Summary

- LandBridge Company LLC is a young, rapidly growing landowner in the Permian Basin, positioned similarly to Texas Pacific Land, with diverse revenue streams.

- LB's unique business model allows it to profit from various operations on its land, including oil, gas, water, and industrial activities, without significant capital expenditure.

- Despite being new, LB shows strong financials, high margins, and promising growth potential, making it one of my top picks in my dividend growth portfolio.

dszc/E+ via Getty Images

Introduction

It's time to talk about the LandBridge Company LLC (NYSE:LB), a company that went public on June 28. I was the first one to cover the company in an article titled "Betting Big On A Tiny Texan - Why I Just Bought LandBridge."

Since then, shares have risen by 28%, making LandBridge the fifth-largest position in my dividend growth portfolio.

In this article, I'll update my thesis. This has a number of reasons. The most important reason is the company's just-released 2Q24 earnings, the first earnings of the company's young history.

Another reason is the demand from a lot of readers. As most readers may know, I have made the Texas Pacific Land Corporation (TPL) my largest position (13% of total exposure). Texas Pacific Land is the only comparable stock on the entire market. My most recent TPL article can be read here.

In light of TPL's historical success, people are curious about what LB is all about.

I am also going with another "I'm So Bullish It Hurts" title. Although I like catchy titles, I never abuse them. So far, I have only applied this title style to three other investments. Only the best-of-the-best stocks on my radar get this title.

LB is one of them.

So, let's keep this intro short and get right to it!

Why LandBridge Became One Of My Favorite Stocks

LandBridge and Texas Pacific Land account for 18% of my total account value. Although one could make the case that this is poor diversification, I would disagree, as I truly believe these two companies have nearly unbeatable business models.

Essentially, LandBridge is a mini-Texas Pacific Land Corporation.

Texas Pacific Land is more than 8x larger than LB's $2.3 billion market cap.

It's also older, as Texas Pacific was founded in the 1880s. LandBridge was founded in October 2021.

