Summary

- AMC Entertainment's financial position remains precarious, with negative working capital and higher interest rates following the refinancing deal.

- Consumer trends and reduced spending capacity pose risks to AMC's revenue recovery and operating income, potentially leading to further declines.

- Despite debt refinancing reducing immediate bankruptcy risks, the high interest rates and dilutive terms may lead to an inevitable failure of AMC's equity.

- AMC remains dependent upon equity investor hope. Should its market capitalization rise, it may raise enough capital to deleverage. Should it fall, its ability to raise capital will too.

- AMC's key balance sheet risks are now extended to 2029, but they may be pushed forward if its operating income remains negative.

Marti157900

Going back to 2020, I have had a bearish outlook on AMC Entertainment Holdings, Inc. (NYSE:AMC). In my view, the company's core issues were growing rapidly in the years before 2020 but were greatly exacerbated that year. Of course, from an investment standpoint, it eventually came out ahead as it gained so much "meme stock" traction that its equity value rose enough that it sold shares and raised significant capital. The company has worked hard at burning that capital since, seeing its working capital fall from nearly $500M to -$575M in Q2 2024.

I followed this with a bearish outlook in early January, indicating my view that the company would go bankrupt despite a recovery in movie ticket sales. It has lost ~90% of its value since then. I updated my view at the end of 2023 in "AMC Entertainment: Dilutive Equity Sales Will Not Work Forever," explaining that its operating income was likely insufficient to attract needed external capital. It has lost around a quarter of its value since December, falling to the high $2 range before rising above $5 following its successful refinancing of around $2.5B debt to a 2029 maturity.

Although the refinancing should extend its life, investors should be aware of the nature of the new loan, which is at a double-digit interest rate. Despite this, its working capital remains quite negative, indicating it could still face financial issues from other sources, particularly if its operating income continues to falter. AMC's life expectancy as a zombie enterprise may have been extended, but its operational and financial position remains precarious, warranting an updated in-depth analysis.

AMC's Risks Compounded By Cyclical Trends

Previously, my view on AMC was that its operational position should remain decent, while its balance sheet was alarming. Since then, its balance sheet has remained concerning, but the extension of maturities pushes that issue into 2029. However, as I've discussed in many articles, we're also seeing more clear negative trends in consumer data. From 2022 to 2023, economic weakness was isolated mainly to the manufacturing sector. Today, there are clearer signals that people are reducing luxury spending due to lower discretionary incomes.

I do not expect a significant recession to result in a massive decline in AMC's sales. However, even a slight decrease in its sales would likely be enough to hamper its operating income at a critical period where it must show positive operating income. Of course, the stock is down so much that a glimmer of hope for the survival of its equity may be sufficient for it to gain value, depending mainly on its ability to mitigate negative cash flow.

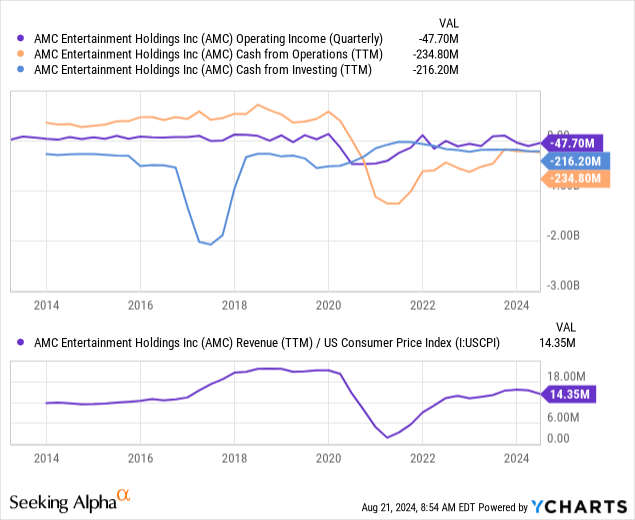

AMC's revenue failed to recover, particularly on an inflation-adjusted basis. That figure also shows a clear negative trend, indicating potential further declines in its core operations. Additionally, its cash-from-operations remains problematically negative at -$234M. Its investment cash flow is also negative due to chronically high capital expenditures. As mentioned in its last call, the company's CapEx will be upgraded. Although it may need to do so to compete, I disagree with the statement, "Our finances prudently allow through capital expenditure dollars," given its chronically negative operating cash flows. See below:

