Summary

- With potential rate cuts looming, trillions may shift from money markets to dividend stocks, creating new opportunities for investors seeking higher returns.

- Three standout investments offer strong yields, resilient business models, and solid growth potential, making them appealing for income and capital gains.

- Positioning now in these investments could be beneficial as market dynamics shift, offering a chance to capitalize on a changing economic landscape.

Dmitri Kalvan

Introduction

In June, I wrote an article titled "Here Are 4 Fantastic Dividends Yielding 6% To Avoid The 'Cash Trap.'" In that article, I explained that dividend stocks could benefit from trillions of new inflows if the Fed were to lower rates.

As most of you may know, because of aggressive interest rate hikes after the pandemic, investors were suddenly able to park their money in low-risk, high-yield investments like short-term bonds.

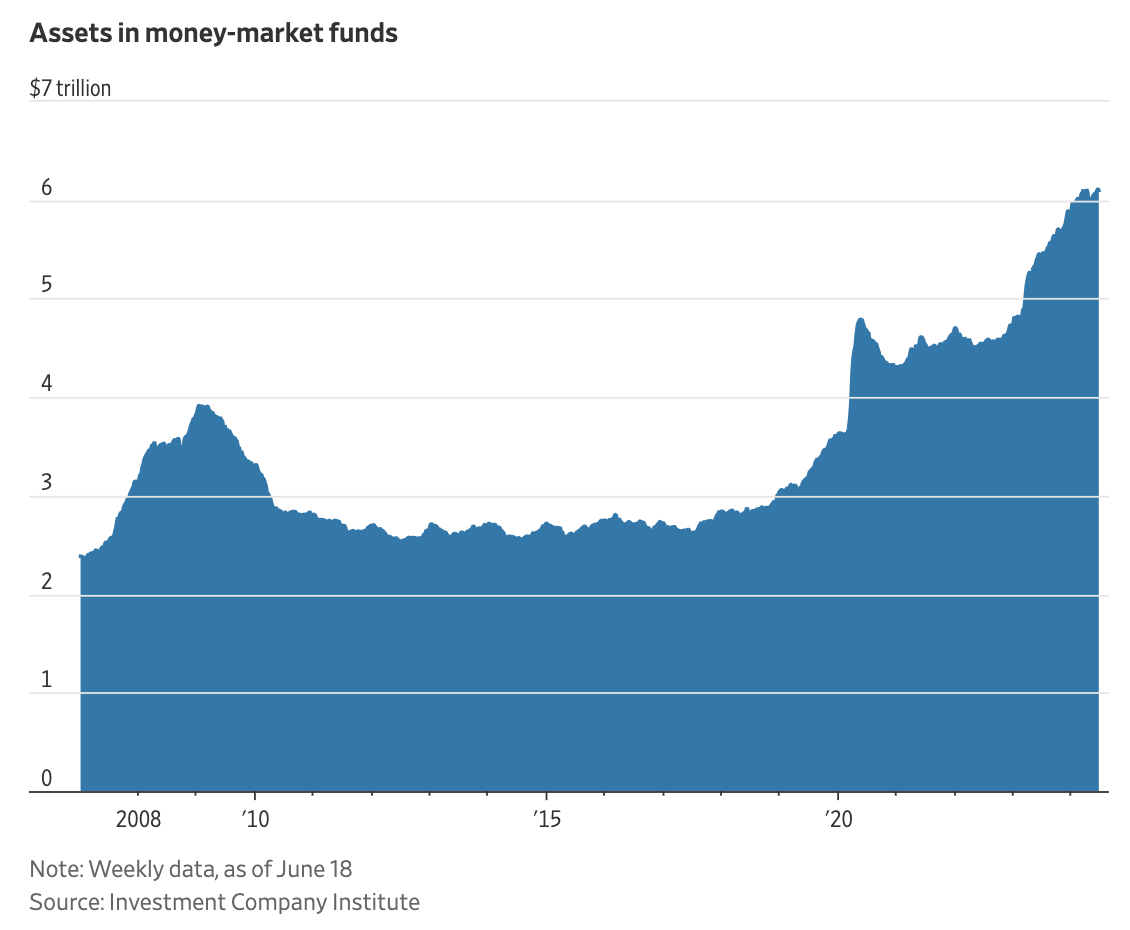

As of June 18, assets in money market funds had ballooned to more than $6 trillion, up from less than $4 trillion before the pandemic hit.

The Wall Street Journal

The chart above also shows a sideways trend in money market assets between 2010 and 2021. During this period, rates were low. This was beneficial for dividend stocks. After all, when government bonds do not offer a decent yield, investors need to look for yield in other places.

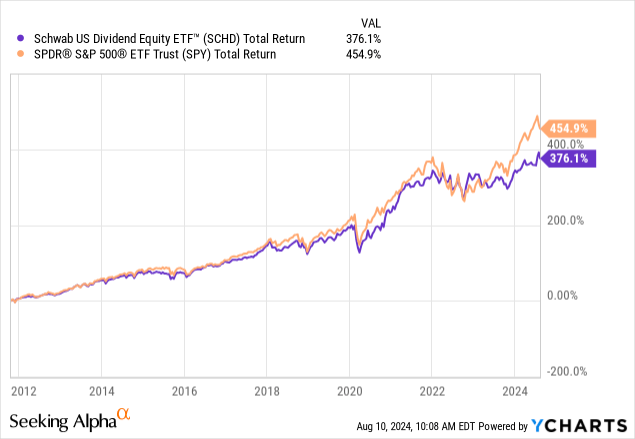

As a result, the Schwab U.S. Dividend Equity ETF (SCHD) saw roughly 200% in total returns between its 2011 launch and 2020 - almost the same return as the S&P 500, which benefitted from elevated tech exposure. Including post-pandemic years, the SCHD ETF has returned close to 380%, which is an impressive result.

Data by YCharts

Data by YCharts

With that said, although I expect interest rates to remain "above average" on a prolonged basis, we are likely working our way to a scenario where rates will come down from current levels.

One reason is deteriorating economic conditions.

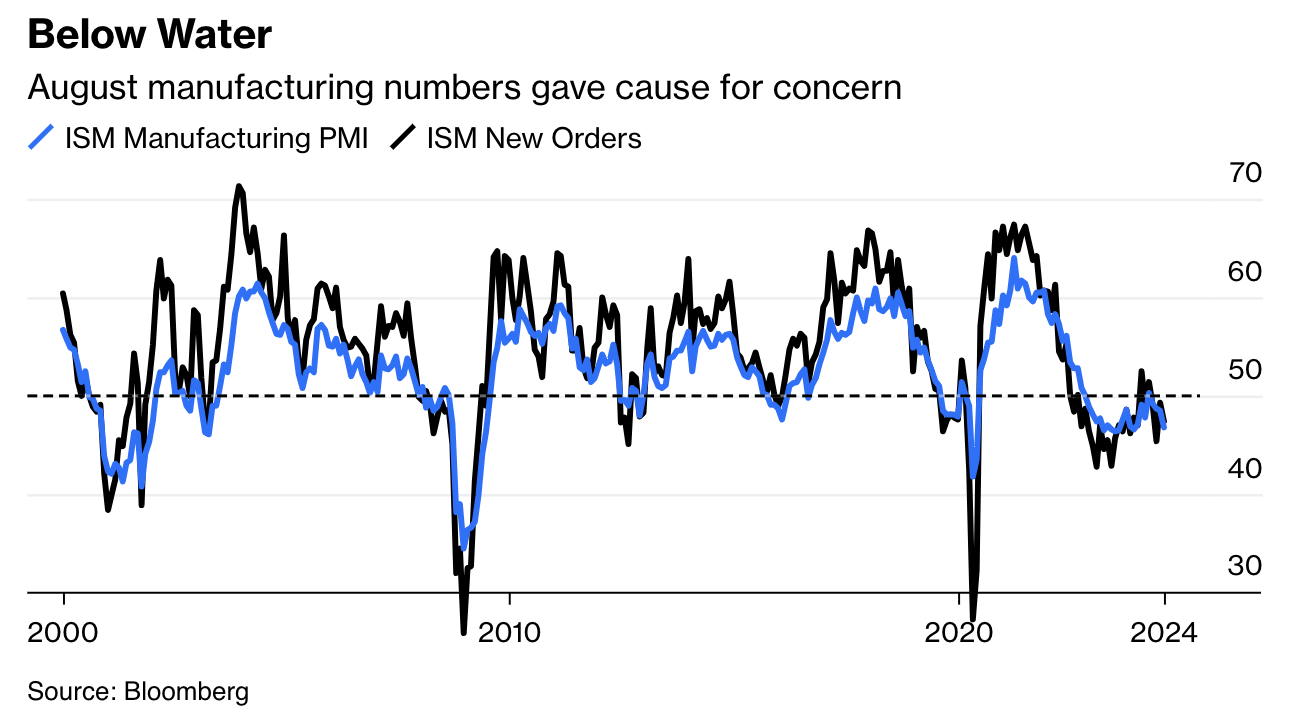

Leading indicators like the ISM Manufacturing Index and its important new orders component are indicating elevated risks of a manufacturing recession.