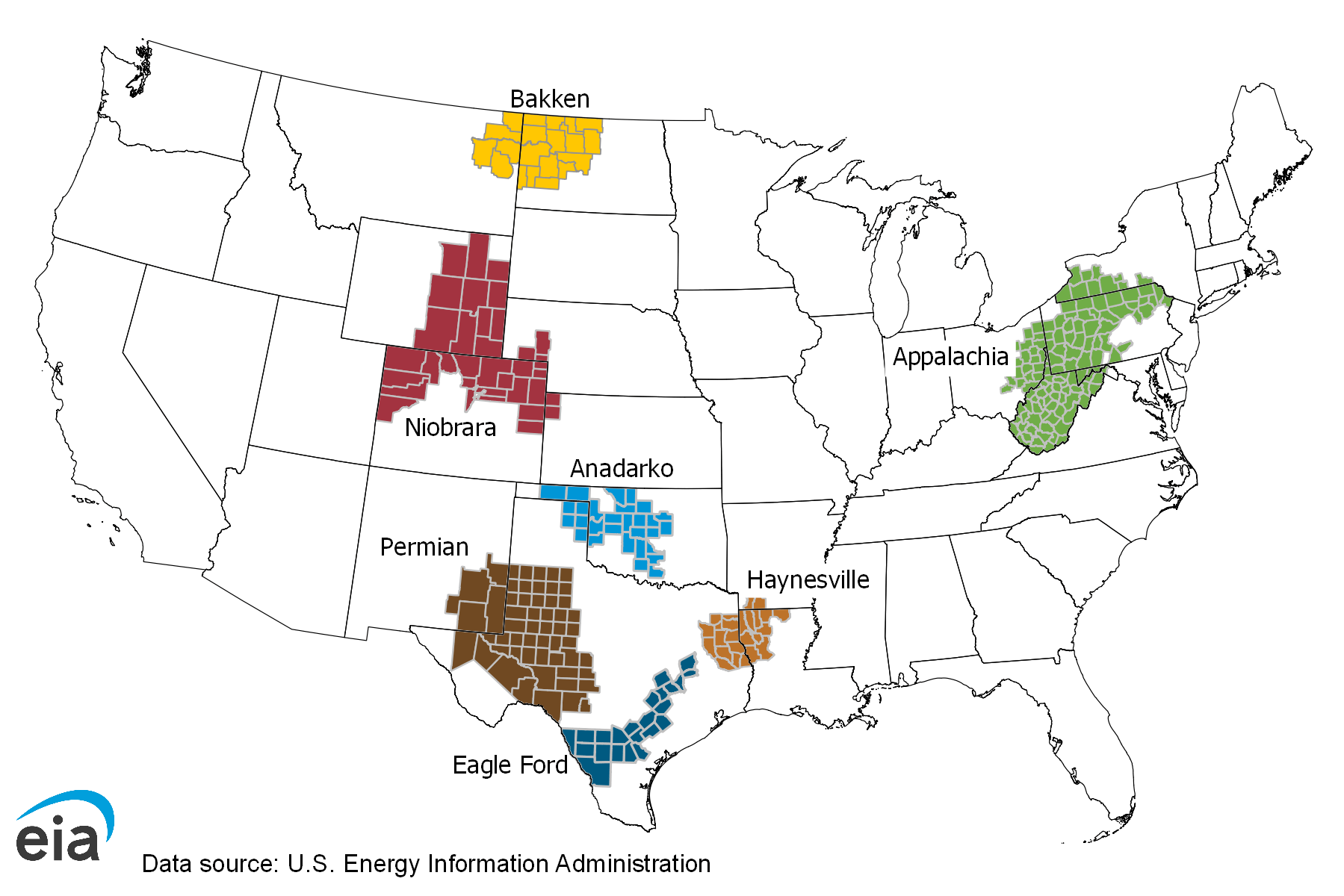

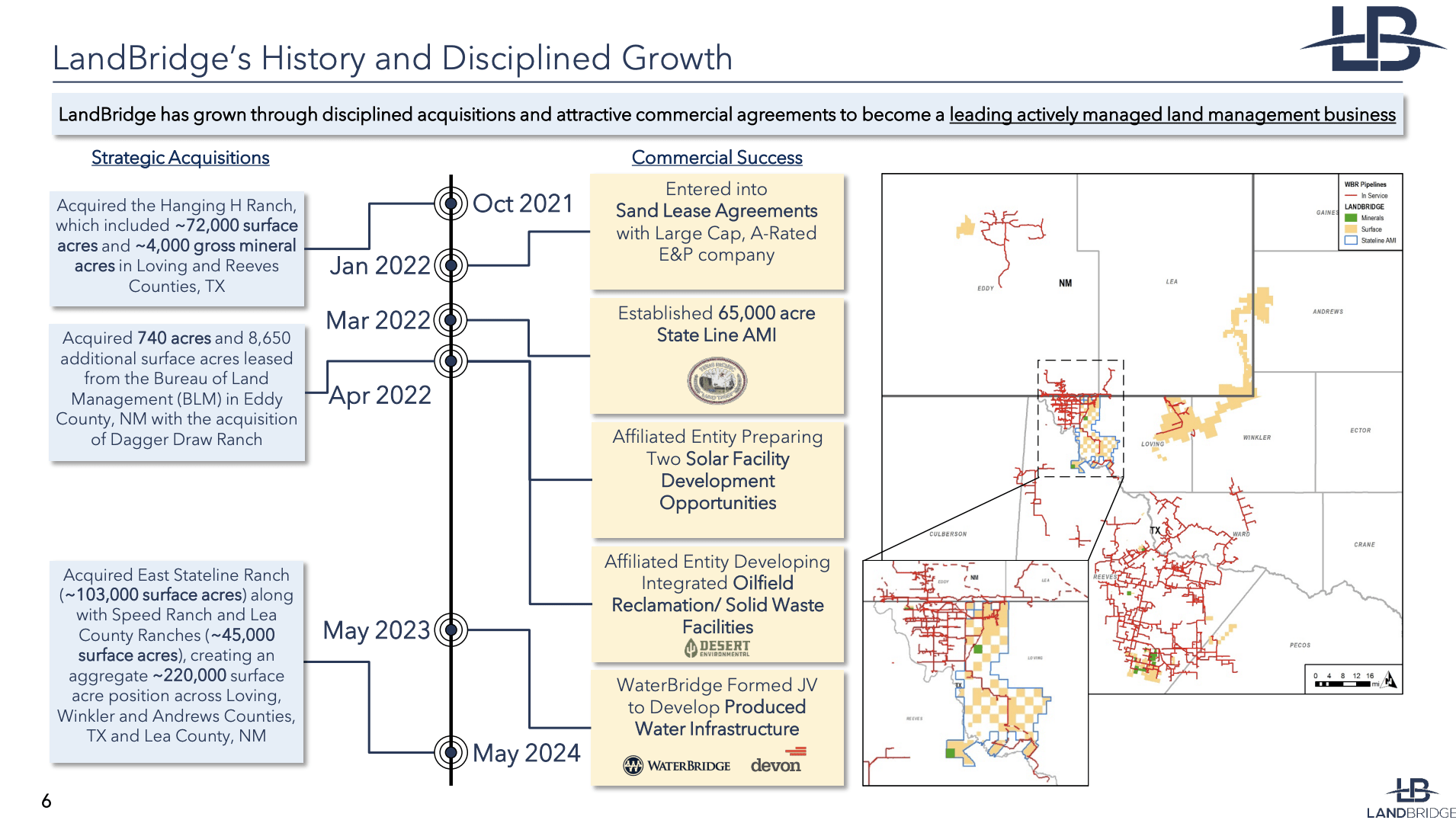

Back then, its owners acquired 72 thousand surface acres and 4 thousand gross mineral acres from the Hanging H Ranch in the Loving and Reeves Counties, Texas.

This is prime real estate in the Permian Basin, the most important oil basin in the United States.

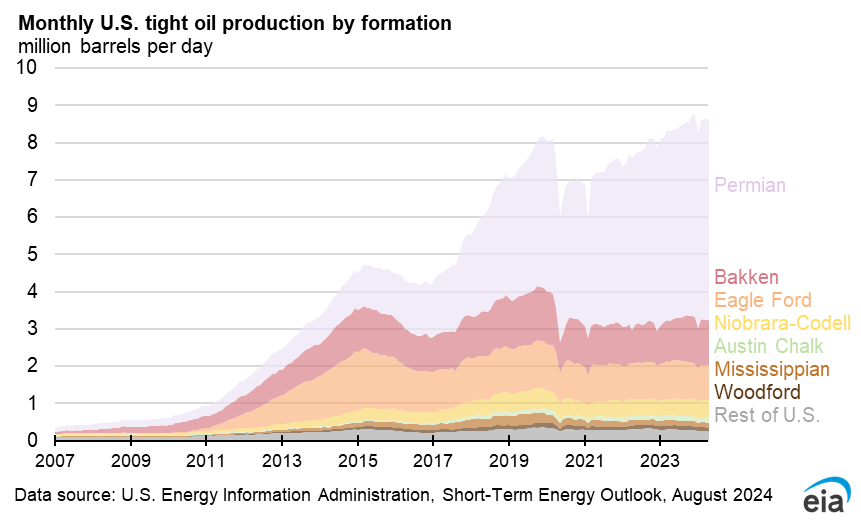

Energy Information Administration

As we can see below, the Permian produces the most oil and is the only basin that still shows consistent growth. Other major basins, including Bakken and Eagle Ford, have run out of momentum roughly ten years ago. This is also one of the reasons why oil prices have held up relatively well - despite weak global growth. Supply growth isn't the major risk it was before the pandemic.

Energy Information Administration

That said, it was not the only deal the company made, as it started to spend big this year, buying the East Stateline Ranch in addition to the Speed Ranch and Lea Country Ranches. These deals added another 148 thousand acres, bringing the total to 220 thousand surface acres.

LandBridge Company LLC

After these deals, LB has become the second-largest public landowner in the Permian, with exposure on both sides of the Texas-New Mexico border.

