Summary

- The "cash trap" is caused by investors flocking to high-yield, risk-free assets due to Fed rate hikes. This influx into money market funds could reverse if rates drop.

- When rates fall, investors may shift from money market funds to high-yield dividend stocks to maintain income. The need for quality picks will grow in this scenario.

- High-yield, high-quality dividend stocks with strong business models and solid balance sheets could benefit most, offering both income and stability as the market evolves.

Antonistock

Introduction

A few months ago, I started discussing the "cash trap" and promised to keep bringing up new ideas to be prepared.

In case you're wondering what the cash trap is, you're not alone, as it's a relatively new phenomenon. As The Wall Street Journal wrote on June 25, the cash trap is the result of a massive surge in yields for risk-free assets like short-term government bonds.

Because short-term assets suddenly yielded more than 5% after a number of aggressive Federal Reserve interest rate hikes, investors moved their money into investments like money market funds.

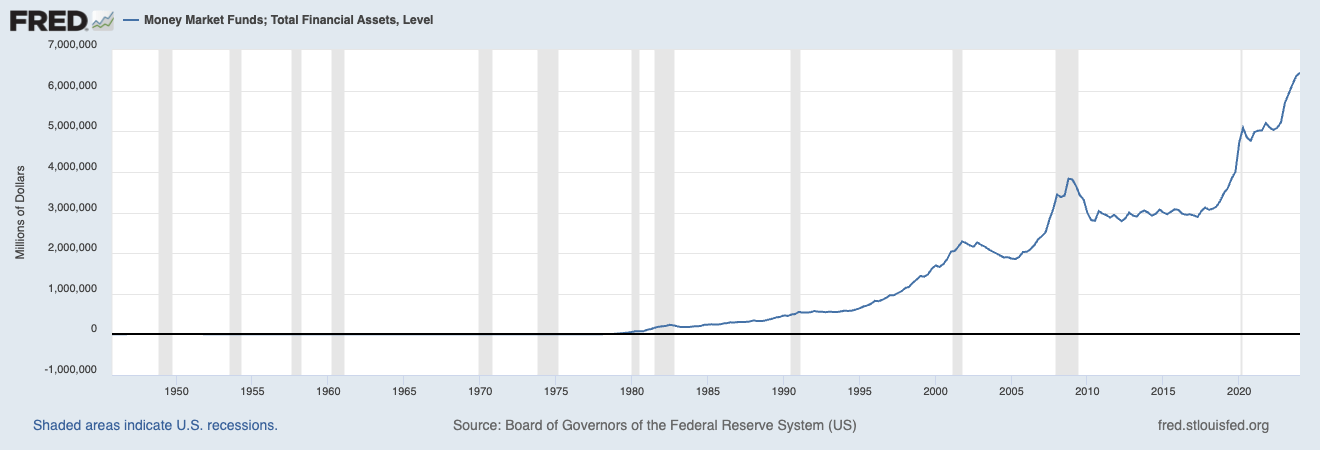

As we can see below, the total assets of money market funds were roughly $3.1 trillion in the first half of 2018. As of the first quarter of 2024, that number was $6.4 trillion!

Federal Reserve Bank of St. Louis

Again, this makes sense. Especially older investors who prefer income over growth benefitted from this, as they often kept the same income (or even improved it) while lowering financial risks.

A lot of (retired) investors who can choose between a 5%-yielding dividend stock and a 5%-yielding money market fund often pick the one with less risk - especially in light of ongoing economic challenges.

So far, so good.

There's just one problem.

Risk-free short-term rates do not tend to remain elevated forever. Although I'm in the camp of people who expect inflation and rates to remain above average on a long-term basis, I don't rule out rate cuts in the quarters ahead.

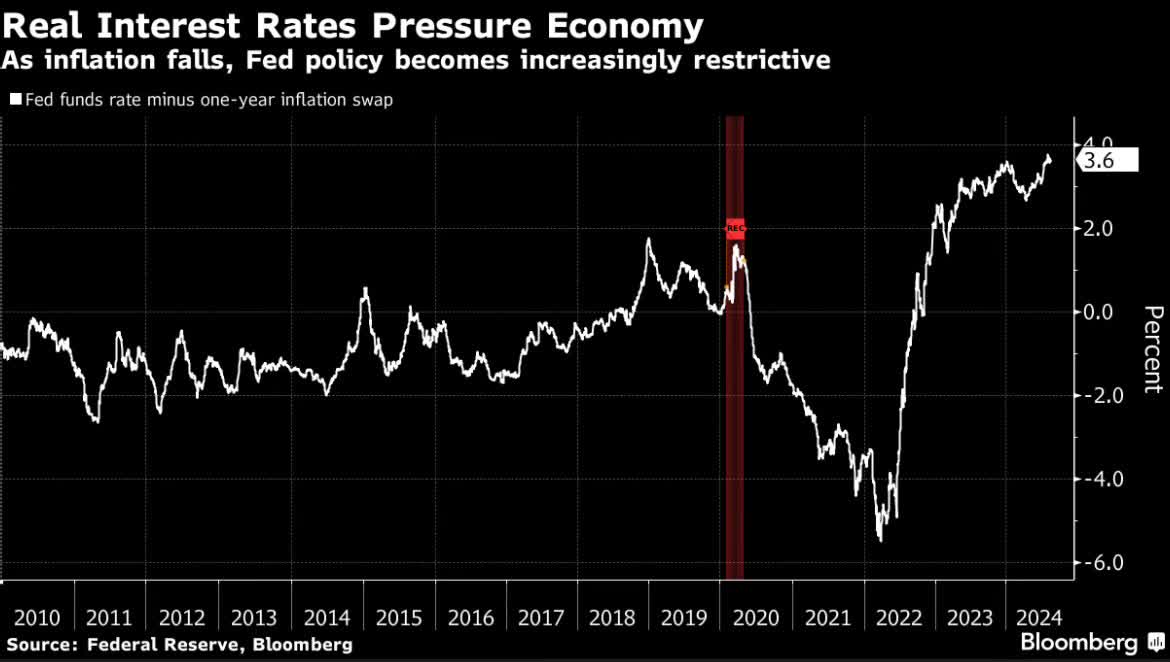

Especially if the economy continues to deteriorate, the Fed may have to cut rates. This is amplified by the fact that lower inflation rates have caused the real federal funds rate to hit a new multi-decade high last week.

Bear in mind that if the federal funds rate remains unchanged and inflation drops, the impact on the economy is more restrictive.

