Summary

- Stock market conditions in 2024 have seen a rally in growth stocks, a resurgence of meme stocks, and a recent spike in market volatility.

- Chewy stock has seen significant fluctuations following a slight recovery in its Q1 report and a substantial investment from "Roaring Kitty."

- Amazon, Walmart, and others appear to have similar prices to CHWY, giving the company no clear competitive advantage in the subscription dog food market.

- Compared to Amazon, I expect Chewy to face more significant marketing costs per customer and higher fulfillment and shipping expenses, giving Amazon a distinct long-term edge.

- Chewy's forward "P/E" appears too high, even with bullish long-term income outlooks, particularly given its material equity dilution rate through stock-based compensation.

Justin Paget

The stock market has been experiencing unusual conditions in 2024. The year's first half saw a tremendous rally in technology and innovation stocks. There's been some resurgence of "meme stocks" that crashed in 2022. More recently, we've seen a significant spike in market volatility, with some unraveling of the first semester's gains.

I believe the former "meme stocks" are among the more interesting to watch today. Many remain over 70% below their 2021 highs, but are up ~50% from their lows. As such, we must ask if those stocks are in a dead-cat bounce that will lead to losses or if they're a value investor's dream as they venture into more significant recovery. Of course, that will differ from company to company.

Chewy (NYSE:CHWY) is a good example. Although it trades at less than a quarter of its former value, it has risen over 50% over the past three months. This came after a strong Q1 earnings report, showing a recovery in both sales and margins. It was followed by a favorable social media post from "Roaring Kitty" (Keith Gill), causing the stock to spike higher as speculation grew surrounding him (and followers) potentially buying the stock. Now, Gill is facing an SEC lawsuit regarding pump and dump schemes. He holds a 6.6% stake in CHWY, creating concern for Chewy's management.

With the stock now mired in a storm of turbulence, it is an excellent time to take a deeper look into its fundamentals. In particular, the company's financial position, operational focus, and competitive viability. Those factors will play a key role in determining a fundamental valuation range.

Aggressive Growth Or Competitive Weakness?

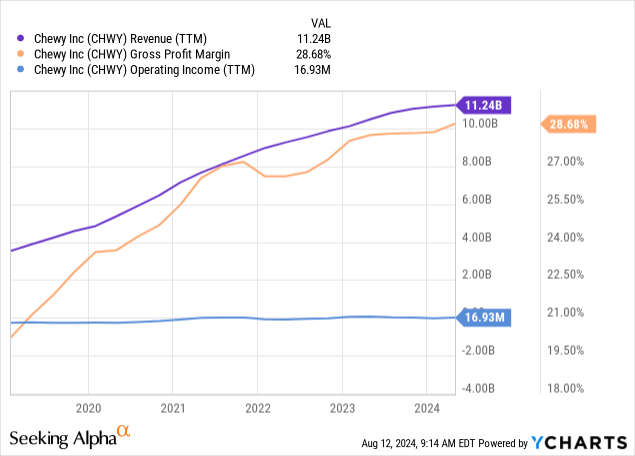

Chewy has had excellent revenue growth in recent years, expanding to over $11B in annual revenue. Further, it has managed this while improving its gross profit margins, indicating a solid path toward profitability. That said, its operating income remains very close to zero, as if its managers can either not earn a profit in the competitive environment or are deliberately reinvesting would-be profits into growth. See below:

