Summary

- SOFI shows resilience with a 9% return, driven by strong loan demand and a slightly bullish technical outlook despite macroeconomic concerns.

- SoFi’s diversified platform, improved loan performance, and tight credit risk management underpin long-term growth, though caution is advised due to historical seasonality trends in August.

- Strong Q2 2024 financials, product innovation, and 58% AUM growth highlight SoFi's operational efficiency and potential for continued expansion.

- SoFi's Q3 2024 growth reflects an expected 18%-22% increase in adjusted net revenue, driven by expanding financial services and customer acquisition.

- SOFI's technical analysis shows neutral-to-bullish momentum with an RSI of 54.20, supported by a bullish divergence and increased buying pressure, as indicated by the VPT.

Viorika

Investment Thesis

Despite recent macroeconomic concerns and interest rate volatility, SoFi Technologies, Inc. (NASDAQ:SOFI) has demonstrated resilience with a 9% return since our last coverage, supported by growing loan demand and a slightly bullish technical outlook.

While high interest rates challenge home loan originations and student loan recovery, SoFi's diversified platform and ongoing technological scalability provide a solid foundation for long-term growth. Current neutral-to-bullish momentum coupled with strong loan performance in Q2 2024 offers upside potential.

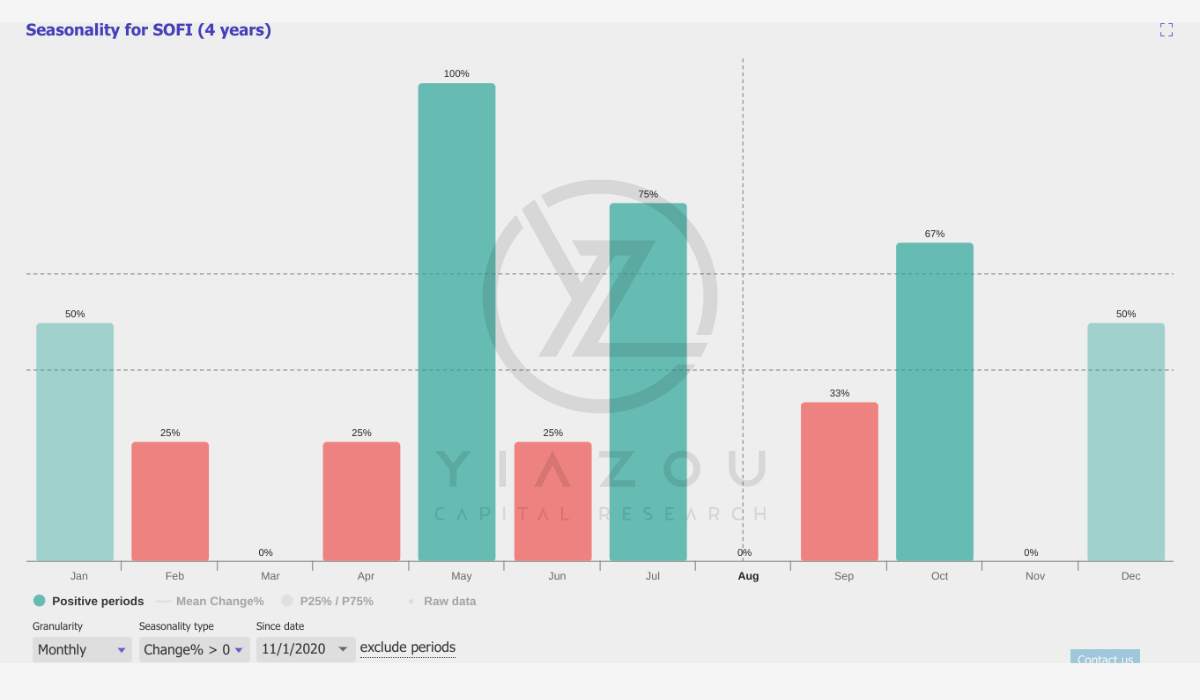

However, caution is warranted in the near term due to historical seasonality trends suggesting limited gains in August. Thus, SoFi remains a promising, albeit cautious, long-term buy.

