Summary

- Dividend growth stocks can outperform the market, but long growth streaks don't guarantee better returns. Investors should dig deeper than labels.

- Research shows abnormal returns diminish after a few consecutive dividend hikes. Beyond that, consistent growth offers no significant advantage.

- Instead of focusing solely on Dividend Aristocrats or Kings, consider high-quality companies with strong fundamentals and growth potential.

Philip Hoeppli/iStock via Getty Images

Introduction

To be honest, I went with a provocative title. But I didn't use clickbait because we have a serious topic to discuss: dividend growth consistency. In fact, I would argue that this is one of the most important topics I've covered in recent weeks.

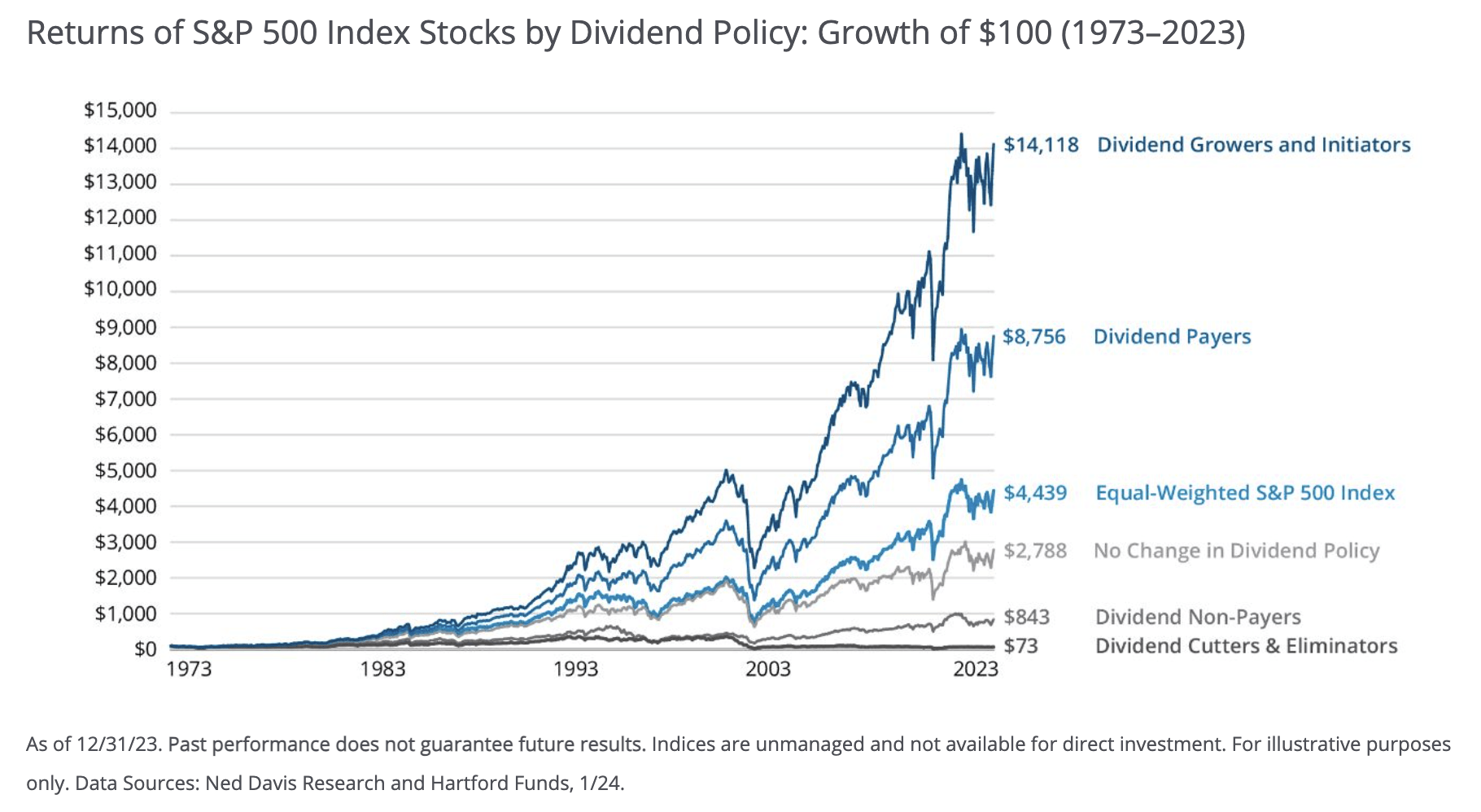

As some readers may know, I am focusing on dividend stocks for a reason. Historically speaking, dividend growers and dividend payers have outperformed the equal-weighted S&P 500 by a wide margin.

Using Hartford Funds data, dividend growers have turned a $100 investment in 1973 into more than $14,000 at the end of 2023. An investment in the equal-weighted S&P 500 would have resulted in roughly $4,300 in gains.

Hartford Funds

The outperformance of dividend (growth) stocks has a number of reasons. Among others:

- Financial Strength and Stability: Companies that consistently grow their dividends often show strong financial health and stability. In general, these companies have sustainable business models, solid cash flow, a commitment to long-term growth, and healthy balance sheets.

- Quality and Resilience: Related to the point above, dividend growth stocks are often associated with high-quality companies that can withstand economic downturns and volatility. I like to call this the "stamp of approval."

- Inflation Protection/Income: Because of consistent dividend growth, investors can buy inflation-protected income, something that becomes very important once dividend payments become a big part of one's income.

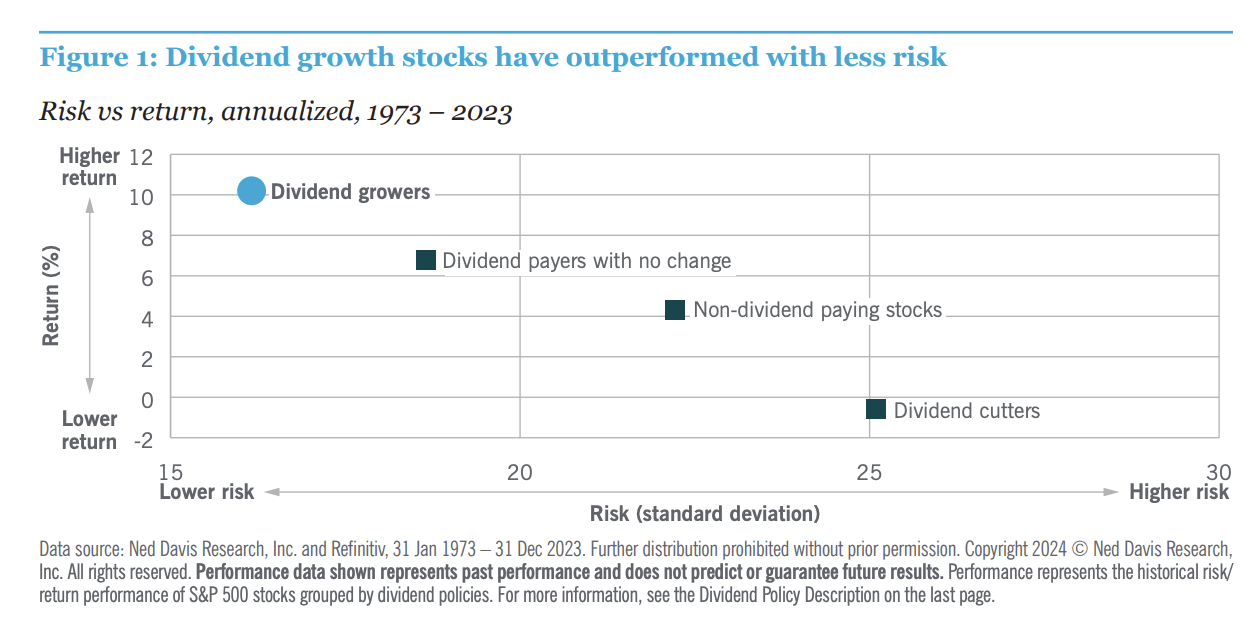

Even better, another graph I have used in prior articles (the one below) shows that dividend growers tend to outperform the market with a favorable volatility profile.