Bloomberg

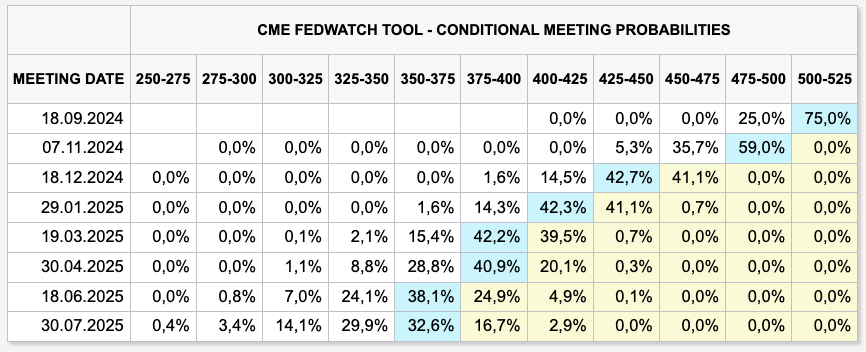

As such, we are slowly but steadily moving to a point where the Federal Reserve might have to cut. Using current federal funds futures, the market expects a rate cut in September, potentially followed by several cuts to a range of 3.50%-3.75% by mid-2025.

CME Group

However, please be aware that federal fund futures are highly volatile. If inflation comes in hot next month, we could easily be looking at a much more hawkish outlook.

That said, what matters more than correctly predicting what the next cycle of rate cuts will look like is assessing the risk/reward. Right now, the odds are much higher that we will see rate cuts in the next 12 months than prolonged elevated rates.

This could have major implications for investors.

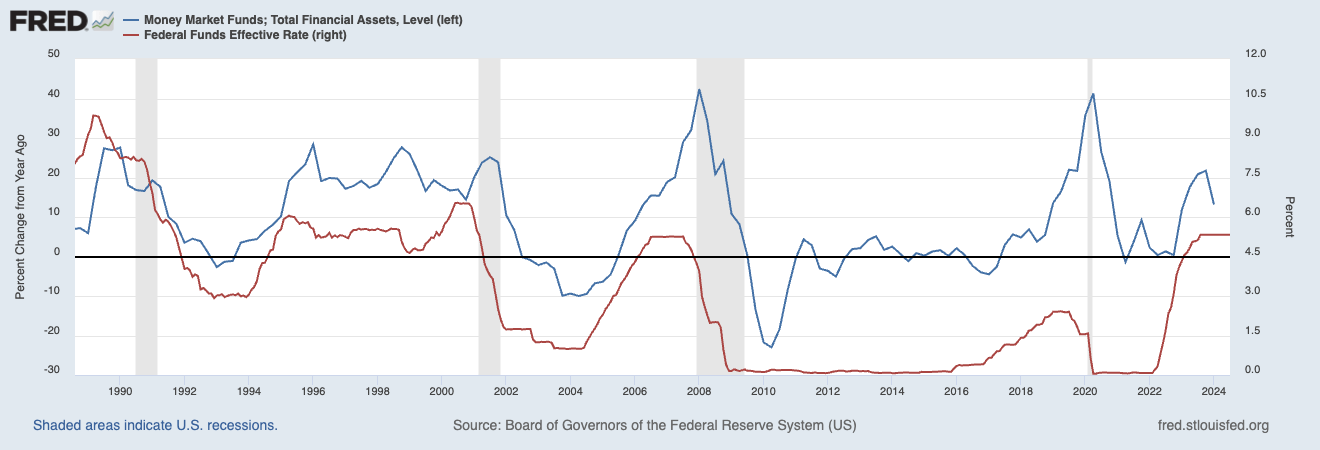

Historically speaking, rate cuts tend to cause huge money market outflows. As we can see below, rate cuts always lead to lower money market fund assets. The only exception was 2020 when rate cuts were quick and accompanied by a massive economic uncertainty due to the pandemic. This kept people invested in safe money market funds.

Federal Reserve Bank of St. Louis

If the Fed starts to cut rates, for whatever reason, investors will have to rotate money into other areas to maintain a steady level of income.

That's the cash trap.

My thesis is that this multi-trillion dollar rotation will benefit high-quality, high-yield dividend stocks. These are dividend stocks offering elevated income without elevated risks. After all, buying high-income is easy. Finding companies that provide both growth and income with subdued financial risks is much trickier.

Hence, in the second part of this article, I will present two high-yielding stocks that I expect to be fantastic alternatives once investors are "forced" to look for income in other areas.

- Both companies have juicy yields (north of 5%).

- Both companies have fantastic business models.

- Both companies have strong balance sheets.

- One of them benefits from elevated stock market volatility.

Hess Midstream (HESM) - 7.5% Midstream Income

Did I ever mention I like midstream companies?

Midstream companies are the backbone of the energy industry, as these companies own the pipelines (and related assets) to transport oil, natural gas, and a wide range of other products.

As such, they benefit from the long-term uptrend in energy production and demand without being directly dependent on the price of the commodities that flow through their systems.

That's where Hess Midstream comes in. Traditionally, the company was a Master Limited Partnership. However, in 2019, the company acquired Hess Infrastructure Partners and simplified its incentive distribution rights.

This includes the conversion to an Up-C corporate structure. As a result, the company issues a 1099-DIV instead of a K-1 form.

As its name already suggests, Hess Midstream is the offspring of the Hess Corporation (HES), which is an oil giant its bigger peer Chevron (CVX) is currently trying to buy. Even if that takeover succeeds, HESM is likely to remain a standalone company.