Bloomberg

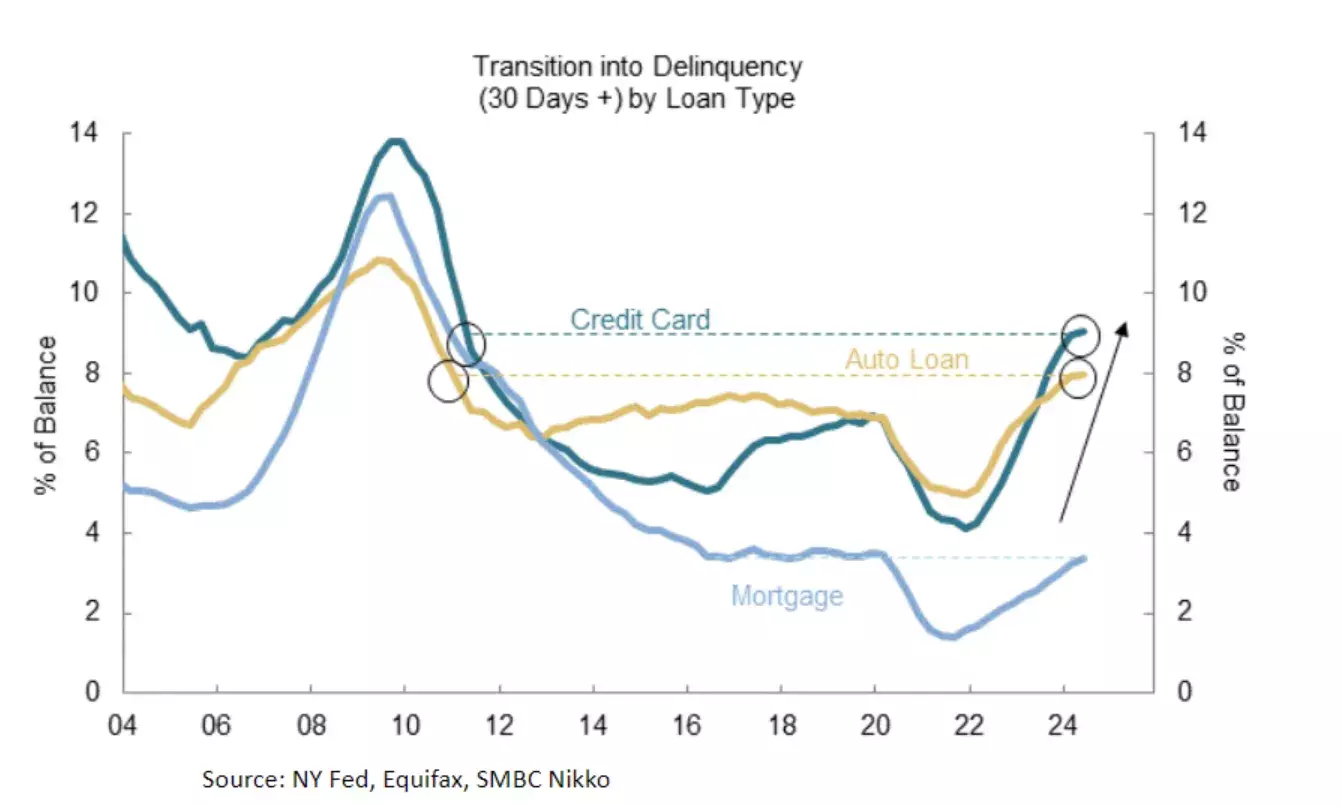

Moreover, because of elevated rates and sticky inflation, debt quality is falling.

While mortgage delinquencies are back at pre-pandemic levels, auto loans and credit card debt haven't been this risky since 2010.

Federal Reserve Bank of New York

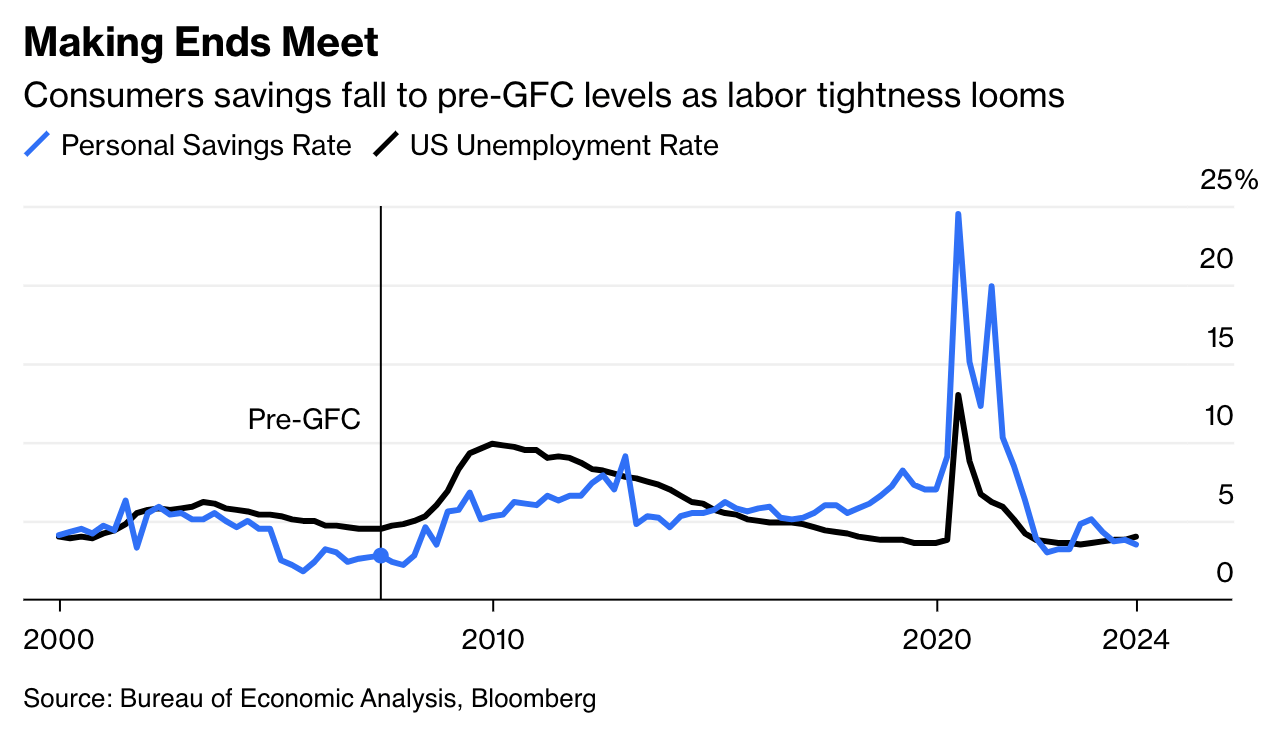

It also does not help that consumers are, more or less, "out of savings" while the unemployment rate is slowly creeping up.

Bloomberg

Interestingly enough, Bloomberg wrote that Bank of America makes the case we shouldn't worry about this until affluent consumers start to weaken.

Is there a cause for alarm? Using proprietary models, researchers at Bank of America argue that US financial conditions are within normal historical ranges. While rising unemployment and delinquencies are feared to put pressure on low-income consumers, BofA's researchers argue that the more affluent should be the focus. The downside risk to personal consumption would come from large asset price declines [...] - Bloomberg

I tend to partially agree with that for one major reason; the poorest consumers have been in a bad spot since 2021. When inflation became an issue, people without investments were pressured by inflation without having the benefit of seeing their stocks go up in value. As harsh as this may sound, these consumers have not been very relevant to the stock market.

Now, it seems the middle-class consumer is starting to struggle. I'm getting that from countless earnings reports, as even companies like McDonald's (MCD) are reporting weaker consumers.

"Rich" consumers are still benefitting from their assets, as even risk-free bonds still pay more than some dividend stocks. In an economy that has gotten used to the poor being poor and the rich being able to spend, it needs more weakness to trigger a recession.

The purpose of this article is not to frighten people into thinking that we are heading for a severe recession. Rather, it is to suggest that we may be moving towards a situation where lower interest rates are necessary to protect the economy.

This could lead to investors looking for higher returns in alternative areas. As trillions of dollars begin to shift, I want to be ready for it.

