Summary

- Align's recent earnings were underwhelming, leading to a 21.56% YTD stock drop.

- Q2 2024 earnings showed mixed results, with EPS beating estimates but revenue slightly lower than expected.

- Align's potential lies in its large TAM, strong gross margin, and top management, but growth needs to accelerate for investor trust.

- Align has the potential to be a quality compounder with its stellar balance sheet.

Monty Rakusen/DigitalVision via Getty Images

Introduction

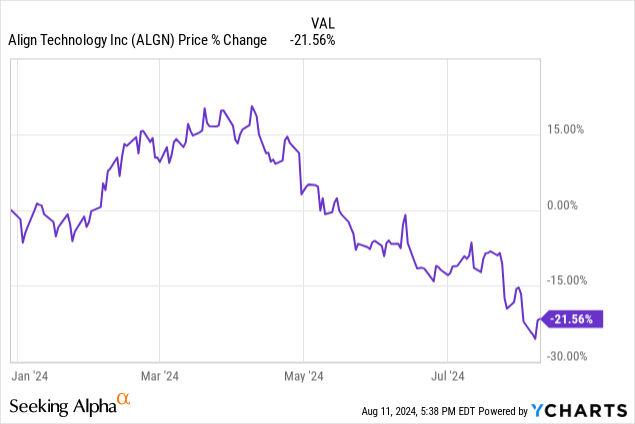

Align (NASDAQ:ALGN) recently released earnings and they were quite underwhelming. While Align is a quality company, the earnings growth is simply not enough.

At the time of writing, Align is down 21.56% year-to-date and the stock dropped over 4% following the earnings report and continued to slide ever since...

Data by YCharts

Data by YCharts

So without further ado, let's take a look at the numbers and see if we can find a reason for this sell-off.

The Numbers

Align Technology's Q2 2024 earnings report wasn't received well by investors. Overall, we could say Align had a mixed quarter. When we look at the 2 main numbers investors look at when they see an earnings release, we can see that Align reported earnings per share of $2.41, which beat the analysts' estimates of $2.32 per share.

On the other hand, revenue came in slightly lower than expected at $1.03B versus the $1.04B that was expected. The $1.03B means that year-over-year revenue growth is 2.6% or 3.1% sequentially. This isn't really impressive for what was once considered a high-growth company.

Nevertheless, it is important to keep in mind that Align is a company with a market cap around $16B, as such it is already in a more mature state of growth compared to most growth stocks. As such, Align is a stock pick that could provide some more stability in your portfolio. Nonetheless, we would like to see some higher growth numbers, which we will discuss in more detail later.

Furthermore, an important positive that must be mentioned is that Align's operating margin improved this quarter due to more operational efficiencies and cost management.

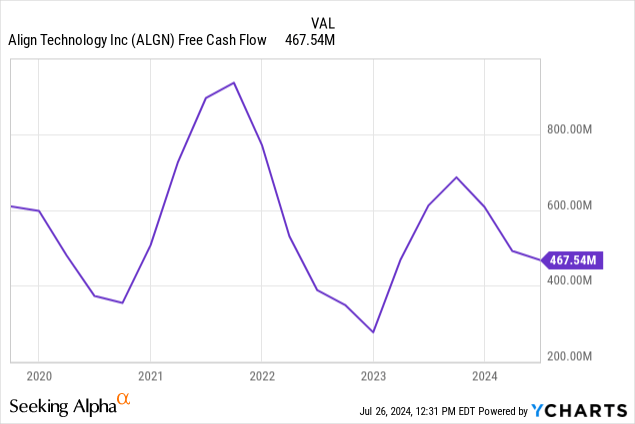

Capital expenditures ((CapEx)) for this quarter were $53.5 million. This might seem high, as the company guided for $100M in total capex for financial year 2024. But, this number is definitely acceptable and is much lower compared to previous years. When we take a look at the CapEx numbers over the last few quarters, they are clearly decreasing, which shows they are doing a good job here.

