Summary

- Texas Pacific Land Corporation and LandBridge Company dominate my portfolio, but Viper Energy, Inc. offers a strong income play with a high-margin royalty model tied to the Permian Basin's growth.

- Viper's partnership with Diamondback Energy provides stability and operational visibility, enhancing its production potential and dividend appeal in a low-cost oil environment.

- Viper Energy's variable dividend policy, offering a potential yield of over 8% at $85 WTI, makes it a top choice for income-focused investors, though yield sensitivity is a concern.

John M Lund Photography Inc

Introduction

By now, I doubt it's a surprise when I say I really like companies that benefit from royalties. Texas Pacific Land Corporation (TPL) and LandBridge Company LLC (LB) are my largest and third-largest investments, respectively. Combined, the two investments account for 19% of my entire portfolio.

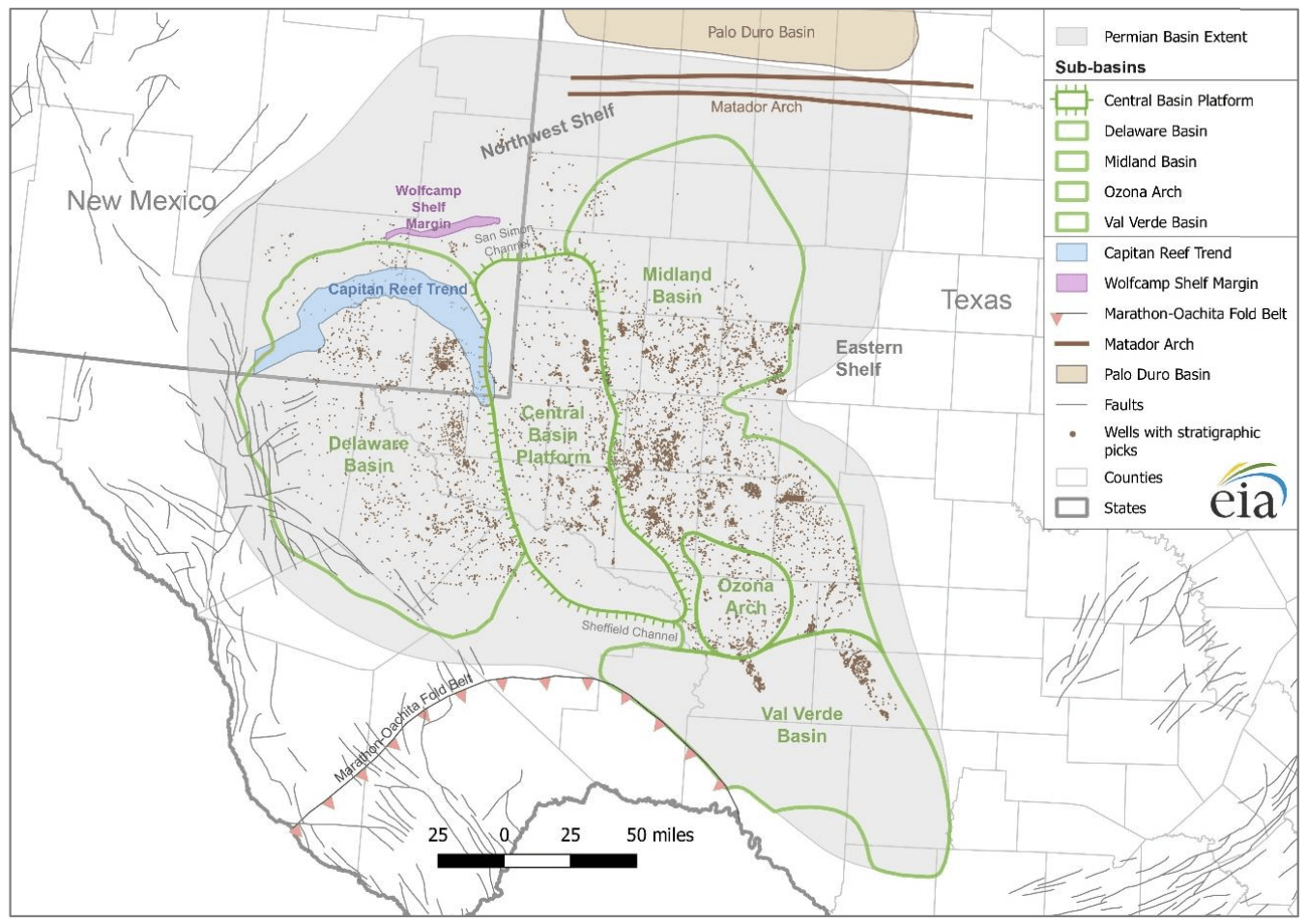

These two companies own massive amounts of land in the Permian Basin, America's most important oil basin located in New Mexico and Texas. This basin alone produces over six million barrels of oil and more than 24 billion cubic feet of natural gas per day. Ignoring natural gas, the basin produces more oil than Iraq, Iran, the UAE, Kuwait, and Nigeria.