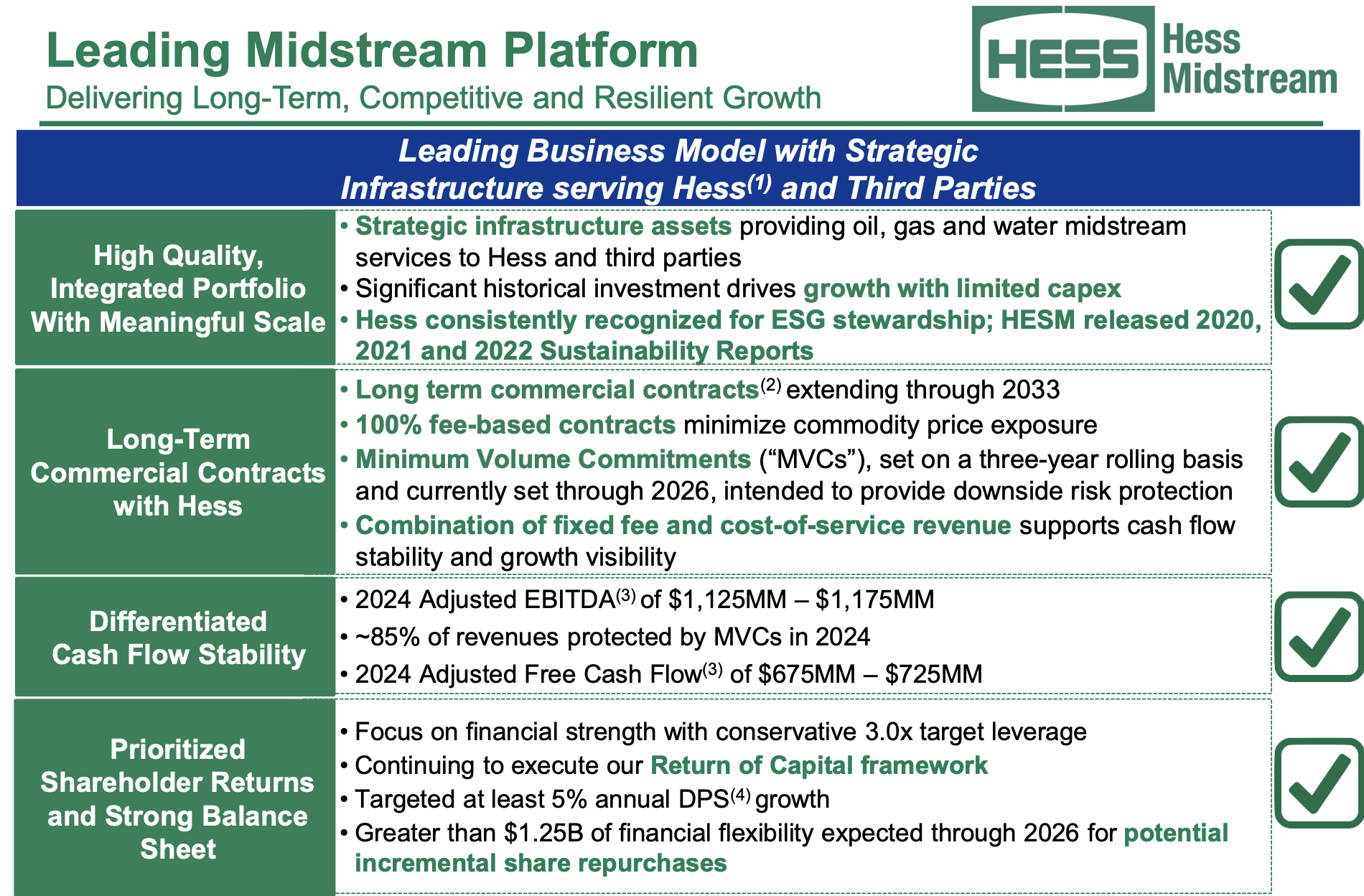

Zooming out a bit, HESM has long-term contracts with Hess. These are 100% fee-based contracts to minimize commodity price exposure. They also have minimum volume commitments to provide even more downside protection - especially at a time when oil and gas prices are so low that total output/throughput suffers.

Hess Midstream

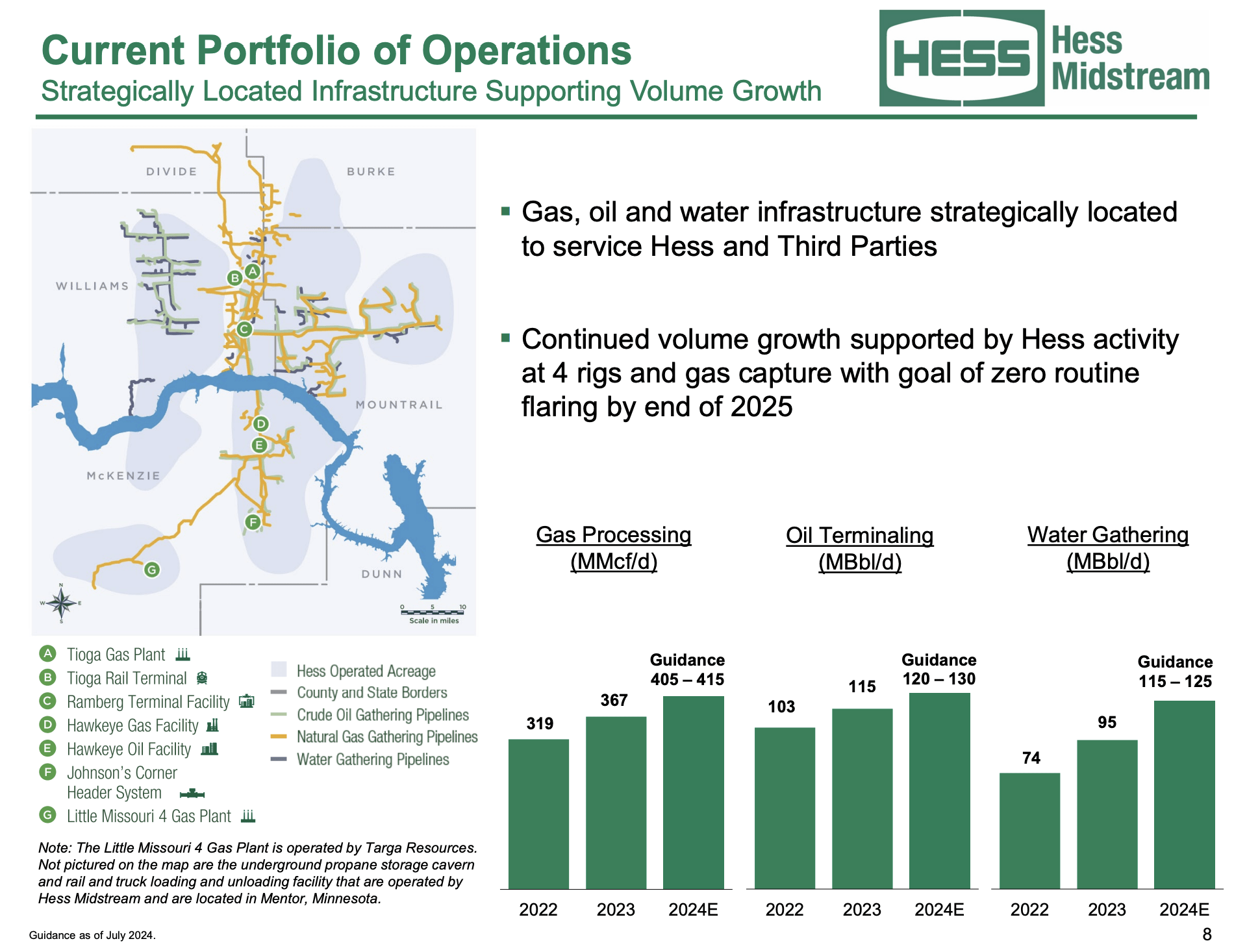

These operations are located in the Bakken Formation, a part of the massive Williston Basin.