Data by YCharts

Data by YCharts

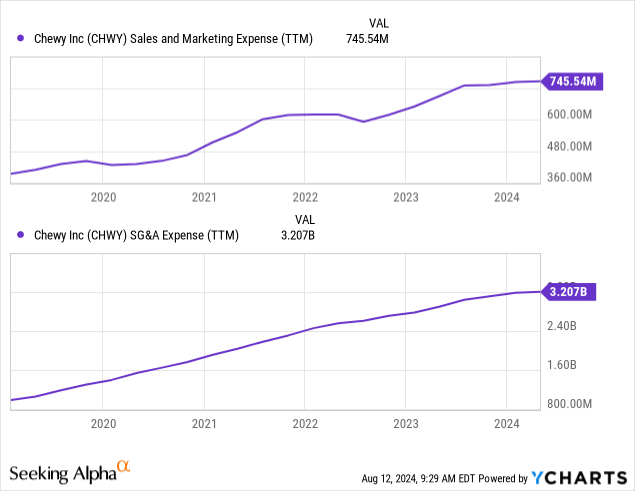

It may be wise for the company to use its gross profits on growth efforts such as marketing. The firm operates mainly on a subscription-based model, so if it can market successfully, it may manage to earn potential customers for many years. That said, most of its gross expenses are selling, general, and administrative, not sales and marketing. See below:

Data by YCharts

Data by YCharts

Its marketing budget is notable and could likely be reduced if the company needed to raise its operating cash flow quickly. That said, it is not so high that it can reduce marketing permanently without potentially losing customers. Further, its SG&A spending is, to me, extremely high, consuming a great deal of would-be profits.

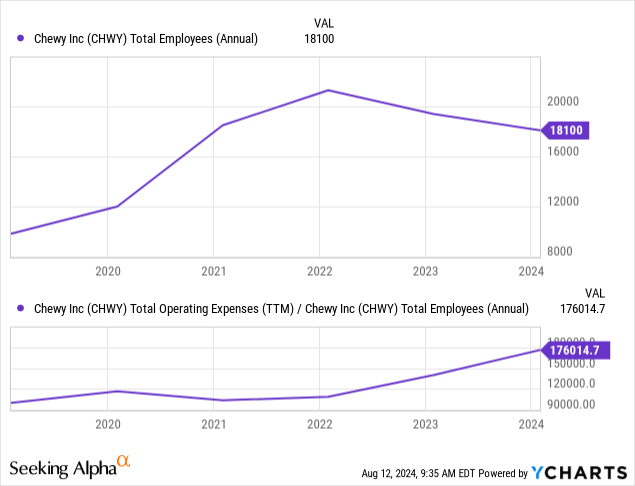

Notably, its OpEx has continued to rise despite layoffs, as the ratio of its operating costs per employee has risen. See below:

Data by YCharts

Data by YCharts

This is not a great sign, as it may indicate that it is paying its remaining employees more to fulfill its needs. That may differ depending on how it accounts for costs as OpEx or COGs, particularly for fulfillment employees. That said, I view its overall situation as an indication that it struggles to compete while maintaining profitable pricing. Ultimately, Amazon and Walmart have subscription services for virtually all items sold by Chewy.

Chewy is generally cheaper than Petsmart, Walmart (WMT), and likely Amazon. It is worth noting that the price differences between Chewy, Amazon, and Walmart are all subject to change and that the gaps are extremely low. That said, while Chewy does not pay the expense of a storefront, it may be that Walmart and Amazon have greater overall supply chain capacity to compete on costs, particularly given they have sufficient capital to offset losses if need be. With a market capitalization of $10.4B, Chewy has decent access to capital, but not nearly as much as its main competitors.

Out of interest, I checked the product I bought, a standard 40-lb beef brand (Nutrish), and saw that it is $52.24 for a Chewy subscription, $55 for a Walmart subscription, and $52.23 with Amazon - all with free shipping. Chewy is discounted by 35% for the first purchase, technically making it the cheapest. However, many may have credit card discounts for Amazon or Walmart, which, for me, makes Amazon the best option. Still, the bottom line is that they're all extremely close. Even Petsmart online had similar pricing but with a more considerable 40% discount on the first purchase.

The price gaps are so low that the competitive pressure is enormous, indicating customers will change if Chewy tries to raise prices. Thus, the company can only compete on the cost front, as the price is standard. In my view, that is an uphill battle, as both Amazon and Walmart have world-class supply chain management with a great deal of vertical integration. From that standpoint, I doubt Chewy's ability to carve a long-term competitive edge in a hyper-competitive market.

