Summary

- Diamondback Energy is poised for growth, supported by its merger with Endeavor, which will enhance its position in the Permian Basin.

- The oil market remains range-bound, but geopolitical tensions and low US supply growth could drive prices higher, benefiting FANG's free cash flow.

- FANG's valuation is almost reasonable compared to peers, with potential upside from higher oil prices and increased production capacity post-merger.

- US oil producers like FANG offer a hedge against geopolitical risks and inflation, making them a strategic addition to portfolios.

Pla2na

The energy market has been among the few to be eerily quiet in 2024. While stocks face heightened volatility and gold surges to consecutive all-time highs, crude oil remains stuck in the ~$70 to ~$80 range since the end of 2022. Geopolitical turbulence and tensions have occasionally caused sharp changes in the price of oil. Still, both concerns of a demand-driven decline or a supply shock surge have failed, leaving most oil producers stagnant.

I've covered Diamondback Energy (NASDAQ:FANG) since 2022, initially with a bullish outlook, changing to neutral after it delivered an 80% gain by April of this year. I analyzed it last in "Diamondback Energy: Oil Outlook Improving, But Valuation Is Stretched, And Merger May Fail," with a neutral outlook. It has fallen by 4.2% since then, effectively unchanged, but it briefly slipped to $185 in June. The article notes that my "buy price" for FANG was $170.

Not much has changed since April, but the stock has maintained its ~$200 price, implying that may be its firm support level. Oil prices remain range-bound, while global production and demand are essentially flat. That said, we're seeing increased signs that the oil price range will soon be broken. That may be to the upside, stemming from low US supply growth and more signs of outages in the Middle East.

Further, it appears likely that Diamondback will finish its merger with Endeavor (EDV) in Q4, subject to FTC approval. Despite the current FTC's usual stance to block mergers, this deal is expected to go through based on how close EDV is to its acquisition price. This deal will bring critical changes to the combined company, which I expect will improve its position if overseas oil production remains precarious.

FANG's Valuation Accounts for Merger Synergy

Diamondback is among the largest oil producers in the Permian Basin and will be the largest following its merger with Endeavor. The vast majority of its revenue comes from crude oil, which it produces at a cash operating cost of $11.67 per BOE, which includes lease costs, general and administrative expenses, taxes, and downstream expenses. The company has slowly but steadily increased its production despite moderate reductions to its capital spending program. That follows the important trend of most US producers, particularly those in the Permian, focusing more on negative financing cash-flows (dividends, deleveraging, and repurchasing) instead of growth since 2020.

At any rate, the company's performance is directly tied to the oil price. According to its sensitivity analysis, its annual free cash flow should be around $2.7B at a $60 oil price, $3B at $70, $3.3B at $80, and $3.6B at $90, or $300M for every $10 increase in oil price. That assumes production is in line with its recent 2024 guidance and there are no sharp variations in production costs. The company also aims to return half of its FCF to shareholders through dividends and repurchases.

Oil has averaged around $80 over the past year, while FANG has had ~$2.1B in FCF, implying its free cash-flow returns on oil are expected to rise. That is likely true, given it had $842M in FCF last quarter at an average realized price of $79.5., which is ~$3.37B annualized. At the current $77 oil price, we should expect an FCF of around $3.2B, giving it an FCF-to-EV yield of around 7.9%.

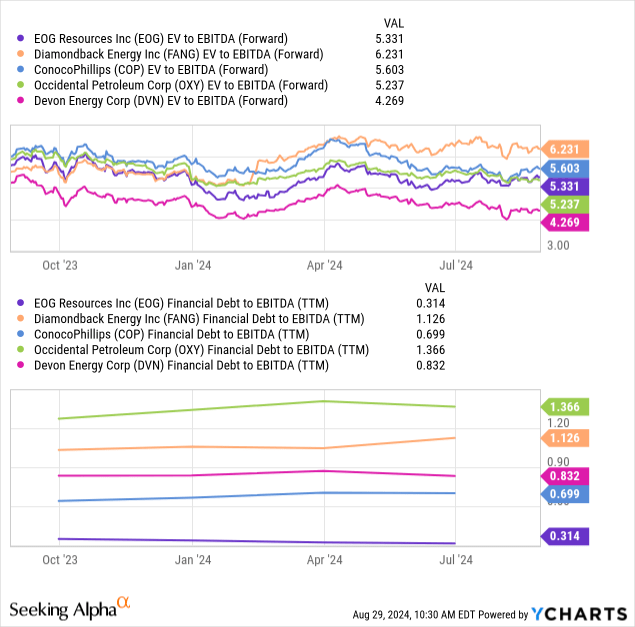

Still, looking at forward valuations, FANG is more expensive than its peers due to its higher leverage not impacting its valuation. Its forward "P/E" is the median compared to the other major producers in the Permian, but its forward "EV/EBITDA" is higher, as well as its leverage. See below:

Data by YCharts

Data by YCharts

I think we must consider whether debt matters to major E&P companies anymore. Years ago, and 2020 in particular, when oil was stuck at a much lower price, Diamondback and many of its peers struggled to survive. Today, they're reaping the rewards of significant investments made then, with cash flows magnitudes higher than interest costs on debt.