As I wrote in a recent in-depth article on the company, in this area, the company focuses on three key segments:

- Gathering Segment: Hess Midstream's gathering segment includes an extensive pipeline network covering over 1,380 miles dedicated to transporting natural gas, crude oil, and produced water. This system ensures the efficient movement of resources from well sites to processing facilities and export terminals.

- Processing Segment: In the processing segment, the company operates state-of-the-art facilities like the Tioga Gas Plant and the LM4 Joint Venture, with a combined capacity of more than 600 MMcf/d. These facilities play a crucial role in extracting value from natural gas and NGLs extracted from the Bakken and Three Forks shale plays.

- Terminaling Segment: Hess Midstream's terminaling segment focuses on key facilities like the Ramberg Terminal and the Tioga Rail Terminal. These facilities enable the storage, transportation, and export of crude oil and NGLs.

Hess Midstream

Currently, this business is booming.

In its recently released second-quarter earnings call, the company reported significant growth, with throughput volume growth of 17% for gas processing, 17% for oil terminaling, and 43% for water gathering.

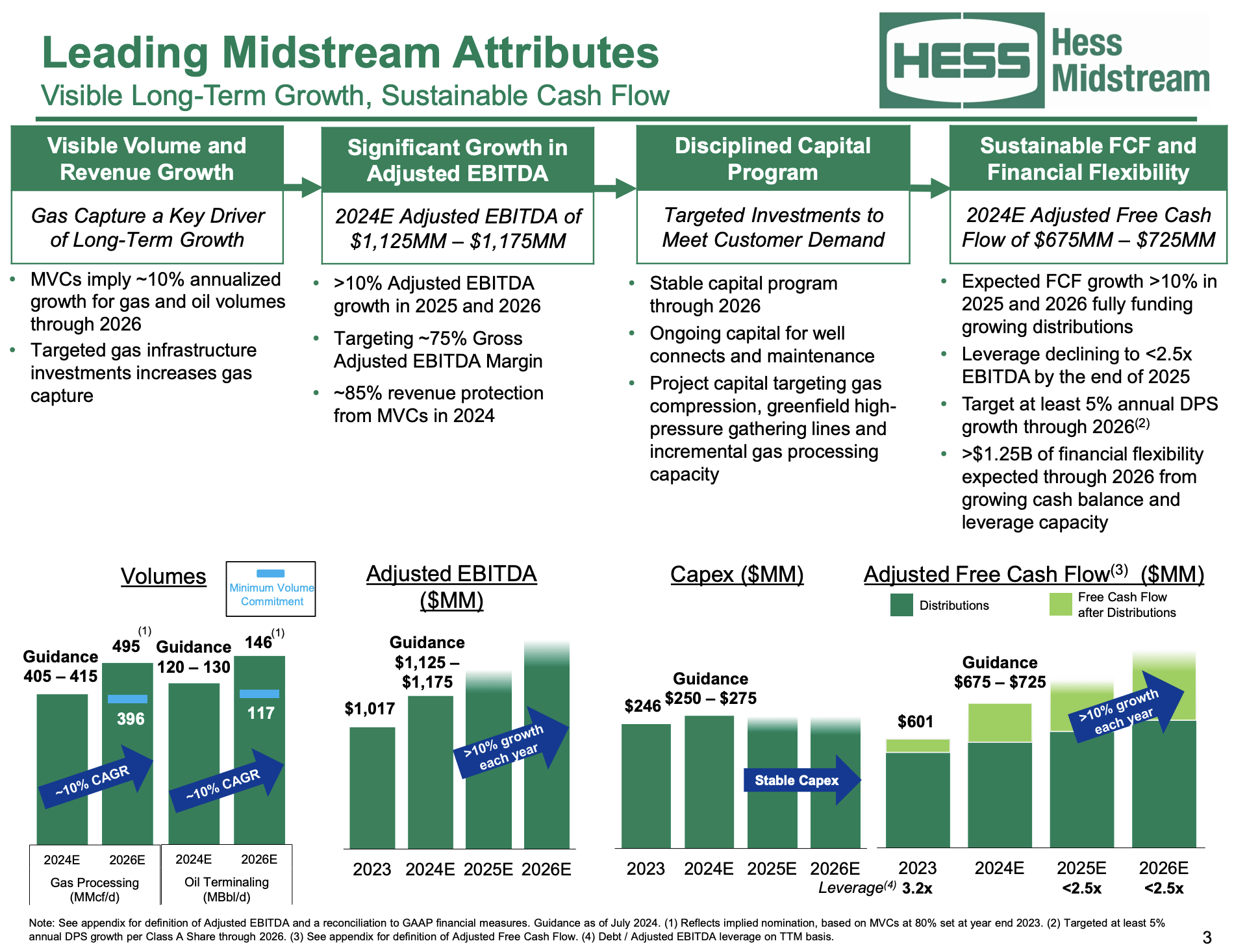

Looking forward, the company forecasts a 10% annualized growth rate in gas and oil volumes through 2026, which is expected to drive more than 10% annual growth in adjusted EBITDA.

Hess Midstream

Moreover, as we can see in the overview above, the company's free cash flow covers its distributions.

Unlike some of its peers, the company's cash flows fully support capital expenditures and shareholder distributions, with free cash flow growth expected to be at least 10% in 2025 and 2026.

It also expects to maintain a healthy balance sheet with a net leverage ratio of less than 2.5x EBITDA.