Moreover, the basin consists of two major sub-basins, which are the Delaware Basin and the Midland Basin, two of America's most desired spots to find low-cost oil in an environment where the shale revolution has run out of steam.

Energy Information Administration

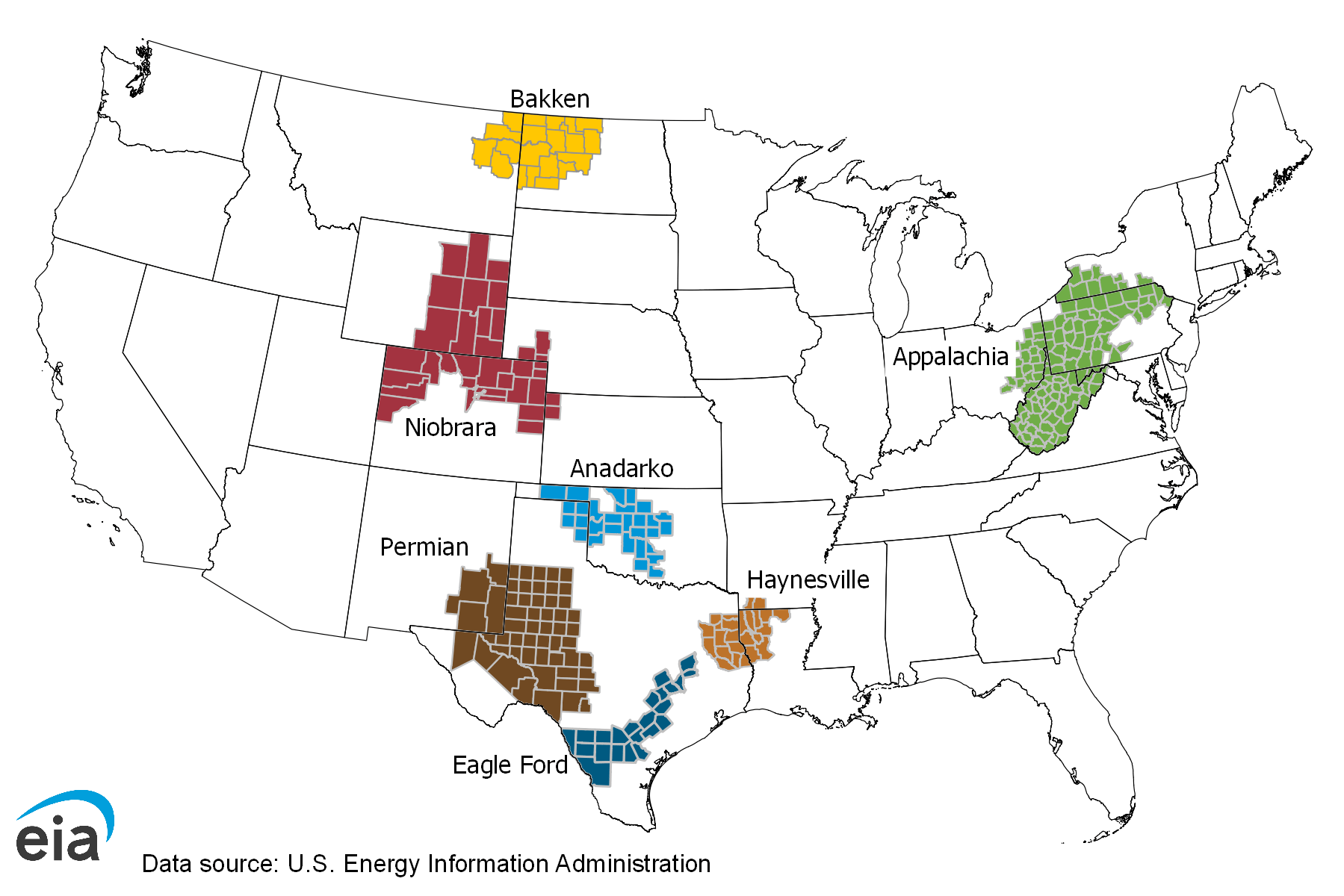

Here's a map showing the nation's biggest oil and gas basins:

Energy Information Administration

The reason I'm bringing all of this up is because whenever I discuss TPL and LB, readers bring up Viper Energy, Inc. (NASDAQ:VNOM) — and rightfully so.

