Summary

- Rio Tinto has lost ~14% of its value since January, while the S&P 500 has risen by 20%, stemming from a sharp decline in iron prices.

- I expect China's iron ore demand to continue to plummet along with its property sector, potentially leading to a permanent 15-25% decline in global iron demand.

- Rio Tinto's exposure to China is exacerbated by its significant Australian iron ore mining, which has supported China's property development bubble.

- The coming glut in iron ore may push the commodity down into the $60 range, dramatically reducing Rio Tinto's overall EBITDA.

- Copper and aluminum are also negatively exposed to this trend, but they have closer ties to manufacturing demand, which may face a more transitory decline due to a global economic slowdown.

Abstract Aerial Art/DigitalVision via Getty Images

In January, I published a negative outlook on the mining giant Rio Tinto (NYSE:RIO) in "Rio Tinto: Iron And Copper Prices Likely To Crash In 2024 As China Stimulus Fails." Since then, RIO has lost ~14% of its value, while the S&P 500 has risen by around 20%. Iron ore prices have crashed by around 36%, while copper has increased by around 6%, though it is currently in a bear market.

My negative outlook for RIO is mainly dependent on my views and understanding of the importance of the Chinese property development market. Although Rio Tinto has a diverse portfolio of operations, its primary exposure is iron ore sales to China from Australia, primarily used for infrastructure and property development projects.

With RIO trending lower and back at its five-year support level of around $60, it seems to be an excellent time to cover the stock and provide an updated short and long-term income outlook. It boasts a low valuation with an 8.5X forward "P/E" based on other analyst estimates and a 7% dividend yield. As such, many analysts and investors are particularly bullish on the stock and see it as a long-term value opportunity. We must consider the broader economic conditions impacting its income, as a long-lasting commodity price decline may upend its profitability.

Chinese Property Crisis is a Permanent Issue

As I've discussed in depth, I firmly believe that China's property bubble is popping and, more importantly, that the CCP has run out of options to stop the implosion. China accounts for ~70% of global iron ore imports, around half is used for construction and the other half for manufacturing. Thus, as China's new home price accelerates lower (the rate of decline is increasing to ~5% YoY from around 0% in January) and its property investment falls by double-digits, iron ore has firmly been pushed into a global glut. Copper has been more resilient, as China built up a considerable inventory base early this year, but I expect that bubble will continue to pop as well.

I believe my thesis on RIO has been proven correct regarding iron ore, which accounts for nearly two-thirds of its sales. China's property prices and investment trends have continued to collapse despite immense stimulus efforts from the CCP. To me, that dispels the myth that China's heavy-handed legal structure can force its economy to grow. Put simply, when a country's residential and commercial property markets have a 20-30% vacancy rate due to extreme overdevelopment, you cannot force an indebted populace to buy empty buildings.

With that in mind, there is virtually no need for roughly half of China's historical iron ore imports. If China accounts for 70% of global imports, with an even split between manufacturing and construction, I'd estimate around 35% of global supplies have been going to wasteful construction projects. These builds are generally secondary household investments, many of which are in empty cities. Of course, now that the bubble has burst (and is continuing to do so), many Chinese people are left paying mortgages on uncompleted properties from failed developers. Keep in mind that the country's largest developers have defaulted.

So, China has a significant excess of buildings and a population that is expected to be ~50% smaller by the end of its children's expected lifetimes in 2100. Its marriage rate has also declined quickly, implying that its population decline may be faster.

While this demographic issue may seem remote to Rio Tinto, I believe it is essential. Many analysts and investors expect the slowdown in China's iron ore demand to be a transitory trend tied to a normal credit cycle. However, I argue that a permanent shift will create a lasting issue for Rio Tinto's iron ore sales to China. China accounts for 60% of Rio Tinto's entire revenue, so if its demand is permanently cut by 25-50%, we'll see a long-lasting glut and supply chain issues for its business model. Fundamentally, this is a crucial issue for Australia's huge mining industry and the broader economy.

This isn't to say that iron ore will still not be in demand for manufactured steel products such as vehicles. Indeed, I expect headwinds in construction to be partially compensated by improvements to China's manufacturing base. China will likely still have some construction, but it will be more similar to most developed countries' "maintenance" construction type of activity. Even then, China has significant domestic iron ore mines that almost certainly have a cost advantage (due to lacking environmental and labor rights) over Rio Tinto's in Australia.