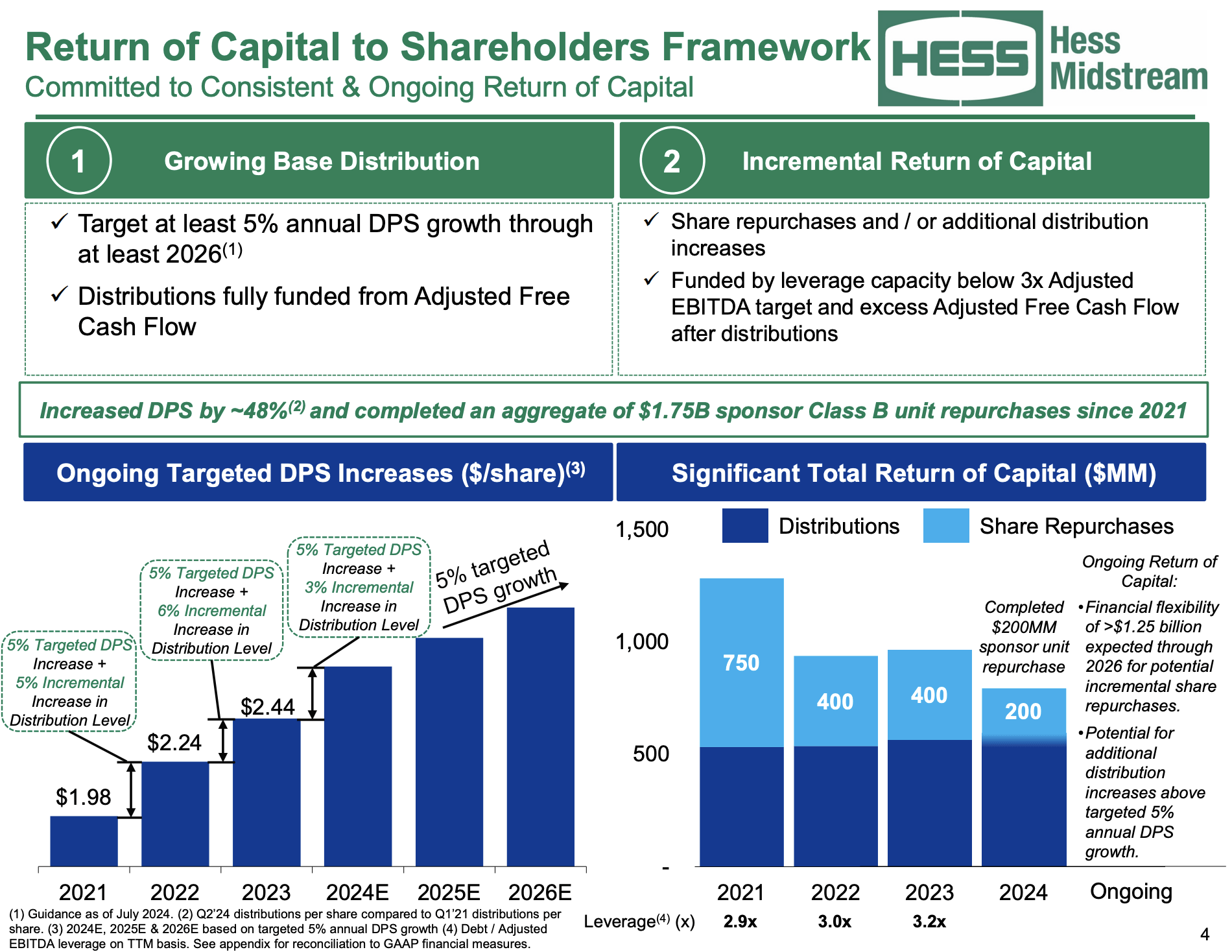

This is fantastic news for shareholders. Currently, HESM pays $0.6677 per share per quarter in distributions. This implies a 7.3% yield.

Going forward, the company aims to grow this distribution by at least 5% per year, supported by share repurchases to improve the per-share value of the business.

Hess Midstream

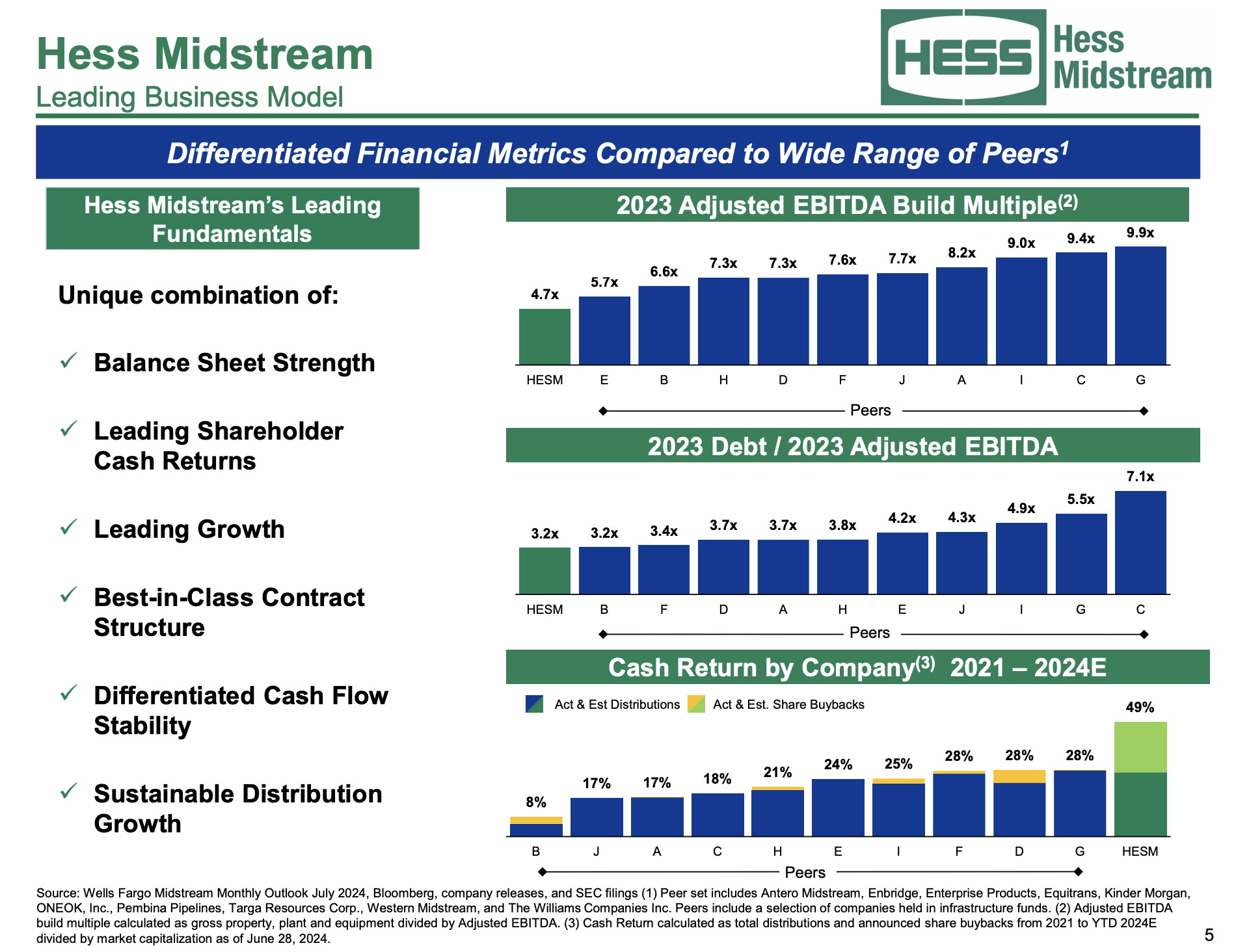

The company is also cheap. Going into this month, it traded at just 4.7x EBITDA, making it one of the cheapest stocks in its industry. It also has one of the healthiest balance sheets and the highest total cash return in the 2021-2024E period.

