Summary

- Texas Pacific Land Corporation is a misunderstood company with a near-perfect business model.

- TPL owns land in the Texas Permian, generating high margins from oil and gas royalties and water services.

- The company's strategic location in the Permian Basin allows for additional revenue streams such as sand sales and potential data centers.

Joey Ingelhart

Introduction

It's time to talk about my largest investment - ever.

After keeping my eye on the company for a while, I finally pulled the trigger earlier this year, putting almost my entire war chest I had been building into the Texas Pacific Land Corporation (NYSE:TPL), a company that now accounts for 13% of my portfolio.

My most recent article on this company was written on May 11, when I went with the title "Texas Pacific Land: I'm So Bullish It Hurts."

Since then, shares have risen by more than 35%, pushing my return to almost 50%, which is one of the reasons why it's such a heavyweight in my portfolio.

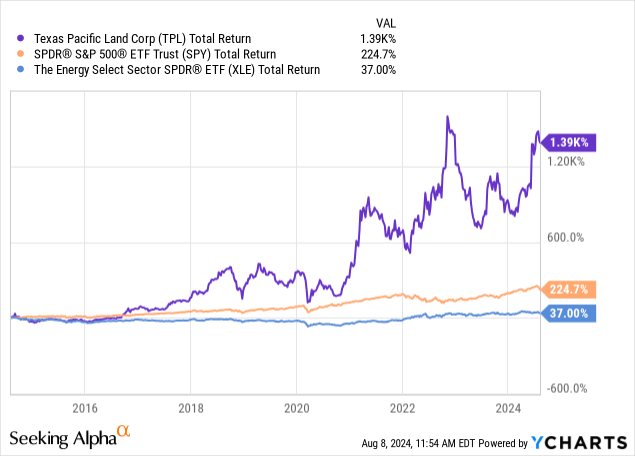

Over the past ten years, TPL has returned 1,390%, beating the 225% return of the S&P 500 by a wide margin. The energy ETF (XLE), returned just 37%.

Data by YCharts

Data by YCharts

In light of its just-released 2Q24 earnings, I'll use this article to update my thesis and explain why I'm far from finished buying this Texas landowner.

So, as we have a lot to discuss, let's keep this intro short and get right to it!

A Near-Perfect Business Model

Respectfully, I have to say that Texas Pacific Land is one of the most misunderstood companies on the market. I was one of the people who underestimated just how powerful the TPL business model is until I spent days digging through its business model.

For starters, Texas Pacific's roots go back to 1888, when it was organized as a trust to manage the property of the Texas and Pacific Railway Company that went bankrupt. That explains its name.

Texas Pacific Land Corporation

The biggest advantage of this land is its location.

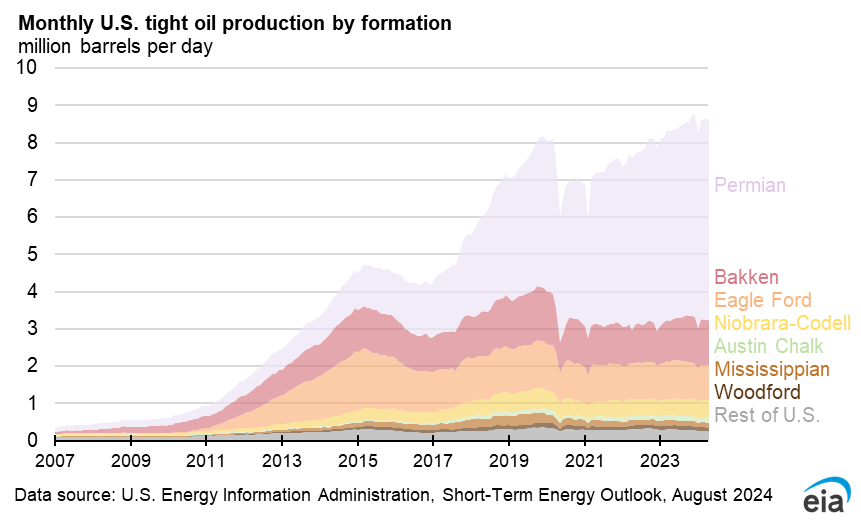

The company's 869,000 surface acres include close to 24,000 core royalty acres in the Texas Permian. The Permian is the most important oil basin in the United States. As we can see below, it's both the engine of the shale revolution and the only basin with consistent growth.