TPL has a base dividend yield of less than 1%, while LB, which went public in June, has not even announced a dividend yet.

Although Viper Energy does not have the surface and water rights benefits that make the aforementioned two players so unique, it is a fantastic source of elevated income. It is a company with a remarkable relationship with its parent company, Diamondback Energy, Inc. (FANG).

My most recent article on VNOM was written on May 21, when I went with the title “Viper Energy: Massive Income Potential And 9% FCF Yield AT $80 Oil Prices.”

Since then, shares have returned 27%.

Hence, after covering TPL and LB, I'll use this article to update my VNOM bull case and explain how attractive the stock is after its most recent rally.

So, as we have a lot to discuss, let's get right to it!

A Fantastic Oil & Gas Business Model

As I already briefly mentioned, my personal decision was to buy lower-yielding landowners who enjoy benefits from surface and water rights. Unfortunately, the trade-off is opting for lower income.

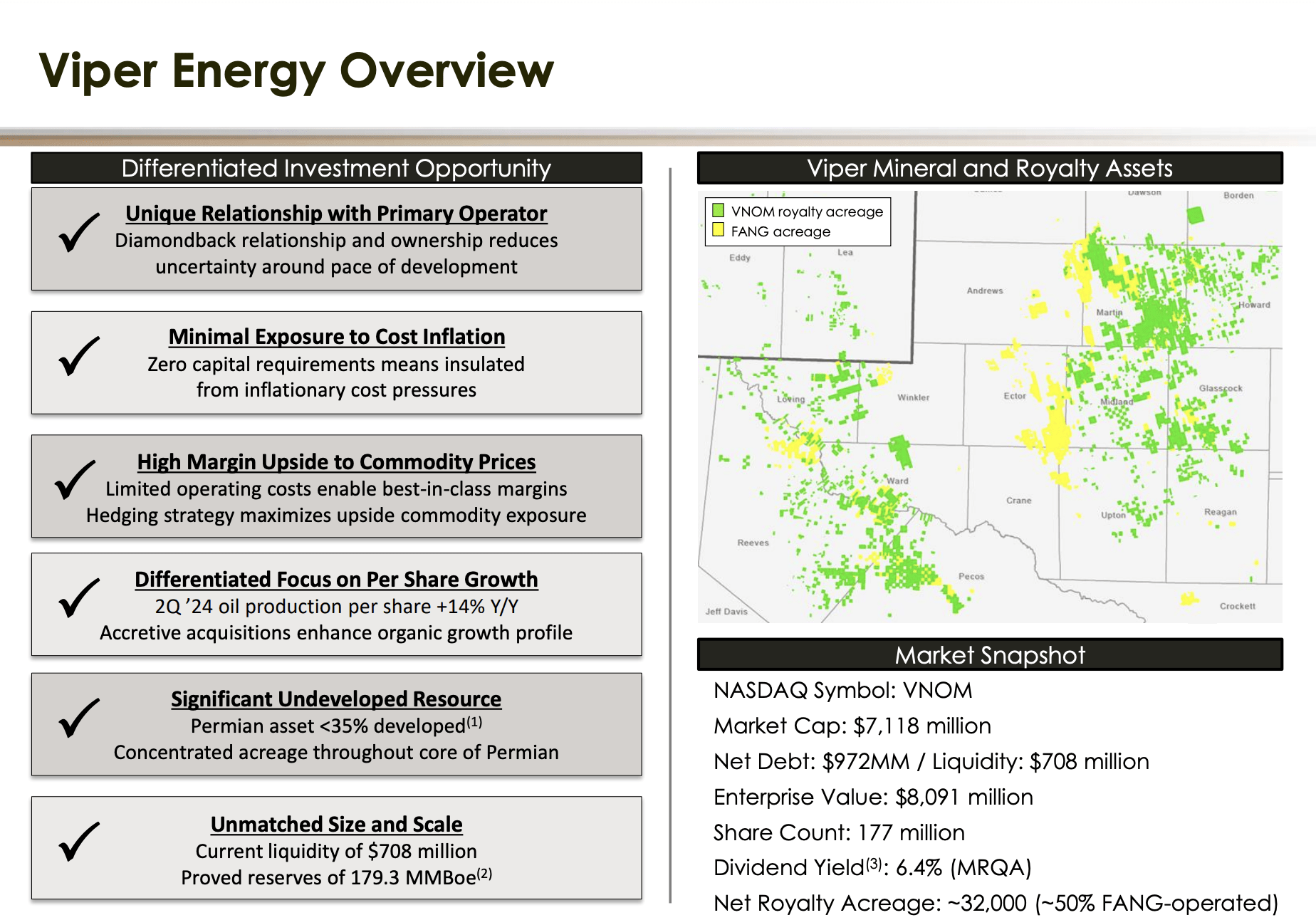

That's where Viper Energy comes in. Going into this year, the company owned mineral and royalty interest on roughly 1.2 million gross acres and 34 thousand net royalty acres, mainly in the Permian Basin. Currently, that number is roughly 32 thousand net acres.

Viper Energy

As we can see above, Diamondback Energy operated roughly half of these net acres. The driller also owns 56% of VNOM's shares, including all Class B Common Stock. Although this makes VNOM highly dependent on Diamondback, it's a good thing for a number of reasons:

- Diamondback is one of America's most efficient onshore drillers. This year, it is working on the merger with Endeavor Energy, a private driller, that will significantly enhance its reserves and production potential. As I have written in a recent article, I believe Diamondback is one of the best energy stocks on the market.

- Being dependent on Diamondback is no problem. The company made the deliberate decision to spin off Viper Energy to streamline its operations. There is no benefit to FANG if VNOM is mismanaged. If VNOM shareholders win, FANG wins as well, as it benefits from a strong royalty partner. This also allows the company to sell more mineral rights to Viper Energy in the future if it likes.

- The relationship between VNOM and FANG creates visibility. By working closely together, both companies have less operating uncertainty. The same can be said about oil drillers who have a major stake in the midstream companies, owning their pipelines and processing assets. It's often a win-win, or a win-win-win, when including shareholders.