If I did not have a major position in Antero Midstream (AM), I would be a buyer of HESM as well.

Hess Midstream

At current prices and in light of a potential multi-trillion dollar money market rotation, I rate HESM a Strong Buy.

CME Group (CME) - The Market Is About To Uncover A High-Yield Gem

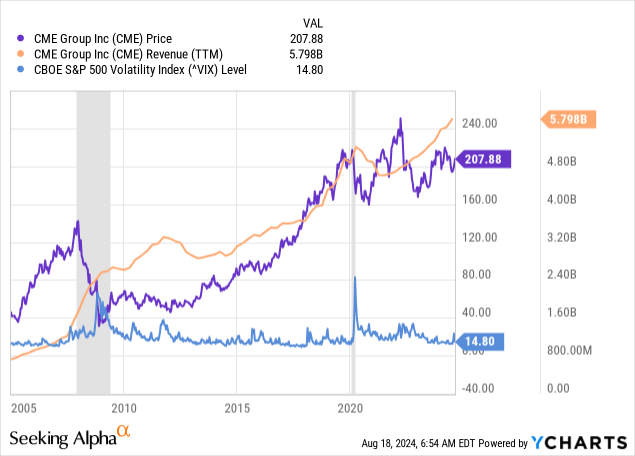

Especially in a time of elevated volatility, I keep going back to CME Group, my only investment in the financial sector - at least for now.

Especially at current prices, I believe CME is the perfect mix of growth and value. It also has the second-highest profit margin of the S&P 500 at more than 55%.

For starters, CME has a transaction-focused business, as it is one of the world's biggest exchange owners. Here's a handy overview I used in an in-depth article on the company earlier this month:

- CME (Chicago Mercantile Exchange) offers a diverse range of futures and options contracts, including interest rates, equity indices, foreign exchange, agricultural commodities, and more.

- CBOT (Chicago Board of Trade) trades futures and options contracts for agricultural products, interest rates, and equity indices.

- NYMEX (New York Mercantile Exchange) specializes in energy and metals trading, including contracts for crude oil, natural gas, and various metals like gold and silver.

- COMEX (Commodity Exchange, Inc.) focuses on metal products, offering contracts for gold, silver, copper, and other base metals.

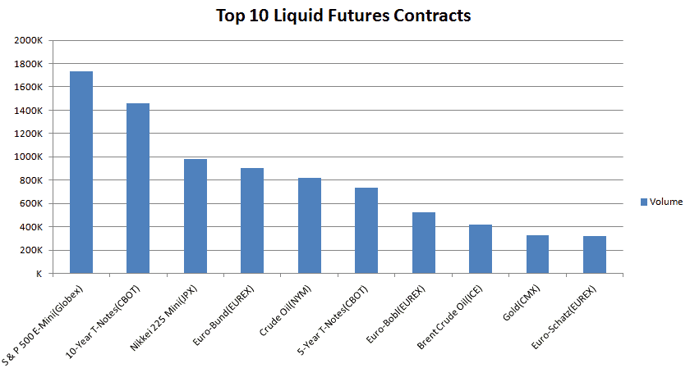

These products include the S&P 500 e-mini, the most liquid futures contract in the world. In fact, CME owns more than just one of the world's "most important" future contracts.

TradingSim

What this means is that CME benefits from secular growth and downside protection.

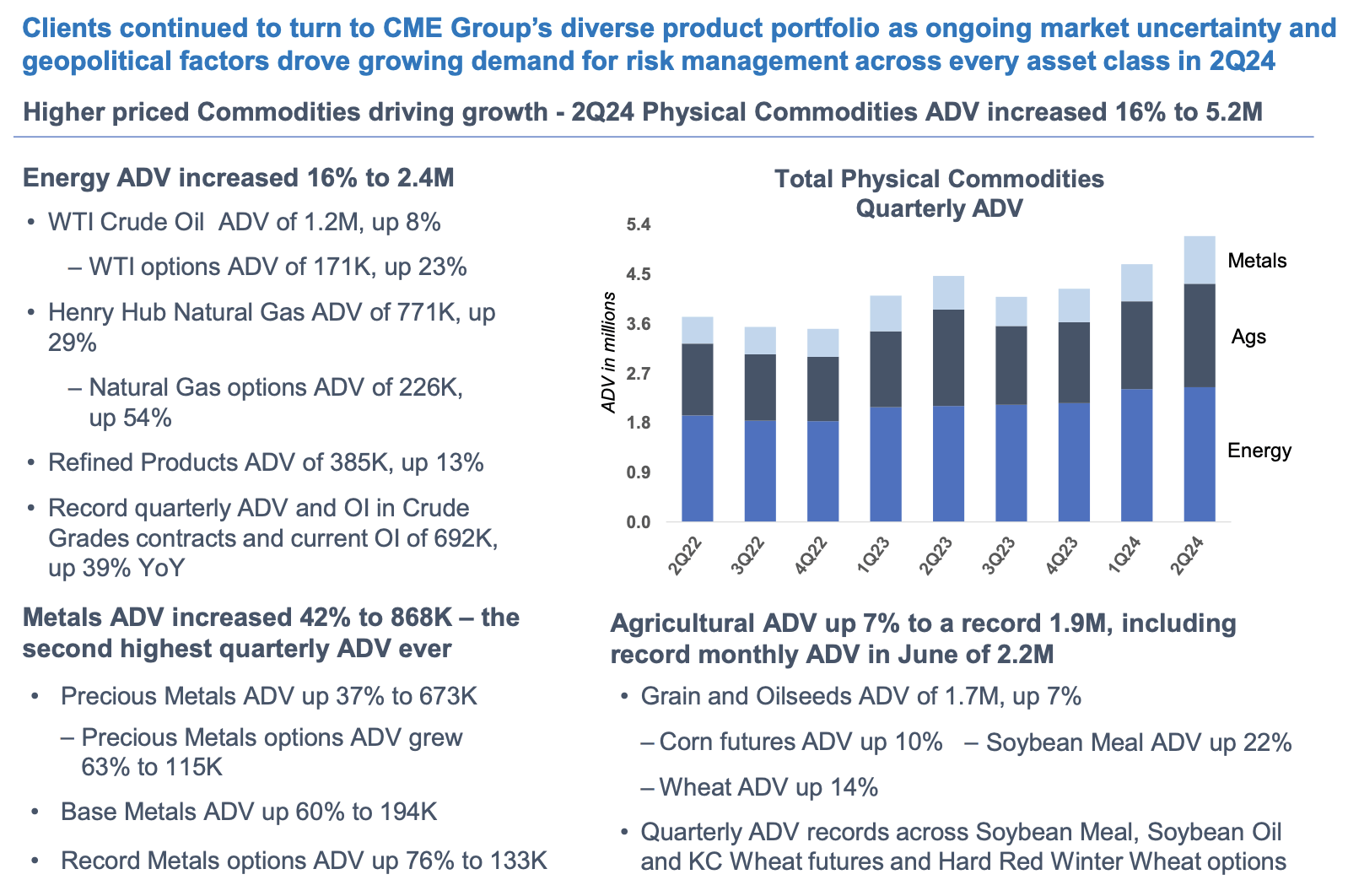

- Secular growth comes from the increasing importance of futures and options in hedging processes and global trading. By launching new products and optimizing its current offering through partnerships with Google Cloud and others, the company remains on top of this trend - regardless of new industry entrants. It also helps that CME has exclusive licenses with companies like S&P Dow Jones Indices, of which it owns more than a quarter. The company's portfolio is so impressive that even in the low-volatility environment of 2Q24, it saw record ADVs in key areas like commodities (and many others).