Energy Information Administration

Even better, two years ago, Bloomberg visualized that the Permian is far from peaking, as just 37% of its wells had been developed by then. Two years later, that number will likely be higher. However, the strategic advantage is still very valid.

Bloomberg

On top of that, the Permian has a major global influence. The Permian alone is larger than the entire oil production of nations like Iraq, Iran, the UAE, Kuwait, and Nigeria. It also produces more natural gas liquids than Russia.

Texas Pacific Land Corporation

With that in mind, the company does NOT produce oil and gas.

The company owns land, with three benefits:

- Surface rights.

- Water rights.

- Oil and gas royalties.

If we exclude LandBridge Company LLC (LB), which just went public, it's the only major royalty company in the United States that owns water and surface rights on top of the right to make money on oil and gas production.

Texas Pacific Land Corporation

Instead of producing its own oil and gas, Texas Pacific Land lets others do the job. This includes Exxon Mobil Corporation (XOM), EOG Resources, Inc. (EOG), Occidental Petroleum Corporation (OXY), Devon Energy Corporation (DVN), and many others.

These companies are not competitors but customers/tenants, or whatever we call their obligation to pay TPL for every barrel of oil, gas, and NGL they extract from the ground.

Texas Pacific Land Corporation

Although this takes away TPL's ability to influence production volumes (that's up to its tenants), it has one major benefit: TPL enjoys a 25% royalty, while oil and gas producers have to deal with capital costs, operating expenses, and a wide range of other costs.

Texas Pacific Land Corporation

As a result, TPL is one of the highest-margin companies on the market. In 2023, it had a net income margin of 64%, which makes it a standout, as most S&P 500 members have net income margins between 5-20%.

On a side note, please note that TPL is not an S&P 500 member. It will be added to the mid-cap S&P 400.

Texas Pacific Land Corporation

Additionally, the company has surface and water rights.

That's where the fun begins!

As the company reiterated during its 2Q24 earnings call, one of its most compelling features is the fantastic performance of its Water Services and Operations segment.

In 2Q24, the company set records across every major water performance indicator, including water sales revenues, volumes, and produced water royalties.

See, oil production is all about water.

- Water is required in the production process of oil and gas, as a mixture of water and chemicals is pumped into the ground to extract oil and gas.

- The production of oil and gas also produces water. This water is toxic and needs to be taken care of. For example, the Delaware Basin (part of the Permian) is water-heavy, as every barrel of oil comes with up to four barrels of produced water.

Texas Pacific Land Corporation

According to the company, with an average water sales volume of 800,000 barrels per day, the company's infrastructure is perfectly positioned to meet the growing demand for both brackish and recycled water, driven by advanced completion techniques like simul-frac and co-completions used by top-tier customers like Exxon, Conoco, and BP.

Texas Pacific Land Corporation

In other words, as companies drill deeper and boost production, the demand for water services grows rapidly.

Moreover, the company makes money from other operations, including sand sales (for fracking), pipelines, and other operations on its land, including (potential) data centers, solar, wind, and others.

After all, the Permian has major benefits:

- Very cheap energy. In some areas, natural gas production growth is so strong that prices are negative. So-called associated natural gas is an increasing issue due to maturing oil and gas reserves. This benefits data centers, hydrogen production, crypto mining, and other operations.

- The land is mostly remote. The Permian isn't home to many people.

- Unregulated transmission lines make it easier to build data centers.

- The fact that the Permian has too much water provides a lot of cooling water for data centers.