Nuveen

In other words, by buying dividend growth stocks, investors can beat the market with subdued risk. What may sound too good to be true is proven by countless papers and researchers.

Speaking of research, I recently dove into the importance of buying consistent dividend growers. I am sure most readers will know that there are a few categories of consistent dividend growers.

For example, companies that have grown their dividend for more than 25 consecutive years are Dividend Aristocrats. Companies with a growth streak of more than 50 consecutive years are Dividend Kings.

As I have said in the past, I don't really care for my dividend companies to become Dividend Kings. I care about long-term dividend growth, not uninterrupted annual dividend growth.

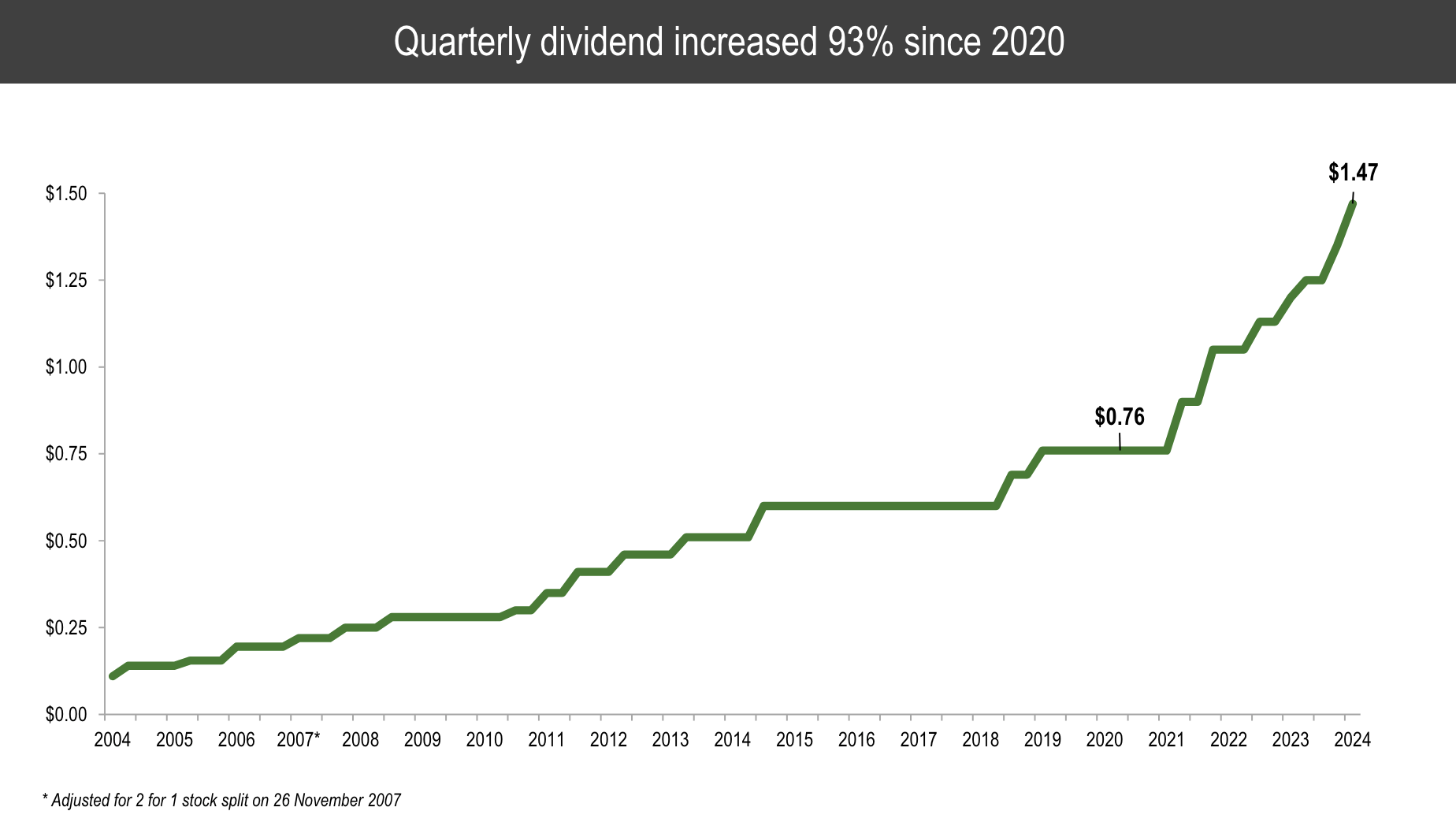

Deere & Company (DE) is a great example of such a company. Because of its cyclical nature, it has kept its dividend unchanged for a few years during the Great Financial Crisis and the tough period between 2014 and 2018. While this means it had reset its dividend growth streak, the big picture remained fantastic.

As we can see below, since 2020, the dividend has almost doubled!

Deere & Company

There are many other examples of companies that have paused dividend growth. I don't mind that, as I believe balance sheet protection is more important than a minuscule dividend hike just to keep a dividend growth streak alive.

Although I am by no means saying Dividend Aristocrats and Dividend Kings are bad (I'll continue to praise their achievements!), there is evidence that suggests we need to be careful when assessing these stocks.

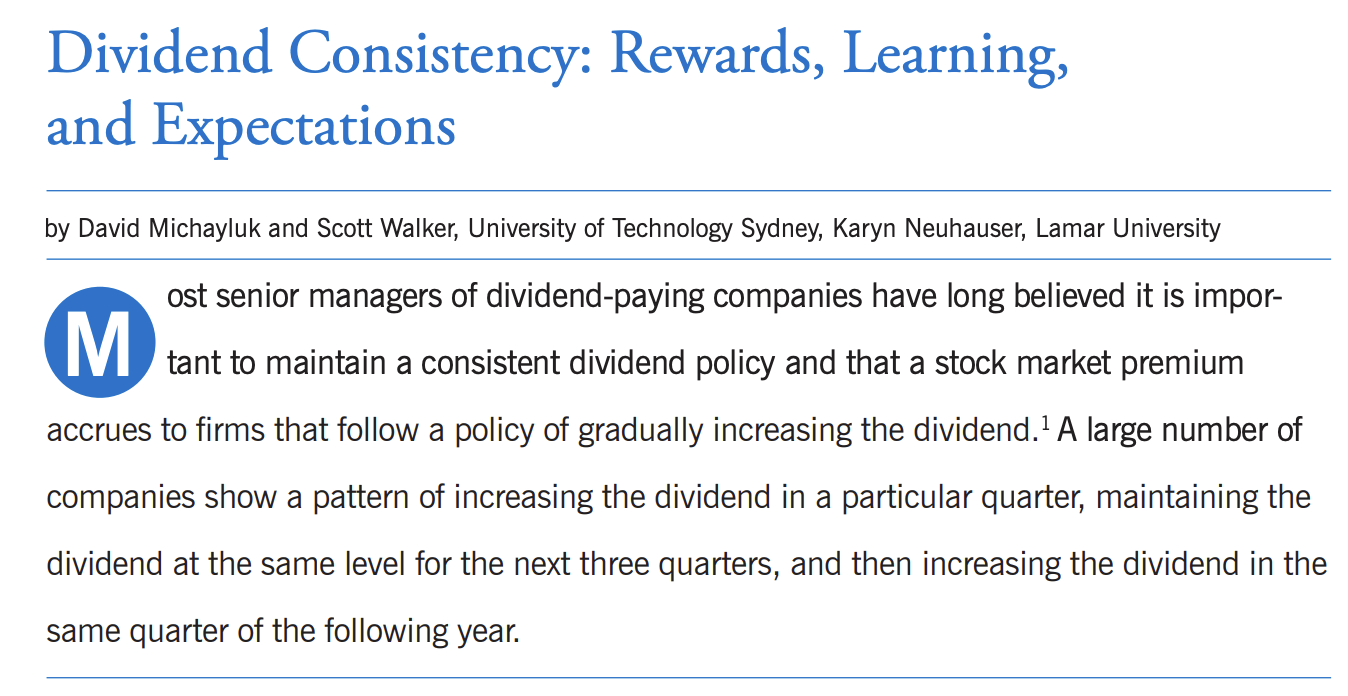

In 2019, David Michayluk wrote an article titled "Dividend Consistency: Rewards, Learning, and Expectations." It was published in the Journal of Applied Corporate Finance.