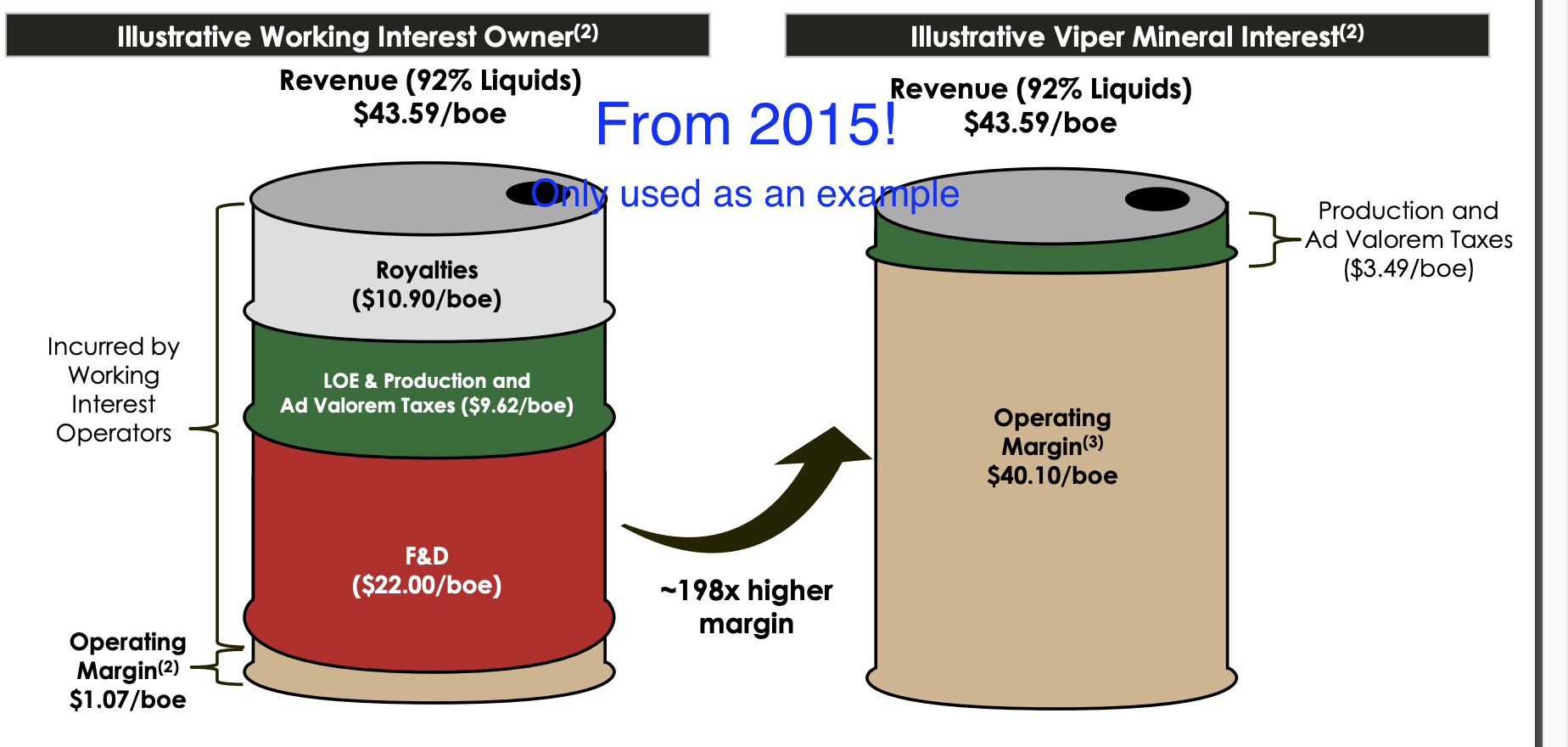

One of the reasons why I like to own the mineral rights owner instead of the driller (I also own drillers) is the favorable cost picture.

As we can see in the company's presentation slide from 2015 (ignore the specific financial numbers), mineral interests mean the company benefits from oil and gas production without having to deal with any of the operating costs.

Viper Energy

This is one of three major benefits the company brings to the table:

- As I just briefly explained, the company has a high-margin business model, as it does not incur drilling costs.

- The Permian is home to almost half of all onshore horizontal rigs in the United States. Essentially, it's the place to be for oil and gas production with elevated reserves and low breakeven prices. In a recent article, I showed the chart below. As we can see, the Permian has mostly undeveloped wells, which bodes well for future production.

Bloomberg

- Related to the second advantage, the Permian also benefits from decent infrastructure, a favorable regulatory environment, and lower operational risks compared to emerging basins. Nonetheless, because of elevated production, more infrastructure is needed in the years ahead, which is one of the reasons why I'm also very bullish on the midstream industry.

I would also add the benefit of inflation protection. Because of its favorable low-cost business model, it benefits from inflation without having to deal with the negative consequences due to the absence of drilling costs.

Moreover, before we move to the next part, please note that Viper Energy is NOT a Limited Partnership. Since its 2017 restructuring, it's a C-Corp, which issues a 1099.

Growth & Income

So far, I have only explained what VNOM is all about. I have not given you many numbers.

Let's change that.