This means the Permian is increasingly important for other operations. It could even be a hotspot for data centers and new, energy-intensive technologies.

While TPL has not yet commented on concrete plans for data centers, it has been working on plans to turn its water business into something even bigger.

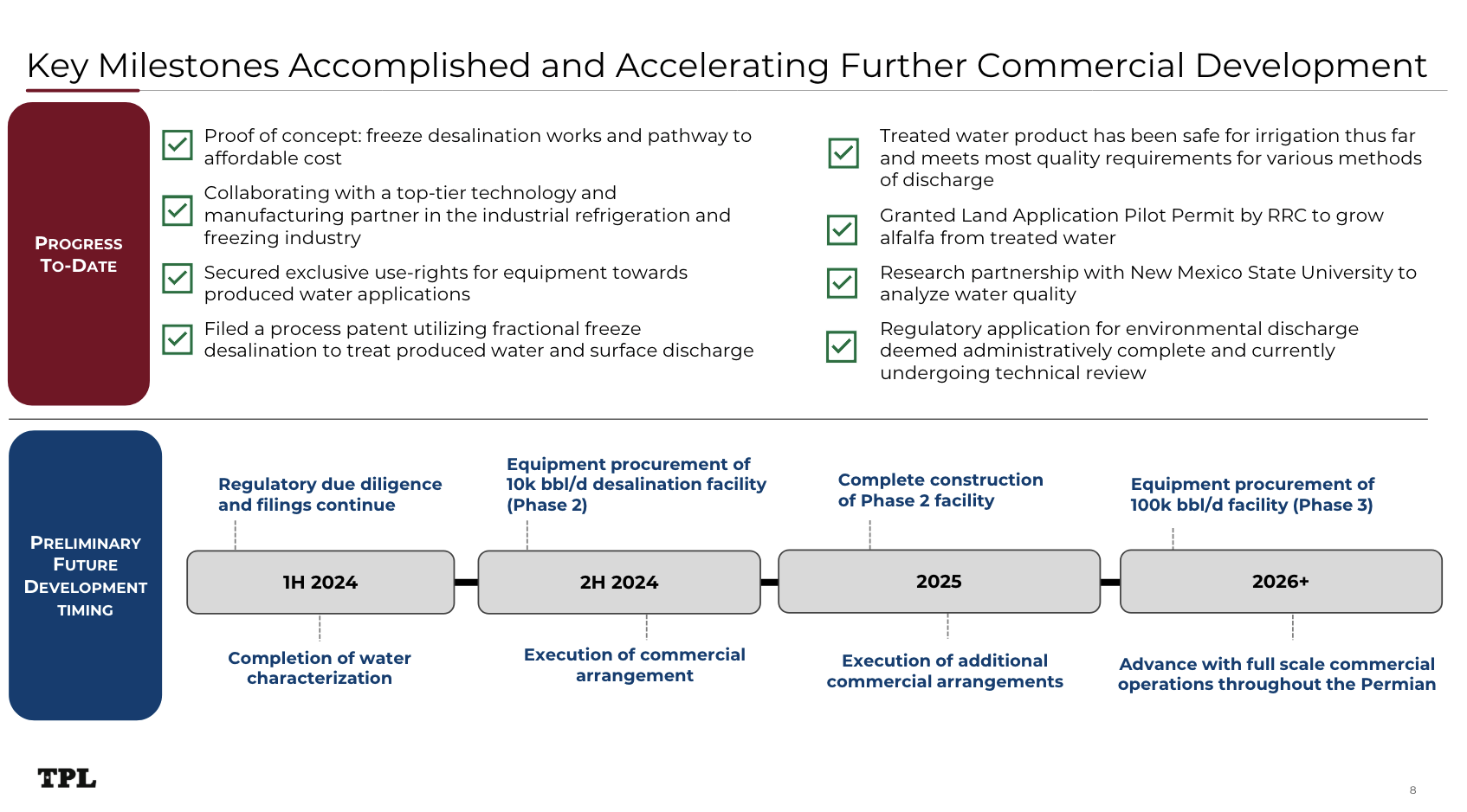

As I wrote in my prior article, the company is working on a method to clean produced water. So far, results have been promising. This could allow the company to sell its technology to producers in other basins and reuse the water on its own land. This could include agriculture.