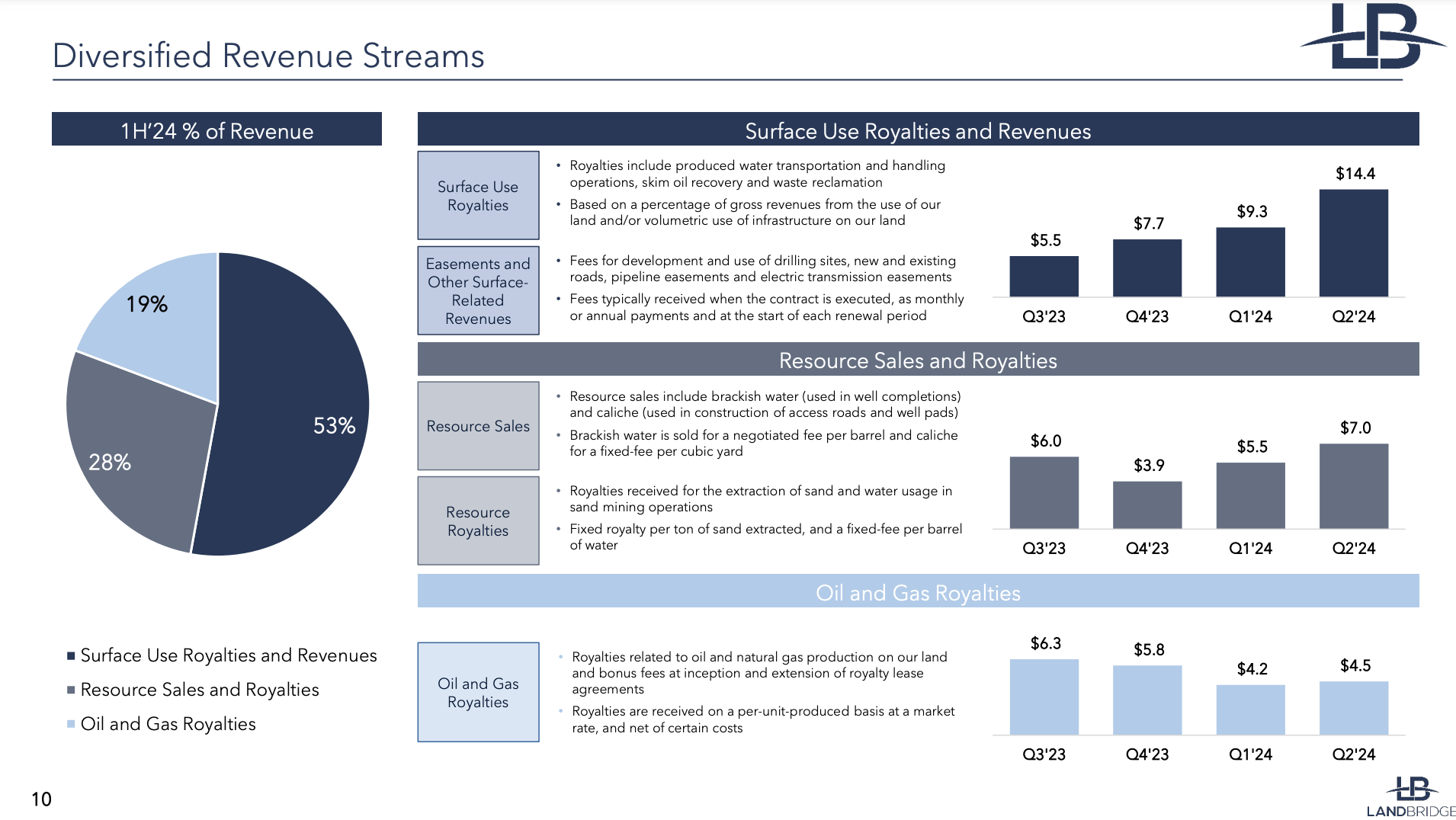

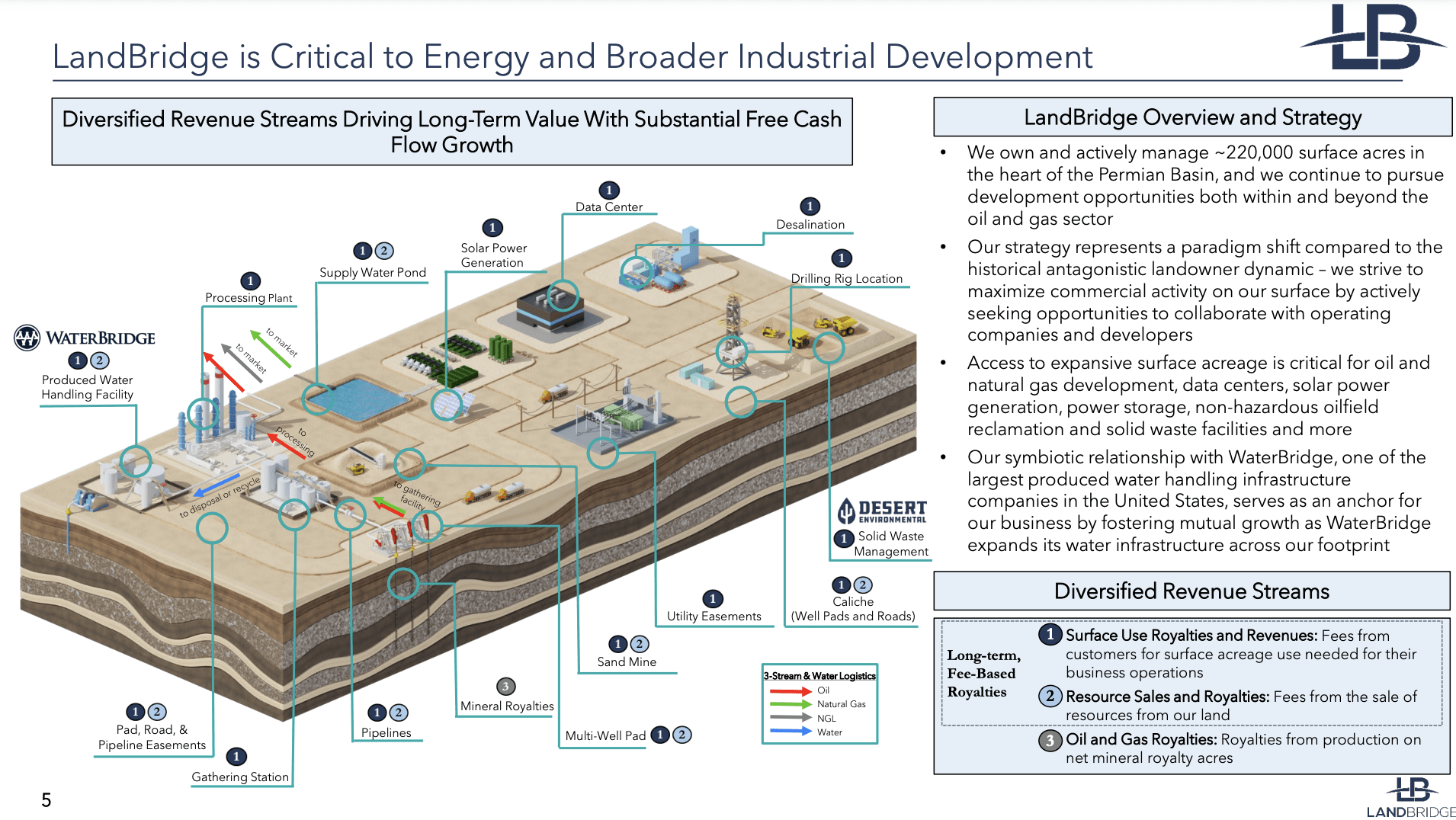

These assets put LB in a fantastic spot, as it makes money on everything that happens on its land. These operations are divided into three segments:

- Surface Use Royalties and Revenues. This segment accounted for 53% of 1H24 revenues and includes royalties from water transportation and handling operations. It also includes skim oil recovery and waste reclamation. This segment also receives fees from the development and use of drilling sites, new and existing roads, pipelines, and electric transmission easements. If anything happens on its land, LB makes money.

- Resource Sales and Royalties. These operations accounted for 28% of the total revenue in 1H24 and include brackish water (used in well completions) and caliche (used in the construction of access roads and well pads). The company is also paid for the extraction of sand and water for mining operations.

- Oil and Gas Royalties. Texas Pacific Land generates 57% of its revenues in this segment. LandBridge generated less than a fifth of its revenues in this segment. As the name already suggests, this segment makes money on every barrel of oil and gas that is produced on LandBridge's land.

LandBridge Company LLC

In addition to its size, its operations are what sets LB apart from TPL.

While LB benefits from oil and gas royalties, most of its money comes from related operations. TPL also has these benefits - it is just much more dependent on oil and gas royalties. That's not a bad thing. Moreover, most of LandBridge's assets are connected. TPL's land is divided like a checkerboard. This comes with commercial benefits, as I will discuss later in this article.

As we can see below, LandBridge has positioned itself as a critical player in energy and industrial development.

It makes money from the entire oil and gas production chain, including water and sand sales for the drilling process, the production of water during the oil and gas production process, pipelines needed to support production, royalties from produced oil and gas, as well as other operations on its land, including solar, data centers, water cleaning, roads, and more.