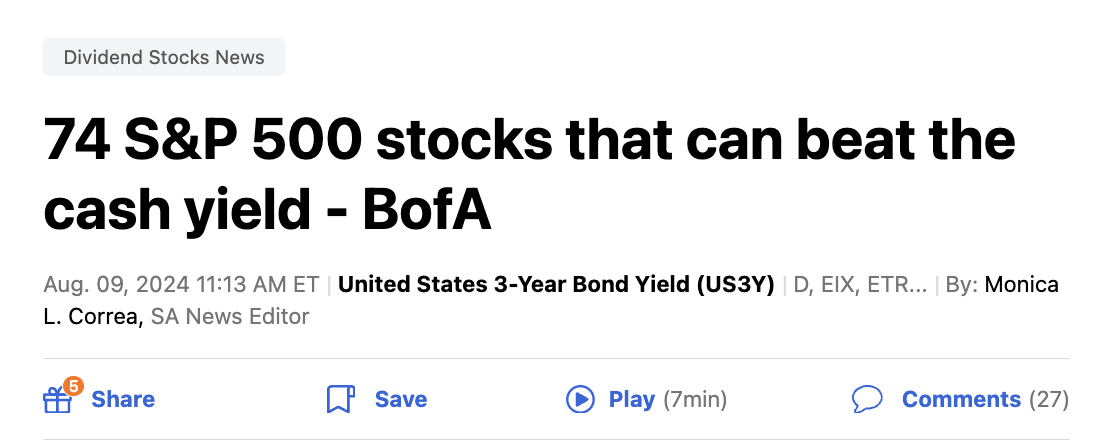

With that said, on August 7, Seeking Alpha reported that Bank of America had found 74 S&P 500 stocks that are expected to beat the cash yield. In this case, the "cash yield" is the three-year U.S. treasury yield, which is a great proxy for risk-free short-term income.

Seeking Alpha

Three of these investments stood out to me, as I have covered all of them before. I also believe that these companies offer a great risk/reward for income and capital gains for a wide range of investors - not just investors looking for income.

Altria (MO) - Smoking Is Cool Again!

The title is sarcasm. Don't smoke!

All kidding aside, Altria is a red-hot stock again.

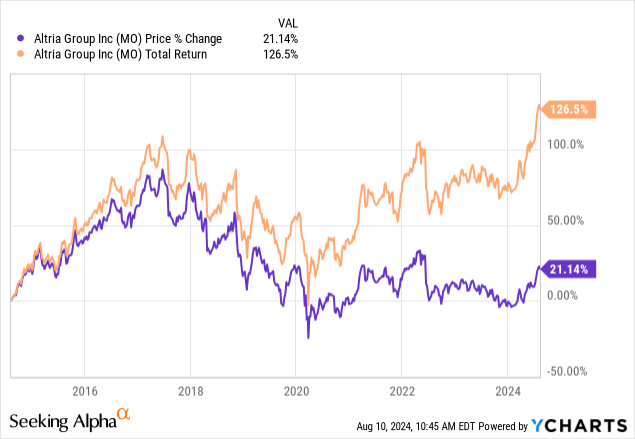

If we include its dividend, the total return of Altria is back at an all-time high, after an impressive rally this year.

Data by YCharts

Data by YCharts

Excluding dividends, Altria is up 25% year-to-date!

With an 8% yield, Altria is one of the best places to get a super high yield without elevated financial risk. Altria is not a complex financial company with elevated risks of a dividend cut.

As almost everyone will know, Altria sells Marlboro cigarettes in the United States - among other products like non-smoke products.

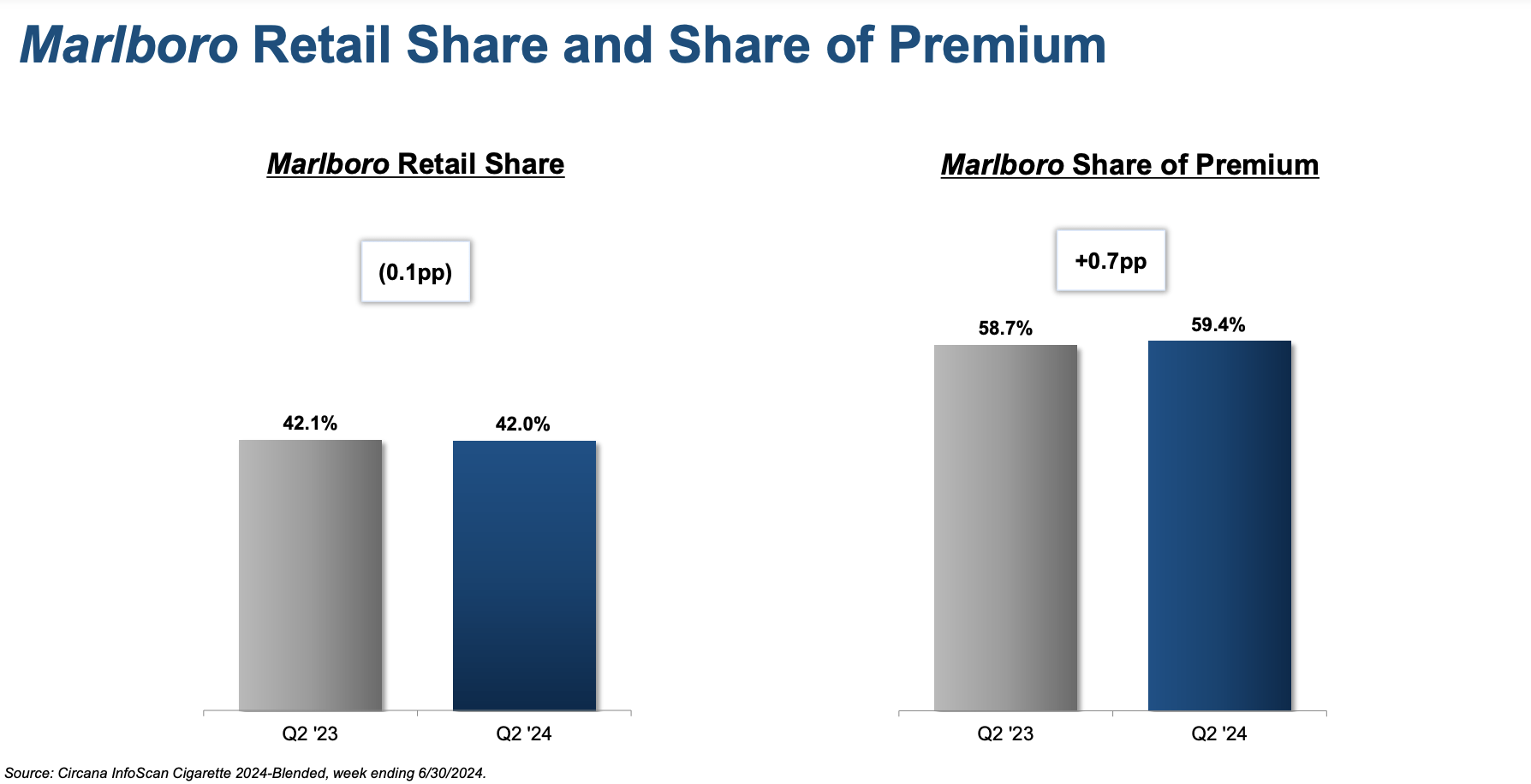

Although cigarette volumes have been in a long-term downtrend, the company is growing its market share. In 2Q24, Marlboro reached a 59.4% market share in the premium segment, up 0.7 points compared to 2Q23.

Altria

Meanwhile, in the oral tobacco segment, shipments of its popular "on!" product are up 37.3% year-on-year, outperforming 9% industry volume growth by a wide margin.

On top of that, its non-combustible NJOY decide has a 25.4% market share in the U.S., up from 11.6% in the first quarter of this year. Shipments of devices rose by 80%, with consumables rising by 15%.

Sure, the company will not turn into a growth stock anytime soon - or maybe ever. However, that does not matter. All MO needs to do is support its 8% dividend yield and maintain low-digit EPS growth to grow its dividend over time.

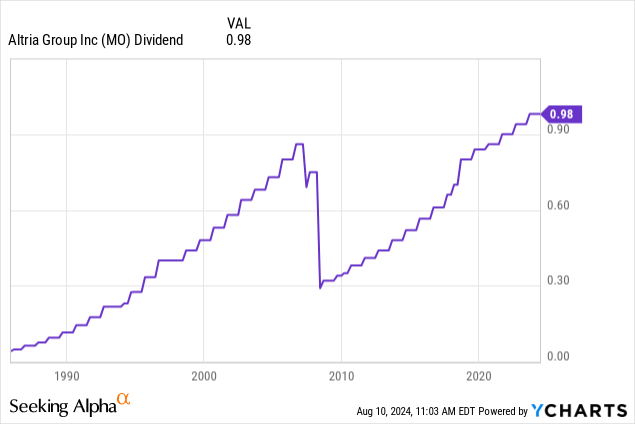

Currently yielding 7.8%, the dividend has an 80% payout ratio and a five-year CAGR of 4.1%. It has hiked its dividend for 54 consecutive years. The decline in the chart below shows the Philip Morris (PM) spin-off. This is NOT a dividend cut.

