is what Morningstar wrote in 2022, which is still very valid.

[...] there are some advantages to investing in the defense industry. Take Lockheed Martin’s LMT deal with the U.S. government to maintain the F-35 fighter jet until 2070. Long-lasting revenue streams come with that political process, where trust between government and enterprises creates an insular environment and contributes to a wide moat. - Morningstar

Right now, the company is bringing on all cylinders, benefitting from a multitude of tailwinds:

- NATO's focus on modernization is fueled by the Ukraine war and years of a lack of spending by mostly European NATO partners.

- The U.S. armed forces are increasingly spending on next-gen projects, including advanced missile defense, space programs, and related.

- More than four years after the COVID-19 pandemic started, supply chains are finally supportive of consistent margin growth in the defense sector.

Lockheed Martin

The reason why Lockheed's stock price is rising is not the risk of an escalating Iran war. Oil would be much higher if that were the case. I believe it's the fact that most defense giants are finally seeing a path to stronger earnings growth and higher margins.

This includes tailwinds in its F-35 program.

We continue to produce at a rate of 156 aircraft per year and expect to deliver 75 to 100 aircraft in the second half of 2024. Over 95% of TR-3 capabilities are currently being flight-tested, and we look forward to delivering full TR-3 combat capability to the customer. In addition, we expect deliveries of F-35 aircraft to exceed production for the next few years. - LMT 2Q24 Earnings Call