Journal of Applied Corporate Finance

It was a fascinating piece that revealed something very important, which is that dividend growth consistency is not as important as one might have thought. Here's a part of their abstract (emphasis added):

The authors find that companies earned significantly positive abnormal returns following each of the first five annual dividend increases, over and above the positive announcement-month returns. Nevertheless, the reward decreases as the track record of dividend increases becomes longer. After the first dividend increase, companies enjoy significantly positive returns for the next two years. Companies that increase the dividend in the same quarter of the following year also enjoy significant positive returns, but returns that are smaller (and less statistically significant) than in the case of first-time dividend increases. And as the dividend-increase track record further lengthens, the size and statistical significance of the abnormal returns continues to shrink; and after the sixth dividend increase, the abnormal returns in the next twelve months are statistically indistinguishable from zero.

In sum, although there is some support for maintaining a consistent dividend policy, the market response diminishes over time, and investors do not earn abnormal returns by buying stocks whose annual dividend has already been increased six or more times.

In other words, while consistent dividend growth is initially rewarded by above-average returns, the longer a dividend growth streak is the lower the benefit. According to their research, companies with dividend growth streaks of more than six consecutive years did not earn any above-average returns!

Using the data from the chart below, the ProShares S&P 500 Dividend Aristocrats ETF (NOBL) has failed to outperform the S&P 500 over the past few years. While this is partially due to the S&P 500's elevated tech exposure, the ETF also failed to beat the Dow Jones, which did not have these benefits.

Data by YCharts

Data by YCharts

Again, don't get me wrong, even this study acknowledged the positive message that consistent dividend growth sends. I added emphasis to the quote below.

Dividend consistency is important because it is rewarded with a stock market premium. These abnormal returns are not simply the result of earnings increases since only a very small number of dividend-increasing firms manage to maintain consistent earnings increases as well. By focusing only on returns related to dividend increases, we show why companies make a special point of publicly proclaiming their track record of dividend consistency and attach more importance to it than earnings consistency.

The important point is that the additional value of a Dividend Aristocrat and a Dividend King over a "non-categorized" stock (for lack of a better term) is non-existent.

While Dividend Kings and Aristocrats are certainly worthy of consideration, we should never base our investment decisions solely on their status. It's important to delve deeper into the underlying fundamentals of these companies.

Hence, in the second part of this article, I'll present three dividend (growth) stocks without Dividend Aristocrat/King status. I believe all three have the potential to deliver both substantial capital gains and dividend growth, making them fantastic picks to potentially beat the market going forward.

EOG Resources, Inc. (EOG) - A Top-Tier Oil And Gas Pick

EOG Resources is a company I have covered quite a few times in the past few years, as it's a fascinating onshore oil and gas producer in the United States. Over the past 24 years, it has returned more than 4,000%, beating the energy ETF (XLE) and giants like Chevron Corporation (CVX), which is a Dividend Aristocrat, by a huge margin.

Data by YCharts

Data by YCharts

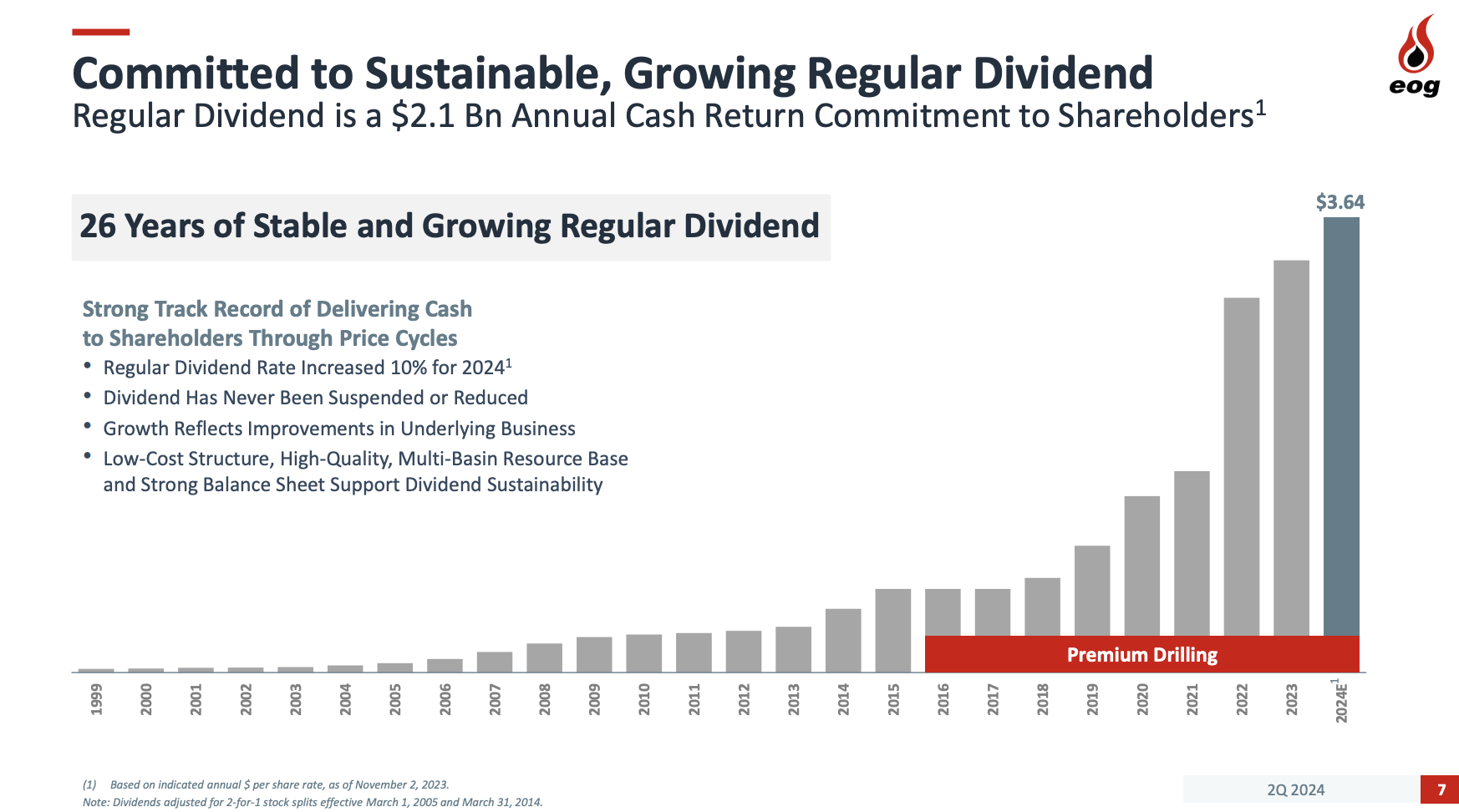

As we can see below, the company has paid a stable dividend for 26 consecutive years. This means it has not cut its dividend since 1999. It has kept its dividend consistent during challenging economic times and used aggressive hikes to boost the payout whenever it saw a path to sustainable growth.

EOG Resources

Currently, the company pays an annualized base dividend of $3.64, which translates to a yield of 2.8%. This dividend has enjoyed rapid growth, as the company got two major tailwinds:

- More favorable oil prices since the pandemic.

- Premium drilling advantages.

