Summary

- The restaurant industry faces pressures from the declining middle class, which affects middle-income family restaurants like Cracker Barrel. These restaurants have struggled with rising costs and declining traffic.

- Cracker Barrel's high operating overhead and attempts to modernize may alienate its core demographic, risking further financial instability and potential equity dilution.

- Despite positive cash from operations, Cracker Barrel's liquidity issues and high operating costs suggest it may need to raise capital or close stores.

- The company's future hinges on economic conditions and middle-income spending; if income trends are negative by 2025, it may be a "value trap."

sanfel

The restaurant industry is facing significant pressures from the bifurcation of consumer spending. This long-term trend stems from the declining "middle" middle class, offset by growth in the lower-middle and upper-middle segments. Although this trend has impacted the market for over a decade, it has seemingly accelerated since 2020.

This pattern impacts restaurants, particularly given their universally rising operating costs. Restaurants that cater more to the upper-middle income segment, such as Texas Roadhouse (TXRH), are performing well. The same can be said for most fast-food and quick-service restaurants catering to a wide spending-power demographic. However, those restaurants that traditionally cater to the middle-income family demographic are, for the most part, not performing well. This segment has seen declining traffic as menu prices have risen sharply in response to the combined increase in food costs, labor costs, and other overhead sources.

Restaurants focused less on the urban market, and more on families seem to fare worse, as more opt for at-home cooking options to cut costs. Again, if we look at the market broadly, restaurants are doing fine. However, the overall statistics seem skewed toward the lower-end and upper-end of the market, with the middle seemingly caving.

Cracker Barrel Old Country Store (NASDAQ:CBRL) is an exciting example. CBRL has lost around half its value this year and is over 75% below its 2021 peak. The company is in a tail-spin as it struggles to push higher input costs forward to menu prices without losing too many customers. In my view, this issue is mainly systemic, impacting Denny's (DENN) and First Watch (FWRG) similarly; however, Cracker Barrel's focus on rural markets may give it a distinct disadvantage, as its primary customer demographic is likely among the more exposed to the inflationary pressures over recent years.

Cracker Barrel's "Millennial Shift" is Risky

Cracker Barrel is doing a lot to turn its prospects around. In my view, we must consider if these changes are all necessary or if the company is trying to change things that aren't broken as a response to external circumstances beyond its control or may prove temporary. Its peers, such as First Watch, may have better exposure to the younger demographics, as seen in its steady growth, while around 43% of Cracker Barrel's customers are over 55. That group is also a significant driver for its sales of physical items. While it may concern the company, it must keep this core group while adapting to a changing market.

The company is looking to make five fundamental changes, which can be boiled down to improving its marketing strategy, focusing on key menu promotions (which Chili's recently did with some success), updating the stores and restaurants, improving digital and off-premise sales, and improving employee retention. While there are few specific details, I think the company is looking to follow First Watch's steps, renovating to become more alluring by adopting new seating, new color palettes, and more simple decor and features.

This significant overhaul is a risk, but it may bring rewards. Indeed, the company is struggling to maintain customers and is partly tied to an aging demographic that has lost more spending power than most, given inflation. The company explicitly blames this issue for its poor performance. However, I believe it risks losing this core demographic by making these changes.

Cracker Barrel Has a Spending Problem

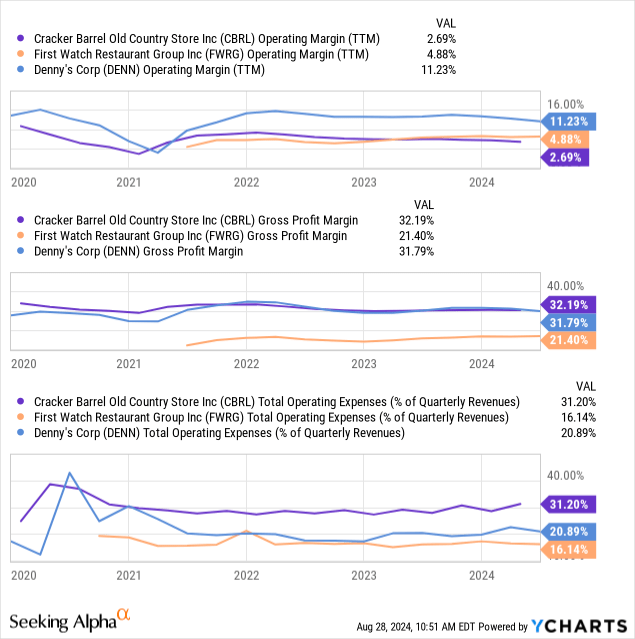

The company's avenues for change are limited. I believe it is looking to emulate some of First Watch's winning strategies. Capturing a wider demographic is undoubtedly a vital part of that, but to me, Cracker Barrel's primary issue is its operating overhead costs. Its business model is slightly different from that of First Watch and Denny's, given that it also sells physical items that should offer higher margins. Still, although CBRL and DENN have similar gross margins, Cracker Barrel's operating costs are so high that it consumes almost all of its would-be profits. See below:

Data by YCharts

Data by YCharts

First Watch has low gross margins, indicating its menu prices are about as competitive as possible. Luckily, its operating costs are also in check, at 16% of revenue, giving it stable profitability. Denny's also has lower operating overhead compared to Cracker Barrel's, at 31% of revenue, giving it net operating margins of 2.7% TTM.