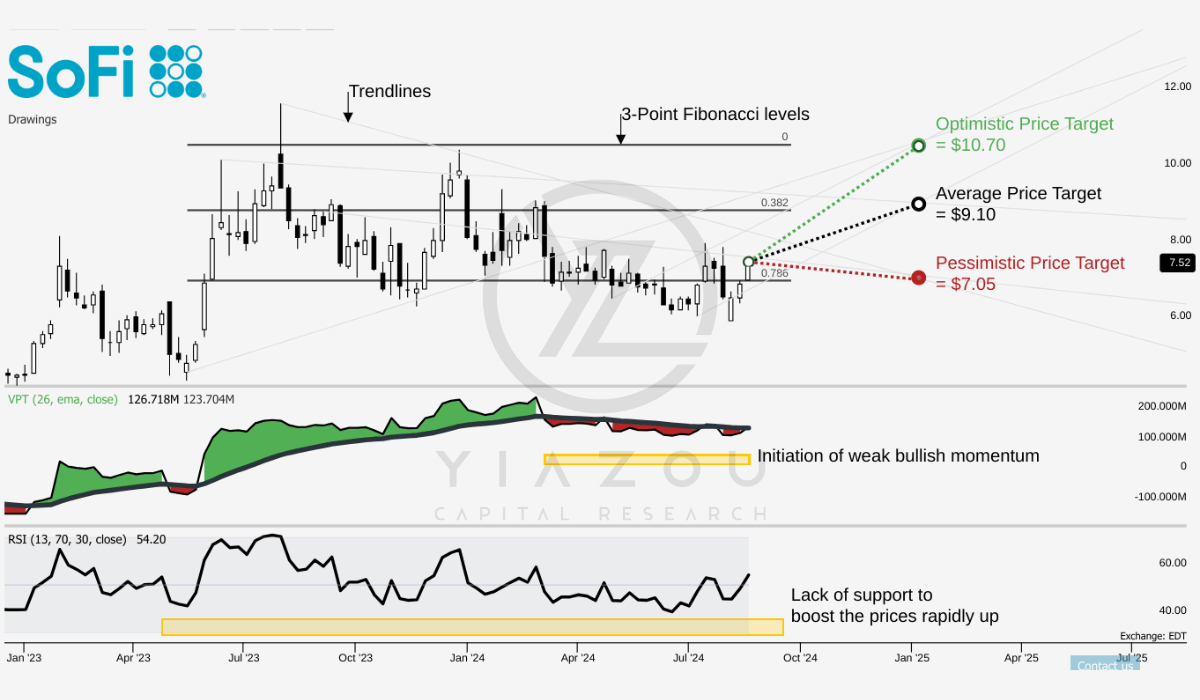

Cautious Optimism for a Potential 2024 Rebound To $9.10

SoFi's stock trading at $7.50 places the stock in a critical range, closely aligned with the pessimistic price target of $7.05, corresponding to the 0.786 Fibonacci level. This alignment indicates that SoFi is hovering near a significant support level, suggesting a potential rebound if this support holds. The average price target of $9.10 and the optimistic target of $10.70 align with the 0.382 and 0 Fibonacci levels, respectively, signaling a potential upside if the stock can break through these resistance levels.

The Relative Strength Index (RSI) at 54.20 is upward, indicating a neutral to slightly bullish momentum. A bullish divergence and the absence of a bearish one further support the potential for upward movement. The RSI value's proximity to the lengthy setup level of 50 suggests that the stock may have recently experienced a bottom, reinforcing the possibility of a near-term rally.

Finally, Volume Price Trend (VPT) analysis complements this bullish outlook. The VPT line at $126.72 million surpasses its moving average of $123.70 million. This crossover typically signals increasing buying pressure, which could increase the stock price.

Yiazou (trendspider.com)

However, the seasonality analysis shows a 0% positive return possibility for August based on the stock's performance since 2020, which implies that historical patterns do not favor a strong performance this month.