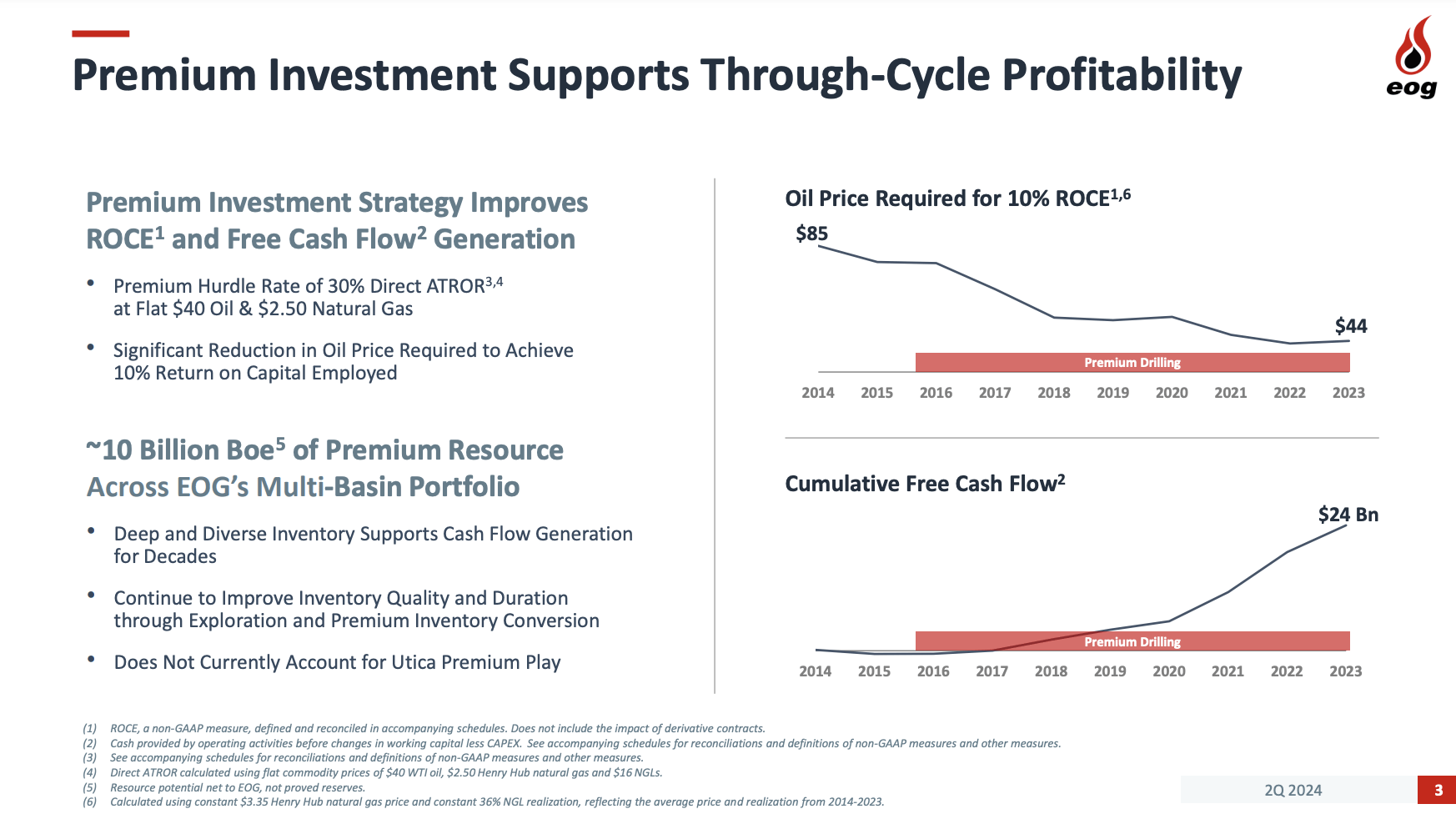

Between 2014 and 2023, the company lowered the oil price it requires to achieve a 10% return on invested capital from $85 to $44. It also benefits from roughly 10 billion barrels of oil equivalent in premium reserves, which allow it to produce without having to fear running out of Tier 1 reserves.

EOG Resources

In general, when assessing new investment projects, the company works based on an oil price assumption of $40 WTI and natural gas prices of $2.50 per Mcf. This makes sure it only pursues high-quality projects that will allow it to produce sufficient free cash flow, even when times are tough.

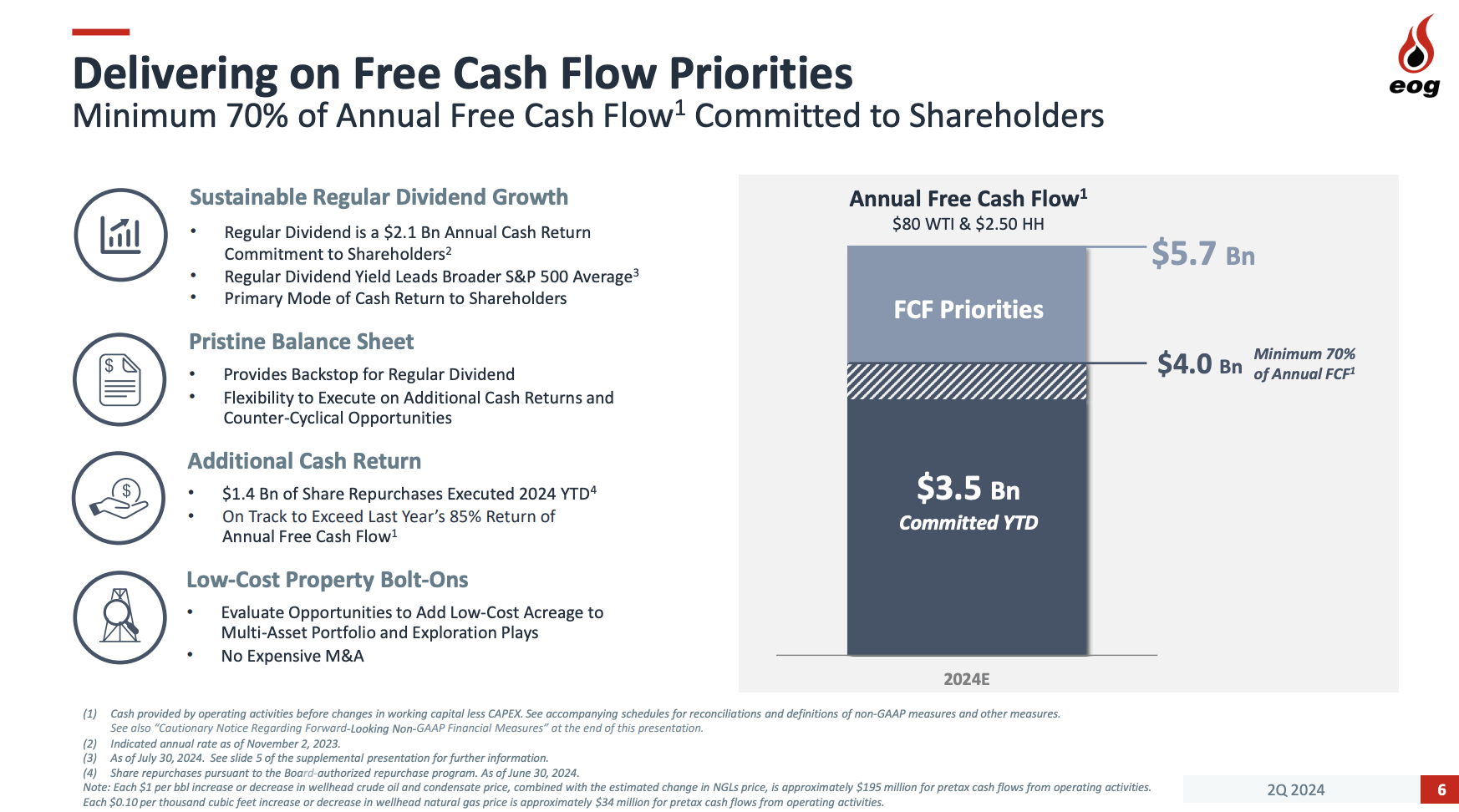

Thanks to successes in key basins like the Wyoming Powder River Basin, the Ohio Utica shale, the Delaware Basin, and Eagle Ford, the company raised its full-year free cash flow outlook to $5.7 billion. This is based on $80 WTI and $2.50 Henry Hub. Right now, prices are slightly below that.

With that said, this bodes well for shareholders. After all, the base dividend is not the only dividend shareholders receive. As we can see below, the company's third spending priority is additional shareholder returns. The company aims to distribute at least 70% of annual free cash flow to shareholders, using regular dividends, special dividends, and buybacks.

This year, the company is likely to exceed last year's cash return of 85%, which shows that it is willing to pay much more than the 70% it uses as a floor.