CME Group

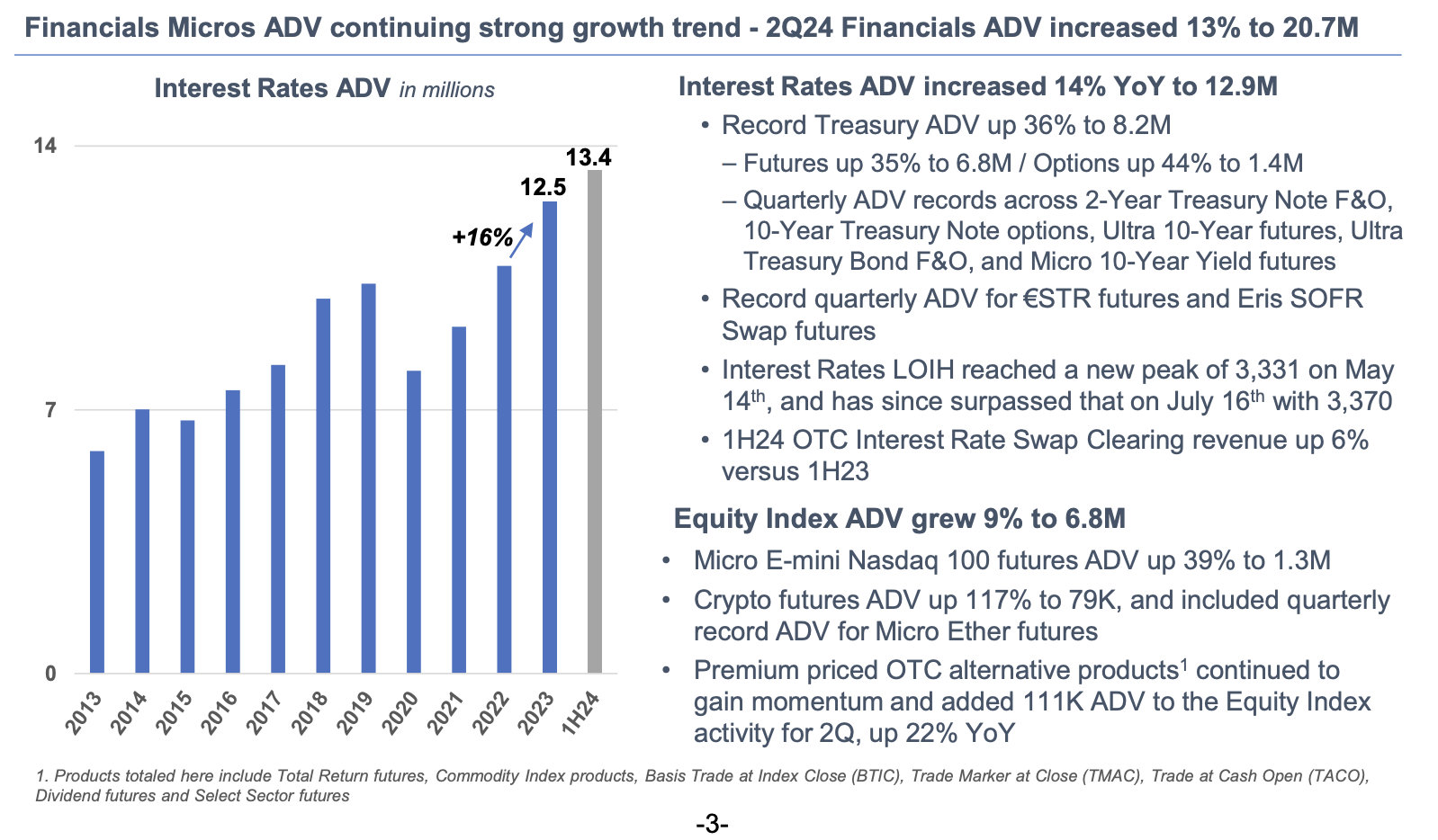

Even better, because of interest rate uncertainty, the company's interest rates ADV (average daily volume) has been on a tear since the pandemic.

CME Group

- Downside protection is provided by the benefit of elevated volatility whenever the market goes down. While the CME stock price tends to fall when markets weaken, underlying revenue often accelerates.