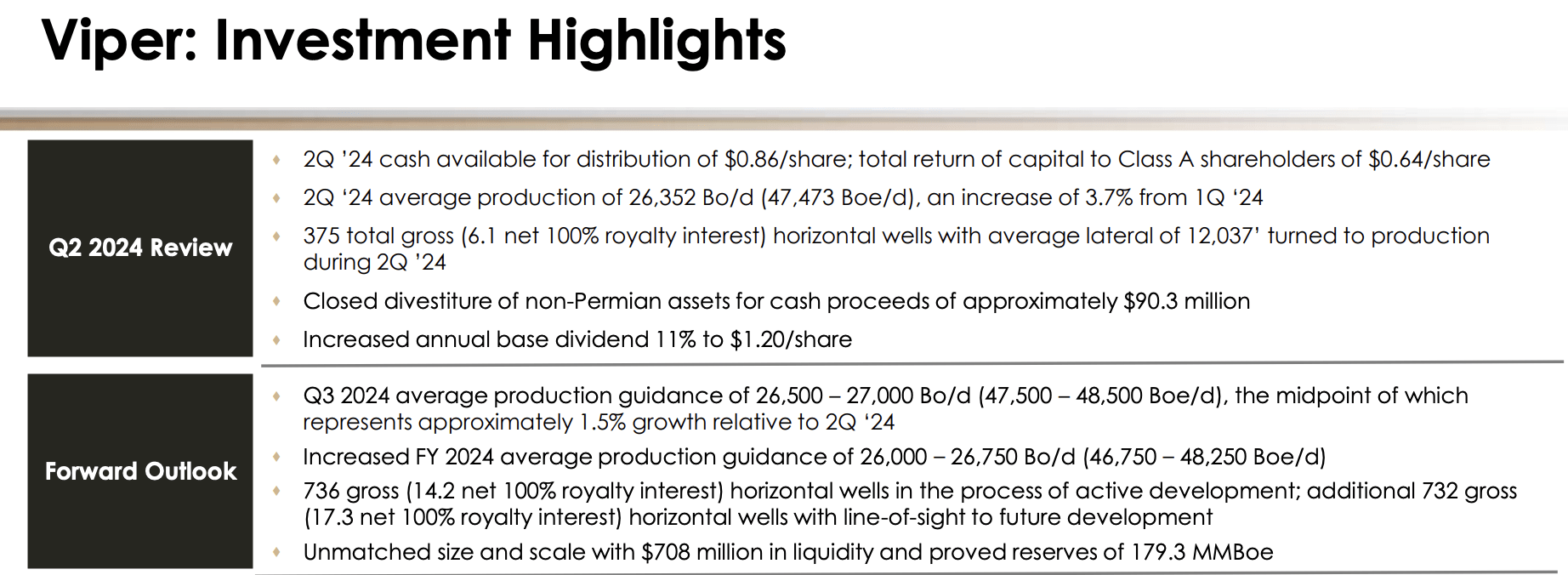

In the second quarter of 2024, its most recent quarter, the company achieved roughly 3.7% quarter-on-quarter production growth to slightly more than 26,350 barrels of oil per day.

This growth trajectory is expected to continue, as the company has raised its full-year guidance to at least 46,750 barrels of oil equivalent per day.

Viper Energy

For the third quarter, Viper expects a 1.5% growth rate compared to the second quarter, even after divesting some non-core assets (150 barrels of oil per day).

This is supported by elevated activity on its land. According to the company, it sees strong activity levels on its acreage, including large-scale development from Diamondback.

To me, this is encouraging, as oil prices (CL1:COM) haven't been doing so well recently. The good news is that oil prices are back at $75, which is generally a level that encourages production growth in the Permian.

Hence, during the M&A part of its earnings call, the company noted that it expects a significant ramp-up in production in the second half of the year, thanks to several “paying wells or paying pads” coming online.

So far, so good.

What matters is how shareholders benefit from this. As I have written in prior articles, Viper Energy has a very favorable dividend growth policy.

Because of a net leverage ratio of just 1.1x EBITDA and a low-cost business model, most of its cash ends up in shareholders' pockets. In the second quarter, the company hiked its base dividend by 11% to $0.30 per share per quarter. This translates to an annualized yield of 2.5%.

At current production levels, the increased dividend represents roughly 50% of the expected free cash flow at $50 WTI and remains protected even if oil prices drop below $30 WTI. That's how safe this dividend is.