Closer Look Into Chewy's Financial Pressures

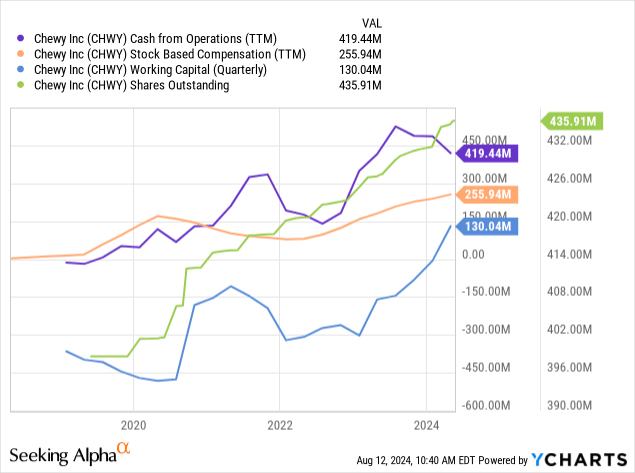

There are positive and negative factors impacting Chewy's balance sheet. It has no financial debt, which is a positive sign. The company also has positive working capital and strong operating cash flow. However, it has no stable net income, meaning its CFO is essentially a function of high stock-based compensation and ample dilution. See below:

Data by YCharts

Data by YCharts

Like many companies, Chewy removes stock-based compensation from its adjusted EBITDA calculation. I find this practice misleading because stock-based compensation is a direct cost to equity investors since it dilutes value. In other words, equity investors indirectly pay Chewy employees' salaries (or bonuses) through dilution.

Currently, the TTM stock-based compensation is about 2.5% of its market capitalization. That is a material cost, but it is not alarmingly high. That said, the fact that its stock-based compensation has risen markedly. At the same time, its market capitalization has declined dramatically is a problematic indication, as that will eventually accelerate the dilution rate unless its valuation increases.

Analyst consensus estimates for Chewy point to strong sales growth, leading to an EPS target of $1.33 by 2027. That would give it a forward "P/E" of about 18X, potentially falling to a more reasonable 12.4X by 2030, though that is based on the target of just one analyst. Its 2025 forward "P/E" is 25X, which would only be reasonable if it can maintain strong sales growth. To me, its recent sales growth trend is not strong enough to justify a high valuation, particularly when its ability to earn a consistent profit remains questionable.

The Bottom Line

Overall, I am bearish on Chewy, but I would not currently bet against it due to its meme stock position and associated volatility. With "Roaring Kitty" and others gambling on the stock, I will not put myself at the other end of speculative traders who, in my view, care very little for fundamentals and are instead looking for a short-term pump. However, I may change my view if the stock rebounds even higher into the $30-$40 range. Short interest on CHWY is 12.5% today, which could be enough to fuel another short squeeze.

In the past, when Chewy first launched, its prices were seemingly more competitive with Amazon and Walmart, which had not yet pressed into the pet market. It could also benefit from taking market share from in-store-focused retailers like Petco (WOOF) and Petsmart.

Since then, those two have focused more on their subscription-based e-commerce businesses, with Amazon, in particular, gaining an edge. Thus, without superior pricing, I see little reason why Chewy would grow organically and, therefore, may need to spend more and more on marketing to gain and maintain customers. Amazon may have better supply chain leverage (due to its vertical integration), and has a massive existing customer base who may prefer it, particularly if they have a credit card discount on Amazon.

It will be interesting to see its Q2 report later this month. In my view, it will be disappointing unless it manages to dramatically reduce SG&A spending without losing sales growth. This could be exacerbated by growing economic consumer strain that may be pushing greater price competition, which I believe Chewy has a disadvantage in compared to Amazon.

Comments