LandBridge Company LLC

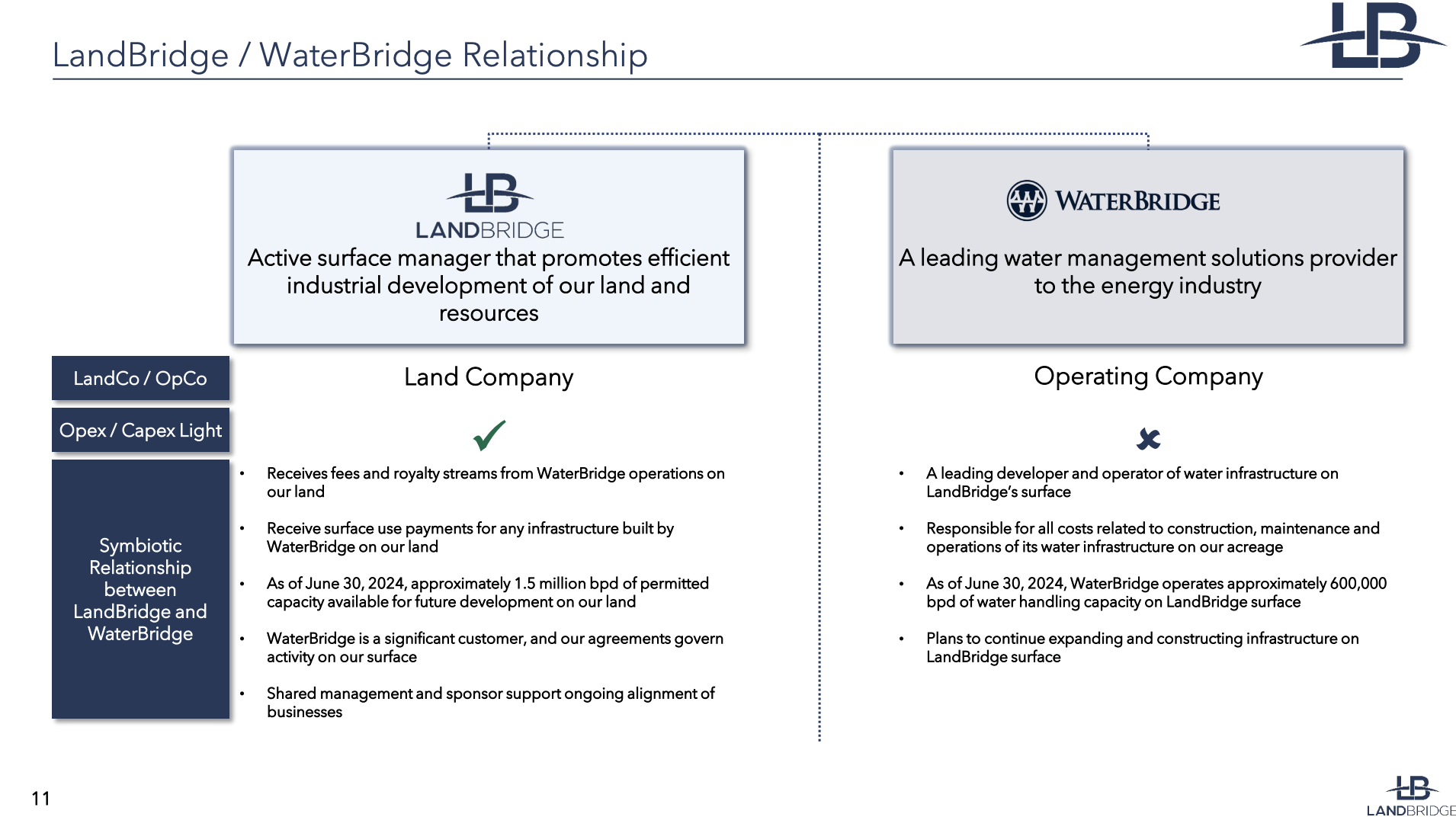

One of its most important partners is WaterBridge. As the name already suggests, LandBridge and WaterBridge have close ties. WaterBridge is also owned by the majority owner behind LandBridge, Five Point Energy.

Five Point Energy is a company that has built a number of successful energy companies. WaterBridge and LandBridge share a management team and have offices in the same building in Houston.

Essentially, LandBridge was founded to manage land for WaterBridge operations. WaterBridge is a leading developer and operator of water infrastructure in the Permian. This company is responsible for all costs related to construction, maintenance, and operations.

As of June 30, the company has roughly 600 thousand barrels of water per day in handling capacity on LandBridge's surface. This includes deals with major drillers like Devon Energy (DVN).

As we just saw, LandBridge benefits from the infrastructure and water volumes on its land - without bearing any of the costs!

LandBridge Company LLC

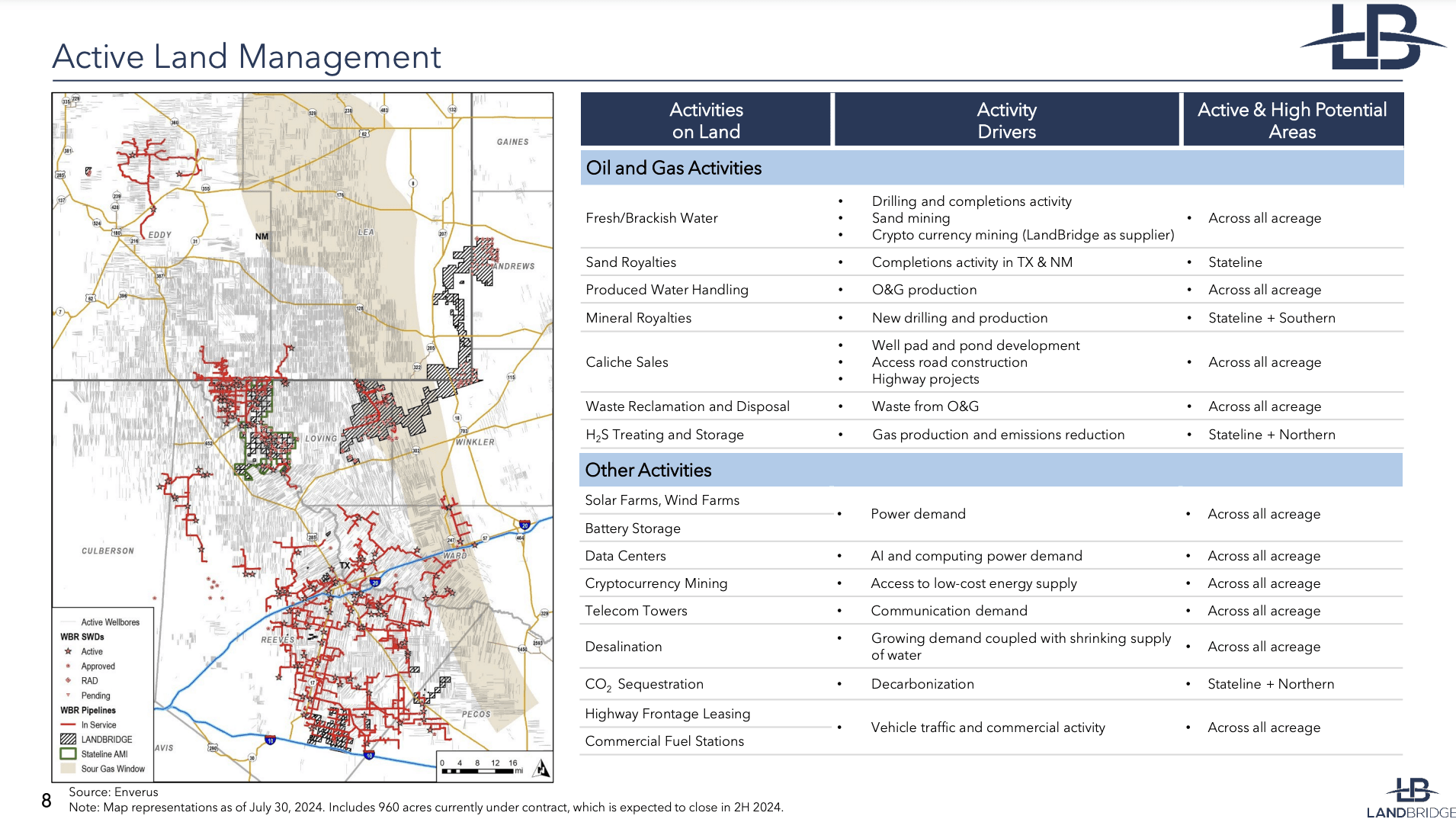

The slide showing LandBridge's history I showed in this article includes a map that shows an overview of LandBridge land and WaterBridge pipelines.