Yiazou (trendspider.com)

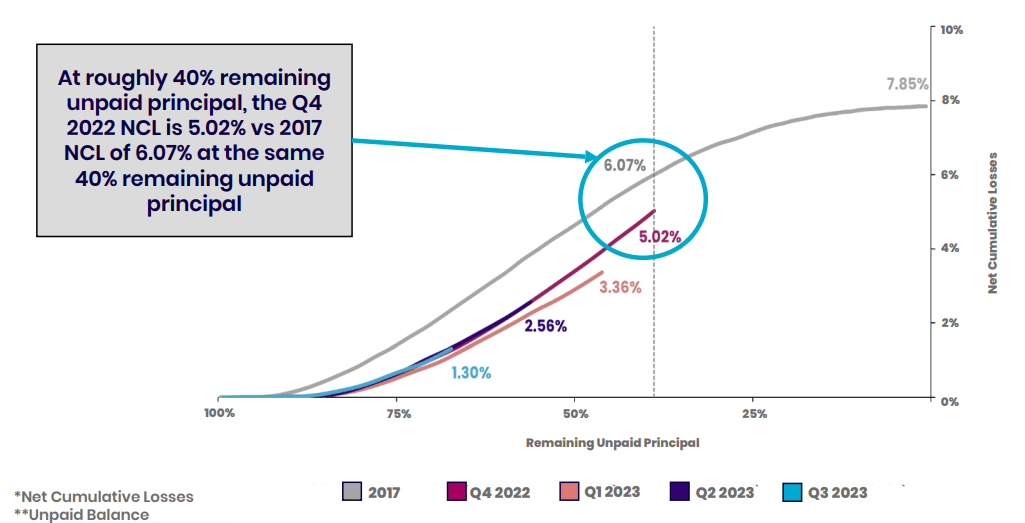

SoFi's Strong Loan Performance and Tight Credit Risk Management Drive Profitable Growth and Improved Efficiency

SoFi's financial health is closely tied to loan performance and credit risk management. Key indicators are net Cumulative Losses (NCL) by loan vintage. The 2017 vintage is a benchmark for credit risk, reaching nearly 8% cumulative life-of-loan losses.

At about 40% remaining unpaid principal balance (UPB), SoFi has an NCL of 6.07%. In contrast, the Q4 2022 vintage had a lower NCL of 5.02% at the same UPB level. This reflects improved credit quality and risk management. Lower NCLs and increased loan originations show SoFi's tighter underwriting standards, with changes in credit cuts in mid-late 2022 evident.

Moreover, the Q1-Q3 2023 vintages perform better than the 2017 and Q4 2022 vintages. This performance is at similar UPB levels, consistently improving SoFi's loan quality. Recent vintages outperform earlier ones, proving SoFi's effective adjustment to market conditions. SoFi originated $34.8 billion in loans from Q1 2020 to Q1 2024, with 44% ($15.4 billion) of the principal remaining outstanding.

Cumulative net losses to date are $1.2 billion. This is 6% of the paid-off principal and only 3% of the total originated balance. To reach an 8% overall NCL for this cohort, the remaining principal must experience an 11% loss rate. Historically, such sharp declines in loan performance are rare, and losses typically stabilize or improve as loans mature. This suggests that final life-of-loan losses will stay below 8%, and SoFi's risk management practices are proving effective.

SoFi's financial performance in Q2 2024 shows strong profitability. EBITDA increased by 80% annually to $138 million, and the margin reached 23%. This growth indicates SoFi's efficiency and ability to generate higher earnings. It marks SoFi's third consecutive quarter of GAAP profitability.

Net income was $17 million, compared to a $40 million loss in Q2 2023, reflecting the company's financial discipline and operational efficiency as sales and marketing expenses dropped as a percentage of adjusted net revenue (6 percentage points from last year). SoFi is becoming more efficient at acquiring customers and generating revenue. Hence, the decline in marketing costs suggests more robust brand growth, leading to more organic growth and better customer retention.

SOFI 2Q24 Slidedeck

SoFi Expands with Product Innovation and 58% AUM Growth

SoFi's focus on product innovation and expanding its product line supports its top-line growth. The financial services sector contributed 91% of new product additions in Q2 2024. For instance, SoFi's Invest business saw a 58% rise in assets under management (AUM) compared to last year. Net inflows and new alternative assets, including private credit, real estate, and venture investing, drove this increase.