Diamondback's leverage will rise following its merger, as it uses cash, shares, and borrowings from its senior notes and term loans to complete the merger. According to its assessments, its ~$40B in EV will be combined with Endeavor's ~$30B to create a $70B giant. This should result in a near-doubling of its net Midland acreage, expected to result in $550M in annual synergies.

Assuming the oil price remains above all-included breakeven costs, likely around $70 for new wells in the Permian ($40 for existing), this merger should be substantially accretive in the long term. While it may be that Diamondback is overvalued compared to its peers, given its higher debt, the cost of that debt is relatively low compared to the potential cash flows from future investments. Thus, based on the current price of oil and its current outlook, I believe Diamondback is pretty valued today compared to its peers. Still, I think its upside from an increase in oil prices may be higher due to the added growth capacity that should come from its merger.

Updated Oil Price Macroeconomic Outlook

Lackluster supply and demand trends obfuscate the outlook for oil. On the one hand, demand for oil and petroleum products has been globally stuck for years and is likely at a peak. Conversely, continued geopolitical tensions and issues in the Middle East threaten global supplies. The supply side of the problem is more critical because conflicts in the Middle East may lower global oil production by multiple percentage points. In contrast, a sharp global recession may only reduce consumption by a few points.

Normal recessions usually result in a 0-4% oil demand decline. A recession did not drive the catastrophic oil demand drop in 2020, but global lockdowns that directly forced lower travel and transportation activity. Global oil production is around 82 million barrels per day. Diamondback produces around 470K BOE per day.

Oil recently surged as Lybia's production fell by around 700K daily amid a standoff between political factions over central bank control, marking a nearly 1% decline in global production. This will impact the supply-demand balance; however, if we see similar trends in other nations, it will be much greater. Iraq is a much larger exporter (3.7M+ BPD), which I believe faces very similar risks given its rising political and economic turbulence. Nigeria and Venezuela may also be affected by similar issues.

Ukraine's increasing ability to strike Russian oil facilities may also disrupt exports from the world's second-largest producer. An Iran-Israel conflict would threaten Iran's exports and potentially the ability of Saudi Arabia to export oil through the straits.

I find it surprising that oil has not risen in response to this risk factor. This could indicate that this conflict is more talk than substance, or that its consequences are so significant that market participants are not able to price accordingly. A quarter of global supplies flow through the Strait of Hormuz. If that were blocked, even for a short period, an international oil crisis would likely cause prices to rise well above all-time highs.

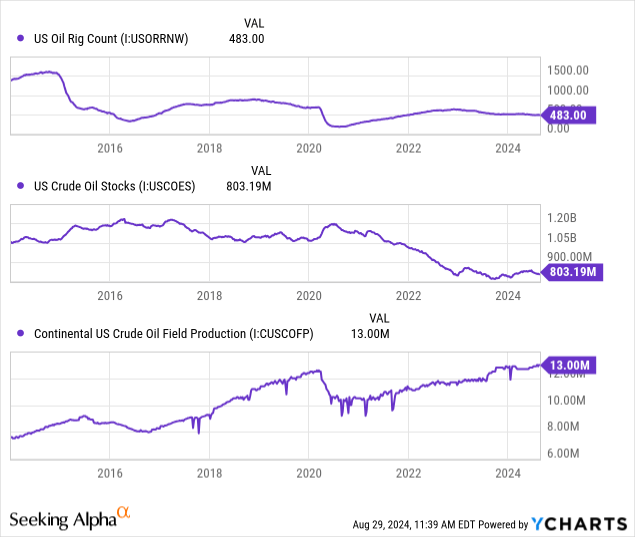

Serious global lockdowns only caused a 10% drop in oil consumption, so the impact of such a potential shortfall would likely be extreme. For me, that is enough reason to buy US oil producers like Diamondback to hedge against this critical risk factor. It may be exacerbated by low US oil storage inventories, with future production growth likely to be flat to negative given the rig count and low inventories of drilled but uncompleted wells. See below:

Data by YCharts

Data by YCharts

Continued US production growth will likely require a higher rig count given the previous support of "drilled but uncompleted" wells is largely gone, as those wells have been a source of cheap production growth for companies like Diamondback. With this in mind, I believe US oil production should remain stagnant or could even decline without improving drilling rates, which would likely require higher oil prices.

Low oil inventories would exacerbate the price impact of a geopolitical event, given the lack of reserves in the SPR. On the flip side, the low SPR reserves offer support for oil at $70 per barrel, given that the Biden administration is buying oil if it falls around that price. Trump has said he will seek to refill the SPR quickly, which would be bullish for oil.

The Bottom Line

I am slightly bullish on FANG today, upgrading it from my previously neutral outlook. There are a few reasons behind my improved outlook. One, the company has shown an ability to raise its free cash flow at the current price of oil, pushing its valuation closer to that of its peers. Two, I feel there are more immediate geopolitical catalysts for higher oil prices, with the Lybian crisis potentially being a "canary in the coal mine."

In my view, US producers, with their innate capacity to export abroad and lack of political risk (compared to the Middle East), make them an ideal portfolio hedge against oil price risk. Remember, a geopolitical oil price shock would hamper the economy while raising inflation, meaning stocks and bonds may decline in that scenario while tying up the Federal Reserve's ability to stimulate the economy. Thus, stocks like FANG are among the few that should offer strong hedges against this risk. With its widening size in the Permian Basin and a reasonable valuation, I think some exposure to FANG may be wise today.

Comments