Data by YCharts

Data by YCharts

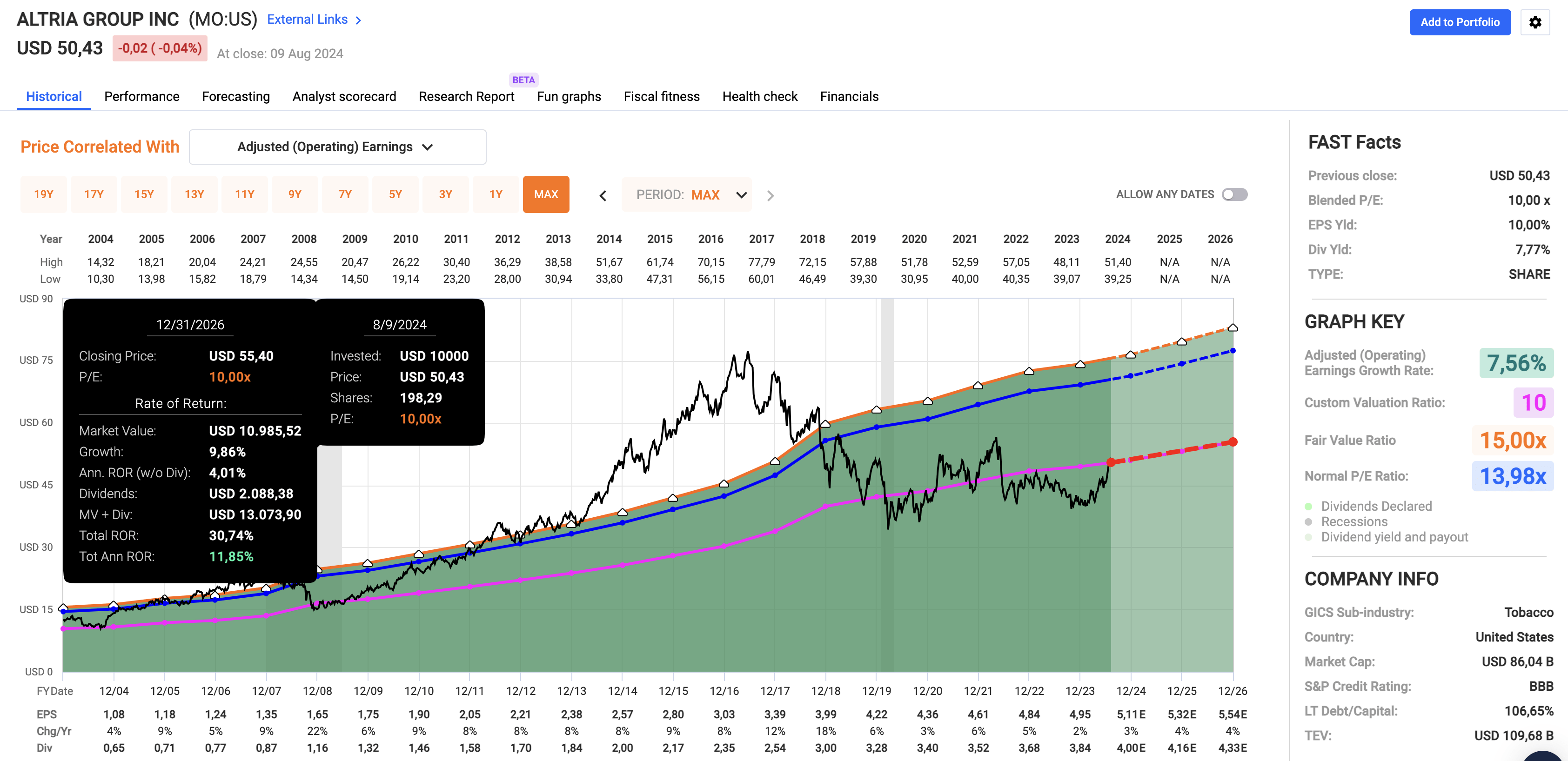

Valuation-wise, the stock is cheap. Trading at a blended P/E ratio of 10.0x, it trades roughly four points below its long-term average. Moreover, going forward, analysts expect 3-4% annual EPS growth, which is good news.

FAST Graphs

If we combine expected EPS growth with its yield, MO could return 10-12% per year at its current valuation(!). Any valuation benefits could propel that number much higher.

I expect that to happen once rates come down, making MO a fantastic high-yield play.

Kinder Morgan (KMI) - High-Yield Pipeline Income

I love pipelines.

As I wrote in a recent article on Canada's midstream giant Enbridge (ENB), pipelines are slowly getting full, reducing demand risks for pipeline operators.