They are offered alongside traditional options like fractional shares and ETFs. This product diversification is likely to attract more customers and boost platform retention. SoFi Plus, the premium membership tier, reached 1 million members. This tier provides higher APY on deposits and increased cashback rewards, enhancing SoFi's value proposition to attract and retain high-value customers.

Additionally, a new subscription-based option for SoFi Plus is planned. This approach provides flexibility for customers who prefer subscriptions over direct deposit requirements. SoFi's recent lending initiatives include home equity products and loans for small and medium businesses. These initiatives position SoFi for future growth as interest rates stabilize. The new lending capabilities help SoFi capture more value per loan. These moves also expand the company's market reach, particularly in home equity loans. Home equity loans offer a lower borrowing cost compared to unsecured loans.

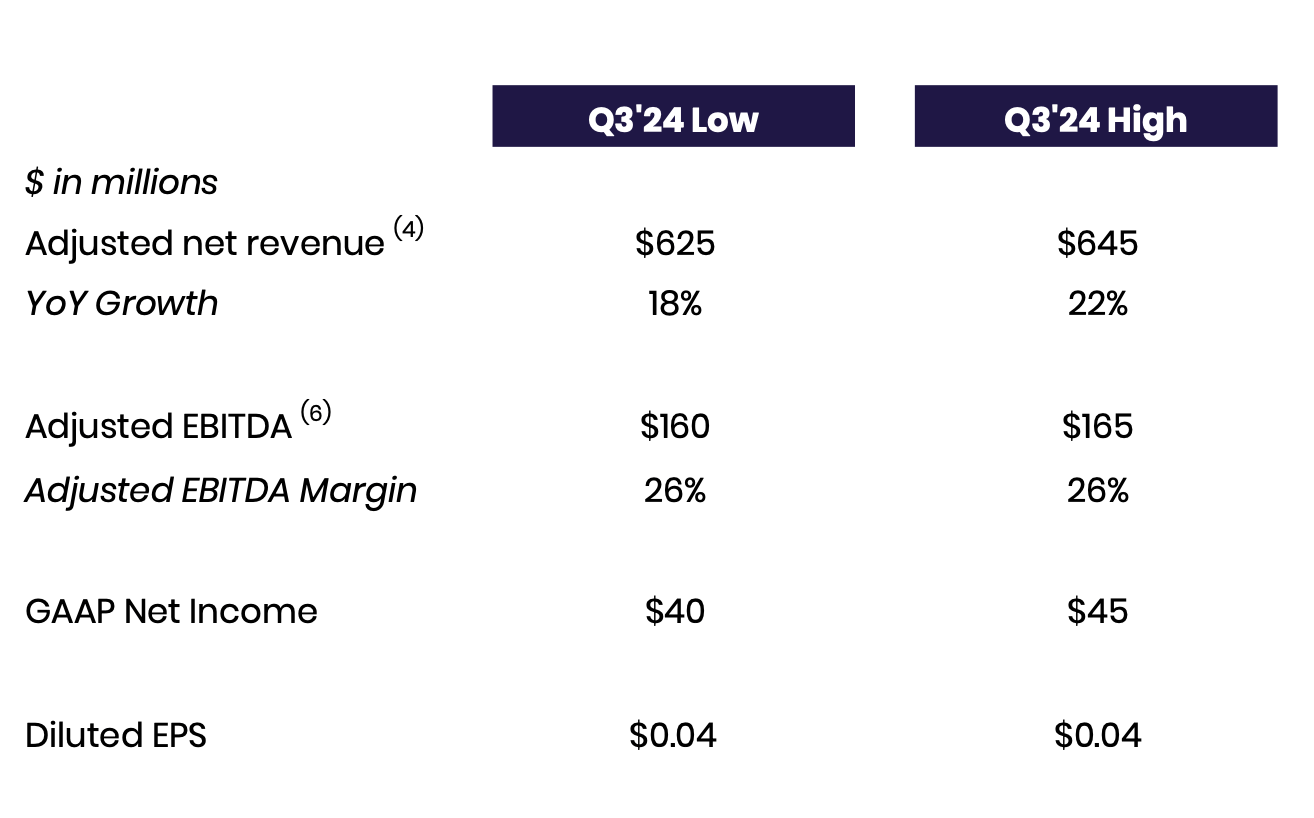

SoFi Forecasts 22% Revenue Growth and 26% EBITDA Margin for Q3 2024

SoFi expects adjusted net revenue to be between $625 million and $645 million in Q3 2024, with annual healthy growth of 18% to 22%. This shows SoFi's success in attracting new customers and improving services, while the narrow range conveys confidence in hitting the targets.

At the bottom line, the expectation is for adjusted EBITDA to be within the range of $160 million and $165 million, retaining a high EBITDA margin of 26%. This margin level shows decent operational profitability, with SoFi doing an excellent job of managing its costs as it scales its operations. The company anticipates net income between $40 million and $45 million for Q3 2024. The diluted EPS is expected to come in at $0.04. This represents an improvement upon specific prior metrics on performance. While the EPS is small, it's the first of many steps toward shareholder value. This is required to attract and maintain investor interest.

