Summary

- As discussed in our previous coverage, the start of productions and shipments of SMCI's proprietary DLC solution is a key catalyst for the stock.

- Margin compression risks remain a key overhang on SMCI's valuation outlook, but the continued ramp of DLC shipments will offer sustained compensation through competitive unit economics and economies of scale.

- Management's latest target DLC penetration rate of 25% to 30% of new global data center deployments over the next 12 months is also a material jump from previous expectations.

- This is a game changer for SMCI, with ensuing fundamental benefits to profitability and cash flows still underappreciated at the stock's current price.

JHVEPhoto

In our last coverage on SMCI (NASDAQ:SMCI), we had discussed how its first-mover advantage in providing direct liquid cooling (“DLC”) solutions at scale in the AI-first era represents a key near-term growth driver and catalyst for the stock. And in the latest earnings update, management had reaffirmed a strong outlook for DLC shipments through FY 2025. Specifically, the company has quantified the DLC monetization outlook, with expectations for deployments in new global data centers to reach 25% to 30% over the next 12 months. This has effectively reinforced confidence in SMCI’s robust outlook for DLC monetization, which is critical to providing direct alleviation to ongoing margin compression risks.

In the following analysis, we provide an update to our previous fundamental analysis and estimates based on SMCI’s latest earnings update, with focus on implications of the company’s DLC monetization opportunity. The advent of robust AI interest has created intensifying demand for power efficient infrastructure without compromising performance. And SMCI’s DLC solution is a complementary companion to the ramping AI transformation, given its reduced manufacturing cost structure and competitive total cost of ownership (“TCO”) offered to customers.

SMCI remains the only server company that can currently ship DLC solutions at scale. With volumes ramping up for deployment, the ensuing growth opportunity underpinning the stock’s upside remains significantly underappreciated at current levels.

SMCI’s DLC Opportunity is Here

In our previous coverage, we had discussed that the start of DLC shipments from SMCI could represent a near-term catalyst for multiple expansion in the stock. This is because DLC represents a unique near-term growth driver for SMCI, given the technology’s capability in unlocking incremental power efficiency and performance gains in the AI- and data-first era.

On one hand, SMCI’s DLC solution offers competitive TCO for customers, enabled through a combination of improved scalability, and reduced time-to-deployment and time-to-online for customers. Specifically, the compatibility of SMCI’s newest DLC technology with its proprietary rack-scale plug and play solutions improves scalability for customers by optimizing time-to-deployment and time-to-online for customers.

For instance, management had disclosed that smaller facilities and/or older data centers looking to upgrade existing infrastructure can leverage DLC integration through its upcoming Data Center Building Block Solutions (“DCBSS”) – one of its most enhanced rack-scale plug and play developments – and reduce deployment times to less than one year. Meanwhile, brand new data centers adopting DCBSS can reduce the average build time of about three years to two years, underscoring significant time and cost savings and, inadvertently, competitive ROI metrics for SMCI’s customers. The compatibility of SMCI’s newest DLC solution with its building block architecture effectively addresses increasing CIO demands for optimization, with many looking to expand their respective AI compute capacity without the need to materially change the “physical footprint and power needs of their current infrastructure”.

SMCI’s DLC solution also directly reduces the time to deploy and take new data centers online due to their lower electrical power requirement. As discussed in our last coverage, SMCI’s DLC solution is capable of reducing data center power consumption by up to 40%. This reduced power requirement does not only save costs, but also effectively minimizes customers’ exposure to long power budget approval wait times from energy suppliers, hence a shorter time-to-deployment and time-to-online for new data centers.

In addition to scalability and improved time-to-deployment and time-to-online efficiencies, SMCI’s latest DLC solution also offers “higher performance and better uptime” compared to traditional air-cooling technologies in supporting increasingly complex and compute intensive AI chips. Taken together, SMCI’s DLC solution is expected to deliver up to 3% in initial capex reduction for adopting customers, and up to $60 million in net opex reduction over five years, contributing favourably to TCO considerations in the board room.

Meanwhile, on the other hand, SMCI can also manufacture its DLC solution at a lower cost than the traditional air-cooled solution, especially as production volumes scale up at its newest Malaysia and Taiwan facilities in the coming months. The latest DLC solution also entails greater scalability given its reduced production-to-delivery completion timeline to as low as two weeks. This compares to the average production-to-delivery completion timeline of four to 12 months observed for traditional air-cooling solutions.

The competitive cost structure of producing DLC solutions at SMCI, and the continued scale of volumes shipped will be key to offsetting the impact from early-stage ramp-up costs. It will also compensate for ongoing adverse implications from SMCI’s prioritization of large-scale data center deal wins at the expense of profit margins, which has been a key multiple-compression risk for the stock in recent months.

