Just based on my local observations, it still feels like the bid-ask on residential real estate is wide.

I wrote Staring Out The Window in October 2022:

Musing #1: Bid-Ask Widening

A year ago the people that paid ridiculous prices for RE were market orders. “Fill me at any price”. Many of them were immediately in the money (ie they probably could have turned around and sold a month later for more. Maybe not net of transaction costs but you get the idea). This isn’t shocking. When optimism turns to euphoria, the rate of change of the returns themselves can explode into a parabolic curve. Of course, such curves are unsustainable. The smug moment of being in the money is short-lived in the same way that a fund that buys a ton of stock going into the close usually gets a favorable mark on their daily p/l. Their sloppy buys drove the price higher in a short period of time. The real sellers didn’t have time to react before the close. But as soon as they check the comps overnight, you can be sure the supply is coming tomorrow morning.

I think of it like water going down a drain…once most of the water is through the drain the remaining liquid swirls quickly around the drain before you hear that sucking sound. Whoosh. The last bid is filled. With maximum punnage — the liquidity is gone.

In the meantime, many other buyers were priced out. You can think of them as limit bids. It’s an imperfect analogy but it will suffice. As things go south now, some of those bidders might be anchored to their original bids which were “cheaper” than where the home traded. However, if they get filled on the way down, they actually have more negative edge even though they got this theoretical house for a cheaper price than the original buyer. You could belabor this with a stylized model but understanding this concept is a big step towards understanding trading.

Anyway, the old limit bids are probably the new ask and the real bid/ask spread is wide. Prospective buyers are adjusting their bids much lower to keep the monthly payment constant or at least manageable, but sellers who likely have cheap financing from the prior low rate regime do not have to cross the spread. If current prices are 5% off their highs but the new mortgage math means homes they should be 20% lower (similar to the stock market) the current listing prices are the “asks” of a wide market.

The current housing market is facing a unique form of illiquidity in the single-family home segment, largely due to the sharp rise in interest rates during 2022 and 2023. The root of this illiquidity lies in the significant bid-ask spread that has emerged as a result of these rate changes.

I’ve been renting the same home since Oct 2020. I have a year remaining on my current lease and have some reason to believe I might not be able to renew again. It’s a bit stressful because renting again without being able to lock is inconvenient. Buying is tough because inventory is lean so it remains a seller’s market even though prices have been flat. Homes locally have been “dead money” for 2 years. (They went down 10% in 2022, recovered in 2023, and flat this year).

Investing instead of owning has been a fairly even proposition on a 4 year lookback but renting for the past 2 years has been a relative windfall. I’m not big on the idea of treating a home as an investment, but the disparity in cost to own vs cost to rent in the past couple years means you’d need opium-level psychic benefits from owning to make it look reasonable.

[My cost to rent is about 1/3 of what it would cost to buy the same house — said otherwise I could rent 3 houses for the cost to own 1. I won’t give exact numbers but it’s equivalent to renting a $1mm house for less than $2,500/m. Crazy when you consider that it’s almost $1k/m for insurance alone out here.

Of course, trying to link home prices to rental cost is only one way of coming up with a valuation. It’s rooted in relative value/opportunity cost type thinking. Another, probably more relevant method, is cost of replacement. Land here is about $2mm acre for average lots and closer to $3mm for premium lots in a flat, desirable location. The cost to build starts at $625/ft. Permitting means you must rent for about 2 years while your home is built. Existing homes trade for about $1k per sq ft.

Throw all of this in a spreadsheet and you’ll find that the IRR to build is terrible…which is another way of saying existing homes are a relative bargain. Especially because building costs only go in one direction which is a safe bet since builder margins suck as it is. Hey, CA is a beautiful place, but it has South America-style disparities, economic dysfunction, and a landed gentry. If I didn’t live here I never would have taken Georgist drugs.]

Anyway, I’m not asking for sympathy by admitting stress. Part of the ownership premium people is so they don’t have that stress. My inconvenience is baked into whatever I think I’m saving so complaining is just being greedy.

Alas, we have been looking at open houses for the past year as depressing as they are. It got me thinking about this wide bid/ask spread that I believe is present but invisible since there’s no true order book. Listings are up, home sales are down, and prices are up 1% y-o-y according to Redfin.

My sense is houses are worth very different amounts to existing homeowners vs buyers. And since many buyers are homeowners (I’m talking about people changing primary residence not second homes), the split valuation even exists within the same brain. You’re Hyde when you list and Jekyll when you bid.