EOG Resources

Using the company's 2024 free cash flow guidance, we're dealing with a free cash flow yield of roughly 8%. Assuming the company distributes 85% of that, we're dealing with a total return yield of almost 7%, which is a great number for a challenging economic environment.

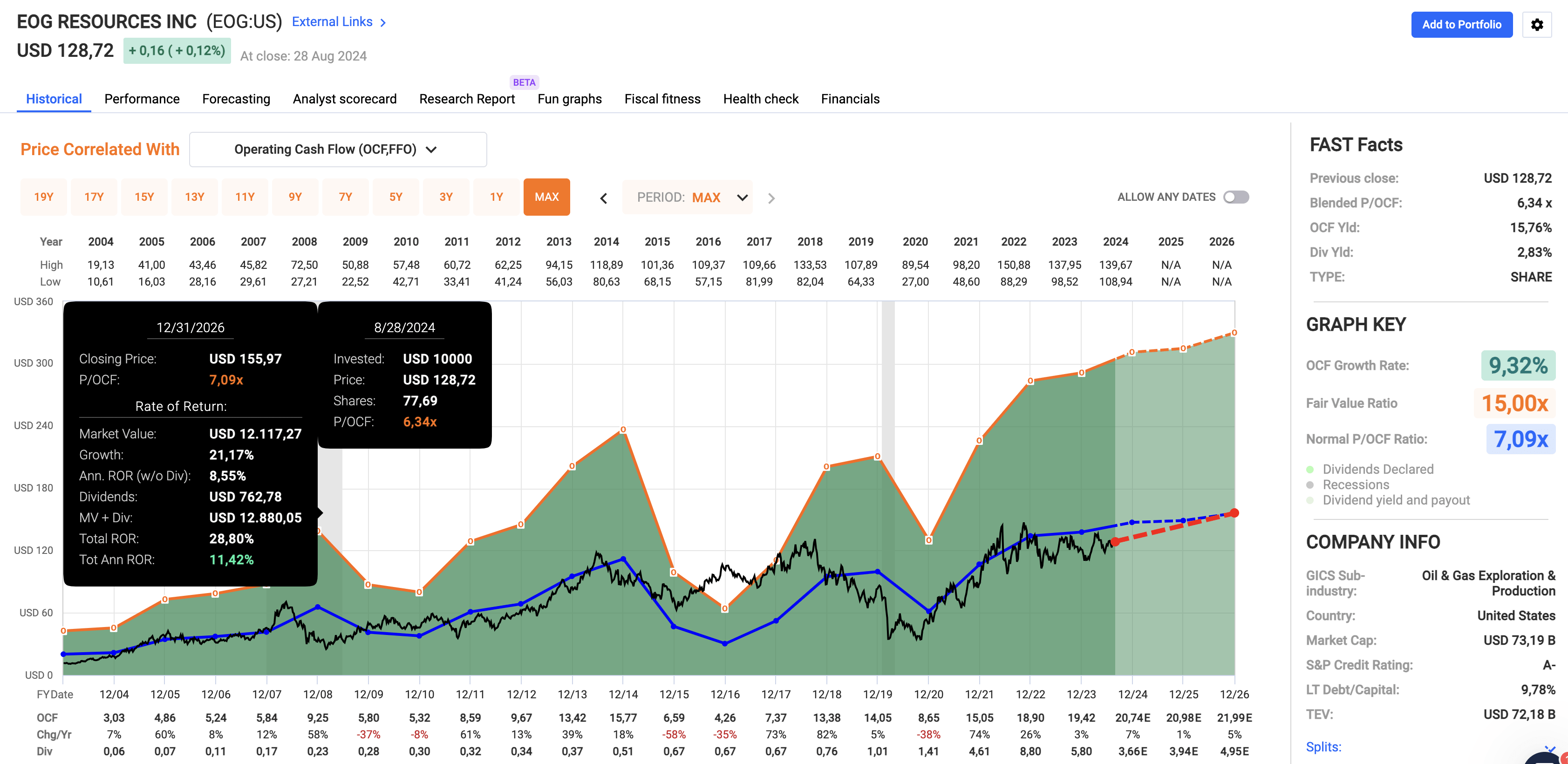

In general, I like EOG's valuation.

The company is trading at a blended P/OCF (operating cash flow) ratio of just 6.3x. It has a long-term average P/OCF ratio of 7.1x. Although I believe that number is too low, given the increasing attractiveness of American onshore producers, even a 7.1x multiple implies a fair stock price of $156, 21% above the current price.

FAST Graphs

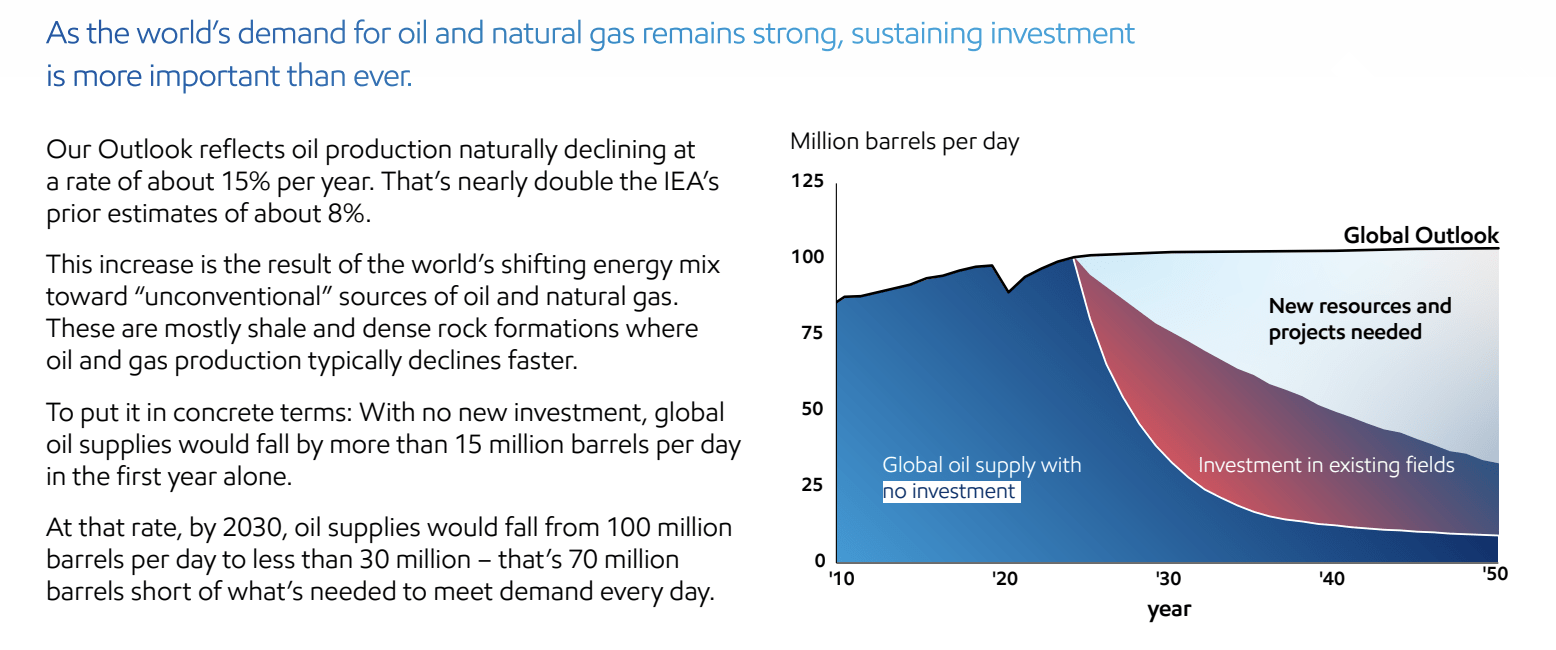

Given consistent oil demand growth and significant underinvestment (I will focus a lot more on this in the future), I believe EOG is a fantastic long-term investment for a wide range of dividend investors.

In general, because of the favorable supply/demand development (see below), I am loading up on energy stocks, expecting this sector to be the place to be for the next decade and beyond.

Exxon Mobil

This brings me to the next pick.

Blackstone Inc. (BX) - An Inconsistent Dividend & Outperformance

Blackstone is the world's largest private equity company. With a market cap of more than $170 billion, the company has a significant size benefit.