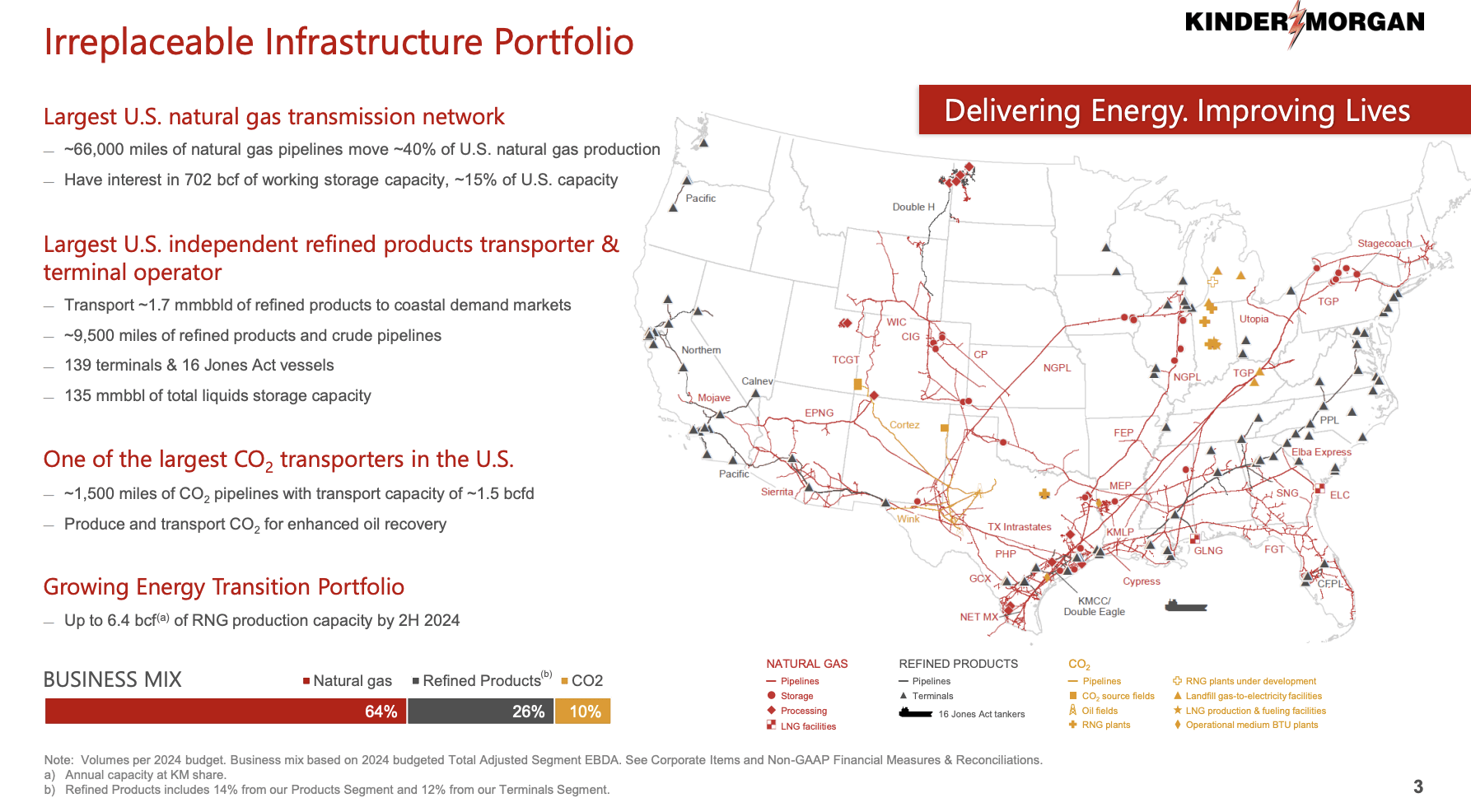

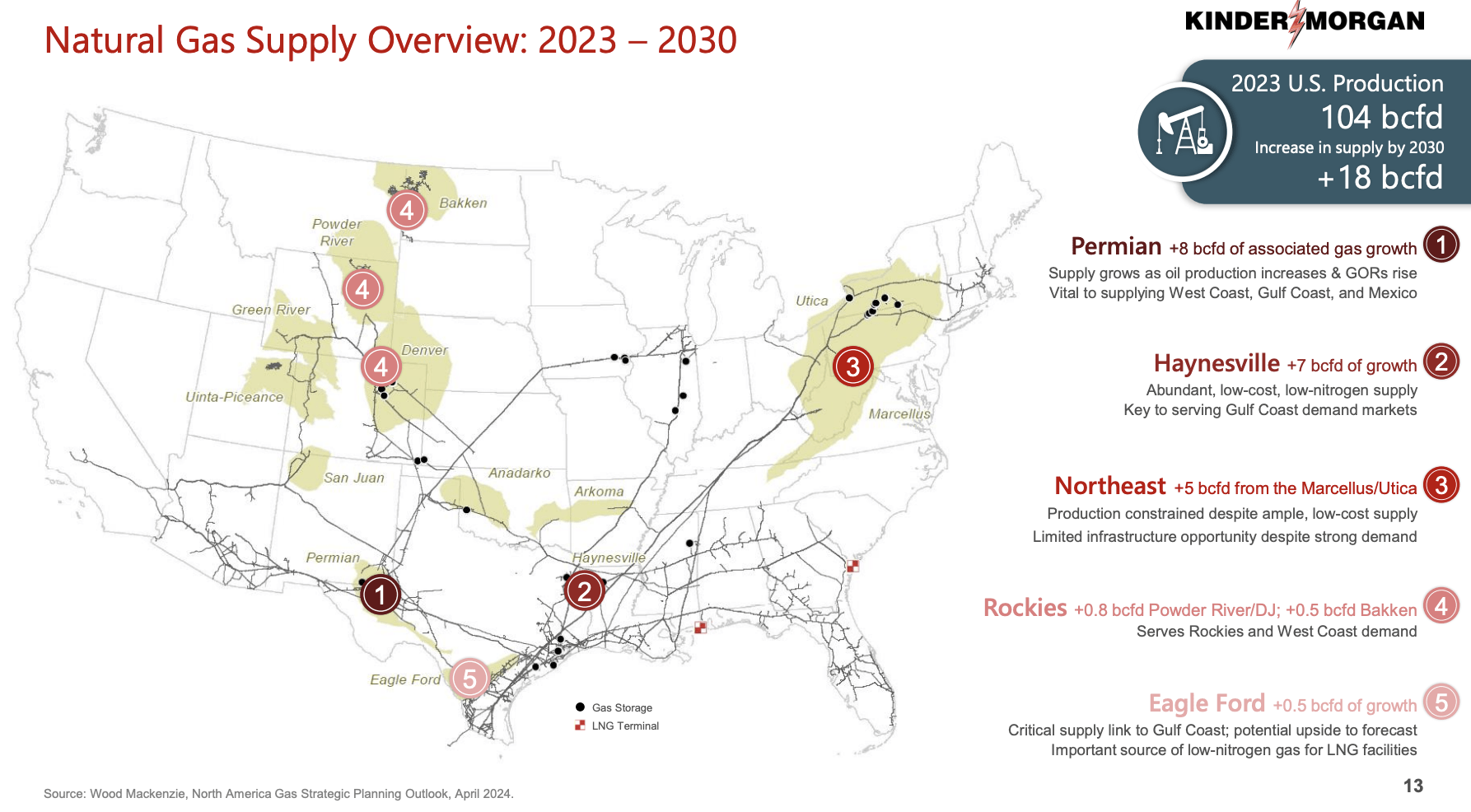

Kinder Morgan is one of America's biggest midstream companies. It owns roughly 66 thousand miles of natural gas pipelines that move 40% of domestic natural gas production. This makes KMI a "mission-critical" player.

It also ships refined products and generates a tenth of its revenue in its CO2 pipeline segment. It also owns export terminals, 16 Jones Act vessels, and an interest in more than 700 billion square feet of natural gas storage.

Kinder Morgan

89% of the company's revenues have take-or-pay contracts, which means customers have to pay even if they don't use the pipelines. It's like paying for a rental car, even if you park it in your garage for a week without driving it.

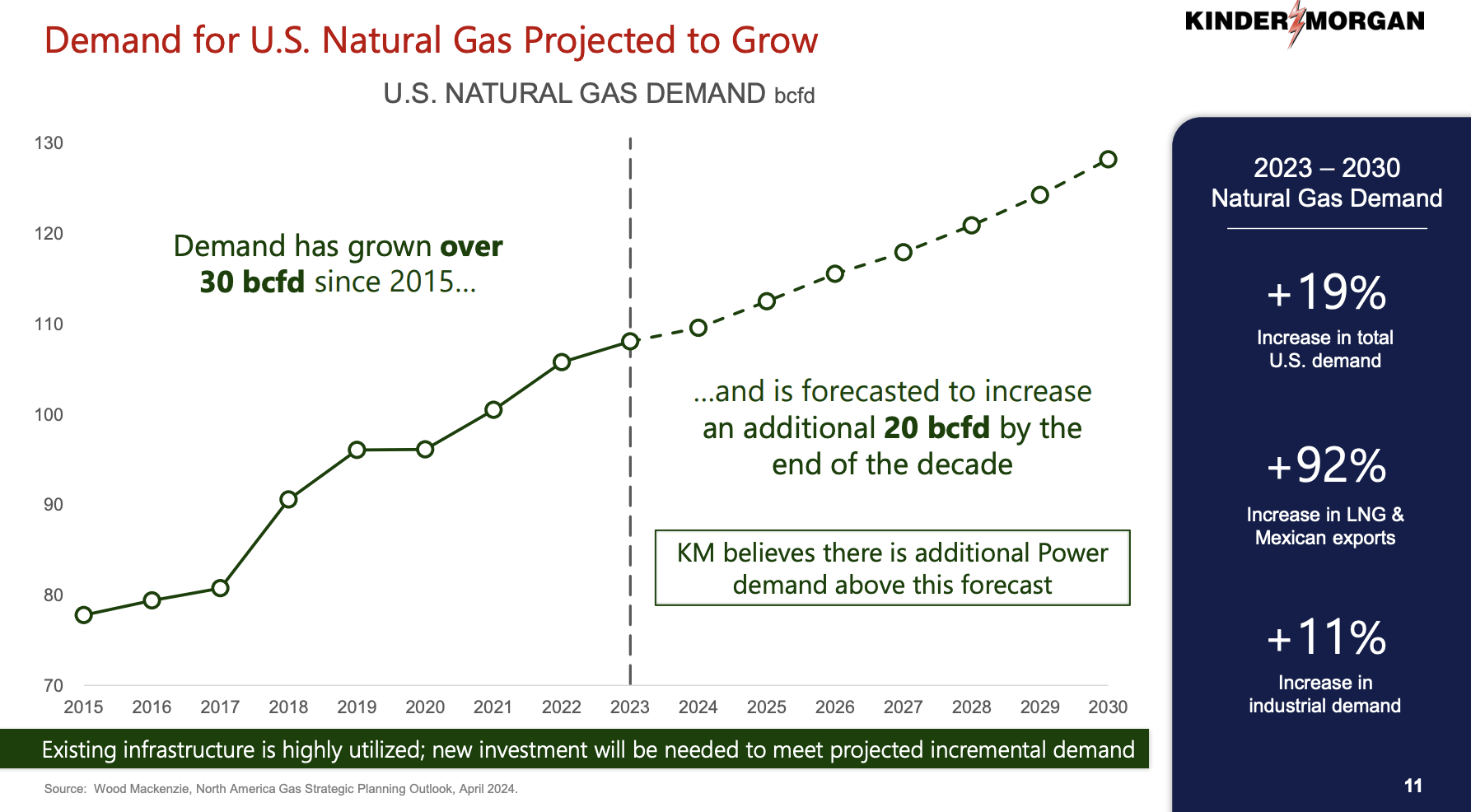

Currently, the company's pipeline utilization rate is 87%. That number was 73% in 2016. Going forward, that number is expected to rise further, as natural gas demand in the U.S. (and abroad) is exploding. By 2030, KMI expects natural gas demand to be 19% higher, with almost 100% growth in LNG and Mexican exports.

Kinder Morgan

Especially in light of the declining quality of the U.S. shale production (higher associated gas production) and secular growth tailwinds like data centers, I am super bullish on the future of natural gas-focused midstream players.

