Last Sunday, I sent out a paywalled flash post explaining why I thought GLD November volatility looked like a sale based on Friday, 8/16 marks. The trade was still available on Monday morning.

It was a good trade.

[Unfortunately I didn’t do it myself and of course I’m cherry-picking by publishing this thread. As karmic penance, this week, I’ll write up a recent trade I did do that didn’t go so well]

Let’s see what happened.

First, I’ve now unlocked the full post so unpaid subs can also see the thought process Flash Post on GLD Vol but the tl;dr was the 90d or November expiry stood at as being expensive.

Post-mortem after 1 week

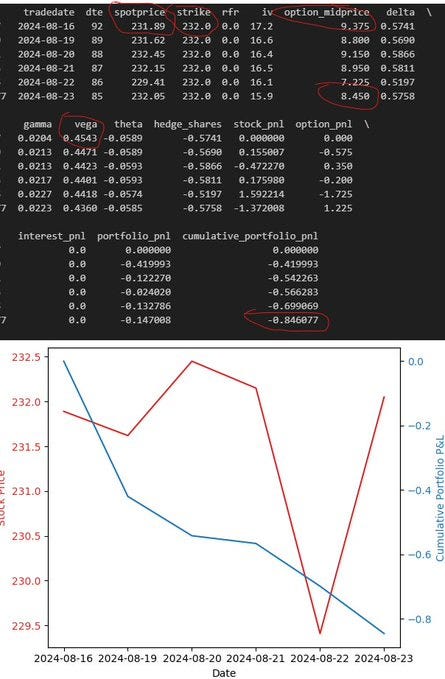

The November 232 GLD ATM call price

⇒ On Friday 8/16 (stock reference: $231.89): $9.37

⇒ On Friday 8/23 (stock reference: $232.05): $8.45

The profit is about $.92 or about 10% of the option premium. But this is a naive way to look at the p/l.

Decomposing the p/l

By selling this option you won to 2 different forces. The trade thesis was that the VRP and vol were both high so it’s not shocking to win on both but it’s never a given.

You would have collected:

1) $.58 in vega p/l due to IV falling

The IV on the 232 call fell from 17.2% to 15.9%. The option vega is $.45.

1.3 vol points x $.45 ~ $.58 cents in vega p/l

That’s an 8% change in strike vol over a week on a 90d option. I haven’t crunched the numbers, but based on writing weekly post mortems on my book for about a decade, I’d estimate that’s about a 1 standard deviation change in the IV for gold.

2) Another $.34 due to realized vol underperforming the IV

Theta won this week’s bout with gamma.

What about delta?

I am being a bit loose with the p/l decomp.

a) If you didn’t delta hedge, the stock went down and then rallied again this week. The calls finished the week down $0.92, despite the stock closing basically unchanged (up $0.16 for the week). It’s probably more accurate to say you made a bit more on the theta/gamma battle since you likely lost close to $.08 on delta p/l

b) If you did delta hedge daily, your P&L would have been +$0.84.

This output is from a daily delta hedge simulation assuming you were filled at market mid-prices. Note, it’s from the perspective of a long option holder, so the cumulative P&L is -$0.84 but I just flipped the sign since shorted the option.

It’s pretty random that the hedged and delta-hedged results were similar. The delta-hedged version is in general the best place to locate the P&L drivers because the trade thesis was grounded in vol not direction.

[Note: Selling an ATM call delta neutral is effectively selling a straddle. To be more accurate, if you sell 100 calls and hedge on a .50 delta you must buy 5,000 shares. You can algebraically re-factor you position as “I’m short 50 calls and 50 synthetic puts” which is 50 straddles. This trade is not quite because you hedged on a model delta of .57 instead of a .50 delta but it’s similar enough that the distinction only warrants being in this bracketed text.]

A thought on exit

If you look at the moontower.ai tools that led to the flash post in the first place they haven’t changed much despite the fall in IV. The short still looks like one of the better legs out there but it did make what I’d estimate is a 1 standard dev profit over a week and it’s not quite as obvious as it was a week ago.