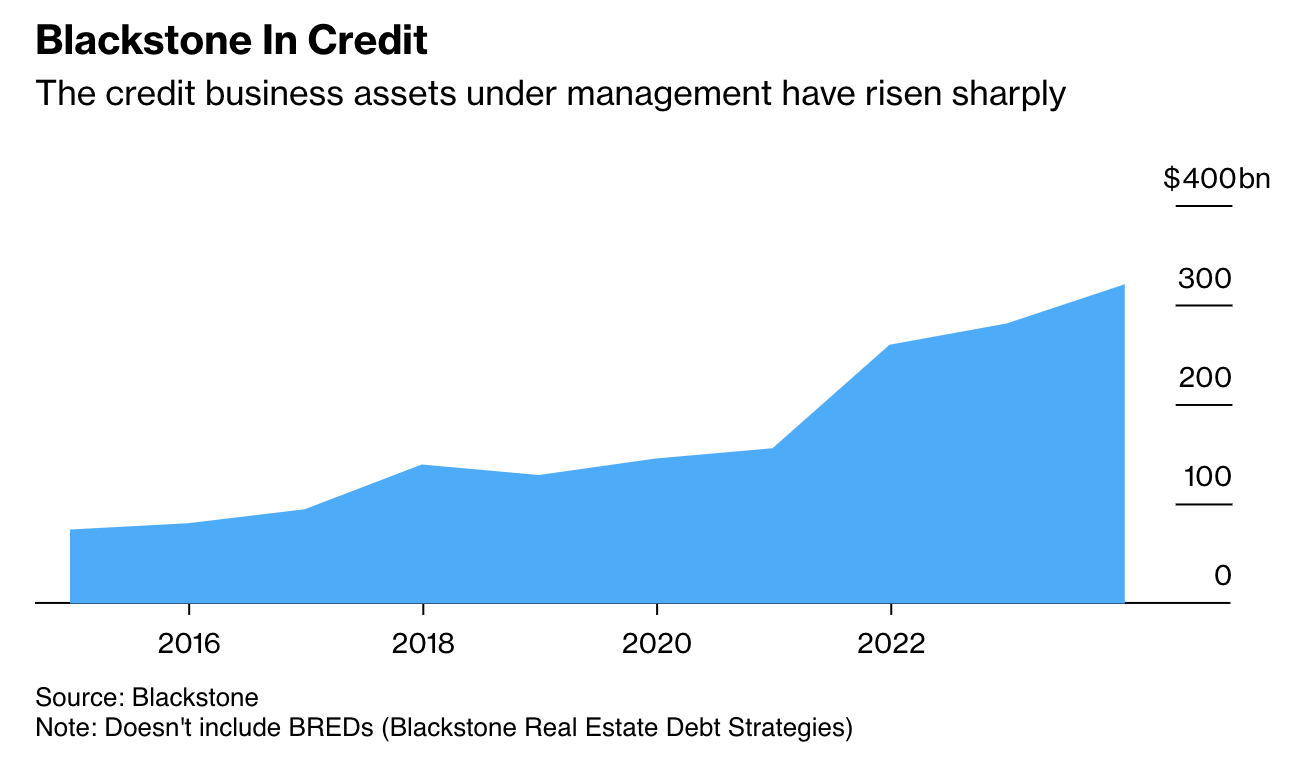

On July 22, I wrote an in-depth article on the company, titled "Playing Real-Life Monopoly With Blackstone." In that article, I explained how the company had become an asset manager with $1.1 trillion in assets under management.

Essentially, in 1991, the company decided to expand into private equity real estate. After adding the credit platform in 2008, it is now a well-diversified asset manager with more than $300 billion in credit assets and the world's largest private REIT.

Bloomberg

This private REIT is called Blackstone Real Estate Income Trust ("BREIT"), which is now three times larger than the next five biggest private REITs.

BREIT has allowed Blackstone to aggressively push into fast-growing areas, including data centers, multifamily housing, single-family housing, and industrial assets. These segments account for roughly 85% of its assets.

It currently has the world's largest data center portfolio worth $55 billion, with an additional $70 billion of data centers in development.

Moreover, the company has a terrific track record of predicting economic developments. As some readers may recall, the company has been calling for a bottom in commercial real estate since early 2024.

Hence, in the first six months of this year, the firm has deployed roughly $15 billion in this area - 2.5x its investment volume in the first six months of 2023.

Positive signs include a six-month trend of stable or increasing private real estate values and increased competition for single asset sales, which drives price improvements.

Moreover, the availability of debt capital has significantly increased while the cost of capital has declined.

When these two factors are combined with a steep decline in new construction starts, it bodes well for long-term value growth as the demand/supply balance shifts in favor of higher prices. - July 22 Article

On top of that, it is the largest infrastructure investor in the world and a beneficiary of an environment of looser financial conditions.

With regard to its dividend, Blackstone currently yields 2.4%. This dividend does not come with a track record of consistent growth. As we can see below, the dividend has been very volatile, as Blackstone aims to distribute 85% of its distributable earnings. This makes the dividend very variable.

Data by YCharts

Data by YCharts

The good news is that this has not kept the stock from outperforming, as investors know they will be rewarded if BX does well.

Over the past ten years, BX has returned 618%, beating the already impressive 234% return of the S&P 500 by a wide margin.