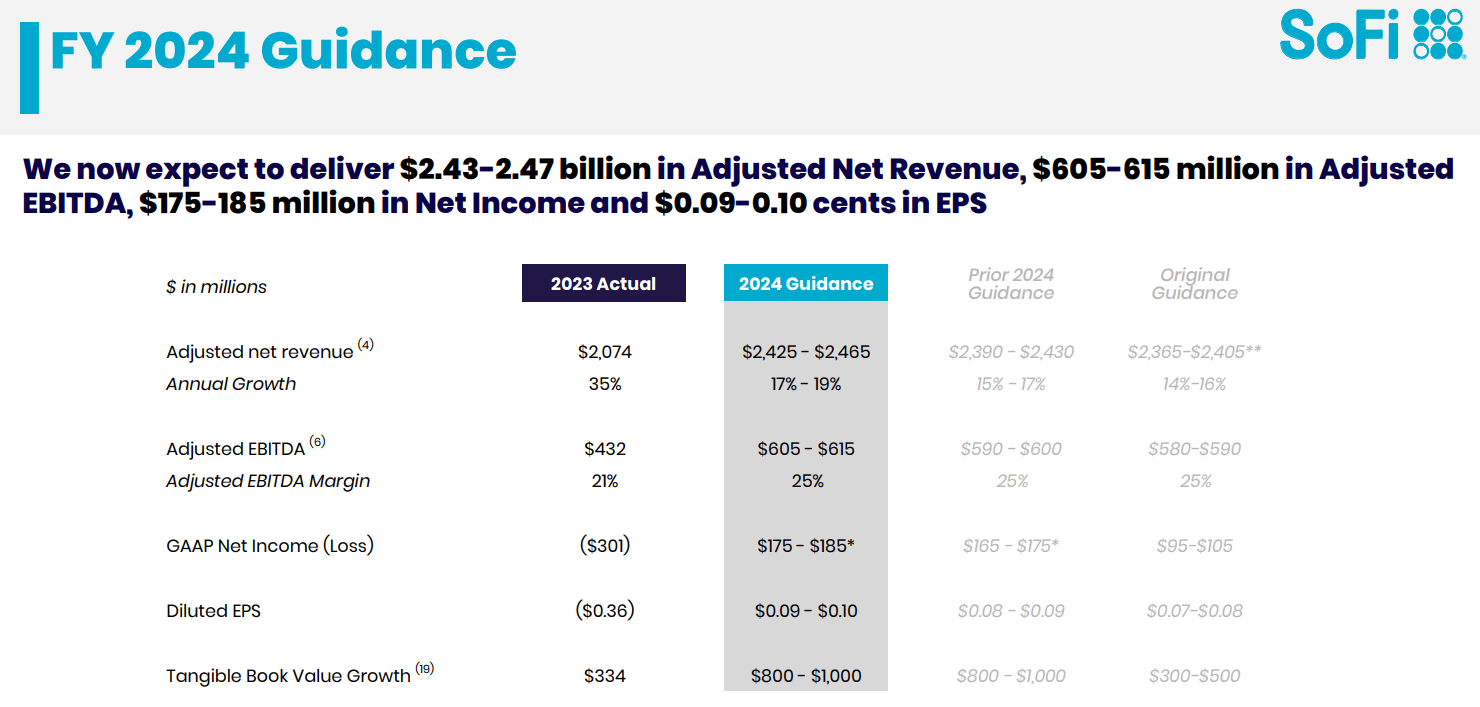

Looking into the future, SoFi expects continued growth ahead in FY 2024. The company expects financial services net revenue to grow by over 80% relative to 2023, reflecting the aggressive growth of the company and the integration in service. Lending adjusted net revenue is expected to be no less than 95% of 2023, demonstrating elasticity in light of fluctuations that could be seen in markets.

SOFI

The Tech Platform segment is expected to experience mid- to high-teen growth, which indicates SoFi's technological edge and scalability. The overall financial projections include a GAAP Net Income between $175 million and $185 million, a significant improvement from previous losses. Adjusted EBITDA is projected between $605 million and $615 million, maintaining a 25% margin and signaling continued operational efficiency and profitability.

Additionally, SoFi forecasts Tangible Book Value growth between $800 million and $1 billion. The total capital ratio is expected to exceed 16% by year-end, highlighting a stronger balance sheet and supporting future expansion, ensuring SoFi is well-capitalized.

Comparing the company's 2024 guidance with 2023 actuals reveals an upward revision in revenue expectations. Now, adjusted net revenue may grow by 17% to 19%. However, per the previous guidance, the top line was projected to hit 15% to 17% growth, reflecting strong performance earlier in the year. For profitability, the Adjusted EBITDA guidance has increased from $605 million to $615 million, up from $432 million in 2023, with an annual increase of 40%. This indicates effective scaling while maintaining profitability with a consistent EBITDA margin of 25% underscores efficient growth.

Net income and EPS projections show significant improvements. GAAP Net Income is guided between $175 million and $185 million, a turnaround from the $301 million loss in 2023. Diluted EPS may rise to $0.09-$0.10, significantly improving from a $0.36 loss per share in 2023, highlighting SoFi's successful transition to profitability.

Lastly, the anticipated growth in Tangible Book Value by up to $1 billion further strengthens SoFi's financial position, providing a solid foundation for future growth. A capital ratio exceeding 16% reinforces financial stability, enabling SoFi to withstand the higher, more extended interest rate scenario and pursue investments.