Free Cash Flow for the quarter stands at $106.4 million, defined with the simple formula (cash flow from operations - CapEx). The FCF still isn't looking great when we look at a larger time frame, it is still significantly lower than in the 2021-2022 period.

YCharts

Data by YCharts

The company guided for a total CapEx for financial year 2024 of around $100M in Q4 of 2023. CFO John Morici reassured this and believes that this will still be the case. Invisalign's CapEx primarily relates to building construction and improvements, as well as manufacturing capacity in support of continued expansion.

The Product Segments

Align's products can be divided into two operating segments, the System and Services segment and the Clear Aligners segment. The company saw revenue growth in both of the segments but was negatively impacted by foreign exchange rates, which accounted for a negative impact of $11.6 million this quarter.

System and Services

Now that we have gone over the most crucial numbers of the earnings report, let us dive a bit deeper into the revenue drivers and where the potential lies for the future.

First, we have the Invisalign Imaging Systems and CAD/CAM Services, which continues to see revenue growth driven by strong demand in both North America and EMEA. Second-quarter revenues increased 16.1% year-over-year and 9.2% sequentially, this shows the strong adoption of the ITero Lumina scanner.

The iTero Lumina is a system for ortho workflows, which was responsible for the majority of the equipment sales. This goes for all things like the iTero Lumina wand upgrades, or the iTero scanner leases.

Furthermore, Invisalign shows signs that they continue to expand in underpenetrated markets, which boosts overall growth.

Investor Relations Align Technology

Clear Aligners

Clear aligners make up the largest portion of the revenue, which as of Q2, 2024 accounts for almost 83% of the total revenue.

Total clear aligner volume increased to 642.7 thousand cases, which is an increase of 3.2% year-over-year and 6.2% sequentially. This quarter, clear aligner volume for teens came in at 216.7 thousand cases, an increase of 8% year-over-year and 8.8% sequentially. Invisalign saw an increase in its teenage demographic and in their adult patients client base, the teens were the main driver of the increase in case shipments.

Clear Aligner revenue came in at $831.7 million, which is a decrease of 0.1% year-over-year. While the company saw an increase in volume sold, the negative impact of the foreign exchange, as we mentioned, caused a slight decrease in revenue on a year-over-year basis. In addition, Align give out some discounts on clear aligners, which offset the increase in volume. But, this is nothing to worry about, while foreign exchange had a negative impact this quarter, it could have a positive impact in another quarter.

CFO John Morici had the following to say about the flat revenues:

For clear aligners, Q2 revenues of $831.7 million were up 1.8% sequentially, primarily from higher volumes, partially offset by lower ASPs. On a year-over-year basis, Q2 Clear Aligner revenues were flat, primarily due to higher discounts. A product mix shift to lower ASP products and the unfavorable impact from foreign exchange offset by lower net revenue deferrals, higher volumes, and price increases.

In Q2 '24, Clear Aligner revenues were unfavorably impacted by foreign exchange of approximately $9.5 million or approximately 1.1% sequentially. On a year-over-year basis, Clear Aligner revenues were unfavorably impacted by foreign exchange of approximately $14.7 million, or approximately 1.7%. For Q2 Invisalign ASPs for comprehensive treatment were down sequentially and year-over-year.

Furthermore, Invisalign shows signs that they continue to expand in underpenetrated markets, which boosts overall growth across the regions, led by strength in Asia Pacific, EMEA, and Latin America.

Potential

Align has a large total addressable market (TAM), after all, everyone needs a dentist, right? When we look at the following slide of the earnings presentation, we can see that Align believes that there are currently 600 million potential patients out there with 2 million doctors that could use their products, this includes an Itero scanner at every chair.

Q2 Investor Presentation Align Technology

In addition to the above visual, the following slide in the earnings presentation gives a solid overview of the investment case for Align Technology.

Align has a moat in a relatively tough market to penetrate. In addition to the large total addressable market, this company immediately ticks off some boxes that resemble quality.