Viper Energy

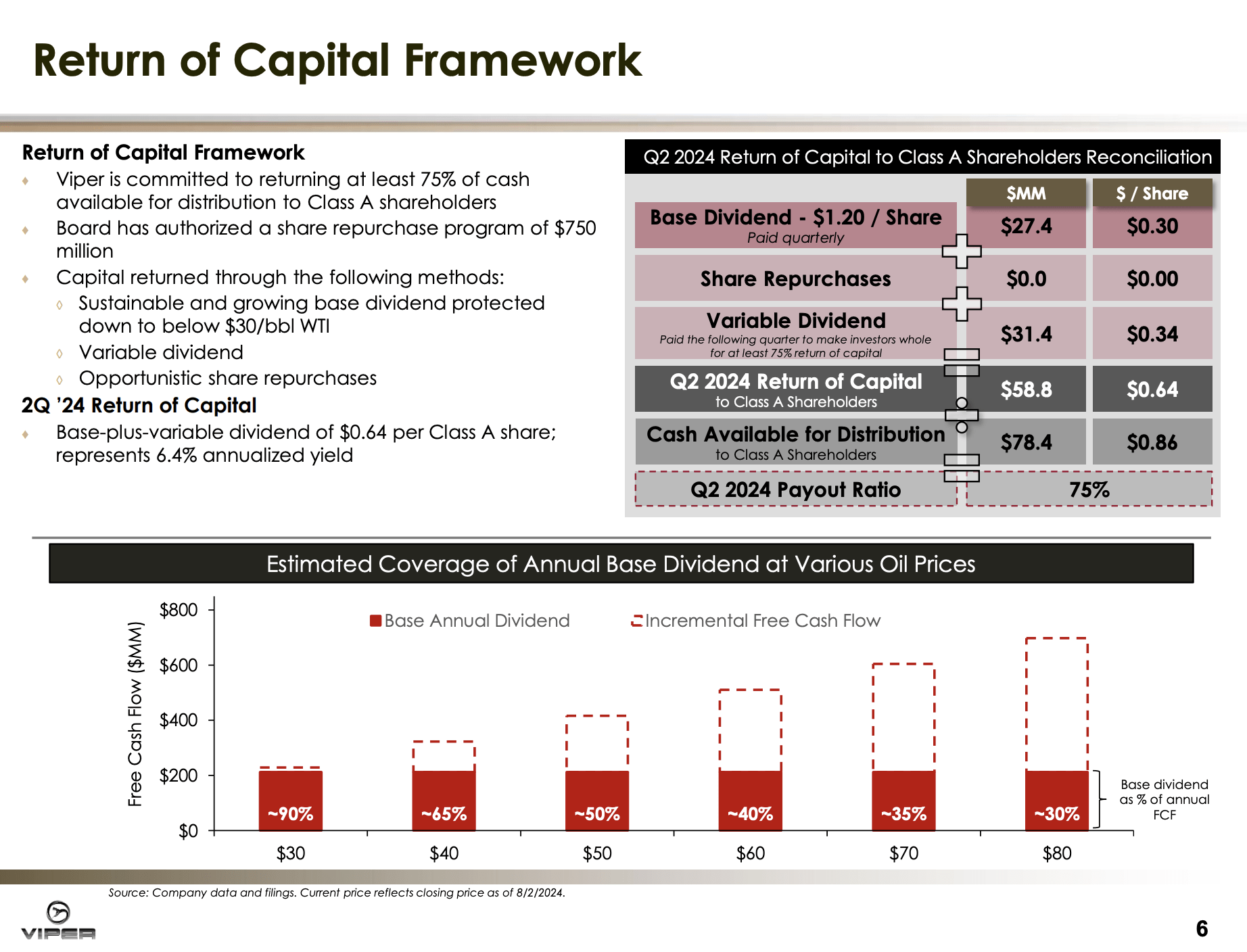

Now, we get to the good part. As a 2.5% base yield is nothing to write home about, the company also has a variable dividend.

Viper Energy is committed to returning at least 75% of its cash to shareholders. For that, it uses variable dividends and buybacks, with variable dividends being preferred over buybacks. In the second quarter, the company returned $0.64 in dividends. This translates to a current annualized yield of 5.3%.