Below, we see a similar overview, including a full overview of potential operations that can take place on LB's valuable land.

LandBridge Company LLC

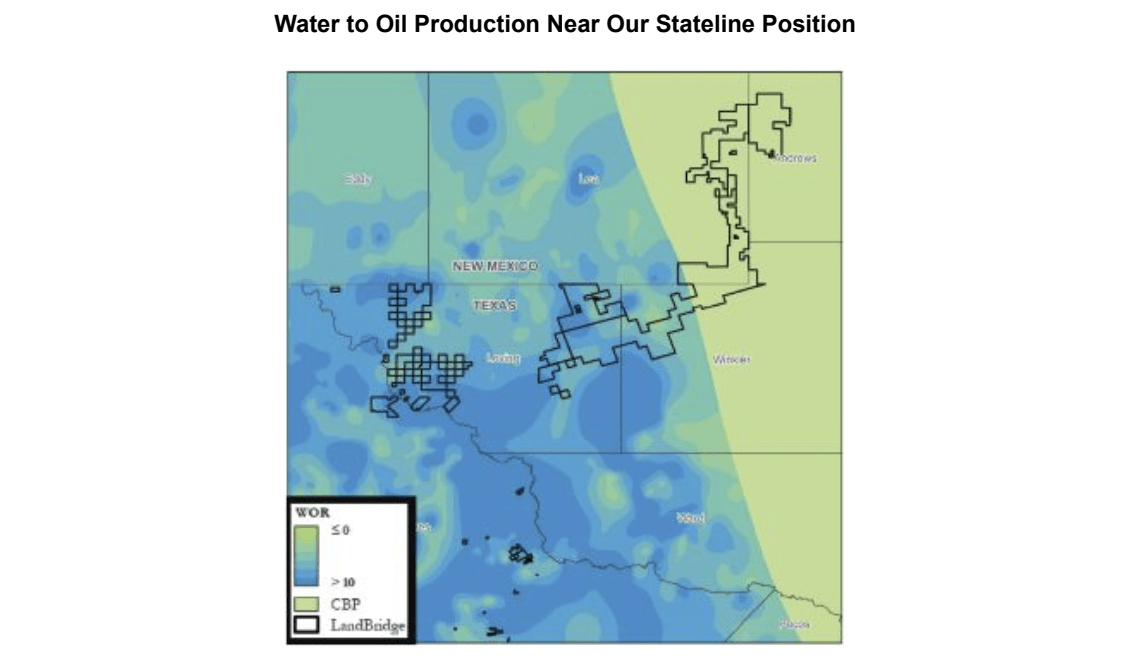

I truly believe the water business is one of the most underestimated operations in the energy sector.

As I wrote in my prior article, water is not only needed in the drilling process but also a by-product of oil and gas production. The map below shows the water-to-oil ratio on LB's land.

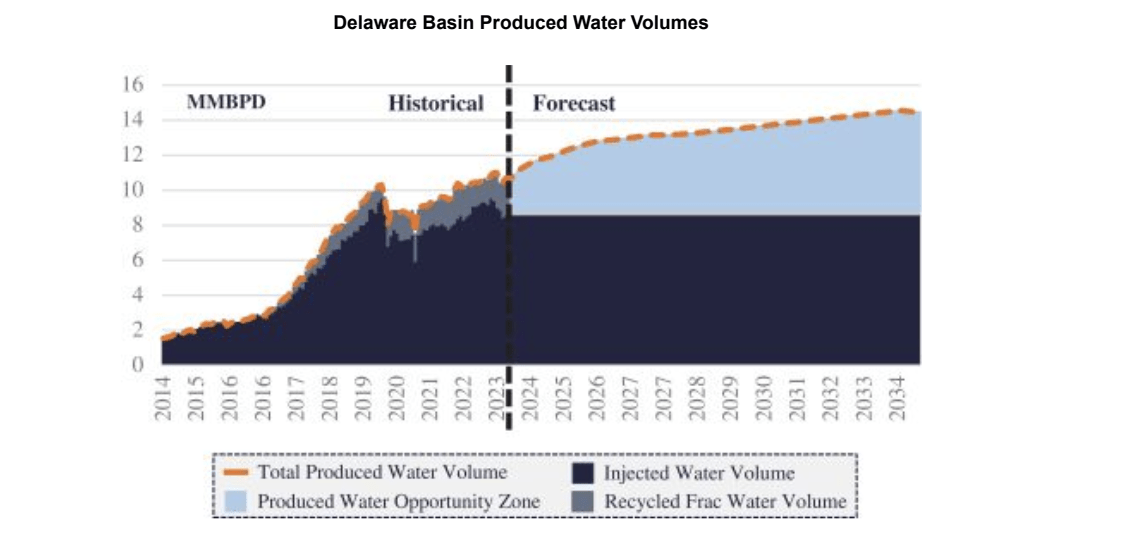

Generally speaking, the Delaware Basin (a part of the Permian where LB operates) sees 4x more water production than oil production.

For every barrel of oil produced, operators must manage four barrels of water, requiring infrastructure for water cleaning and disposal.

Using the map below, we see LandBridge's land is strategically located on top of oil reserves that come with a lot of water.

LandBridge Company LLC

In general, the Delaware Basin is expected to see significant water production growth. Between now and 2034, water volumes are expected to rise from roughly 10 million barrels to more than 14 million barrels. That's daily volumes.