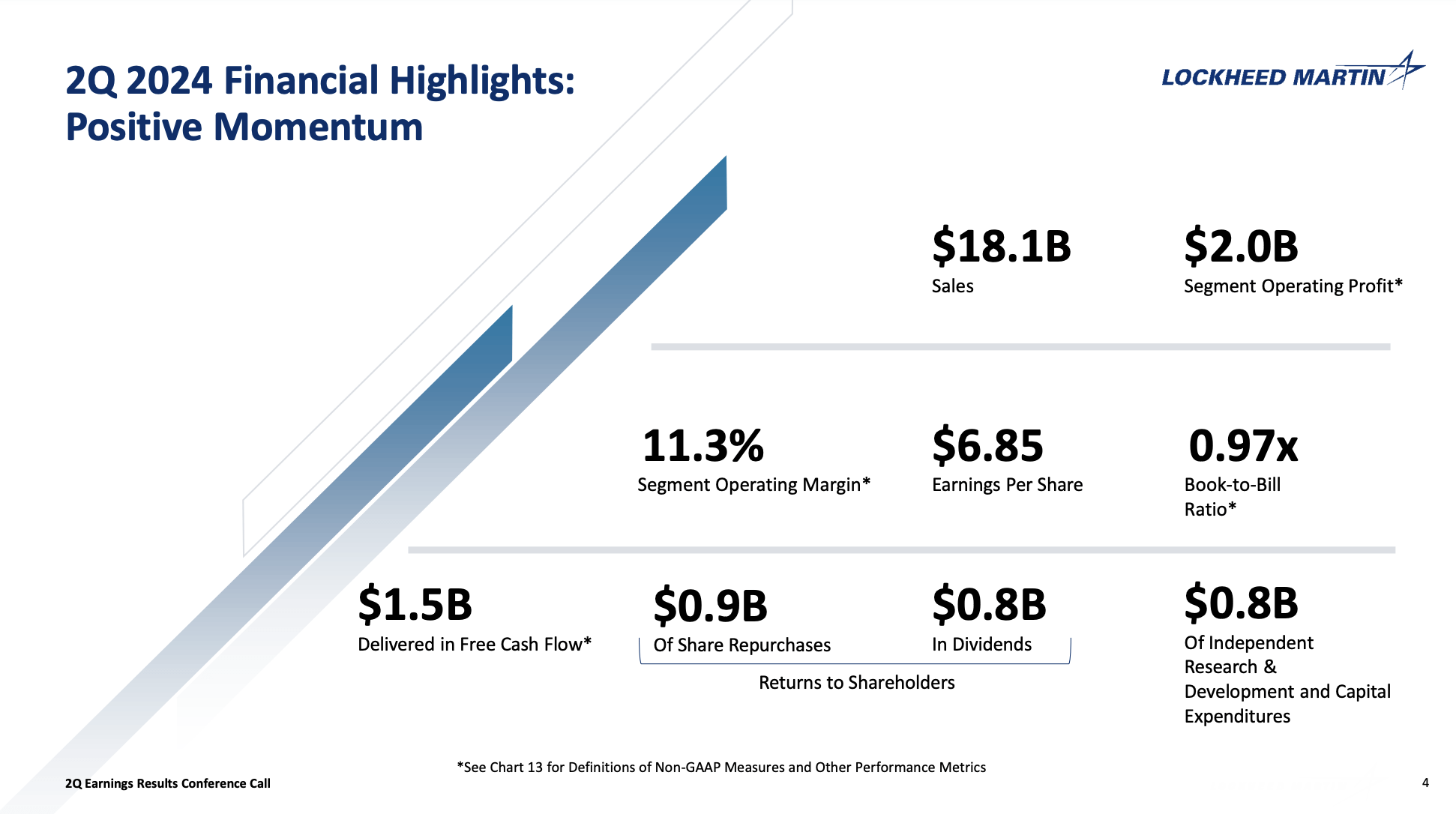

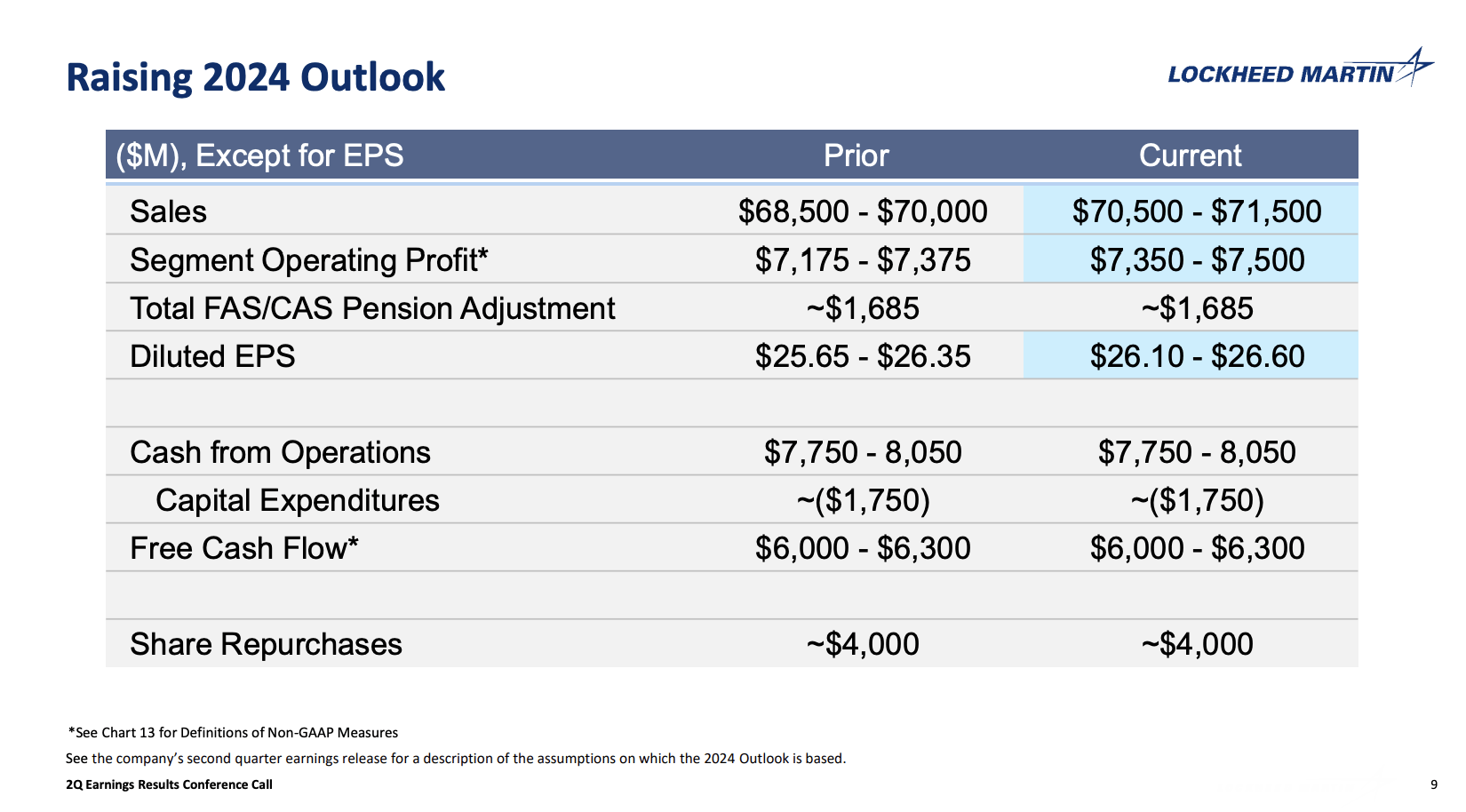

As such, the company recently hiked its sales, operating profit, and EPS guidance.

Lockheed Martin

This bodes well for shareholders.