Texas Pacific Land Corporation

Although we are a few years away from a mass adoption of its technology, water-cleaning technologies could significantly improve the value of its surface acres through agriculture (i.e., for alfalfa production).

Texas Pacific Land Corporation

So, what does this mean for shareholders?

Shareholder Value

Earlier in this article, I showed the company's ten-year performance, which was truly mind-blowing.

However, I have even better statistics. Using the data below, we see TPL returned 29% PER YEAR between 1/1/2017 and 12/31/2023. This happened despite an oil CAGR of just 4% during this period.

While TPL benefits from higher oil prices, all it needs is oil prices to remain above "depressed" levels to warrant higher oil production in the Permian. After all, when oil production increases, it benefits from water sales, produced water, royalties, and everything related to the drilling and production process.

Texas Pacific Land Corporation

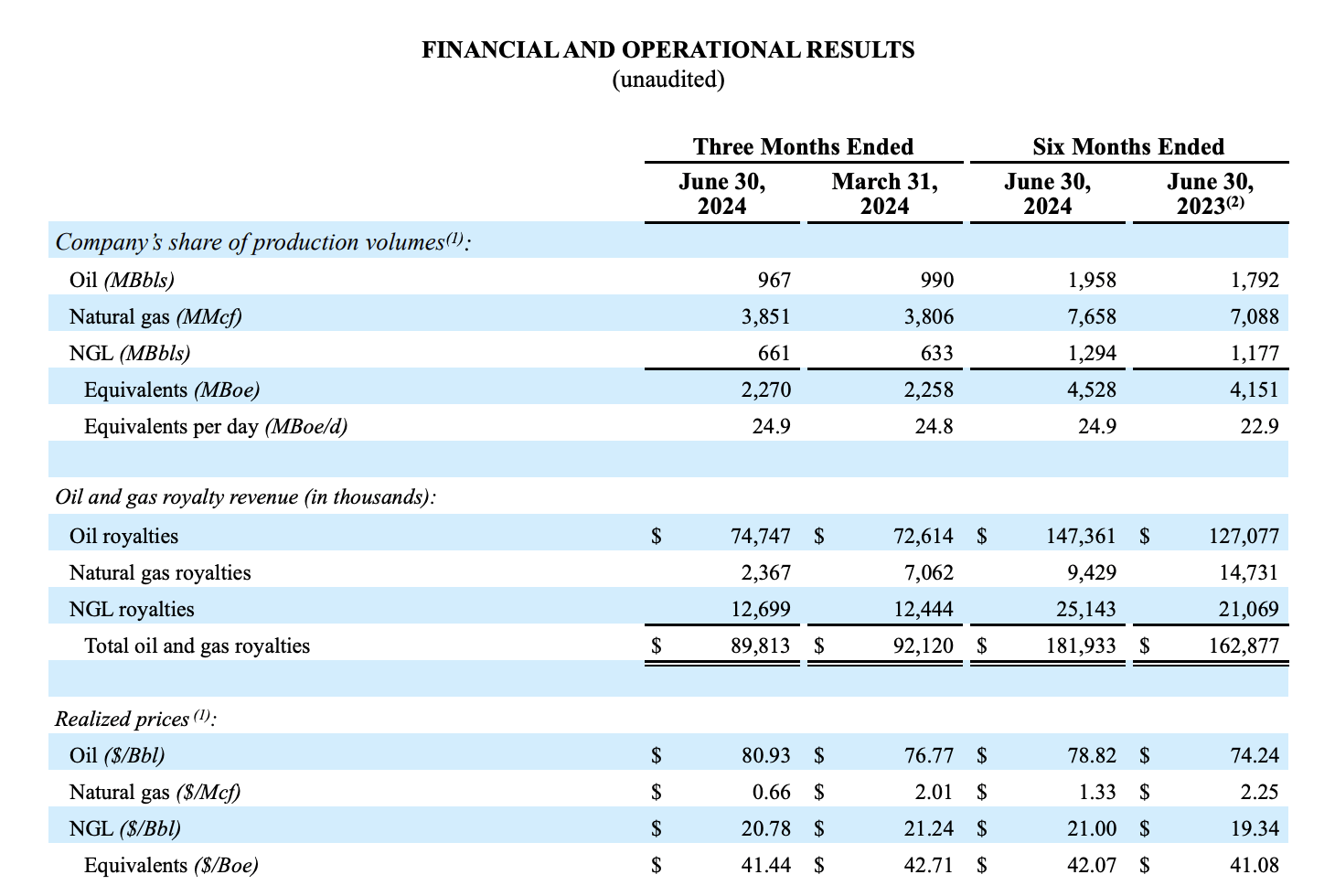

This was also reflected in its 2Q24 results.

The company received 2.27 million barrels of oil equivalent in royalties. That's up from 2.26 million in the prior quarter. Total royalty payments were slightly lower at $90 million (down from $92 million) due to much lower natural gas prices, which more than offset a slight increase in crude oil prices.

However, later this year, the Matterhorn pipeline is expected to improve takeaway capacity in the Permian, which should allow local natural gas prices to improve.

Texas Pacific Land Corporation

Furthermore, what's interesting is that the company grew its water sales by roughly 10% on a quarter-on-quarter basis! Produced water royalties increased by 10% as well.