And SMCI is showing signs of timely execution on this front. Initial DLC shipments in June and July totalled more than 1,000 units, with related sales contributing more than 70% of revenue generated from enterprise and cloud service provider (“CSP”) markets. These levels represent about 15% penetration of new data center deployments worldwide, with SMCI currently accounting for up to 80% of global liquid cooling solution market share. And management is targeting 25% to 30% penetration of new global data center deployments with SMCI’s proprietary DLC solution over the next 12 months – a materially higher proportion than current levels disclosed during COMPUTEX ’24 and SMCI’s latest earnings update. This represents a key margin accretive factor in the near-term, given improved economies of scale.

The ensuing economies of scale benefit is further corroborated by the record-high order backlog for SMCI’s DLC solution. While management had disclosed that DLC shipments have represented 70% of enterprise and CSP revenues in F4Q24, the figure would have been higher if it were not for the supply shortage on key components for the product. About $800 million in DLC revenue previously earmarked for realization in F4Q24 were delayed into July due to the supply bottleneck. The constrained supply is expected to ease through FY 2025, which will be complemented by the continued ramp-up of production volumes in Malaysia and Taiwan, driving realizable unit economic improvements critical for margin accretion.

Fundamental Considerations

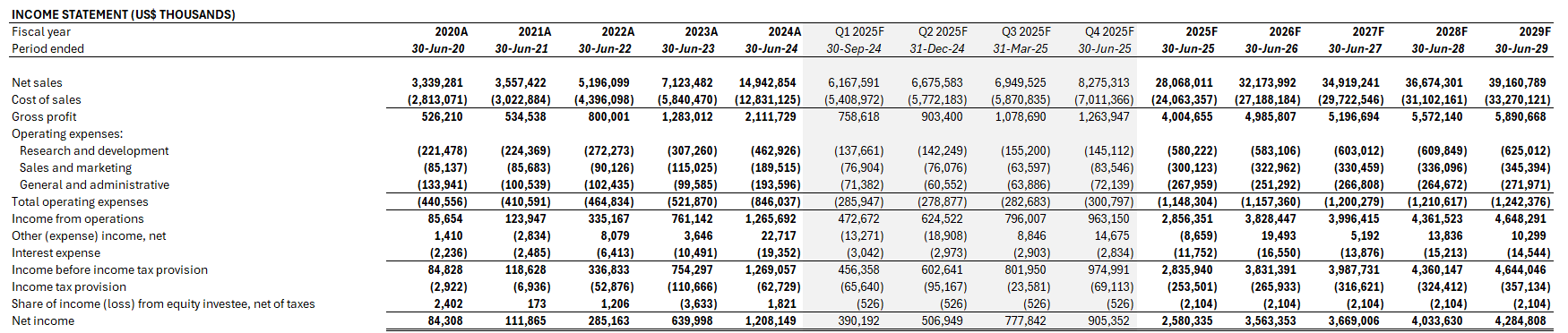

Adjusting our previous forecast for SMCI’s F4Q24 results and F1Q25 outlook, we estimate current year revenue growth at 88% y/y to $28.1 billion. This is consistent with management’s high-level FY 2025 revenue target of $26 billion to $30 billion, underpinned primarily by the robust demand environment for SMCI’s new air-cooled and DLC AI GPU clusters.

Author

Our near-term growth forecast considers incremental detail on the monetization prospects of DLC provided by management in the latest earnings update. Specifically, management’s expectations for 25% to 30% DLC penetration in global new data center deployments over the next 12 months is a significant jump from current levels considered in our previous estimates. Admittedly, management deepening push for “liquid cooling as the mainstream product solution” in next-generation data center deployments in the AI era might entail high customer acquisition costs. This risks extending current margin compression headwinds, as management continues to prioritize large-scale data center deal wins with a competitive pricing strategy.

However, the robust DLC order backlog, as well as the technology’s reduced manufacturing cost structure entails a competitive scalability advantage. This effectively provides a greater margin to absorb incremental short-term customer acquisition costs, with additional deal wins driving further operating leverage improvements and ensuing margin accretion. These considerations in our updated estimates is corroborated by management’s commitment to maintaining SMCI’s cash burn run-rate based on the FY 2025 growth guidance provided.

Mehdi Hosseini

And then a question I have for Charles. Obviously, you've done a good job of doubling revenue in fiscal year '24. But you also had a negative free cash flow of $2.6 billion. And if I were to look at the high end of your revenue guide for fiscal year '25, you're on track to double revenues again. Does that mean that you're going to need to burn another $2.5 billion to $2.6 billion of free cash flow to hit those revenue targets?

Charles Liang

Not necessarily. I mean if we try to be very aggressively growing market share maybe, if [for] example we forecast on $30-something billion [revenue], right, so in that case, we may need more. But if we try to focus on below $30 billion then not necessary.