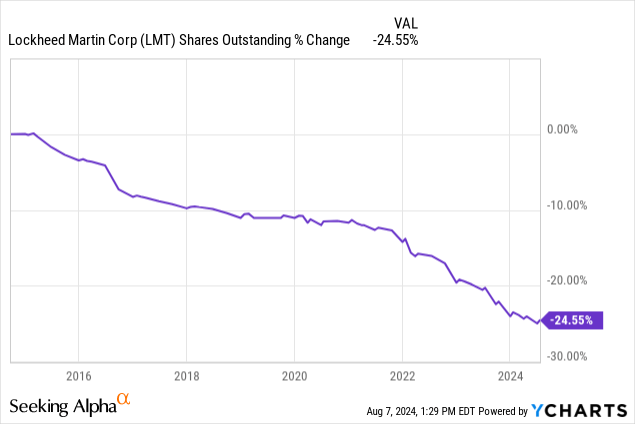

Over the past ten years, LMT has bought back a quarter of its shares.

Data by YCharts

Data by YCharts

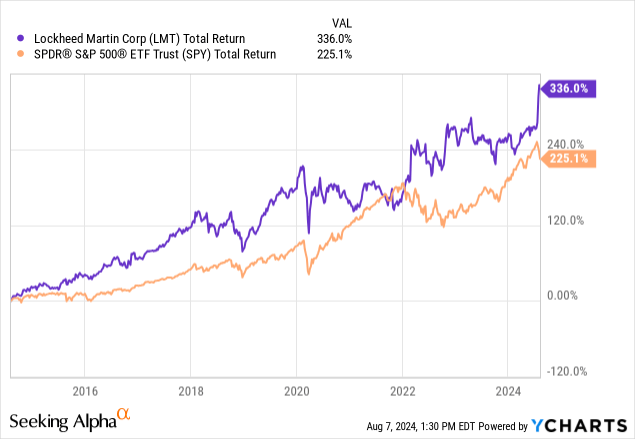

These buybacks have helped the company to return 336% since 2014, exceeding the S&P 500's performance by a wide margin.

Data by YCharts

Data by YCharts

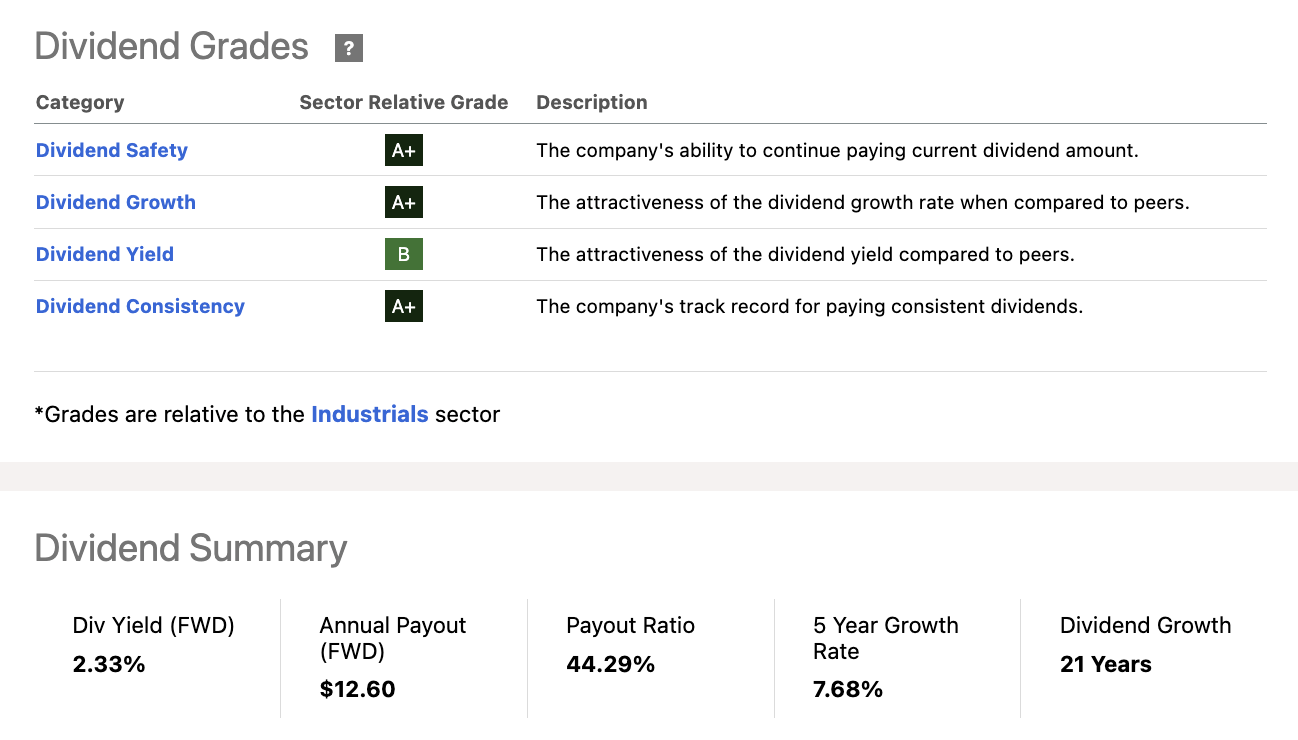

Its dividend isn't bad, either. Yielding 2.3%, the dividend has a 44% payout ratio and a five-year CAGR of 7.7%. The dividend has been hiked for 21 consecutive years. The company's dividend scorecard has 3x A+ scores.