Viper Energy

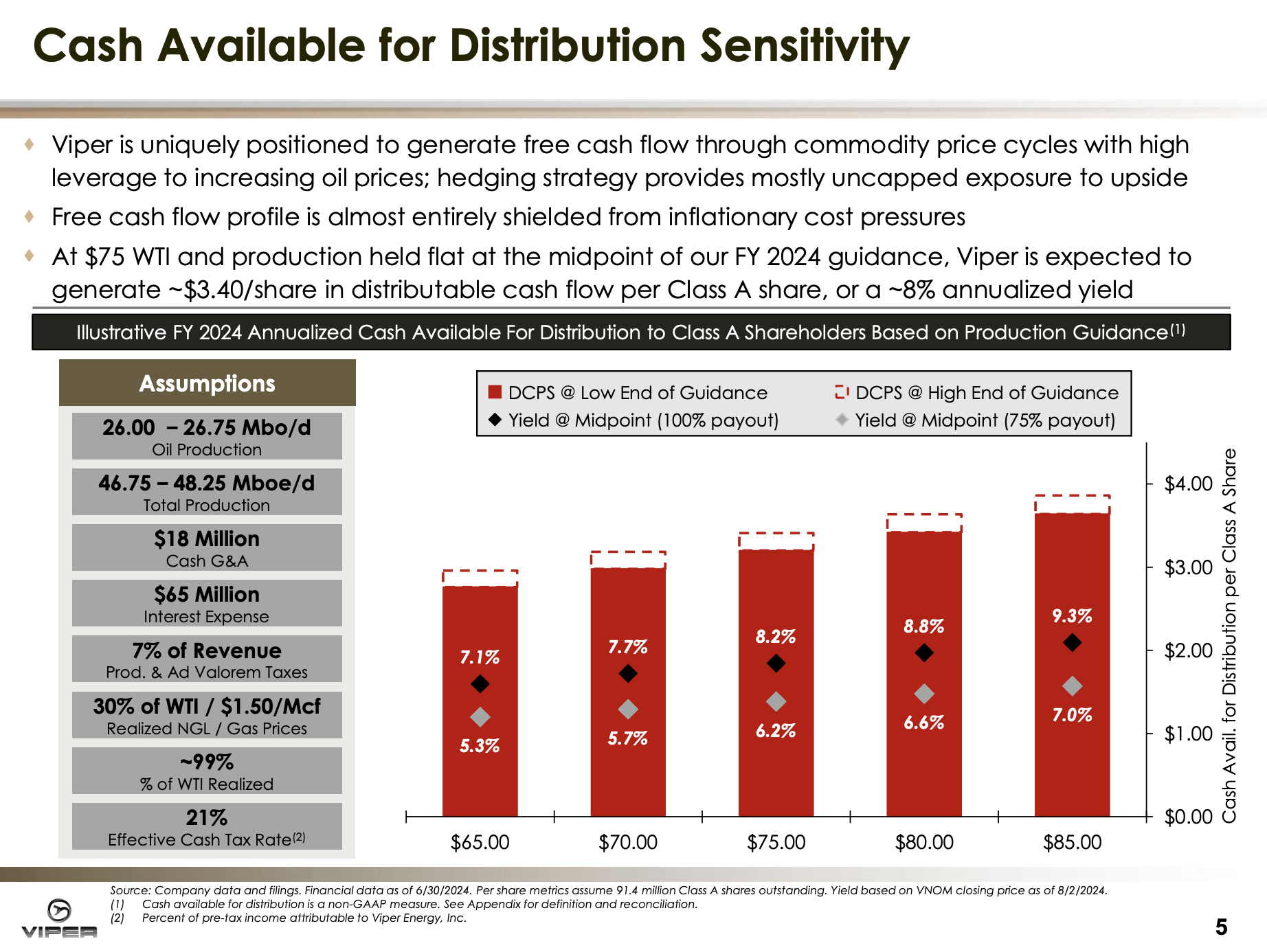

To show us what we can expect in terms of potential dividends, the company made the graph below. Please note that this excludes the future impact of buybacks and production growth. After all, both production growth and buybacks improve the per-share value of the business.

Currently, at $75 WTI, the company is expected to generate $3.40 in distributable cash flow. This currently implies a 7.1% yield. At $85, that number rises to almost $4.00, indicating an annualized yield of 8.3%.

Viper Energy

This is also the valuation part of this article, as it's all about one's income goals.

Personally, I still like VNOM at current prices. A potential yield of 8.3% at $85 WTI is highly competitive, especially compared to most upstream companies with much riskier business models.

However, I would not buy VNOM if it were to keep rising 5-10% this year. That would reduce the potential yield too much for me.

Data by YCharts

Data by YCharts

That said, as I just mentioned, at current prices, VNOM is still a Buy, benefitting from consistent production growth in the Permian, a fantastic business model, a healthy balance sheet, and its focus on special dividends to reward its shareholders.

I truly believe the value VNOM brings to the table is difficult to beat in the energy space.

Takeaway

Viper Energy remains a remarkable investment choice for those seeking reliable income and exposure to the energy sector.

While my portfolio leans towards lower-yielding landowners like TPL and LB, VNOM offers a compelling balance of growth and income.

