Vega, represented by the Greek letter, measures an option's sensitivity to changes in implied volatility. It’s a crucial parameter in volatility trading, which is another term for options trading.

Volatility is a term used to describe how quickly the price of a stock, future, or index changes. The same principle applies to options, where the change in the volatility of the underlying asset is positively correlated with the option price. In other words, the higher the volatility of the underlying asset, the higher the option price, and vice versa.

The wider the range of the underlying asset's fluctuations, the greater the likelihood for buyers to achieve their expectations, hence the higher cost. For sellers, it's the opposite; higher volatility of the underlying asset translates into greater risk, thus commanding a higher option premium.

Three Types of Volatility

There are three types of volatility related to options: Historical Volatility (HV), Forecasted Volatility, and Implied Volatility (IV).

HV refers to the actual historical volatility of the underlying asset, calculated by statistically analyzing its price changes over a past period.

Forecasted Volatility is an estimated volatility derived from historical data and used for theoretical pricing of options.

IV is derived by reverse engineering from the option's current price, It represents the market's current perception of the future volatility of the underlying asset.

Basic Concept of Vega

Vega measures how much an option’s price changes when IV moves by 1%, assuming other factors stay constant. For instance, if Vega is 0.37, a 1% change in IV will alter the option price by $0.37.

Vega reflects the relationship between IV and option prices. An increase in IV raises option prices, while a decrease lowers them. Unlike Theta, which affects time decay, Vega influences the option’s extrinsic value, not its intrinsic value.

For options with the same strike price, both call and put options have identical Vega readings, meaning IV impacts them equally.

Vega and Position Direction

A long option position has positive Vega, benefiting from rising IV. A short option position has negative Vega, benefiting from falling IV.

When combining Greek letters across different options strategies, subtle differences arise. For example, while Long Call and Short Put both signal bullish positions, their Gamma, Theta, and Vega differ, showcasing varied nonlinear characteristics. Mixing these positions creates a range of strategies.

Impact of Vega on NVIDIA Options

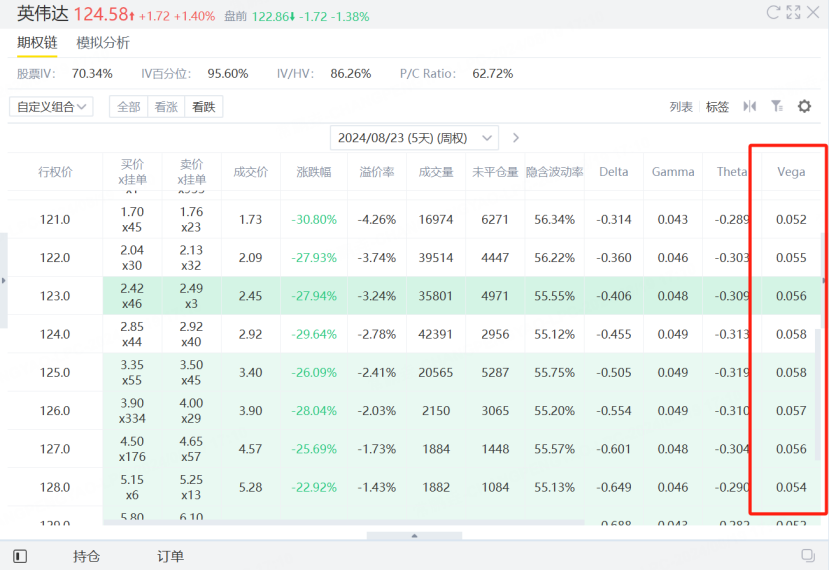

Typically, Vega is highest near the at-the-money strike price, and decreases as you move into in-the-money (ITM) or out-of-the-money (OTM) options.

For $NVIDIA Corp(NVDA)$ , with a strike price of $123 and an IV of 55.55%, a 5 percentage point increase in IV would raise the option price by $0.28, an 11.4% increase relative to the current price of $2.45. Larger volatility changes would have even more significant effects.

Investors can profit from Delta, Theta, and Vega, but Vega tends to be the most volatile and offers higher returns. In cases of sudden IV spikes, out-of-the-money options can double in price. Keeping an eye on changes in IV helps investors capitalize on Vega’s opportunities in the options market.

Comments