Data by YCharts

Data by YCharts

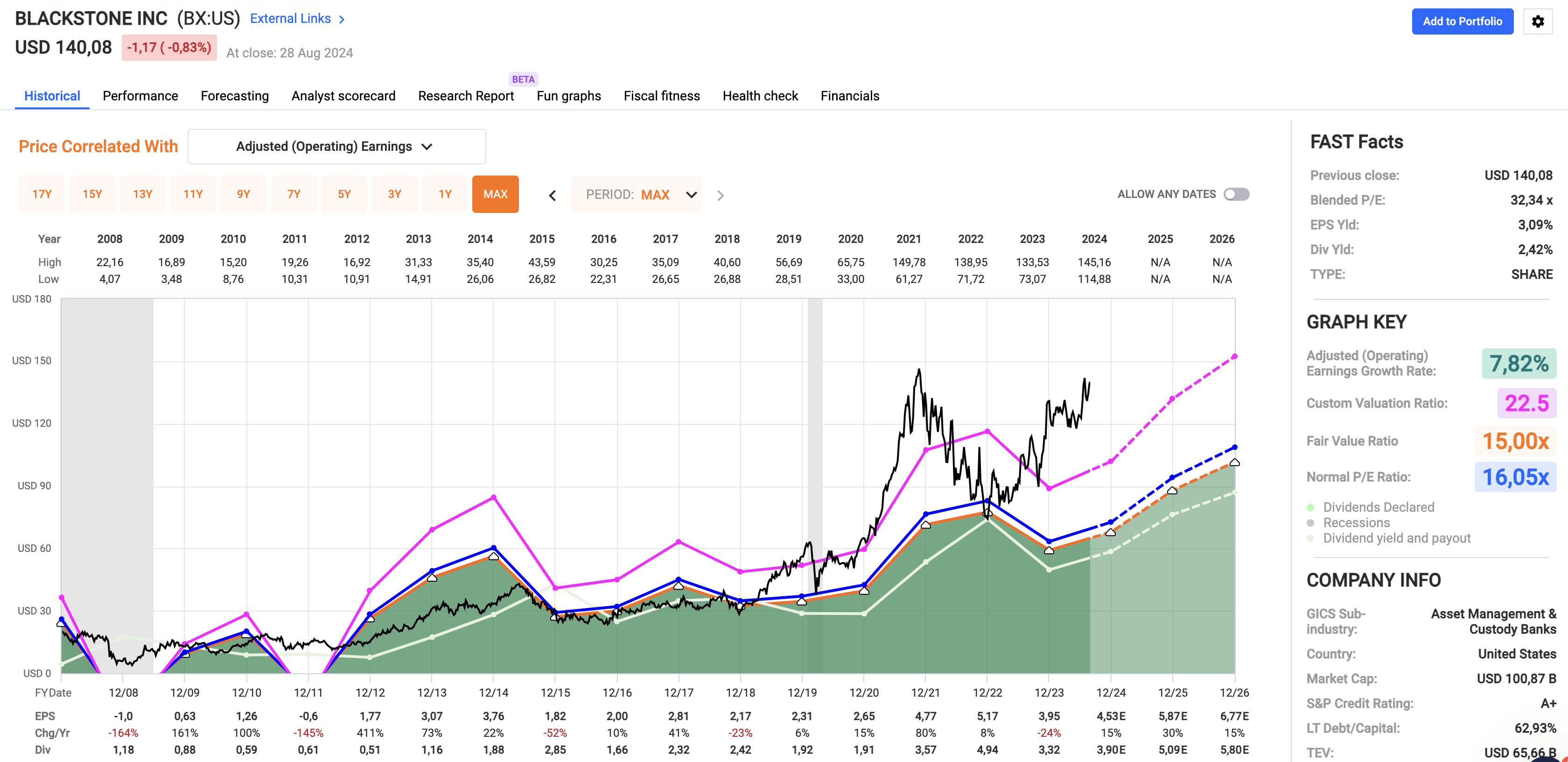

That said, trading at an all-time high, BX isn't deep value. However, using the FactSet data from the chart below, analysts expect 72% cumulative EPS growth in 2024-2026, fueled by lower rates, elevated inflows, and recovering real estate and credit markets.

Applying its five-year average P/E ratio of 22.5 implies a fair stock price target of $152, 9% above the current price. When adding its dividend, the stock could return 7% per year.

FAST Graphs

On a long-term basis, I expect BX to keep outperforming the S&P 500 and believe the private equity giant is a great investment on weakness.

Antero Midstream Corporation (AM) - A Dividend Cutter With A Bright Future

Last, but not least, I wanted to include a company that cut its dividend.

Antero Midstream became a holding of mine in January when I decided to pull the trigger after being bullish on the company for a while.

My most recent article was written on August 2, when I called it my favorite high-yield stock.

Antero Midstream owns the midstream assets of Antero Resources Corporation (AR), one of North America's largest and most efficient natural gas producers. Unlike AR, AM is not directly dependent on natural gas prices, as it is paid on the use of its pipeline system, which consists of more than 600 miles of pipelines, 4.5 billion cubic feet of daily compression capacity, and close to 400 miles of water pipelines.

It also helps that AR has extremely low breakeven prices, allowing it to produce natural gas when others are forced to cut output. This bodes well for AM's volumes.

Antero Midstream

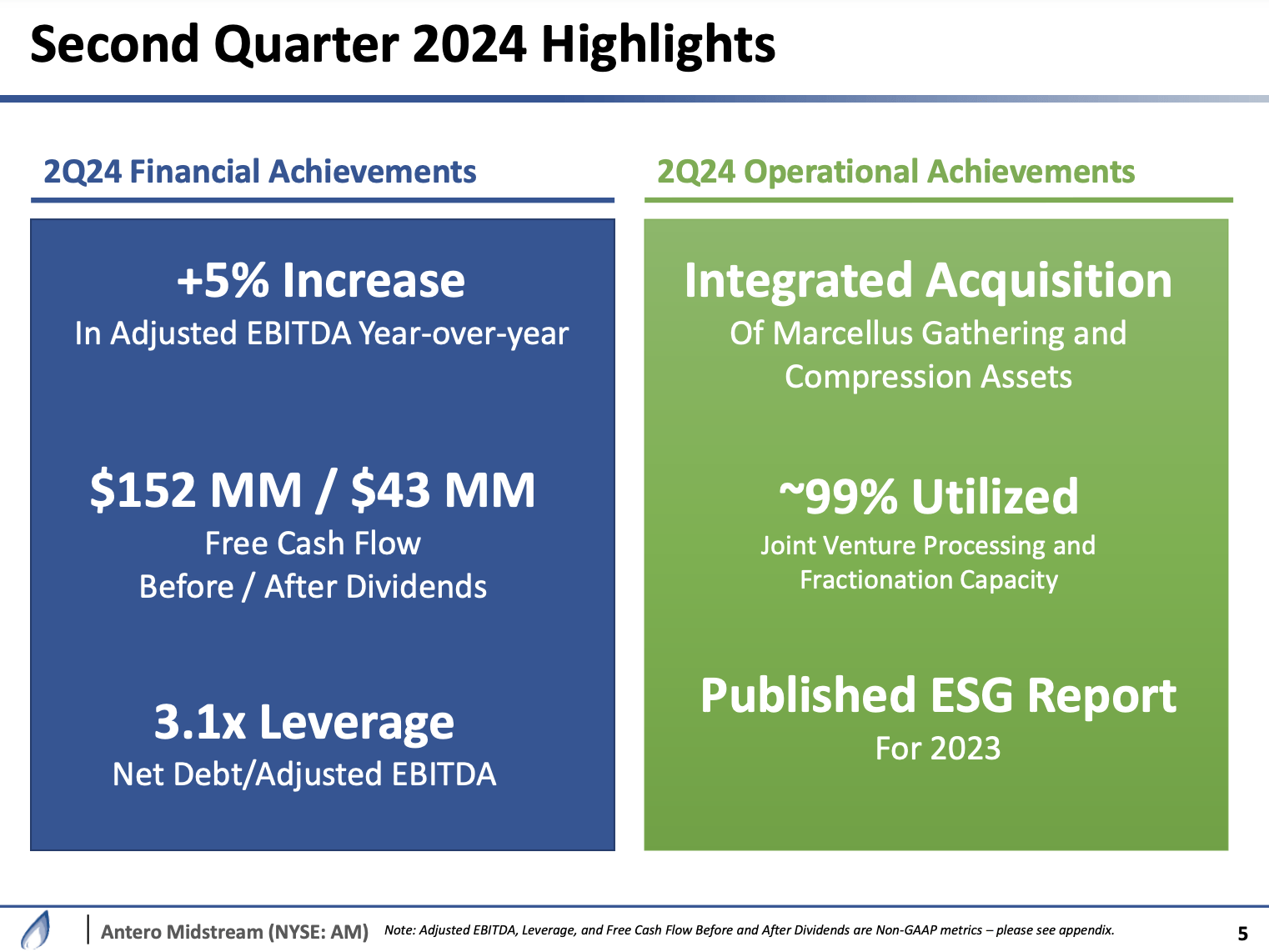

Hence, despite very subdued natural gas prices this year, AM had a fantastic second quarter, growing EBITDA by 5%, reducing leverage to 3.1x EBITDA, acquiring new assets, and generating $43 million in post-dividend free cash flow.