Its partnership with Diamondback Energy provides stability, and the company's variable dividend policy ensures shareholders benefit directly from its success.

With a potential yield of 8.3% at $85 WTI, VNOM is still attractive at current levels.

However, I'd be cautious if the stock continues to rise, as it may lower its yield appeal.

For now, however, VNOM is a solid buy in the energy sector, with a business model that's difficult to beat.

Pros & Cons

Pros:

- High-Margin Business Model: VNOM benefits from oil and gas production without the drilling costs, thanks to its royalty interests.

- Strong Partnership: Its close relationship with Diamondback Energy provides stability, operational visibility, and growth opportunities.

- Attractive Dividend Policy: With a variable dividend targeting 75% of cash returns to shareholders, VNOM offers a potential yield of more than 8% at $85 WTI, making it a great choice for income-focused investors.

- Permian Exposure: As the biggest U.S. oil basin, the basin's low breakeven costs and strong infrastructure are favorable for long-term growth.

Cons:

- Market/Commodity Volatility: Energy stocks can be highly volatile, and VNOM is no exception. While it has a low-cost business model, it is still prone to oil and gas prices.

- Limited Diversification: Unlike Texas Pacific and LandBridge, the company has no surface and water rights, which prevents it from benefitting from operations in water sales, pipelines, and similar.

Comments