The bulk of its OpEx is going to "other store operating expenses," which account for around a quarter of its total revenue. This includes operating supplies, third-party delivery fees, credit and gift card fees, property taxes, insurance, maintenance, utilities, and rent. It does not include labor, not general and administrative (G&A being 6.7% of revenue).

In my view, Cracker Barrel's primary issue is cost management. If it had operating overhead similar to its peers, it may not need to raise menu prices to potentially uncompetitive levels, resulting in lower traffic. I feel there is limited discussion of this issue in its investor calls and filings, focusing more on remodeling the stores to "evolve the store experience." To me, that means more capital spending costs at a time when it may need to focus on improving its cash position and cash flows.

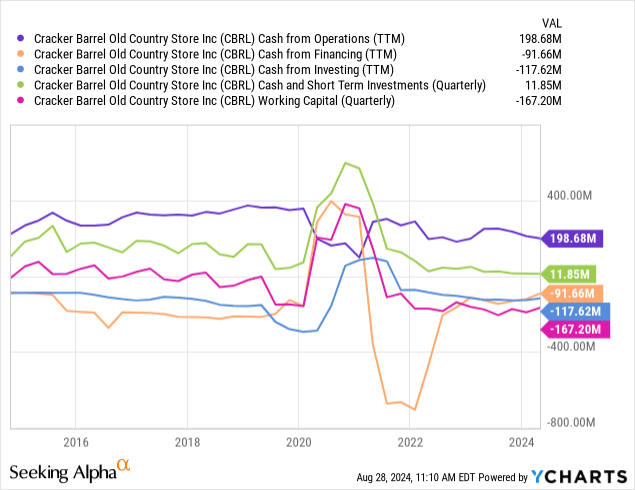

The company has positive cash from operations of nearly $200M TTM. However, its cash and short-term investments are around $12M while its working capital is -$167M, indicating some liquidity needs. Its debt is not a significant issue, but raising debt may be costly. See below:

Data by YCharts

Data by YCharts

If its CFO continues to trend lower, I expect it may need to raise capital from equity investors to finance its overhaul, as seen in its cash from investing. The company dramatically cut its dividend earlier this year, ideally improving its cash-from-financing trend enough to avoid dilution. Its overall balance sheet and cash position are not terrible, but they are trending in a problematic direction and, to me, may not be aided by the company's turnaround efforts.

The Bottom Line

In my view, Cracker Barrel suffers from difficult economic and demographic conditions and potentially poor managerial decisions. For example, it has only closed a few stores despite their underperformance. I believe the underperformance of many of its stores is indicated by its abnormally high store operating overhead costs compared to its sales, mainly when its gross margins are solid.

I think the company may focus on costly changes that fix something that is not broken, while avoiding store closures or similar changes that could improve cost management. Further, although it will be testing these changes slowly, Cracker Barrel's appeal stems from its non-modern appearance, and modernizing it may cause it to lose its remaining demographic niche.

On top of that, the broader economic landscape does not bode well for its market. Most direct cost-growth factors, particularly in food input costs, are no longer a major issue. However, it continues to face higher labor costs. Going forward, I do not expect it will face challenges relating to higher costs, but more associated with lower discretionary spending demand from its key customer demographic. This risk is potentially associated with the recessionary risks, as explained in "Brinker International: Sales Growth May Prove Transitory As Consumer Restaurant Spending Slows."

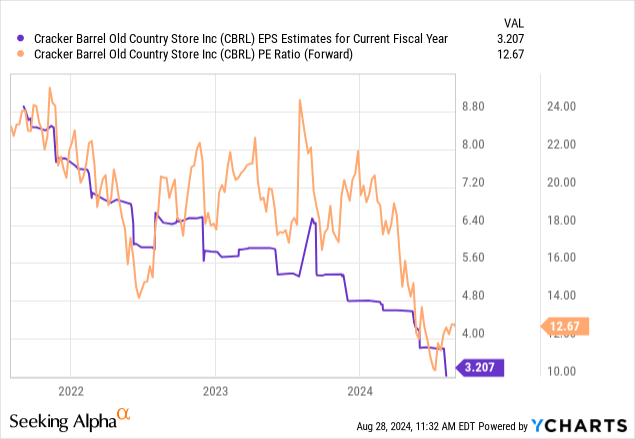

I am bearish on CBRL because I expect its income to turn negative by 2025, although that depends on the economy's strength. Given its cash and cash-flow circumstances, I think it may need to close stores more rapidly in that scenario, which may set the firm back dramatically and could result in equity dilution. Thus, the fair value of its equity today is vague, given the significant uncertainty surrounding its long-term income potential. That said, its immediate forward "P/E" is much lower than normal. To me, its valuation is low enough that it is likely not a short opportunity, but it still may be a "value trap." See below:

Data by YCharts

Data by YCharts

Cracker Barrel's EPS outlook has fallen so much that it may trend toward zero over the coming year or two. If so, its "low" 12X "P/E" valuation would not be low. Of course, if its margins recover and its EPS rebounds to $6+, its valuation would be very low at ~6X.

Overall, one's outlook on CBRL at its current valuation should be tied to their views on the restaurant industry, specifically for middle-income families and seniors. Even if it inexpensively renovates its stores, it will still be tied to the "middle middle" income market. There is solid evidence that that demographic will continue to struggle; however, the primary risk to my thesis is that this demographic starts to spend more as inflation slows, which is tied to the "soft landing" theory compared to my "hard landing" expectation.

Comments