Seeking Alpha

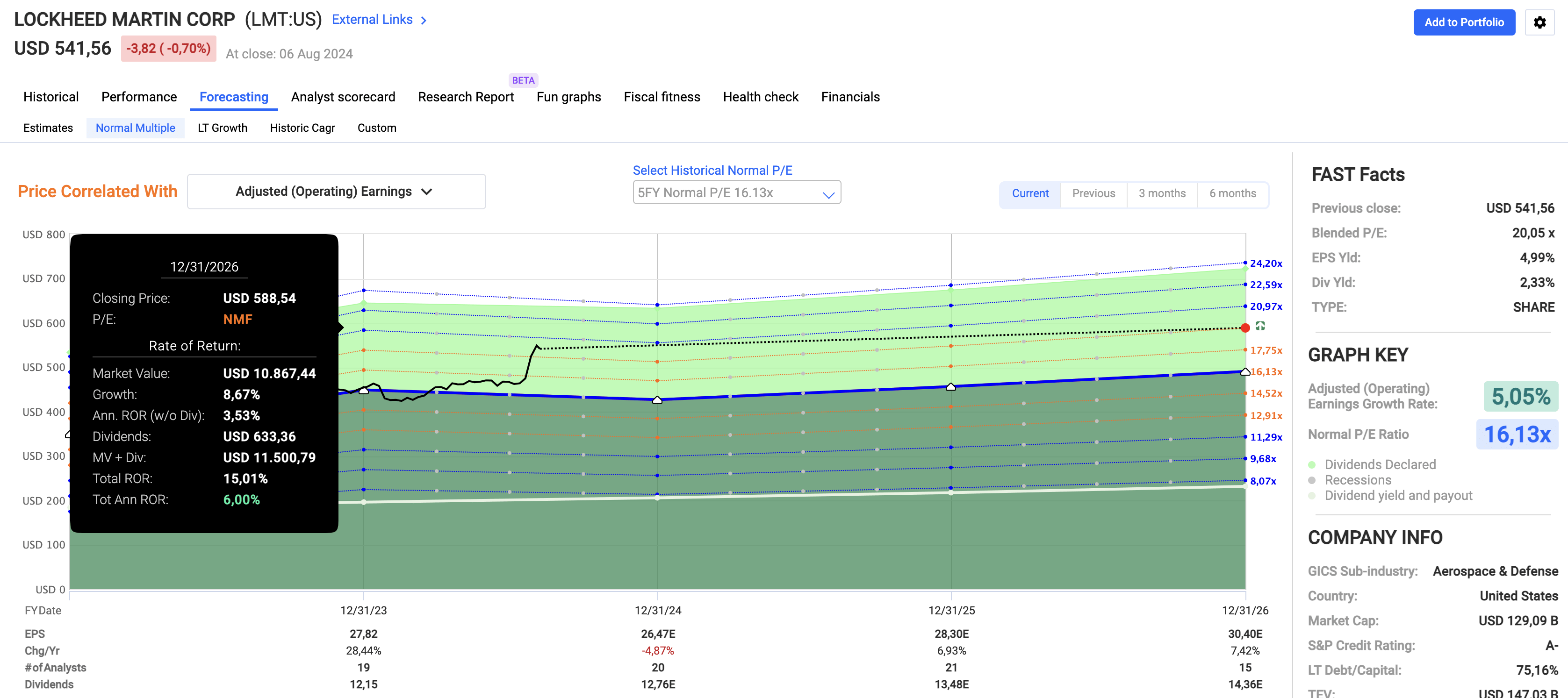

Valuation-wise, analysts expect the company to grow EPS by 7% in both 2025 and 2026. I expect these numbers to last. When applying a 19x multiple, we get a fair price target of roughly $590, 10% above the current price.

FAST Graphs

I consider LMT a fantastic long-term play and will be buying more on the next dip. It is currently my second-largest investment.

Takeaway

Recent volatility caught many off guard, including me, but it's a reminder that corrections are normal and even beneficial for long-term investors.

My "win-win" strategy thrives on this principle: I win when stocks rise, and I win again when I can buy quality stocks at a discount.

Companies like Republic Services, Cboe Global Markets, and Lockheed Martin fit perfectly such a strategy, as they are long-term investments that offer stability and growth, even in volatile times.

So, remember, market dips are not a cause for panic but an opportunity to strengthen your portfolio. It's just important to pick the right stocks.

Comments