Data by YCharts

Data by YCharts

I believe any benefits from its debt maturity are offset by lower operating income and inflation-adjusted revenues. It may be that its sales are falling due to weakened consumer spending or the long-term impacts of the Hollywood strikes last year. As I detailed in my previous AMC article, I viewed the strikes as a significant negative headwind facing the stock in 2024. The company confirmed it faced issues from this in Q2; however, it may be that it points to the problem of covering for naturally lower demand. Many large movies have been released throughout 2024 but have had far lower box office performance than hoped.

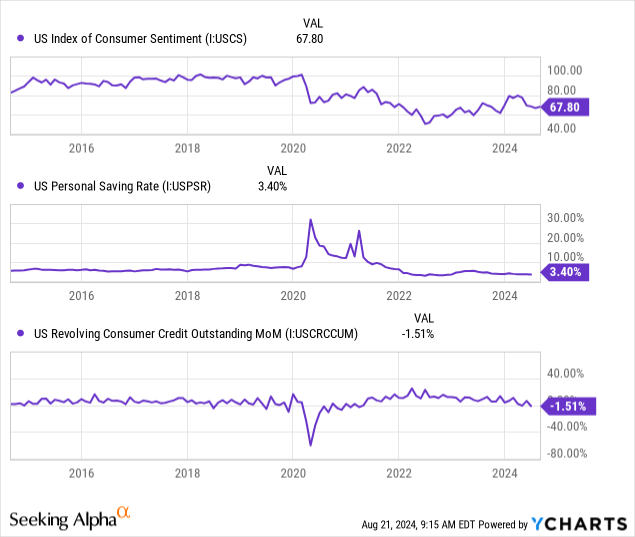

Habits have permanently shifted toward watching new-release movies at home, which is cheaper and often more comfortable. Movie theaters no longer monopolize recent movie releases and likely never will again. Add on a decline in consumer spending capacity, and it seems likely that theater ticket sales will remain low. Consumer sentiment has been chronically low since 2020; however, consumer spending has been strong due to lower personal savings (down to the 3% range from 5%+ pre-2020). Much higher credit card borrowing levels also supported consumer spending. Today, we're seeing a clear negative shift in revolving consumer credit, telling me that spending should now decline unless wages accelerate. See below:

Data by YCharts

Data by YCharts

At this point, we can still only speculate regarding the probability of a more significant recession with a rise in unemployment. Such would undoubtedly be very problematic for AMC. In my view, even the current conditions of negative revolving credit changes point to lower consumer spending on discretionary items like movie dates. Of course, that isn't because people are taking on credit card debt to go to the movies but because negative consumer credit tends to point to broader weakness in consumer spending stability, which usually disproportionately impacts entertainment spending, particularly given potentially superior streaming alternatives. For this reason, I expect AMC's operating income may remain negative over the coming year.