As more than 70% of its water sales came from customers outside of its own land, there's a lot of room for growth.

With regard to profitability, it ended the quarter with an EBITDA margin of 89%.

What's even more important is its balance sheet and how the company wants to use it going forward.

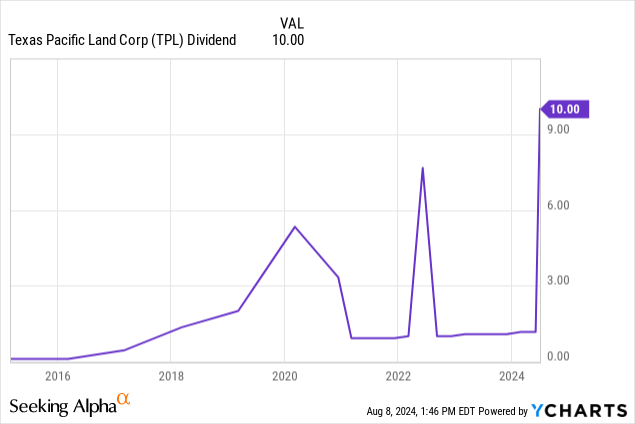

As of June 30, the company had roughly $895 million in cash and cash equivalents. This allowed the company to distribute cash to shareholders, including a $10 per share special dividend. This special dividend translates to a yield of roughly 1.3%. When adding its base yield of 0.7%, we get an annualized dividend yield of 2.0%. That's not half bad!

Data by YCharts

Data by YCharts

Furthermore, the company does not have a penny in gross debt, which protects it against elevated interest rates.

Looking ahead, the company's goal is to keep its cash balance limit at $700M. Everything above that will be used to reward shareholders or for opportunistic M&A.

This is what the company said during its 2Q24 earnings call. I added emphasis as the quote is quite long:

Last June, we announced that we had set a target cash and cash equivalents balance of approximately $700 million. Above this targeted level, TPL will seek to deploy the majority of its free cash flow towards share repurchases and dividends. In conjunction with this announcement, we also declared a $10 per share special dividend. Our cash and cash equivalents balance at the end of the second quarter of 2024 as of June 30 was approximately $895 million, though the $10 per share special dividend was paid in July with a total outlay of approximately $230 million.