Source: SMCI F4Q24 Earnings Call Transcript

The robust demand outlook for SMCI’s rack-scale plug-and-play solutions, including its latest DLC AI GPU clusters, which is critical for margin expansion going forward, is further corroborated by robust industry capex allocation to new data centers. For instance, Amazon (AMZN) has earmarked more than $100 billion on data center investments in the next 10 years. Other hyperscalers like Meta Platforms (META), Microsoft (MSFT), and Google (GOOG / GOOGL) have also announced tens of billions of dollars in capex spend on AI infrastructure alone in the current year.

The strong demand outlook will be supportive of management’s commitment to bringing SMCI’s gross margins back to the 14% to 17% target range by the end of FY 2025. This is key to assuaging peak investors’ concerns over SMCI’s dire profitability and cash flow growth outlook, despite eyewatering revenue growth in recent quarters. Specifically, SMCI finished FY 2024 with 38% sequential revenue growth in the June quarter. But the strong growth performance was overshadowed by a 12% sequential decline in earnings, weighing on cash flows critical to the stock’s valuation outlook. This was primarily the result of management’s continued prioritization of large-scale data center deal wins through a competitive pricing strategy, which was further exacerbated by DLC production ramp-up and exploration costs during the June quarter.

Looking ahead, SMCI’s gross margin headwinds have likely bottomed, with management calling the F4Q24 a “unique quarter”:

Okay. For June, it's really a unique quarter because we deploy lots of liquid cooling and we pay lots of exploration cost. So that makes our June gross margin much worse.

Source: SMCI F4Q24 Earnings Call Transcript

This is supported by the continued ramp of DLC AI GPU cluster shipment volumes from both its Taiwan and Malaysia facilities through FY 2025. Accelerating DLC shipments will be key to unlocking the new technology’s intended manufacturing cost efficiencies when compared to traditional air-cooling solutions, and also drive incremental economies of scale by realizing the record-setting order backlog.

The upcoming start of production of SMCI’s newest DCBSS solution will further complement margin accretion from the ramp of DLC AI GPU cluster deployments through FY 2025. Specifically, DCBSS will be another key margin accretive factor for SMCI in the near-term, as the new solution entails “more software, onsite deployment, maintenance and end-to-end management service” deployments which generate greater profitability.

Author

Valuation Considerations

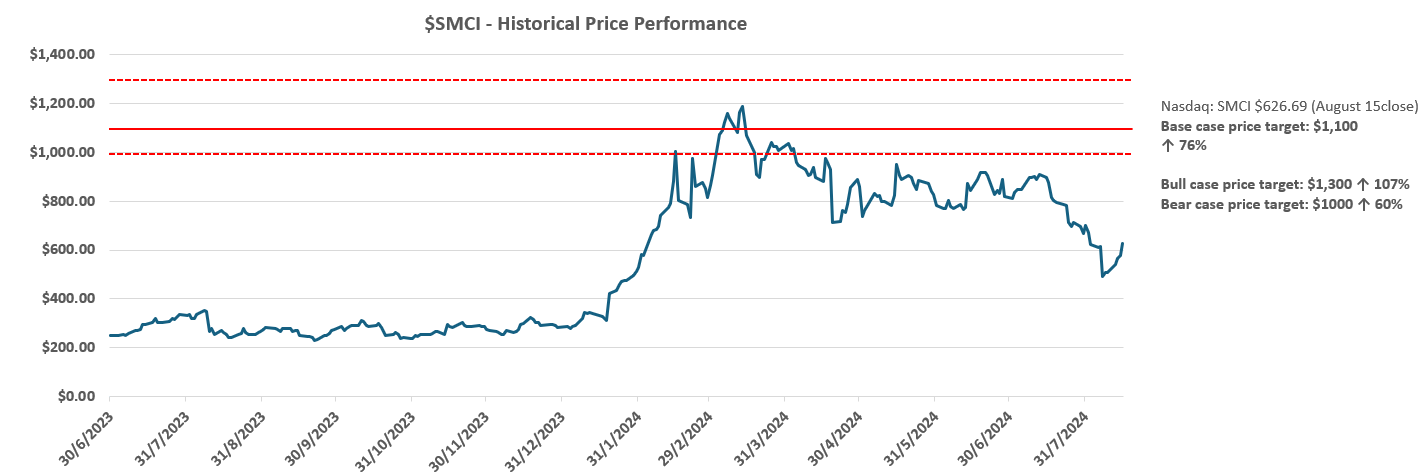

Based on the foregoing analysis, which confirms robust monetization of additive DLC growth opportunities ahead, we are maintaining our base case price target for SMCI at $1,100 apiece.