Data by YCharts

Data by YCharts

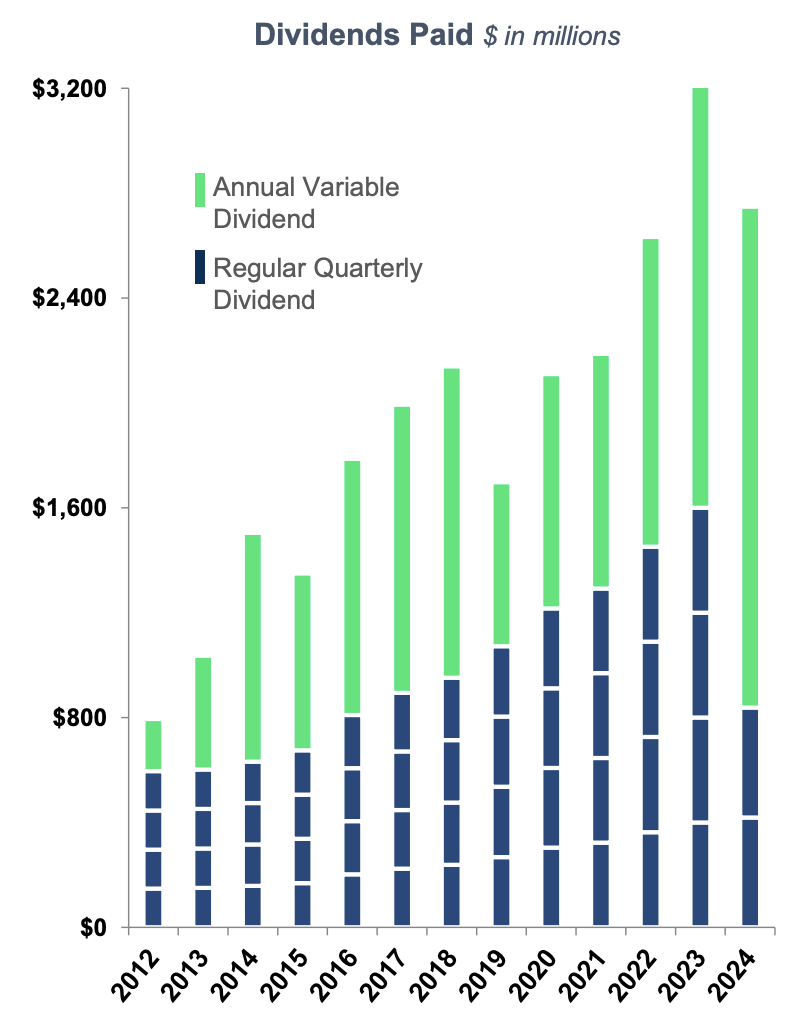

With regard to its yield, the company has a regular quarterly dividend and one special dividend - announced in 4Q and paid in 1Q.

Currently, the base dividend yields 2.2% ($1.15 per month per share). This base dividend has been hiked by 4.5% on February 8.

The special dividend is variable. Usually, CME Group distributes roughly 100% of its free cash flow to shareholders. It can do this because it has a fantastic balance sheet with a double-A rating and no need for its cash, as CME is not an M&A-focused company.

This year, analysts expect the company to generate $3.8 billion in free cash flow. This translates to 5.1% of its market cap. Hence, based on its current price, I expect a full-year yield of roughly 5% (including its special dividend).

CME Group

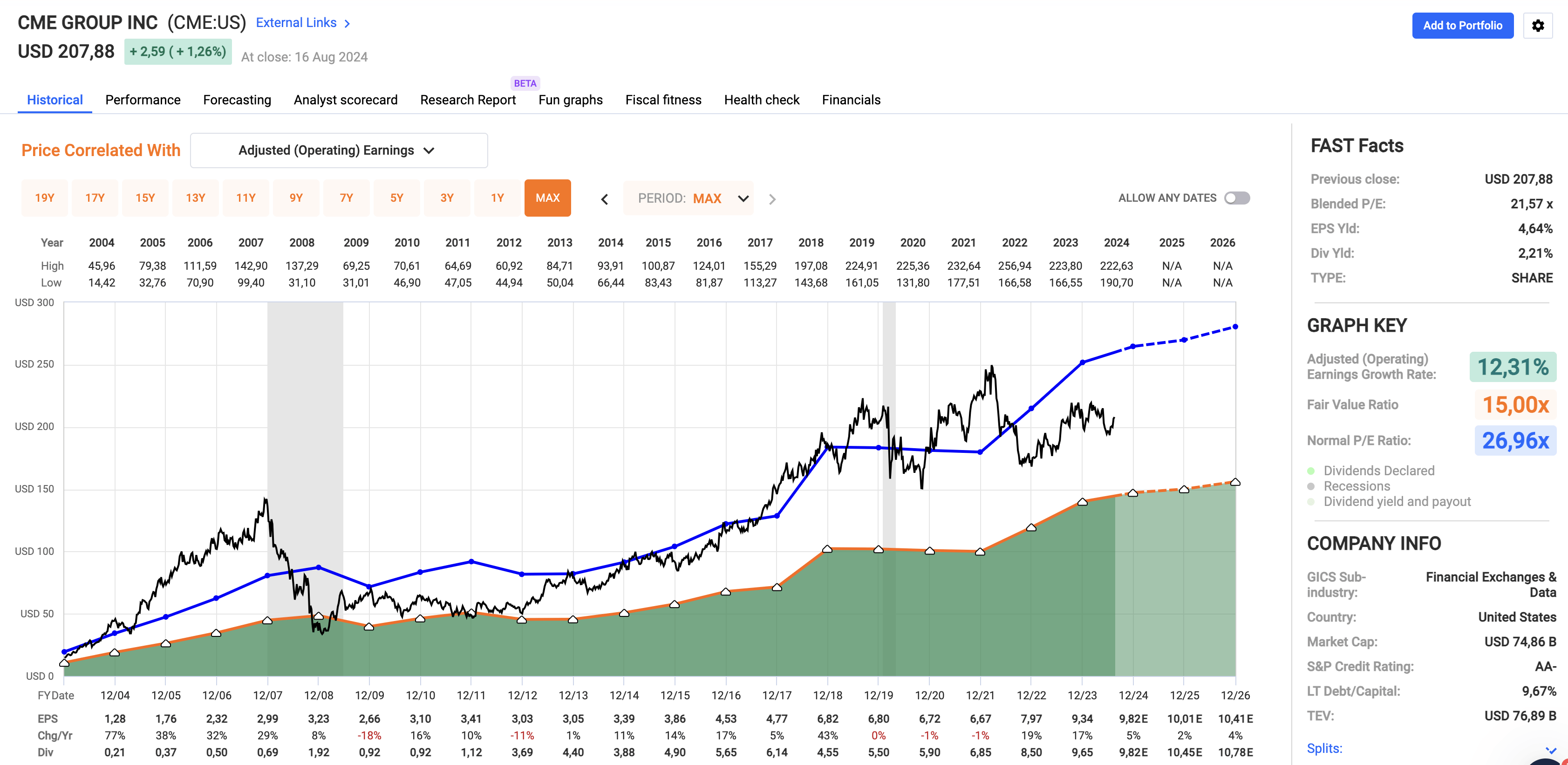

The valuation isn't bad, either!

CME has a normalized P/E ratio of roughly 27x. Although that may seem elevated, it is warranted, as we are dealing with an ultra-high margin company with a stellar business model.

FAST Graphs

If we assume 2-5% annual EPS growth through at least 2026, we get a fair stock price of $280, 35% above the current price. This is one of the many reasons why CME has become one of my favorite stocks at current valuations.

Like HESM, I'm giving CME a Strong Buy rating as well.

Takeaway

The "cash trap" presents a unique challenge for investors relying on short-term, risk-free assets.

With the potential for Federal Reserve rate cuts on the horizon, the once-attractive yields of money market funds could start falling, likely pushing investors to seek alternative income sources.

This is where high-quality, high-yield dividend stocks like Hess Midstream and CME Group come into play.

These companies not only offer elevated yields but also come with strong business models and balance sheets, making them ideal candidates for investors needing to maintain income levels in a changing rate environment.

They aren't just attractive, but two of my favorite high-yield plays in this market.

Comments