Kinder Morgan

Although I completely understand it if some investors are disappointed in KMI for cutting its dividend in the past, I believe the current KMI company is different.

Data by YCharts

Data by YCharts

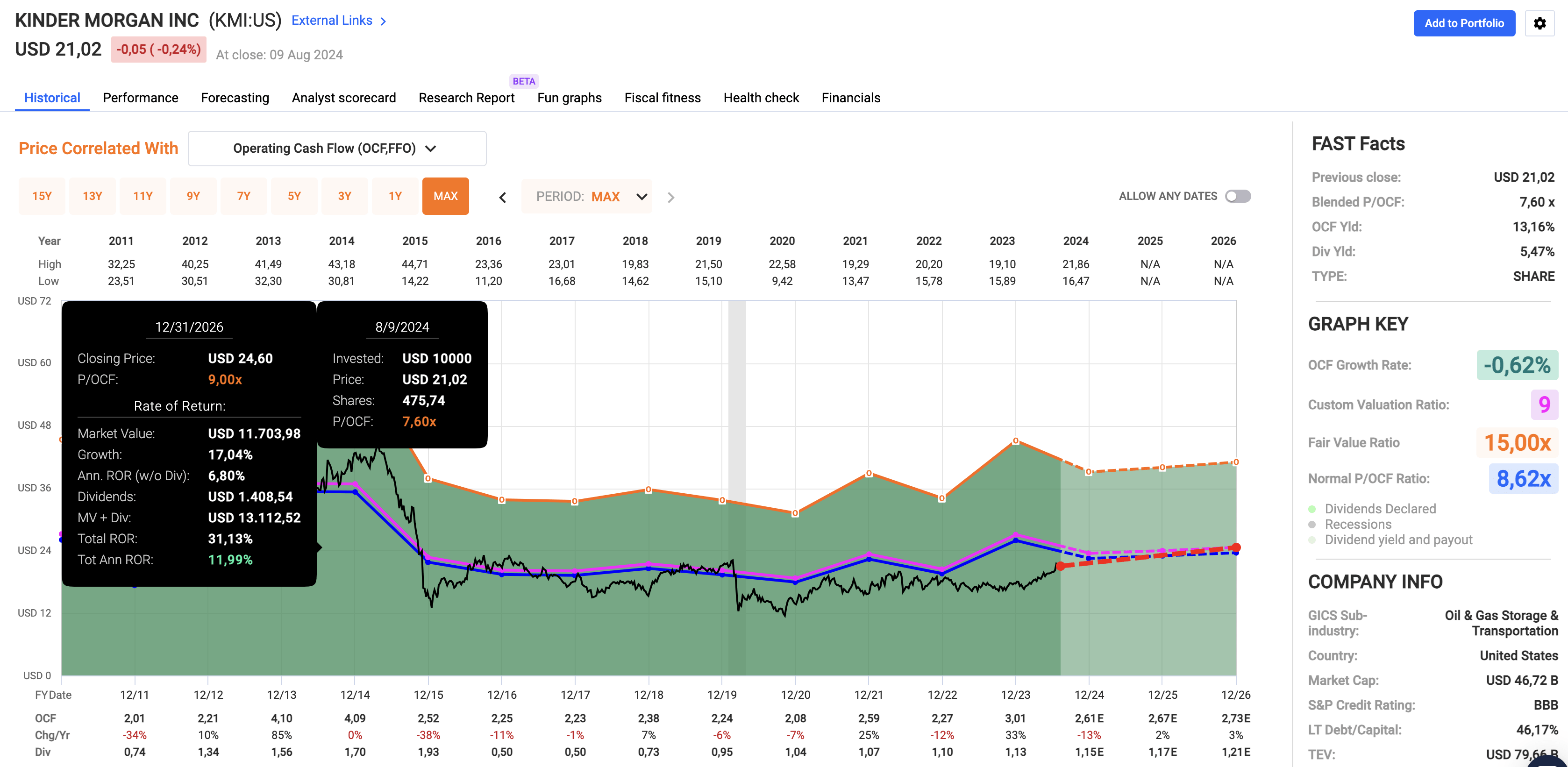

Currently, KMI trades at a 5.5% yield and is expected to grow its operating cash flow by 2-3% per year through 2026. Using a 9x operating cash flow multiple paves the way for 10-12% in annual expected returns, similar to Altria.

FAST Graphs

The next stock also comes with a very anti-cyclical business model.

Mid-America Apartment Communities (MAA) - Let The Landlord Pay You

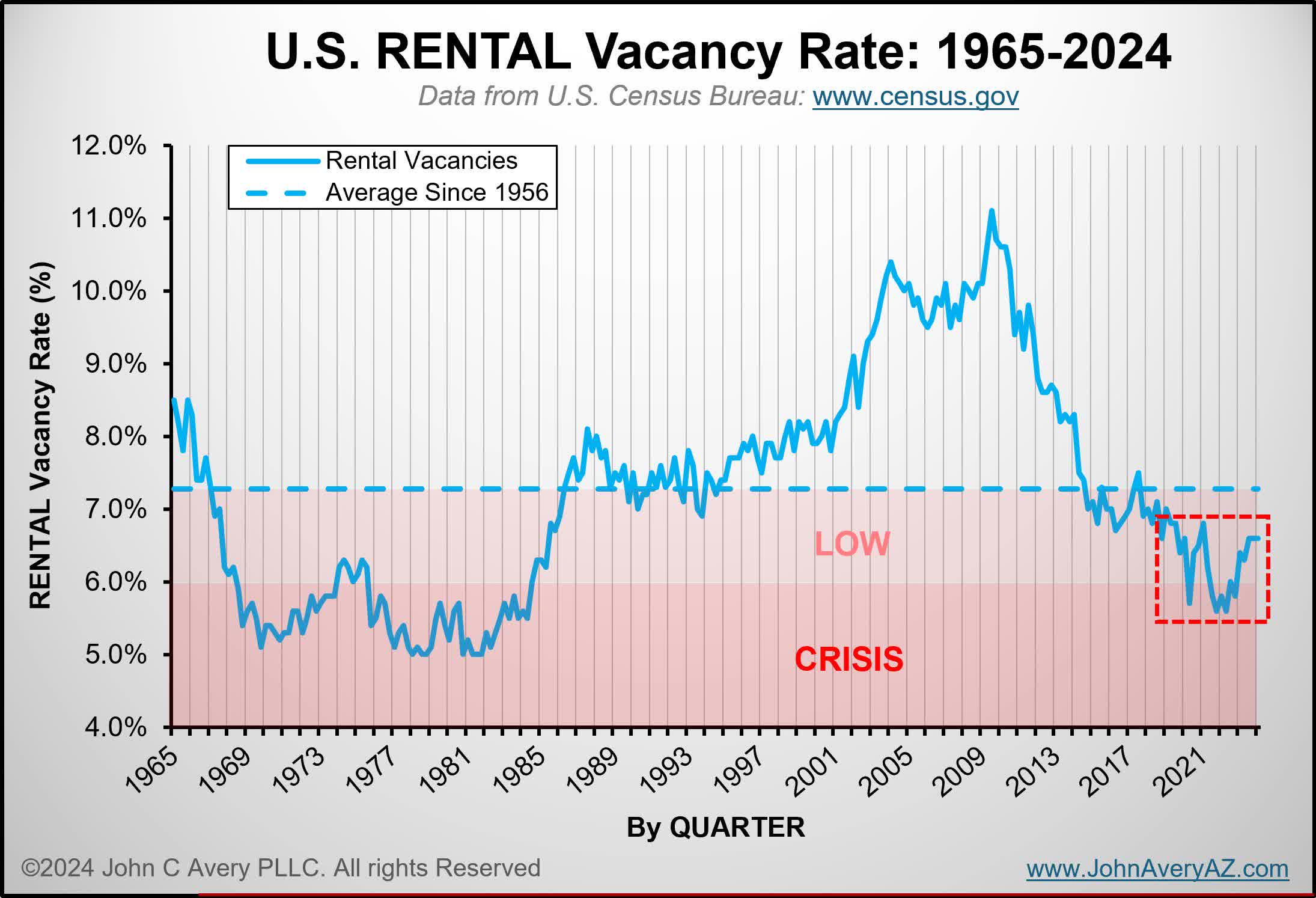

When it comes to housing, the rental market in the United States is red-hot. That makes sense, as the rental vacancy is very low. Shortly after the pandemic, vacancies were in "crisis" territory.

John C. Avery

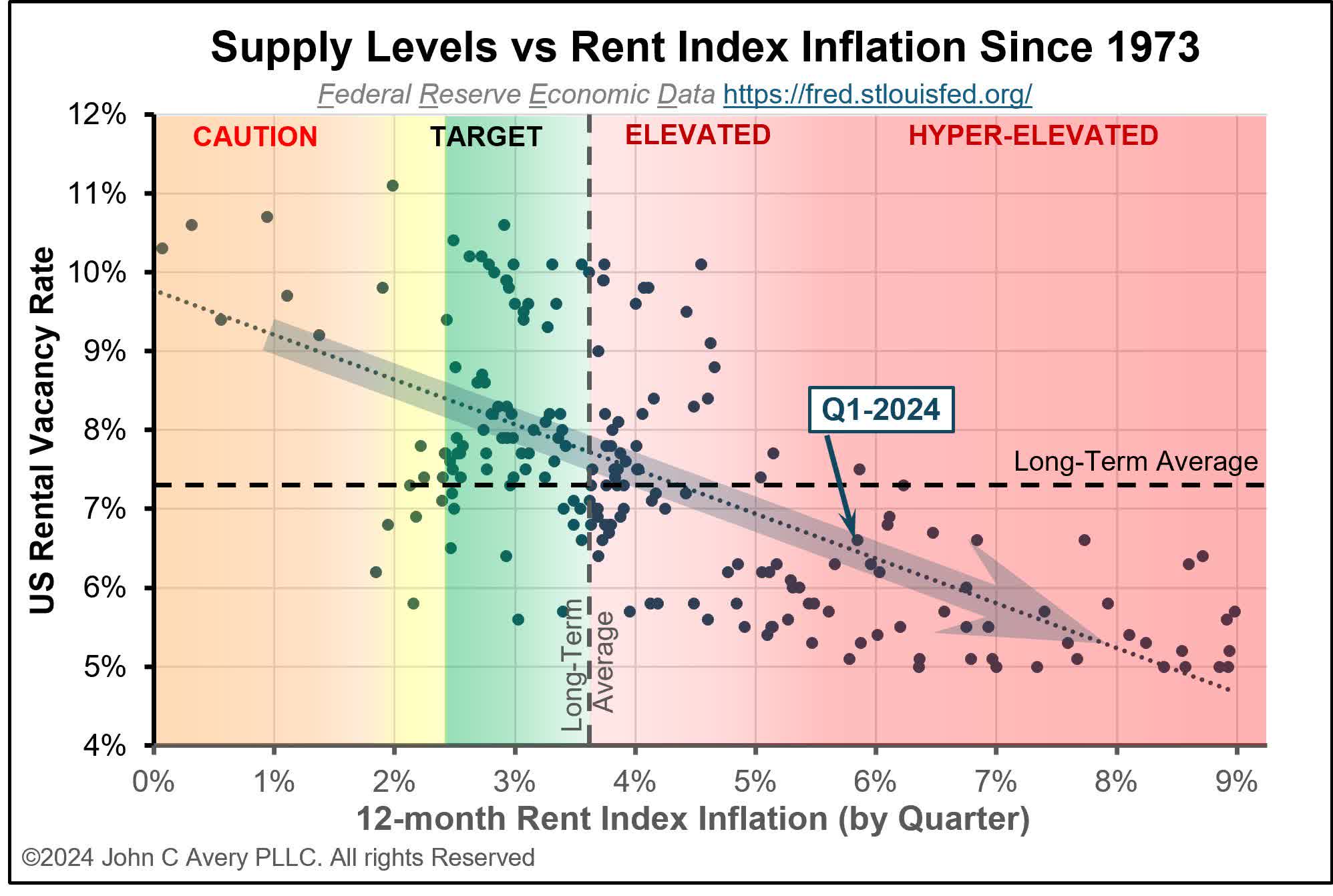

As Economics 101 teaches us, when supply is limited and demand is strong, prices tend to go up. As we can see below, vacancy rates below 7% tend to cause 4-9% annual rent inflation. Once vacancy rates rise above 7%, the odds of sub-3.5% rent inflation start to rise.

John C. Avery

That's where Mid-America Apartment Communities comes in.

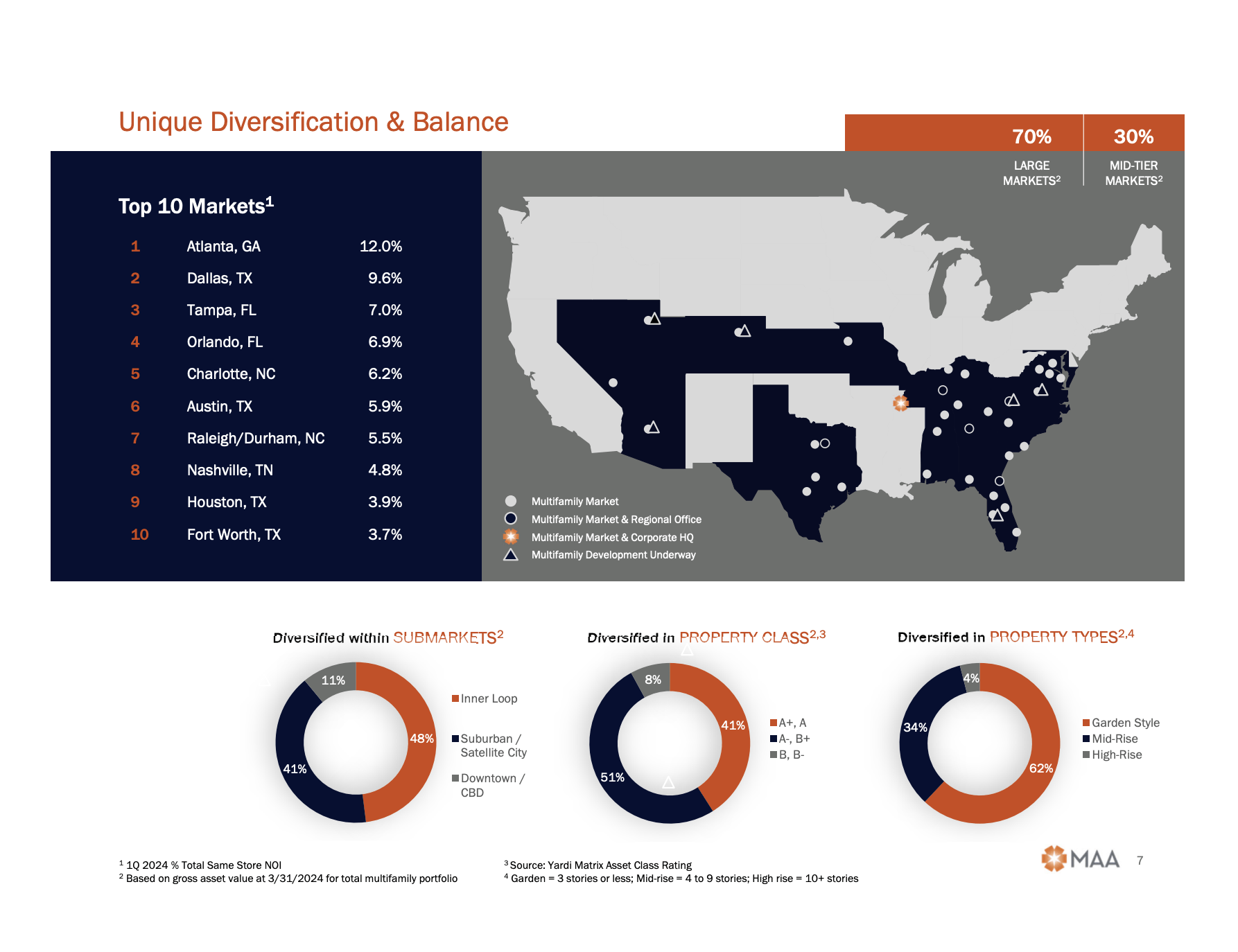

This S&P 500 member has been a public company for 30 years. Since then, it has paid 121 quarterly cash dividends and built a portfolio of more than 102 thousand apartment units.

Most of its assets are in Sunbelt states (excluding California), with a focus on high-growth markets in Texas, Florida, Georgia, and the Carolinas. These markets tend to come with superior population growth, an influx of new businesses, and looser regulations.

Mid-America Apartment Communities

Furthermore, what sets MAA apart is the fact that the median age of its tenants is 35 years old. 80% of these tenants are single. The average income is $88 thousand, bringing the average rent/income ratio to just 22%, roughly ten points below the nation's average.

This brings a lot of safety to the table.

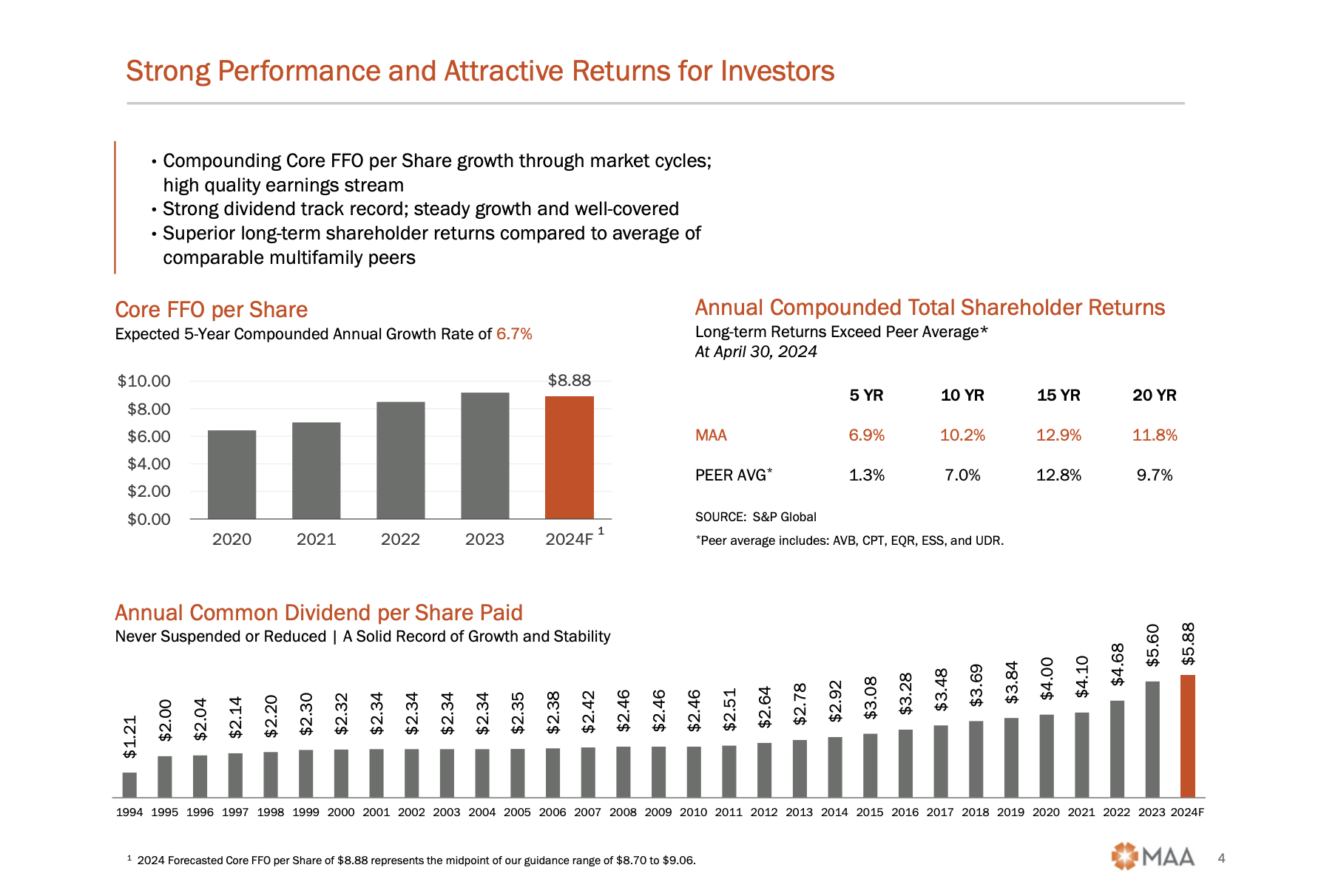

Currently yielding 3.8%, the company has a 2024E AFFO payout ratio of 72% and a track record without any dividend cuts - even during the Great Financial Crisis.

Even better, over the past 20 years (ending April 30, 2024), its shares have returned 11.8% per year, beating its peers by more than 2 percentage points per year.

Mid-America Apartment Communities

Its five-year dividend CAGR is 8.9%.

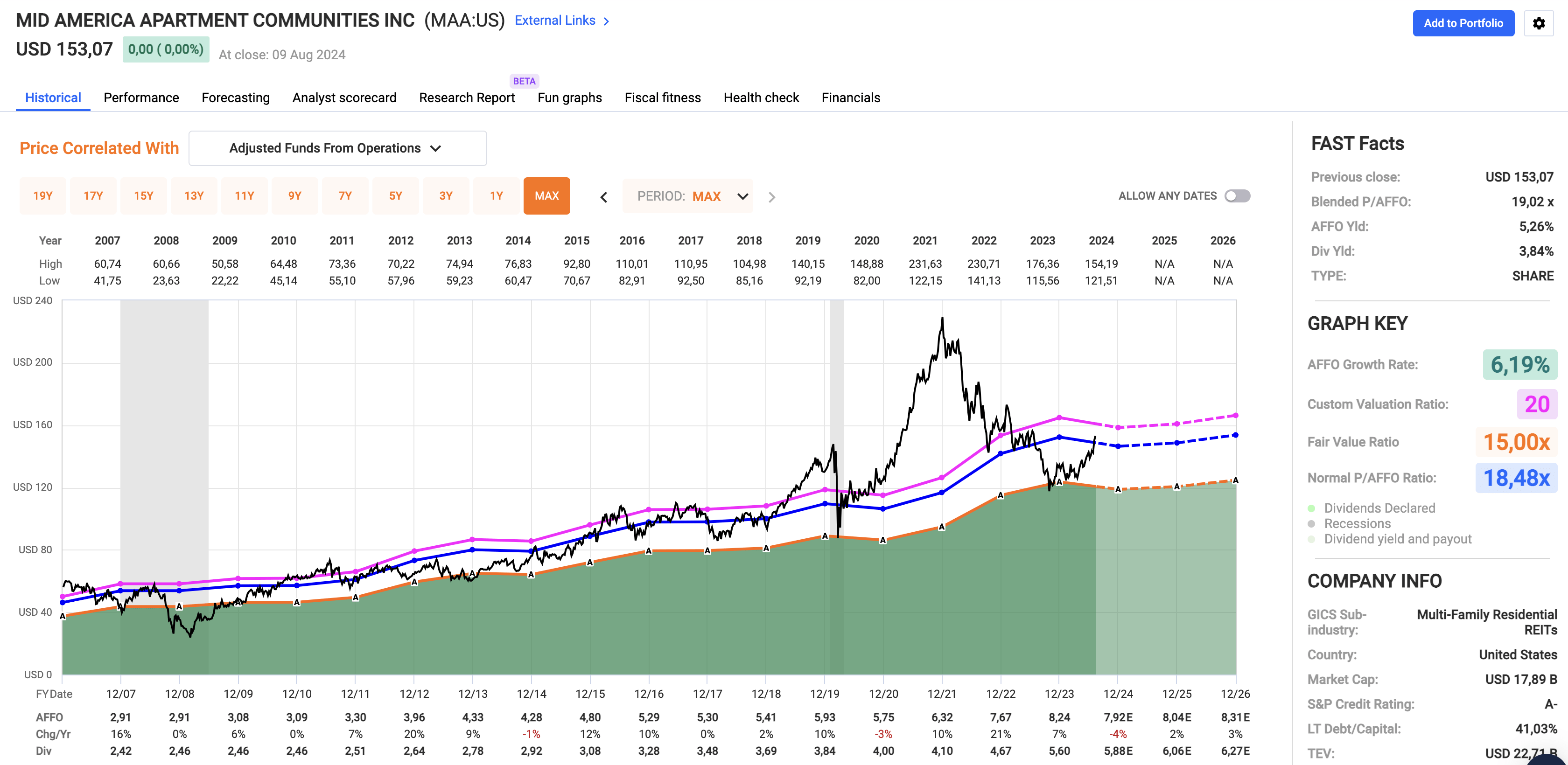

With regard to its valuation, the company, which has a healthy credit rating of A- from S&P Global, is expected to grow its per-share adjusted funds from operations by 2-3% per year after 2024. Personally, I expect these numbers to be substantially higher if the Fed is forced to cut. Lower rates would be bullish for rents and home prices, and likely warrant a higher multiple than its 18.5x AFFO average since 2007.

FAST Graphs

As such, I expect MAA to return 8-10% in a "base case" scenario, with more upside if the rental market sees a second wave of inflation.

Takeaway

As economic indicators suggest potential rate cuts ahead, we're likely on the brink of a significant rotation of trillions from money markets and similar investments back into dividend stocks.

Based on this context, Altria, Kinder Morgan, and Mid-America Apartment Communities offer compelling opportunities with their high yields, resilient business models, and solid growth potential.

These investments are well-positioned to attract inflows as investors seek higher returns, making them strong candidates to secure income and capitalize on the shifting market landscape.

I believe positioning ourselves strategically now could pay off as this rotation unfolds.

Hence, I will continue to focus on this topic in the weeks and months ahead.

Comments