Q2 Investor Presentation Align Technology

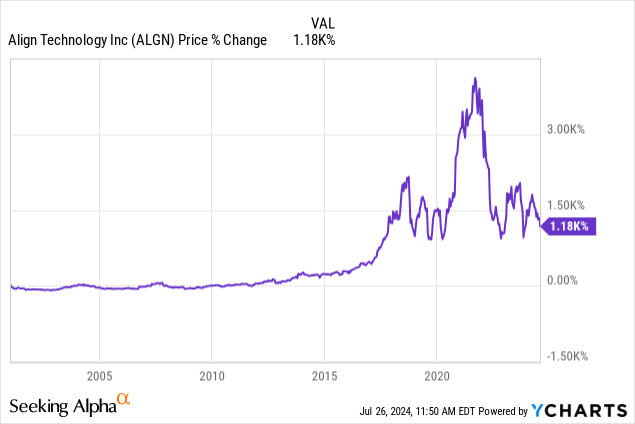

In addition, Align has a top management with a proven track record. Furthermore, the company has over 1,900 patents, which makes it hard to compete with them.

Something that must be addressed is that the company is not run by its founder, which can be seen as a negative, but doesn't necessarily have to be a problem. The founder Zia Chishti left the company more than 20 years ago and sold all of his shares back then. The reason he left and sold all of his shares isn't clear.

Overall, this wasn't an issue as the company is up over 1000% since his departure in 2003.

YCharts

Data by YCharts

Last but not least, the visual below shows the expected orthodontics market size. This projection foresees quite a nice growth for the orthodontics market, with a CAGR of 12.3% per year from 2022 to 2032.

This again shows that the TAM is huge for Align, but the company hasn't been living up to its growth potential over the last few years.

Precedent Research

Deeper Into The Details

In this paragraph, we take a deeper look into the numbers and address some points that could be worrisome for investors.

We will take a look at 4 specifics:

Revenue Growth: Align's revenue is up only 5.98% since Q2 of 2022 and up 1.68% since Q2 of 2021. This is not great, we would like to see this at a minimum 3Y-CAGR of 5%.

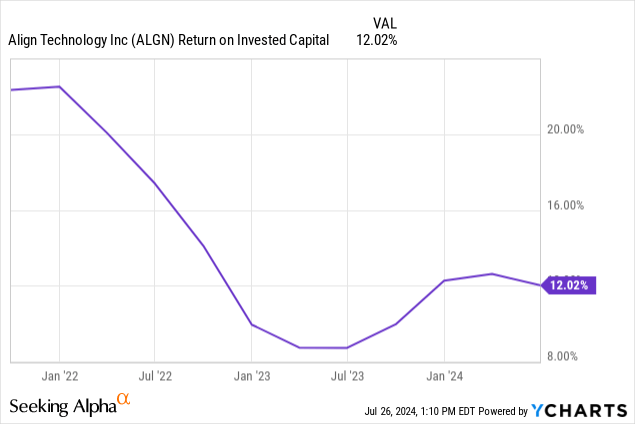

ROIC: A good measurement for the quality of a company is the ROIC. I think for a company like Align, a ROIC number above or around 20% should be the goal. This is also what the management indicated a few years ago as the long-term goal. As of today, the ROIC of Align Technology is just 9.40% according to my own calculations and Guru Focus. According to YCharts, Align's ROIC is 12.02%, while this is better, it still isn't the 20% we would like to see.

YCharts

Data by YCharts

As such, it is no wonder that the stock is trading at lower multiples compared to the historical average.

Gross Margin: The gross margin came in at 70.3% on a constant currency basis it was 70.6%, this is a strong gross margin that shows pricing power. Around 60% would be the minimum for me personally in the case of Align. Good to see that Align is able to hold a strong gross margin even when the company is experiencing overall slower revenue growth. The pricing power stays. Nonetheless, this is lower than the same quarter last year, where the gross margin was 71.2%.

Average revenue per Aligner Case Shipment: The average Aligner Case revenue per customer came in at $1,295. This is a decrease of $55 compared to last quarter and the lowest number we have seen since Q4 of 2022. This also resembles a decrease of $40 or 3% year-over-year.

