Summary

- Copper prices surged earlier in the year, but have since reversed gains as China's copper inventories slipped from extreme highs.

- Rising copper mining costs may offset post-2020 gains in copper, depending on economic and political risk in Latin America.

- China's efforts to bolster copper stockpiles may have pulled future demand forward, potentially leading to a sharp decline in imports later this year.

- It may be unlikely that electric vehicle demand will rise enough to increase copper consumption, or EVs will continue to require so much copper.

- The rising gold-to-copper ratio may indicate a global decline in manufacturing activity.

shells1

Last year, I published "COPX: The Copper Shortage Is Unlikely To Persist In 2024." At the time, I held a bearish view on the Global X Copper Miners ETF (NYSEARCA:COPX), expecting the shortage in copper would reverse into a glut this year. To be fair, that is not exactly what has occurred, at least not yet. Copper prices surged during the first months of 2024, but recently reversed those gains. COPX is currently around 3% lower than I covered last in April 2023, making it essentially unchanged. However, it has dramatically underperformed the S&P 500, which has risen 30% since then.

Given the ongoing volatility in copper and the stock and bond markets, I believe it is an excellent time to take a closer look at the commodity and the valuations of copper mines in COPX. Copper is often viewed as a strong economic indicator, potentially implying the bust in copper prices may be a global recessionary indicator. That said, I continue to believe copper is increasingly a measure of the Chinese economy, with a lower emphasis on the US market compared to the past. Overall, the copper market appears likely to weaken, though that depends significantly on China's ongoing efforts to stimulate its economy.

Copper Mining Costs are Still Surging

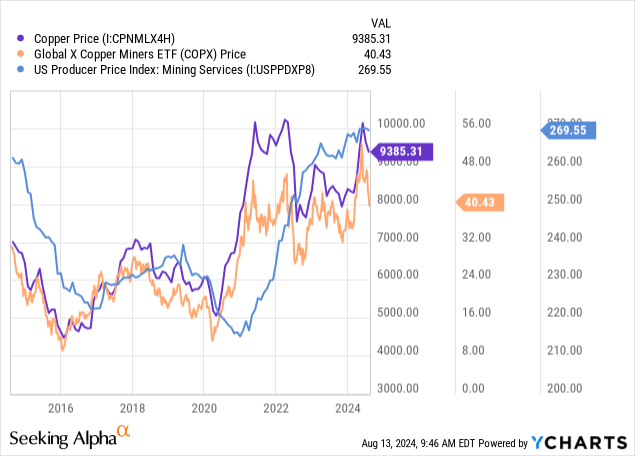

COPX is closely correlated to the price of copper. Indeed, the price of copper is the driver of the revenue of most major copper miners in the ETF. Mining companies profit from the spread between prices and mining costs, so if costs are rising at the same pace as prices, profitability does not improve. In my view, this factor is often overlooked, particularly given the ongoing rise in inflationary pressures and economic turbulence in key Latin American countries and, to a lesser extent, North America.

We can indirectly measure copper mining costs by looking at the PPI of mining services, which are involved in a wide array of mining operational expenses, depending on the company. Realistically, a rise in the copper services PPI will not proportionally increase the AISC for mining, though it is a strong indicator. See below:

Data by YCharts

Data by YCharts

Since 2020, COPX has essentially doubled in value. The global price of copper has increased by about 55%, while the mining services PPI has risen by around 17%. Thus, there has been a notable increase in copper miner profitability, leading to higher prices.

The weighted average valuation of COPX is lower this year at 12.6X compared to 16.1X in 2023. Its price-to-book is also down to 1.2X from 1.3X last year. The change in valuation is mitigated by the negative trend in the price of copper and the comparatively high profits of most copper miners in the previous twelve months, potentially skewing the "P/E" ratio lower.

The all-in-sustaining cost of producing copper for most large miners is likely around $2.85/lbs, based on First Quantum's estimates. First Quantum (FM:CA) is the largest holding in COPX with operations around the globe. Few significant miners publish their AISCs, so I expect this figure to somewhat indicate the others in COPX. The company had an AISC of $1.77/lbs in 2019, marking an 11% annualized growth rate and a 60% overall increase. That increase is not as significant as the rise in copper prices, but it is enough that copper may not have the best profitability outlook if prices decline while costs continue to grow.