Antero Midstream

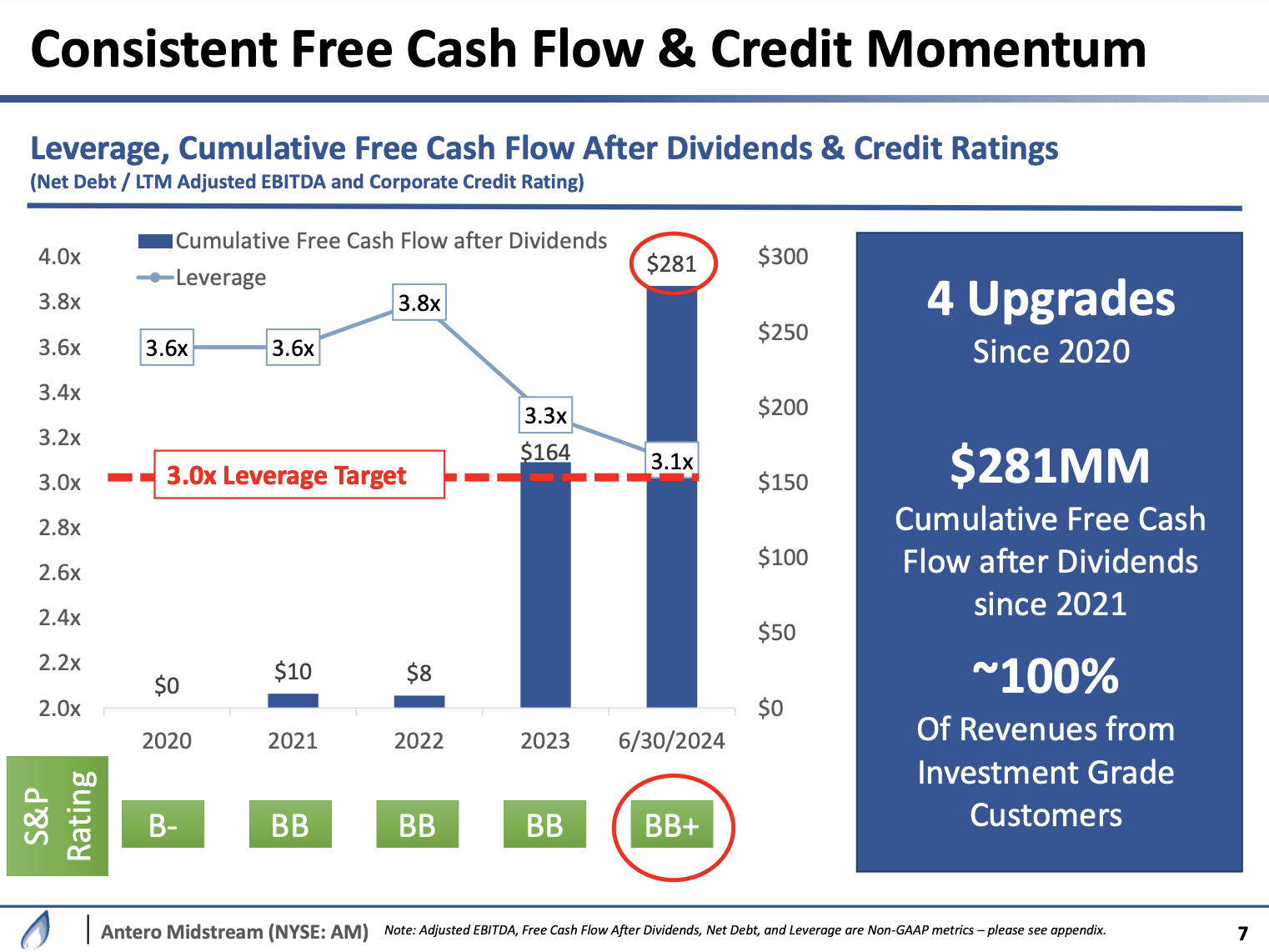

As we can see below, the company has no debt maturities until 2027, close to $700 million in liquidity, and extended major maturities until 2032.

As a result, the company's credit rating has been upgraded four times since 2020. Although a BB+ rating is not an investment-grade rating, the balance sheet is very healthy and supported by predictable income.

Antero Midstream

Once the company reaches its 3.0x leverage target, it will grow its dividend again and use buybacks to improve the per-share value of its business.

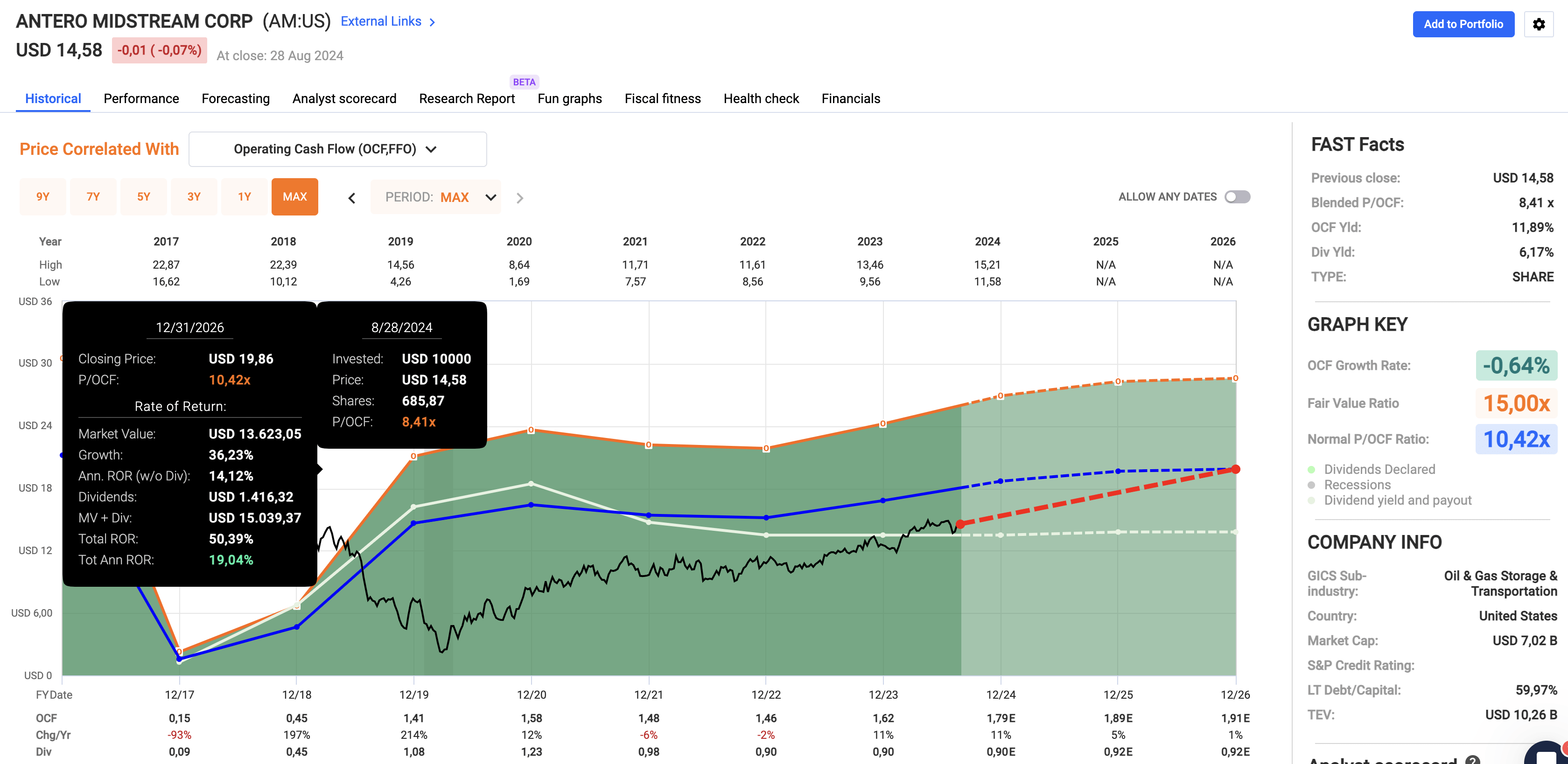

Speaking of the dividend, AM currently pays $0.225 per share per quarter. This translates to a yield of 6.2%.

Data by YCharts

Data by YCharts

In 2021, the company cut its dividend. This was based on its decision to focus on projects with elevated return potential. Back then, most midstream companies were still in the midst of massive expansion projects. This was a great decision, as we're now dealing with a company that enjoys a healthy balance sheet and an implied free cash flow yield of 11%, indicating a lot of room for future dividend growth and buybacks.

Valuation-wise, the company has a bright future. Trading at a blended P/OCF ratio of just 8.4x, it trades two points below its long-term average. Assuming 6-7% cumulative per-share OCF growth through 2026, we get a fair price target of more than $19 (30% above its current price), which is why I expect AM to deliver double-digit annual returns in the years ahead.

It's also why I have consistently added to my position and bought it for a number of family accounts.

FAST Graphs

I believe AM will be one of the best examples of a dividend cutter that turned into a great source of growth and income.

Takeaway

Dividend growth consistency is important, but it's not the be-all and end-all of investing.

While Dividend Aristocrats and Kings have their benefits, it's clear that the market rewards consistency only up to a point.

Companies with long dividend growth streaks may not always deliver the above-average returns many investors expect. That's why it's important to look beyond the label and focus on the underlying fundamentals.

By doing so, we can uncover gems like EOG Resources, Blackstone, and Antero Midstream, companies with strong growth potential and the ability to outperform, even if they don't always follow a "traditional" dividend growth path.

All things considered, buying companies with a Dividend Aristocrat/King tag is a benefit but should never be the starting point of our research.

Comments