As a retail trader, I wouldn’t add. I’d have a bias towards maintaining the short since it’s still looks relatively high although I’d probably care to take a closer look at how much election vol is embedded. (I’m not a registered advisor so I can speak relatively freely but to be clear I’m not suggesting anything other than how I would think about this. It should be very obvious that what is suitable for me or anyone else doesn’t mean it’s suitable for you. I write a newsletter that should be construed as entertainment and that is how you should view all newsletters. That the entertainment overlaps with useful doesn’t change what it is. If I put this under the guise of advice, I’d have to change a lot of stuff but it would also, like, cost money. I personally like that we have different channels for info to exist rather than trying to stuff all expression into regulated grooves. Don’t poison the commons by being a moron.)

If I was in my fund seat, I wouldn’t add to it (this is the market maker inside me who always argues with the position trader Jekyll who lives on the other side of the corpus collosum) but I certainly wouldn’t cover. If I were short 100k vega and my bid was hit for 20k vega and be content with the “screen edge” to mid-market.

[The nature of being in a noisy, unsystematic, repeat business with brokers is messy art….although my thinking risks becoming “quaint” every year that passes en route to 1 giant supercluster replacing the entire trading world which itself will be a pastoral phase to ruminate upon while we await being refined into robot fuel.

Sorry just a joke. Well, unless I’m right. Then I want the credit inscribed on the steel-ribbed drum containing my innards.]

Commentary

If you look at the “funnel” thinking from the flash post showing how I found this expensive option, you’ll see that I thought IV and VRP tailwinds were aligned. That doesn’t happen often. The charts you find in moontower.ai make the “no easy trades principle” really visible. Volatility risk premiums (VRPs) are high when vols are low and vice versa.

Another way of understanding the principle is what I call “distributional edge vs. carry” — aka the problem with buying low and selling high. You can read more about it here: Distributional Edge vs. Carry.

Moontower.ai offers a vol trader’s perspective. If you are professional vol trader running a relatively vol-neutral book there’s always things that look cheap vs expensive. By definition if you define fair cross-sectionally, half the universe is expensive relative to the other half. If this is your mandate you are in a low-margin trading business that has very attractive scaling properties.

But you are not that.

Instead you can just look at look at the tools regularly. You’ll typically conclude: “nothing to see here”. There’s nothing wrong with folding cards especially when there’s no ante. Retail’s advantage is not needing to trade. Buffet’s fat pitch and all that.

Buffet, of course, also keeps studied so he can recognize and act quickly when the opportunity comes. I look at moontower.ai every day. Most days I shrug, meh nothingburger, get back to regularly scheduled life and work. Breaking even on the cost of a sub is making (or saving) a dime on 100 contracts in the course of a year. It’s a low bar. The real cost is in glancing at it at least once a week to develop intuition. I talk about this more in this FAQ question. If that cost is too high, there’s no shame in avoiding options altogether or ‘index and chill’. (This is what most people should do. Our tool is for the self-selected ‘compelled’).

The tools really shine when you blend their insights with your own fundamental and directional biases to fine-tune or discover bets. While it doesn’t have all the features of full-fledged option software yet, it started with “how I want to see things.” It is opinionated. Of course, we care deeply about what users want, but I can’t deny the influence of my own taste. In fact if it wasn’t for me wanting to see things my way we wouldn’t even be this far. I certainly didn’t look at the option software space and conclude “oh this looks like a great way to make money”. It starts with having a differentiated way of seeing options and operationalizing it. Making money on the software will be a byproduct of having an experienced approach and philosophy that offers something different as opposed to making shinier versions of features that can feel disjointed when they aren’t pulled together with a trader’s lens.

Wrapping up

As I mentioned earlier, this trade was cherry-picked for the post-mortem. I wouldn’t even have considered the “victory lap” if I hadn’t built the delta-hedged simulator this week. That’s where I pulled the Python screenshot.

So far the only two flash posts I’ve done are this one and the GME trade — winning two for two is statistical significance, right? Ok, ok. I’ll make an offering to the delta gods by writing up a bad trade I did in IWM later this week using a similar volatility decomposition framework.

The main thing I want you to takeaway is that options are always a vol trade (except for reverse-conversion funding stuff). Put-call parity is a very deep insight.

Your understanding of bets, even those without options, will grow significantly if you use even simple option decomposition to think about path dependence and attribution. I’ll keep hammering this point — I’m pretty sure even a middle-schooler with an attention span (and interest, of course) could learn this stuff if it’s repeated enough.

If the Moontower sphere, the writing and the software, isn’t making it easier, then I’m screwing up.

Comments