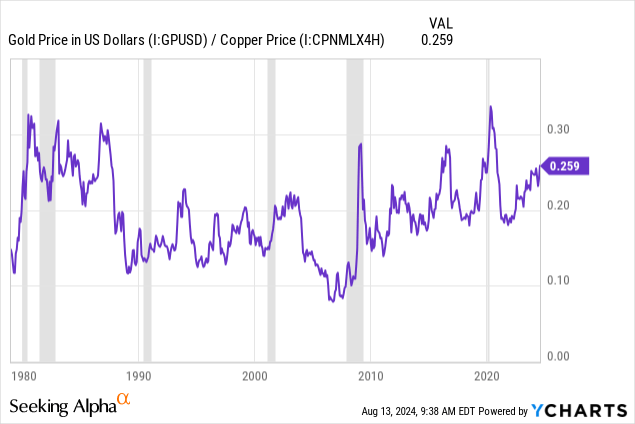

Based on the gold-to-copper ratio, there is reason to believe the global market is slowing down. Historically, this ratio is seen as an indicator of a worldwide recession because copper is closely dependent on industrial demand, while gold and copper share similar supply cost factors. The ratio is rising today, which has occurred in most recent recessions, but has also happened without a recession. See below:

Data by YCharts

Data by YCharts

Comparing copper to gold, copper is not necessarily discounted today, but could become more discounted. If the ratio were to return to 2020 levels, we'd expect to see copper fall to around $3.2/lbs from its current ~$4/lbs. Since it costs around $2.85/lbs to mine, that would erase most of the TTM profits in COPX's holdings, particularly if costs continue to rise as First Quantum expects.

Although copper prices surged earlier this year, I do not see firm evidence that that was tied to an acute shortage. Throughout this year, China's imports of copper have flattened. China alone imports over half of the global copper trade market. Its overall import level remains high, but due to high prices, it has been increasingly made up of scrap from the US, offsetting demand growth for miners.

More importantly, much of those imports are going to inventory buildup. Shanghai's copper exchange inventory has risen to around 322KT, the highest level since 2020, with the LME's increasing inventory. The fact is that China's real estate market, which is the singular largest copper demand market, is in free fall despite waves of government efforts to try to stem losses. China's residential property prices have declined for years, leading property investment trends to multiple years of double-digit declines. This issue is worse for iron than copper, but I expect it will worsen as more Chinese banks face issues relating to surging non-performing loans.

So, the copper shortage earlier this year seems to have been driven by China's effort to increase inventories. There could be multiple reasons for this, but given the negative trend in much of its economy, I suspect it may be geopolitical, as the country has made a tremendous effort to expand commodity stockpiles in recent years.

Of course, some may have a bullish outlook due to EV demand, which may have played some role in the copper rally earlier this year. However, EV sales are falling due to high interest rates limiting vehicle demand. Further, recent technological innovations may dramatically lower copper needs over the coming decade, potentially upending the belief that a long-term shortage is inevitable.

Further, copper miners, most of those in COPX, may see a more considerable rise in production costs due to ongoing political and economic turbulence in Latin America. In recent years, we've seen increased strikes and anti-mining sentiment in most key copper-producing countries, such as Peru and Chile. BHP (BHP) is now facing a strike at one of its largest copper mines. In my view, the rise of populist left-wing political leaders in most of Latin America indicates a risk to COPX, which could drive taxes and costs and limit capital investments. Of course, this risk is difficult to calculate; however, should the global economy turn toward a recession, as I expect, I imagine we'll see a significant associated increase in mining costs, similar to the post-2020 trend.

The Bottom Line

Overall, I am more bearish on COPX today than in the past. I expect the price of copper will continue to slide due to waning demand from China and Western nations as manufacturing and construction activity weakens globally. Indeed, I believe we would have already seen this trend if not for China's effort to bolster its stockpiles earlier this year. To me, this effort has pulled future demand forward, as higher stockpiles should limit imports at some point over the coming year or two.

COPX's valuation on a TTM basis is not too high. However, if we assume a decline in prices back to around $3-$3.5/lbs and a cost increase to over $3/lbs, then most COPX miners may lose the bulk of their TTM profitability by next year. Of course, that is a speculative outlook that depends significantly on the state of the global economy and my view that China's stimulative efforts will continue to fail.

I expect COPX may decline to or below $30, which is the low-end of its post-2021 range, associated with a negative demand outlook. Of course, in the event of a significant global slowdown, I would not be surprised to see COPX fall back into the $20 to $30 range, as most miners lose most of their profits. Still, in the long run, the sector may be supported by low historical capital investment levels. In the past, I saw that as a critical bullish factor for copper miners; however, I believe the demand outlook is weak enough to offset lackluster supply growth.

Comments