LandBridge Company LLC

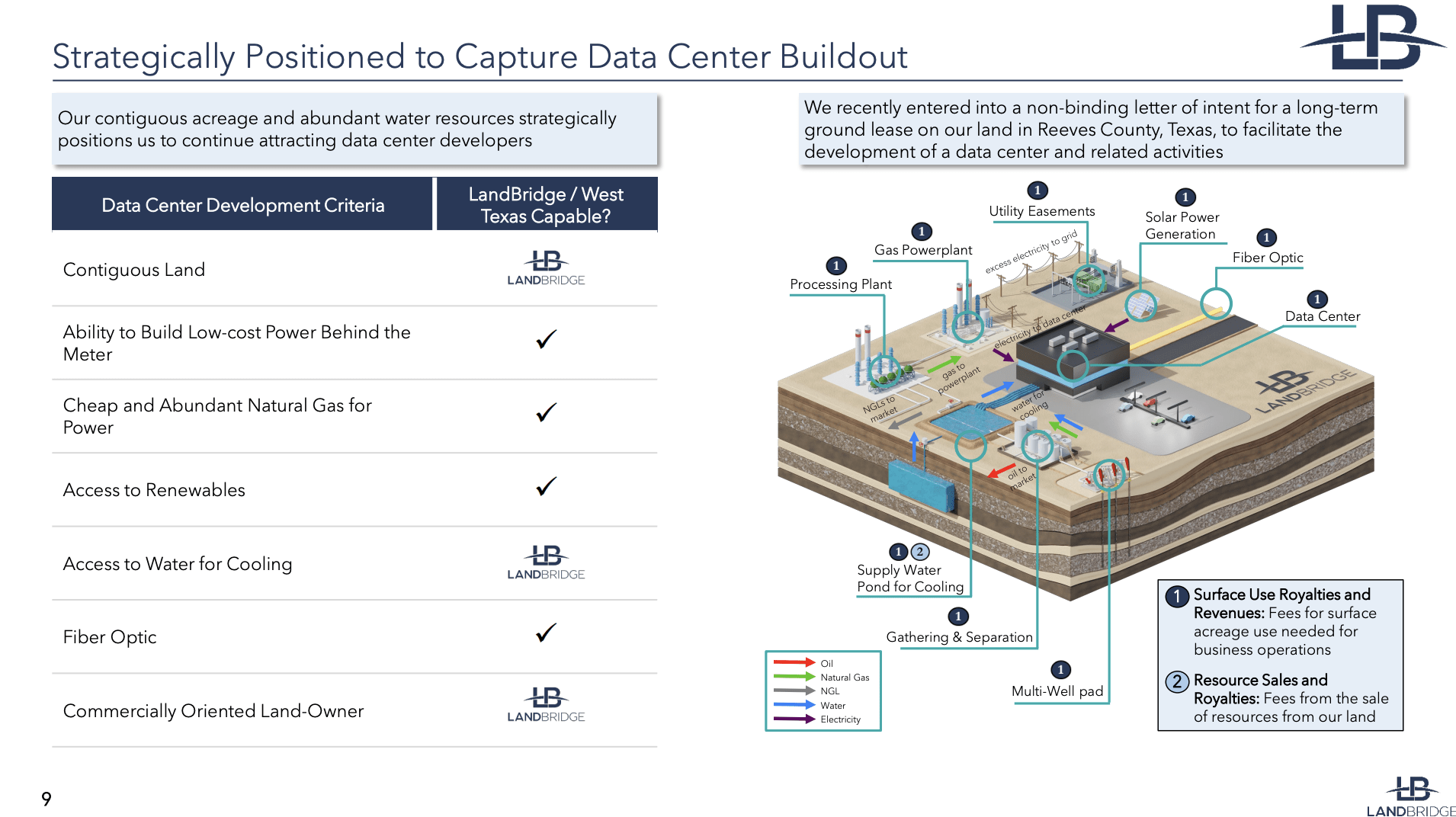

Not only will LandBridge benefit from rising water volumes, consistent oil production, and similar products, but it will also benefit from industrial development.

Its land in the Permian has a number of benefits:

- There's a lot of oil and gas. We already discussed this. However, one additional benefit is cheap natural gas. Because the quality of oil reserves is declining, the production of "associated gas" is rising, pressuring natural gas prices in the region. Some producers burn natural gas to avoid paying companies to take it away. That's how cheap it is.

- Texas has a mostly deregulated electricity market, which makes it easier to build transmission lines.

- Because there's so much water, it's a cheap resource that can be turned into value-adding operations.

- The Permian is very remote.

The three bullet points above make the Permian perfect for a wide number of industrial companies that have nothing to do with oil and gas. Data centers, for example, need cheap energy, transmission lines, cooling water, and locations with low NIMBY (not in my backyard) risks.

LandBridge "recently" entered into a non-binding letter of intent for a long-term ground lease on its land in Reeves County to support the construction of a data center with related assets.

As LandBridge has continuous land, it's often easy for it to close these deals, as the number of stakeholders to take care of is low. It also has cheap energy, water, and other benefits that all result in additional surface royalties.

LandBridge Company LLC

The company will continue to seek similar opportunities in the future, such as solar farms, hydrogen production, energy-intensive crypto mining, and other industrial operations that are well-suited for the Permian area.

In my opinion, the favorable revenue mix and long-term opportunities make LB stand out as one of the best business models in my entire dividend growth portfolio.

After all, the company benefits from many tailwinds without having to spend capital! It lets other companies invest in return for royalties and related revenue streams.

This is great news for investors.