Again, this is not what we like to see, but is due to the discounts that were given during this quarter. Nonetheless, this is still acceptable and isn't something to worry about at this moment in time.

Conference Call and Guidance

Joe Hogan, the CEO of Align was happy with this quarter's results, but investors weren't if we look at the stock price, and for me personally, this wasn't a quarter to get excited about. So let's get straight to the guidance.

They expect fiscal year 2024 total revenue growth of 4% to 6% year-over-year, due to lower Clear Aligner ASPs from unfavorable foreign exchange conditions and product mix. The analyst consensus was 7% growth, which partially explains the negative stock price reaction.

The guidance is also lower due to the Lumina restorative that was expected to launch in Q4 of this year being delayed to Q1 of 2025, which also weighs on the potential revenue. But, the Restorative would be less than 1% of total revenue anyway, according to CFO John Morici, so this really shouldn't have a big impact.

The company is also guiding for high single-digit growth in Q4 of 2024, which is close to pre-COVID levels. This shows that they believe we will see a return to normal in the near future, in which we should expect growth to accelerate once again. Keep in mind that Q4 is always a stronger quarter, with the teen demographic playing an important role there.

John Morici said the following after an analyst question regarding the full-year guidance:

We actually saw in the second quarter. I mean, I'm not saying it's a return to normal seasonality, but it was much more seasonal in the second quarter in terms of how our volume progressed and how it changed quarter-over-quarter to more normal seasonality. And so our reflection of what we tried to do for the rest of this year based on what we see. In terms of volume, takeout FX and some of that noise that gets caught into Q2. But from an underlying volume standpoint, we saw, um, more normal seasonality. And as we play out the rest of this year, we expect that to continue with the teen season that comes in, that we're in now.

For the longer term (3 years), Morici had the following to say:

When we think of the total and looking out into 3 years, and so look, we're in an underpenetrated market, and we've talked about a lot about that. We think we have the products and the go-to-market capabilities to really move this market forward. And it's up to us to be able to help drive this market forward. And when we look out, and we look out in our long-term model, we believe in, in the opportunity revenue growth is 25% plus percent and up margin 25% plus. And that's how we are positioning things for growth, for whether it's Direct Fab, and the growth opportunities that we have there and the efficiencies that we can drive as well as the standard production that we have now.

This shows that Morici and the executive team as a whole are still confident in the long-term growth of Align. We hope we get back to revenue CAGR numbers, as can be seen in the chart below, which management believes could start as soon as 2025.

Q2 Investor Presentation Align Technology

Conclusion

I'll keep this short. Let's be honest, this wasn't a great quarter. But, a turnaround might be upon us starting in 2025.

Nonetheless, revenue growth must accelerate and preferably the average aligner case shipment revenue goes up again as well. While Align has the potential to be a quality compounder for the next decade, they have to regain the trust of investors again.

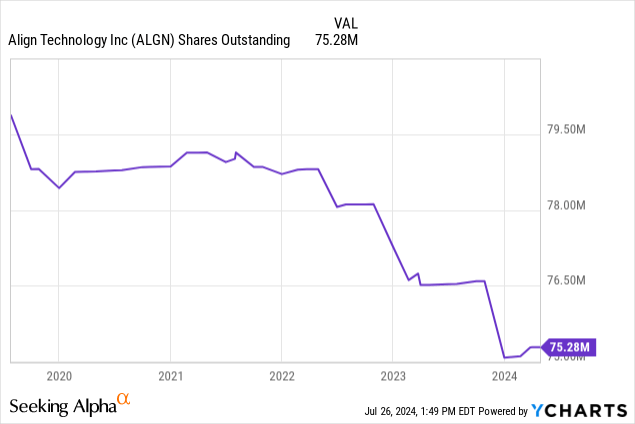

Align has a stellar balance sheet, which mitigates potential risks in case of a recession. In addition, Align has been decreasing its shares outstanding, which could add fuel to the fire once the company starts moving in the right direction.

YCharts

Data by YCharts

Comments