SOFI 2Q24 Slidedeck

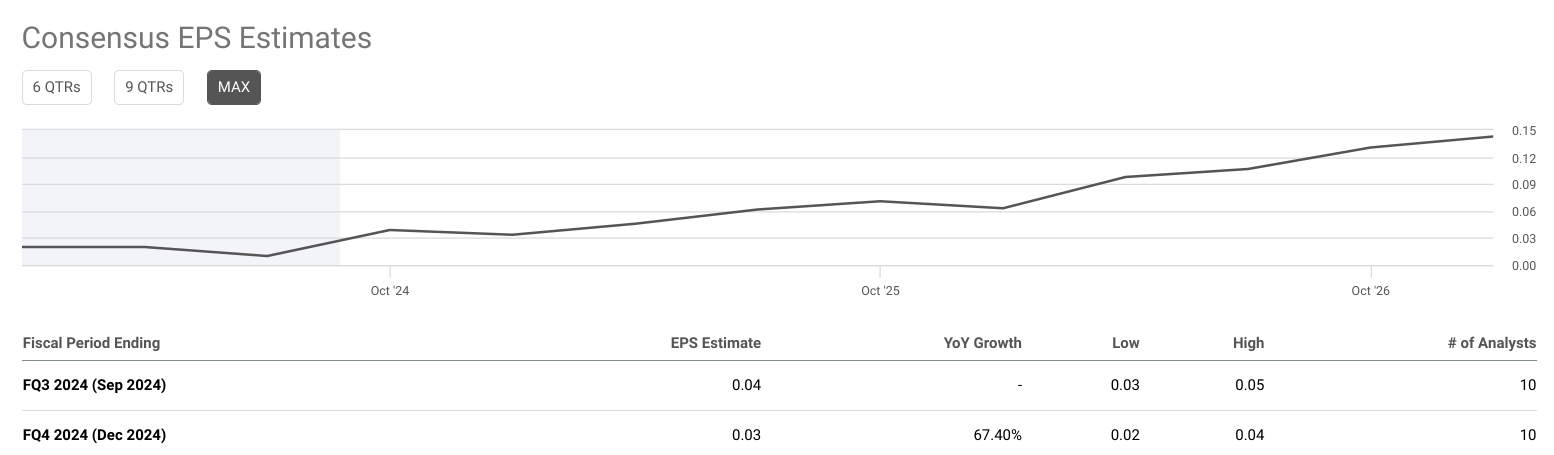

Finally, Consensus estimates for EPS in Q3 and Q4 2024 show positive growth. For Q3, the consensus EPS estimate is $0.04; for Q4, the EPS estimate reflects a 67.40% annual growth. Moreover, analyst projections for revenue in Q3 and Q4 are also solid. For Q3, the consensus revenue estimate is $625.85 million with a 17.93% annual growth; for Q4, the revenue estimate is $642.77 million, reflecting an 8.17% annual growth. In short, high revenue growth and tight EPS estimates align with SoFi's growth trajectory targeted by the management.

seekingalpha.com

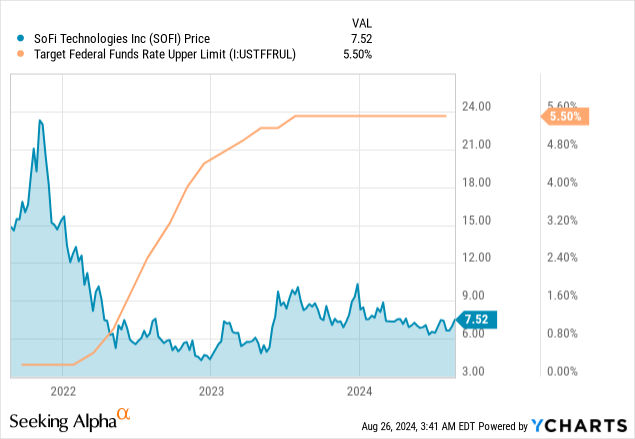

SoFi's Financial Strain: High Leverage and Market Uncertainty

This has made the SoFi balance sheet highly leveraged and capped its investment capacity for growth. The company has used senior secured financing to finance loan origination and balance sheet diversification, which increases the element of financial risk. Indeed, the new $989 million in senior secured financing in Q2 2024 continues to add to SoFi's debt. While providing liquidity, it increases the firm's debt burden.

Reliance on this financing would mean credit market disruptions may hurt SoFi's stability. Rising interest costs would put more pressure on the company's operating margins. Managing and divesting parts of its loan portfolio only adds to the complexity. Loan sales are not that attractive during high-interest-rate scenarios. High interest rates reduce the origination of home loans, directly affecting borrowers' affordability.

SoFi did report an increase in home loans for the second quarter of 2024, but it is not likely to continue. High interest rates may mute those growth prospects, and exposure to student loans in the SoFi market is also a very big negative. Therefore, in conjunction with economic uncertainty, this may keep a cap on continuing growth prospects for the SoFi stock.

Data by YCharts

Data by YCharts

Takeaway

Interest rates now indicating a falling trend should benefit SoFi with increased loan demand, especially in personal and home loans, tending to boost its revenues going into Q3 2024. The firm has good financial health, diversified revenue streams, and robust growth in non-lending businesses such as investments and financial products.

SoFi's Q3 revenue projection of $625 million to $645 million entails confidence in operational strength. While the stock is still at volatile levels, below $10, lower rates might turn things around. The bottom line for investors is that while caution over the short term should be exerted as volatility will persist, long-term potential looks strong with SoFi continuing to innovate and expand its offerings.

Comments