Author

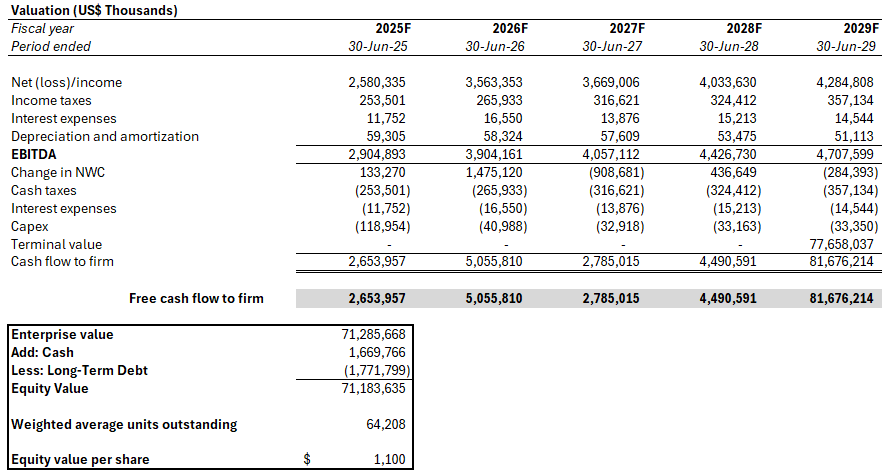

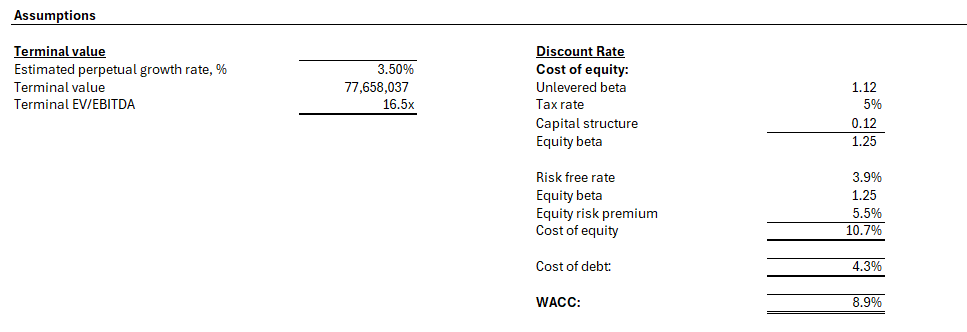

The price I derived based on the discounted cash flow approach, with consideration of cash flow projections taken in conjunction with the fundamental forecast discussed in the earlier section. The analysis considers a WACC of 8.9%, which is in line with SMCI’s risk profile and capital structure. We have also applied an estimated perpetual growth rate of 3.5% to FY 2029E EBITDA to determine SMCI’s terminal value. The valuation assumption applied is in line with the upper range pace of economic expansion observed across SMCI’s core operating regions, and is reflective of its role as a key beneficiary of the AI infrastructure build-out cycle ahead.

Author

Author

Risks to Consider

From a valuation perspective, the SMCI stock has been inherently volatile amid burgeoning investors’ interest in AI developments. The stock has increased its value by more than 300% during the first three months of 2024 alone, before rapidly paring gains almost half since. Investors continue to grapple with the dichotomy between SMCI’s mission-critical role in supporting ongoing AI developments which entails sustained growth, and its uncertain profit outlook which introduces multiple compression risks to the stock’s valuation. SMCI’s upcoming 10-for-1 stock split in October could lead to further volatility. Although stock splits result in no fundamental change, they have historically been accompanied by large price swings.

Meanwhile, from the fundamental perspective, near-term supply chain constraints facing the DLC solution’s ramp trajectory remain a key risk overhang. Although management expects these constraints to ease through FY 2025, with improved production volumes for SMCI’s DLC solutions going forward to support realization of intended cost efficiencies, a protracted shortage of key components could elevate the business’ exposure to execution risks, and result in further multiple compression for the stock. However, SMCI remains well-positioned in achieving the lower-end of its FY 2025 revenue guidance at $26 billion, which would be accretive to profit margins. As mentioned previously, management also does not expect further intensity to SMCI’s cash burn run-rate in realizing its FY 2025 growth outlook. This is favourable to cash flows underpinning the stock’s valuation outlook.

Conclusion

We believe management’s continued execution on ramping DLC shipments through FY 2025, alongside the margin accretive introduction of DCBSS later this year will be key to unlocking a sustained recovery rally for the stock. This is supported by tangible fundamental benefits, given competitive unit economics in the production of DLC solutions compared to its predecessors, alongside incremental economies of scale benefits as volumes ramp-up. Realization of said earnings benefits are further reinforced by SMCI’s strong deal pipeline, which also provides validation to the scalability advantage of its proprietary rack-scale plug-and-play and building block solutions. Taken together, the SMCI stock at current levels represent an opportunity for further upside, especially as short-term customer acquisition costs in the underlying business drive long-term economies of scale benefits to cash flows underpinning its valuation prospects.

Comments