There's A Lot Of Value In LB

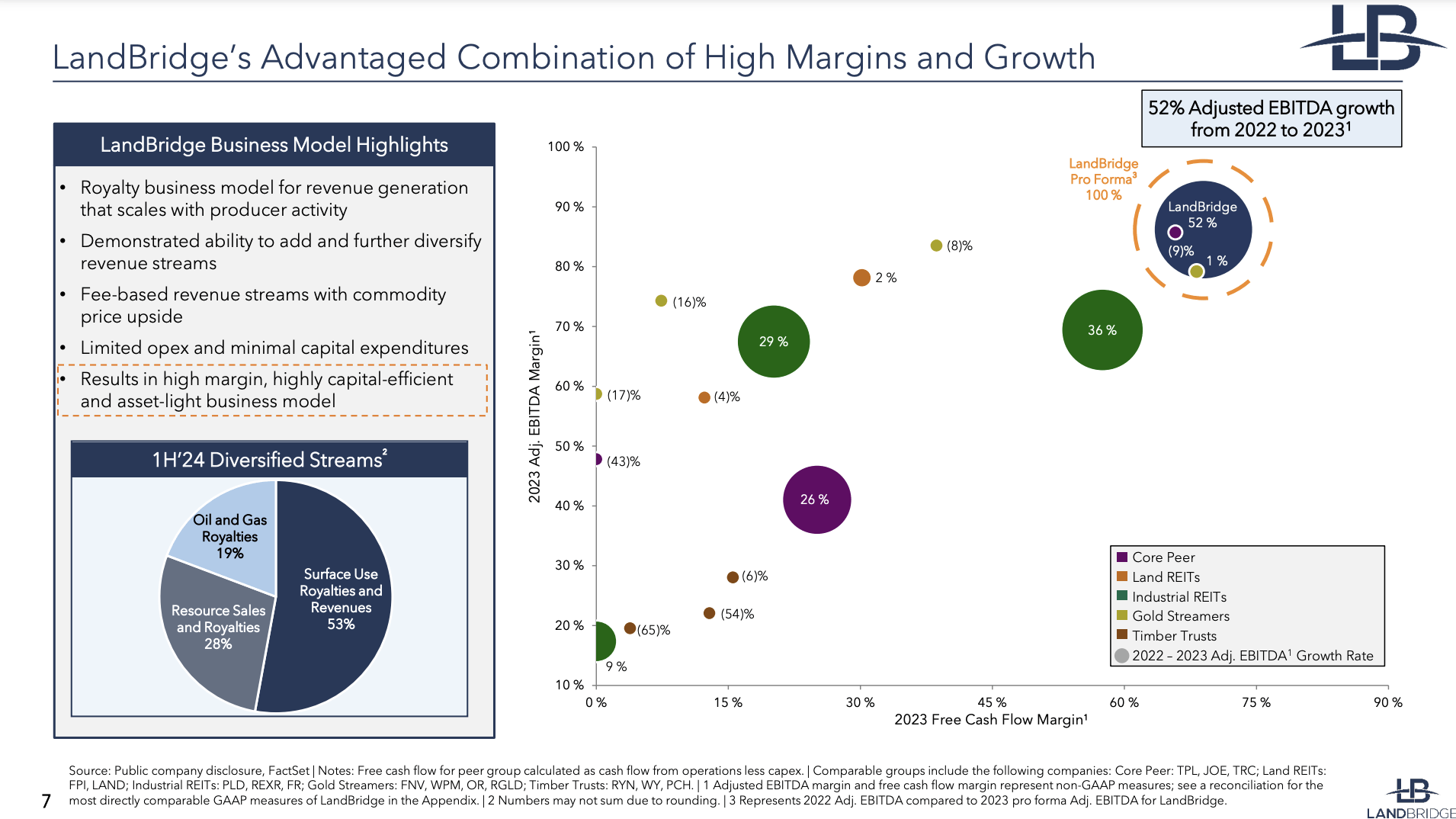

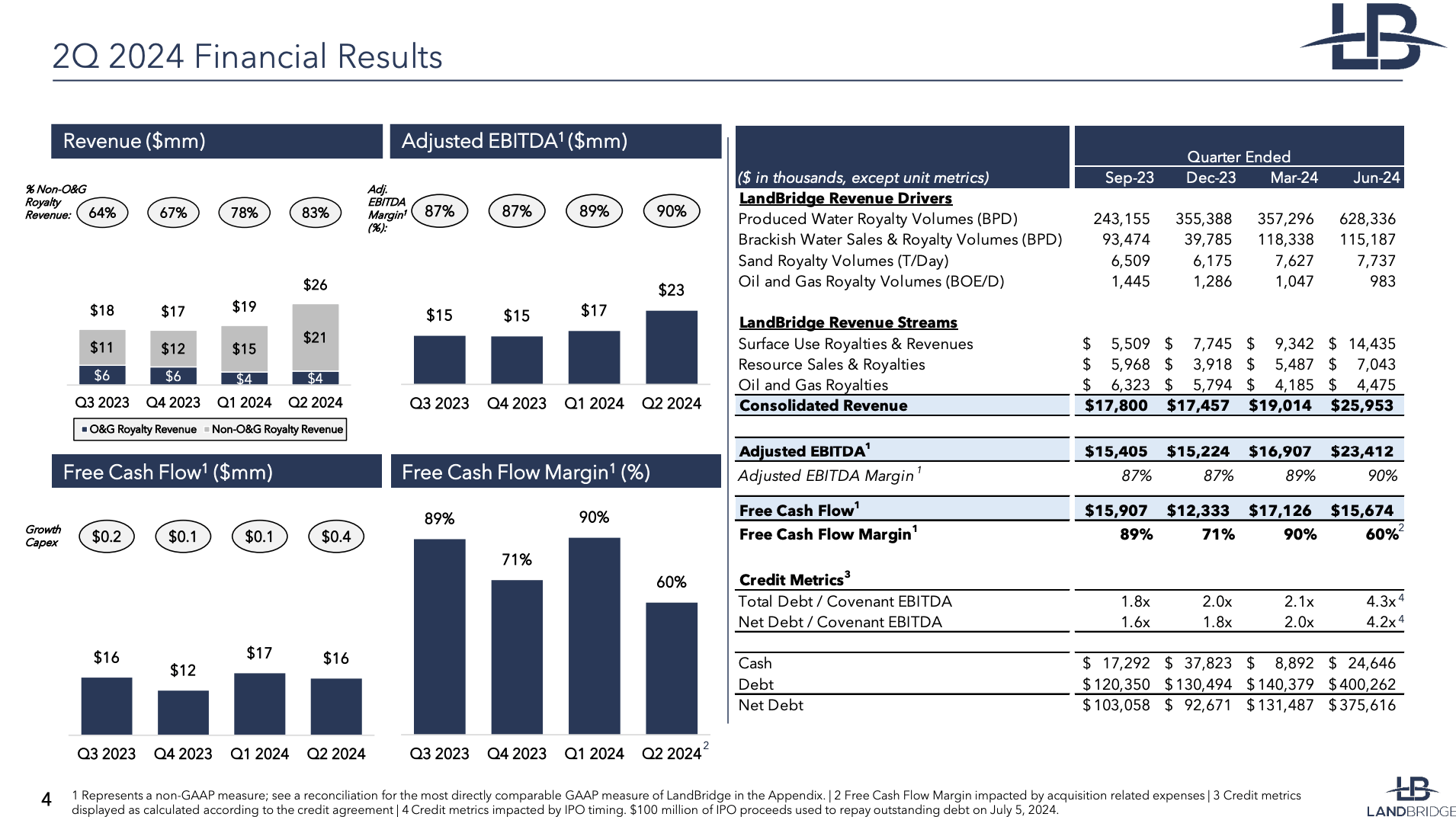

The power of LandBridge can be seen in the overview below. As of its just-released second quarter, the company has an adjusted EBITDA margin of 90% and a free cash flow margin of 60%. In 1Q24, the company had a free cash flow margin of 90%.

These numbers are mind-blowing, as the company is basically turning every revenue dollar into 60 to 90 cents of free cash flow. As we can see below, the company is more efficient than its core peer (that's Texas Pacific Land), all land REITs, industrial REITs, and high-margin gold streamers. Gold streamers are companies that finance mining operations in return for the right to buy future production at a discount.

This margin profile also comes with tremendous inflation protection. I would even make the case that LB is one of the best inflation plays on the entire market.

LandBridge Company LLC

Moreover, in its just-released second quarter, the company reported fantastic numbers.

It saw 628 thousand barrels per day of produced water royalties, up from 357 thousand daily barrels in the first quarter. Brackish water sales slightly declined to 115 thousand barrels per day. Sand volumes remained steady at 7.7 tons per day. Oil and gas royalties fell to 983 barrels per day, which is down from 1,047 barrels per day in 1Q24.

Thanks to these developments, revenue increased by 20%, adjusted EBITDA rose by 24%, and adjusted EBITDA margins rose by 3 points.

LandBridge Company LLC

Moreover, the company ended the quarter with $376 million in net debt. This translates to an adjusted net leverage ratio of 4.2x.

However, because the company completed its IPO at the start of the third quarter, not all benefits are visible. Because of the IPO, the company was able to reduce net debt by $100 million, lowering the net leverage ratio to 2.6x.

LandBridge Company LLC

One year from now, the company will likely have a sub-2x leverage ratio, which is its target ratio. Also, note that EBITDA is adjusted for costs related to the IPO.

So, what does this mean for investors?

As you may know, I exclusively invest in dividend (growth) stocks. Well, until I bought LandBridge. Because LandBridge is so young, it has not yet announced a dividend.

The good news is that in my first article, I already mentioned that LB had the intention to pay a dividend. Now, it has reiterated this plan.