The target cash balance is intended to provide a framework and some predictability on how the company will allocate cash. The company continues to generate substantial free cash flow while maintaining a pristine balance sheet. Even beyond this most recent special dividend, the company still retains tremendous optionality to return additional capital to stockholders and to invest in attractive growth opportunities. - TPL 2Q24 Earnings Call

I believe the company went with a special dividend after the massive stock price increase in recent months. I agree with that move. Buybacks make more sense after a steep stock price decline.

Moreover, some readers of mine have expressed concerns about the company potentially "wasting" money on M&A deals. Readers want the company to focus on what it does best, which is making the most money with its existing assets.

During its earnings call, it noted that opportunistic M&A is on the table. However, the company will not force any deals as it can grow entirely organically. There is no need for M&A to reach its goal, as TPL is very clear about that.

It also helps that its largest shareholder, Murray Stahl, is a part of its Board. He has a fantastic track record and adds a lot of safety to TPL's operations - I think.

With regard to free cash flow, last year, it generated $415 million in free cash flow, 10x its 2016 result.

Texas Pacific Land Corporation

Going forward, TPL is upbeat about higher oil production due to favorable DUC (drilled but uncompleted wells) inventory levels. It is also upbeat about the "oil cut," noting that the share of oil production will likely remain in mid-40% levels.

Valuation-wise, TPL trades at a blended P/FCFE (free cash flow to equity) ratio of 40.1x. Its normalized P/FCFE ratio is 31.2x. While both these numbers may seem lofty, investors need to be aware that we are dealing with an ultra-high margin company that enjoys strong secular growth.

FAST Graphs

Using the FactSet data above, analysts expect 17% and 15% per-share FCFE growth in 2024 and 2025, respectively, potentially followed by 11% growth in 2026.

If this growth lasts - I expect it will - we are likely looking at a $900 stock with room to run to $1,000 without being overvalued.

As such, I obviously remain bullish and will try to buy more TPL stock on dips.

Although I have a huge position, I consider TPL one of the best investments in my portfolio, with a multitude of tailwinds and long-term growth opportunities.

In fact, all of our family accounts own TPL stock with the intention of buying more this year.

Takeaway

I'm big in Texas Pacific Land and I don't see that changing anytime soon.

After a 50% return on my investment and TPL's strong 2Q24 earnings, my conviction has only grown stronger.

TPL's near-perfect business model, with its powerful mix of land, water, and royalty rights, continues to outperform, and the company's strategic positioning in the Permian Basin ensures it's primed for even more growth.

With a rock-solid balance sheet, sky-high margins, and a clear plan for higher shareholder value, TPL is one of the most compelling investments I've ever made.

Needless to say, I'll be adding to my position on any dip, confident that this Texas landowner is set for even greater heights.

Pros & Cons

Pros:

- Unrivaled Business Model: TPL's combination of land, water, and royalty rights makes it a cash-generating machine with minimal operational risk.

- Strategic Location: Sitting on prime real estate in the Permian Basin, TPL benefits from the heart of U.S. energy production.

- High Margins and Strong Returns: With a 64% net income margin and a track record of outperforming the market, TPL consistently delivers exceptional returns.

- Debt-Free and Cash-Rich: A pristine balance sheet with no debt and a robust cash position allows TPL to reward shareholders generously while pursuing growth opportunities - even if it's not a high-yield stock.

Cons:

- Complex Valuation: Valuing TPL can be challenging due to its unconventional business model, making it difficult to determine its true intrinsic value. Compared to high-yield royalty plays, it may not look attractive.

- Regulatory Risks: The company's expansion plans, particularly in water management, may face regulatory challenges, although I believe these risks are subdued.

- Demand Risks: Generally speaking, recession risks are always present, as declining economic conditions will likely hurt oil and gas demand and prices.

- Oil & Gas Production: TPL does not produce oil and gas. It is dependent on the growth plans of its "tenants." However, given that the Permian is the only basin capable of strong output growth, I have no doubt that its tenants will continue to boost output.

Comments