Refinancing Fails to Salvage Balance Sheet

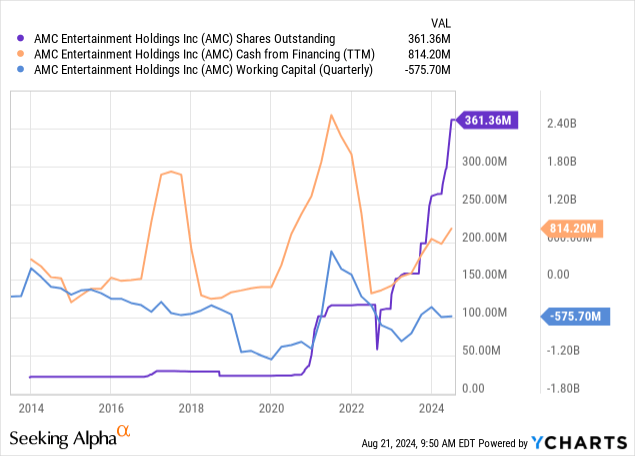

Of course, the company is still paying a considerable amount in interest at a net of about $100M last quarter. Thus, it is highly dependent on cash from financing, primarily equity dilutions, which become less feasible as it lowers its market capitalization. See below:

Data by YCharts

Data by YCharts

After its refinancing, AMC reported negative working capital of -$575M. At a market capitalization of $1.8B, it may need to dilute around a third of its shares to cover its negative working capital. Of course, some of those current liabilities, such as its lease obligations, should be made up by revenues, but that could still be difficult if its operating income fails to retain a consistently positive position.

Many investors had a positive take on AMC's debt refinancing deal. Its new agreement dramatically reduced its debt maturities this year through 2027, pushing them out to 2029. The deal allows the firm to refinance up to $2.45B. Of course, this deal came with some severe costs. For one, it's at SOFR plus 6-7%, or around 12% today. The bulk of this is to go to refinancing its 2026 debt, which had an effective interest rate of ~8.4%. This deal also included refinancing $414M in second lien notes for the same amount in exchangeable PIK notes. Although that gives AMC some opportunity to reduce its debt permanently, it would be at the cost of diluting its equity. Should its market capitalization decline by then, it could result in severe dilution.

Overall, I believe it is fair to say this refinancing deal reduces its immediate bankruptcy risks, particularly those that I previously expected could occur around its ability to refinance its debt. However, to me, it nearly guarantees the inevitable failure of its equity, given the high interest rates and dilutive terms of this deal. That is, if AMC cannot dramatically raise its operating income over the coming years, I do not expect its 2029 maturities will go successfully, particularly considering the extremely high rate of interest it will be paying from now to then, which may not be made up for in operating income.

The Bottom Line

Fundamentally, I see no value in AMC stock because its ability to earn a positive EPS seems very low. That is not only due to what may be sustained negative operating income but, more importantly, due to excessive interest costs that should rise. Of course, a recessionary slowdown in business may be the final nail in the coffin; however, that risk is offset by the potential that an economic slowdown results in a much lower SOFR rate, lowering the interest on its debt. Still, even a vast, and for now unlikely, 500 bps rate cut would fail to cut the interest on its new debt in half.

Although I am bearish on AMC, I would not short-sell it. To me, AMC has too much "meme stock" potential that often pushes it up by 50%+ over short periods following temporarily positive news. Further, unless its revenue faces a significant economic-driven decline, its debt refinancing mitigates its bankruptcy risk.

Even then, should investors lose hope in AMC enough that its market capitalization falls to the $1B or lower range, I expect that its remaining equity value may crater. The company is dependent on equity dilution, and some of its outstanding debt is tied to PIK loans that could be paid with equity. So, if its market capitalization falls enough, it may likely be unable to raise sufficient external capital.

The opposite is also true. If investor hope rises, the company may sell more shares and raise cash to deleverage. To me, that is unlikely, given its highest TTM operating income of $33M from Q1 23 to Q1 24. That was during a relatively strong rebound for consumer economic activity and film production, but it is insufficient to give it a reasonably high fair Enterprise Value. Given it can hardly turn a positive operating income during good periods, I'm not sure it can avoid financial restructuring or even liquidation.

Indeed, the company (not its equity) may have some value if it can close underperforming locations while investing in its better locations. However, between its debt obligations, lease obligations, high operational overhead, and the weakness of the film and theater industry, even the best management team has very limited ability to stop the bleeding.

Comments