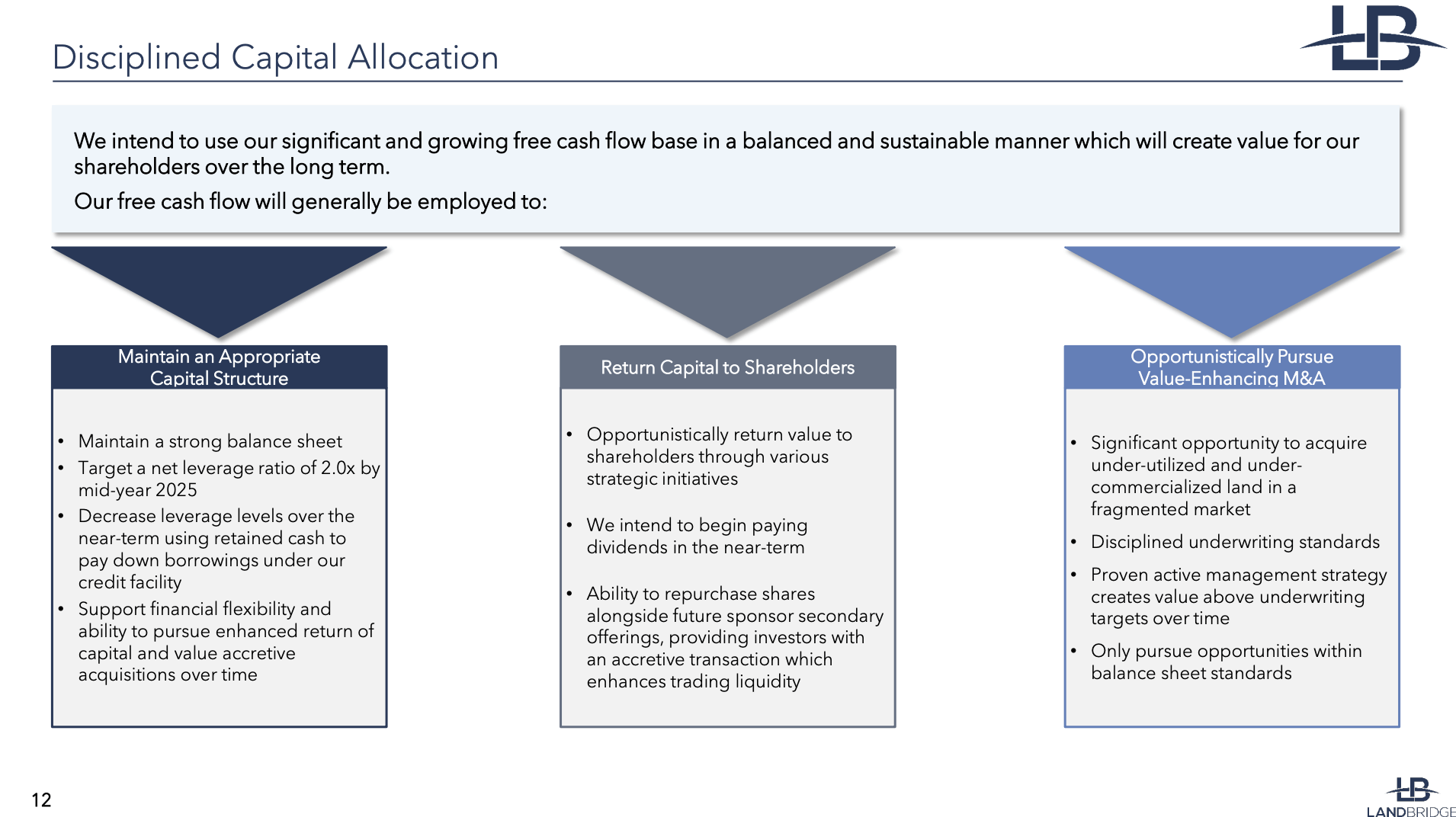

Essentially, the company has three uses for its capital:

- Maintaining an appropriate capital structure. The company wants to maintain a healthy balance sheet, with a net leverage target of 2.0x by mid-year 2025. Lowering debt benefits shareholders due to lower financial risks and interest payments.

- Returning capital to shareholders. The company wants to opportunistically return value to shareholders through various ways. This includes its intent to begin paying a dividend in the "near term."

- Opportunistic M&A. The company wants to keep buying under-utilized and under-commercialized land in a highly fragmented market. However, the company will not spend money recklessly just to expand its business. It will carefully pick investments and start buying if it sees a clear path to higher value down the road.

LandBridge Company LLC

So, what is LB worth?

That's one of the toughest questions, as the company is so young. Its potential is "limitless" and it is not clear what LB will look like a few years from now.

- How many large commercial deals will it close?

- How aggressive will its M&A strategy be?

- What will oil, gas, and water production in the Permian look like a few years from now?

These are just three questions that are hard to answer.

For now, we have a number of expectations, including a path to $173 million in sales by 2026 (from $112 million in 2024E). An 80-90% EBITDA margin would imply a path to at least $140 million in EBITDA. In fact, 2026 is expected to see $156 million in EBITDA.

Net income is expected to rise to $128 million.

Texas Pacific Land trades at a blended P/E ratio of 42x, with a three-year average of 35.4x (FactSet data). While these numbers may seem elevated, please be aware that we are dealing with an ultra-high margin company.

However, Texas Pacific Land also has zero gross debt and a proven track record. LB does not have these benefits yet.

Nonetheless, applying a 30x multiple to LB would indicate a market cap of $3.8 billion. That's 65% above its current market cap.

I believe this is a fair assessment. It's also the reason why I stick to a Strong Buy rating. Moreover, even though I have a large investment already, I'm looking to buy more shares on future corrections, as I truly believe LB is one of the best companies on the stock market - across all sectors.

Needless to say, LB is young, and analyst estimates are prone to a lot of uncertainty. Regardless of how bullish I am, always do your own due diligence.

Takeaway

LandBridge has quickly become a cornerstone of my portfolio, thanks to its exceptional business model that benefits from a wide range of tailwinds in energy and industrial operations in the Permian Basin.

The company's first earnings report confirms its strong performance, with impressive margins and a strategic advantage that allows it to profit from every aspect of its land without bearing operational costs.

With a path to significant revenue and EBITDA growth, I remain highly confident in its long-term potential.

Despite its young age, LandBridge is one of the most compelling investment opportunities I've encountered in my career.

Pros & Cons

Pros:

- High Margins: LB has an almost unbeatable margin profile, as it has a low-cost profile and multiple revenue streams from tenants and third parties.

- Prime Real Estate: Located in the heart of the Permian Basin, LB controls valuable land with exposure to growing oil, gas, and water production.

- Diverse Revenue Streams: LB earns from multiple sources, including surface use, resource sales, and royalties, making its business model highly resilient.

- Growth Potential: With strategic acquisitions and strong partnerships, LB is positioned for significant long-term growth, supported by favorable market conditions.

- New Technologies/Industrial Development: LB is in a great spot to benefit from strong data center demand, crypto mining, solar/wind energy production, hydrogen production, and other opportunities.

- Dividends: Although we know little about its dividend plans, we are likely looking at a dividend announcement in the months ahead.

Cons:

- Young Company: LB is still in its early stages, with a limited operating history, making its future performance more uncertain compared to established peers.

- Leverage Risk: Although the company is reducing debt, a slower-than-expected decline in its debt could delay dividend payments.

- Unproven Dividend: LB hasn't yet initiated a dividend, which might be an issue for income-focused investors.

- Market Dependency: LB's success is closely tied to the health of the oil, gas, and water markets in the Permian Basin, making it vulnerable to sector-specific downturns.

Comments