Let’s walk through it.

Homeowners who secured low-interest-rate mortgages years ago effectively “shorted bonds”. As interest rates rose, the value of these loans plummeted, embedding equity into these “short bond” positions. This means that the mortgage itself has become an asset that is highly valuable to the current owner. It’s like “it’s equity in a mark-to-theo short”. But that equity is trapped. It’s specifically tied to that home. The new buyer doesn’t get it because they must finance at the higher current rates.

This mechanically alters fair value of the asset depending on who owns or doesn’t own it. The homeowner might not be able to articulate it but they have two assets: the physical home and the valuable low-interest-rate mortgage. If they were to sell the home, they would have to buy back the mortgage at its face value, rather than its current impaired value thus losing the accrued profit from the “short bond” position.

Let’s make it concrete with a numerical example.

You bought a $500k house 5 years ago with a $100k down payment. You borrowed $400k at 3%.

What do you owe today?

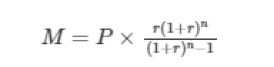

Step 1: Calculate the Monthly Payment on the Original Mortgage

The formula for the monthly payment of a fixed-rate mortgage:

Where:

- M = monthly payment

- P = principal loan amount = $400,000

- r = monthly interest rate = 3%/12 = 0.0025

- n= number of payments = 360

Monthly payment = $1,686.42

The mortgage still has 25 years (or 300 payments) until maturity.

The remaining balance after 5 years is $355,625 (from this calculator)

In our fake world that’s pretty similar to the real one, a lot has changed in 5 years. Interest rates have doubled to 6%.

What is the value of the outstanding mortgage?

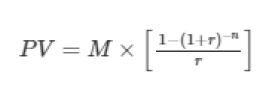

Step 2: Calculate the Present Value of the Remaining Payments

We need to find the present value of these remaining payments, discounted at the current 6% market rate.

The formula for the present value of an annuity is:

Where:

- M = $1,686.42 (monthly payment)

- r = 6%/12 = 0.005 (new monthly interest rate)

- n = 300 (remaining payments)

PV=1,686.42×[1−(1+0.005)−3000.005]

PV = $261,744

The present value of the remaining ~$356,000 mortgage, when discounted at the current 6% market rate, is approximately $261,744.

This significant difference highlights the additional equity embedded in the homeowner’s “short bond” position due to the lower interest rate. The homeowner has an intuitive sense that they are losing when they sell the home because they will have to pay the bank $356k to close the loan when it’s only worth $262k. Eww.

The additional $94k of equity that the homeowner has at prevailing interest rates represents almost 20% of the value of the $500k home!

If mortgage rates fall, the conventional wisdom that marginal demand to buy should increase is a fair assumption. However, rates falling cuts directly into this shadow equity that owners feel compared to a high-rate environment. I suspect this will actually “loosen” a bunch of trapped supply as the bid/ask spread narrows as the homeowners embedded equity in their “bond short” shrinks.

[I’m using the word “shadow” but it’s quite real vs the alternative of buying the same house for $500k at the higher interest rate. It’s “shadow” because the only way to monetize it is to let time elapse until the mortgage eventually goes away. Your lower cost of living relative to someone who doesn’t have a low interest-rate mortgage on the same property is the only way to realize the equity.

Active solutions to this illiquidity trap is allow homeowners to somehow port their mortgage to a new property or allow them to buy back their mortgage at the current value instead of the remaining principal amount.

I already hinted at a passive solution. Let the clock run. As time progresses, homeowners continue to pay down their mortgages. With each payment, the principal balance of the mortgage decreases, and the equity in the home increases. Over time, the impact of the low-interest-rate mortgage diminishes as the remaining balance shrinks. This gradual reduction in the outstanding mortgage balance reduces the value of the “short bond” position, making it less of a factor in the homeowner’s decision to sell. Eventually, as the mortgage balance becomes smaller relative to the home’s value, the embedded equity becomes less significant, narrowing the bid-ask spread.]

If mortgage rates fall in concert with the economy and employment weakening (pretty standard backdrop to falling interest rates), then supply may loosen in combination with general demand shortfall. It feels like a downside risk…but by now I’m also resigned to believing home prices won’t fall. We don’t have enough of them. Lending standards are conservative. There’s nothing frothy about the supply/demand balance. At the same time, it’s illiquid and unaffordable. My selfish position is I’d like to see prices ease but I’d happily settle for a wider selection of homes, even if they are overpriced.

Comments