Rio Tinto Income Outlook

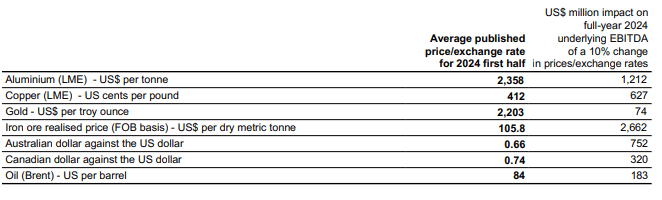

Rio Tinto provides EBITDA sensitivity analysis based on potential changes to underlying commodity prices. During the first half of 2024, the company earned an EBITDA of ~$12.1B. Higher copper prices partially made up for reduced iron ore profits. Its overall H1 realized prices and its full-year EBITDA sensitivity is shown below:

Rio Tinto EBITDA Sensitivity (2024 H1 Report)

The current price of iron ore is $98/T, though I expect it will fall to around $60/T as the glut builds over the coming twelve months, back to its glut price range of 2014-2016. Assuming a $2.66B EBITDA drop for every ~$10.6/T iron ore price change (10%) implies a ~$12.4B EBITDA decline. Based on a similarly bearish outlook for copper, I expect it will fall from its current price of $4.18/lbs to back below $3/lbs. If every 10%, or $0.41/lbs, change leads to a $627M EBITDA change, that implies a ~$1.8B EBITDA decline (with a $1.18 price decline for copper).

China appears to be stockpiling aluminum, similarly to copper, creating an artificial improvement in demand. Shanghai aluminum inventories have been high for most of this year. China also accounts for the vast majority of global aluminum smelting, with around three-quarters going to manufacturing and a quarter to construction. Thus, I have a bearish outlook on aluminum, but not to the same extent as iron ore.

Aluminum is priced at $2.49K/T, rebounding after falling earlier this year. I project its long-term price at $2.3K/T, in-line with its average price level in 2023. Fundamentally, I do not expect any material EBITDA change from Rio Tinto's H1 level for aluminum, though my outlook may change depending on whether China's manufacturing sector continues to be resilient. I also do not expect changes in gold, exchange rates, and oil - at least not material to Rio Tinto's bottom line.

Overall, I expect Rio Tinto's EBITDA will decline by ~$14.28B due to an expected continued decline in iron ore and copper. Its H1 annualized EBITDA was $24.2B, so I look toward a forward annual EBITDA of ~$9.9B ($14.3B lower). Crucially, its EBITDA should remain around $24B if iron ore, copper, and aluminum remain around their spot prices today. My projection is based on a commodity price change outlook, as its income should be stable without a decline in iron ore. Indeed, I expect many readers and analysts may find my iron ore price outlook of $60/T to be too low. Although that may seem unlikely, I believe it is the most reasonable, given the trend in China's property development.

The Bottom Line

Importantly, I expect Rio Tinto's EBITDA will be stuck in that $10B to $20B range for the next decade. Obviously, that can change with exchange rates and inflation; however, I believe the iron ore market is headed into a long-lasting glut. Perhaps higher steel needs in the rest of Asia may make up for lost demand in China someday. India's steel production is rising, but it is still only around 10-15% of that of China, so I do not expect that to matter over the coming years.

Further, I don't expect we'll ever again see a property bubble such as that which is now bursting in China, as it makes the former US property bubble look like small peas. Thus, I expect a permanent decline in iron ore demand, at least in the foreseeable future. Importantly, I do not expect global iron ore production to decline quickly in response to a glut because production costs for iron are still far above prices. For example, Rio Tinto's Pilbara iron ore mine has a unit cash cost of just $23/T.

Since the recovery in commodity prices, RIO's "EV/EBITDA" has been around 4.5X to 5.5X for most of the past seven years. It has also held that range during the stable periods in the 2000s. Thus, under my bearish commodity projections, I project its "fair" enterprise value at ~$50B to ~$100B. The company has a net financial debt of just ~$3B, so I project its market capitalization at the same range, giving it a price target range of ~$30 to ~$60.

For me, the main question is no longer if China's iron ore demand will collapse. Further, although many will likely disagree, I do not see a question of how long its iron ore demand will remain low, as I view that as being a permanent shift following the end of (what I view as) China's "make work" construction industry.

I think the main question for Rio Tinto is potential changes in manufacturing demand. My projection is primarily based on changes to construction demand from its key market, while I'm assuming manufacturing should be stable. Still, that leaves us with an extensive price target range for RIO, with a potential 50% decline in construction and manufacturing decline. Unlike construction, I expect a decline in global manufacturing demand not to be long-lasting. Still, weakening economic data in Western countries may indicate that is likely. If both manufacturing and construction demand falter, Rio Tinto's income may temporarily become negative due to a potentially large glut. Though it is around the upper end of its fair-valuation range, I maintain a bearish outlook on RIO. It may be reasonably valued today if we assume iron, copper, and aluminum spot prices will remain stable.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments