Summary

- BlackRock's immense scale and strategic growth into high-demand areas make it a powerhouse, compounding returns and outpacing competitors.

- The firm's diversified approach, strong AUM growth, and acquisitions like GIP and Preqin drive its resilience and expand market influence.

- With consistent dividend hikes and buybacks, BlackRock offers robust shareholder value, making it a compelling investment despite its size concerns.

Philip Thurston/E+ via Getty Images

Introduction

I have to be honest. Sometimes, investing feels like being a very small fish in a very big pond. When I was a kid, we used to play a simple online game where a player started as a small fish. We then had to eat smaller fish. The bigger we got, the bigger our potential prey became.

Vecteezy

As silly as that sounds, it's a real issue on the stock market.

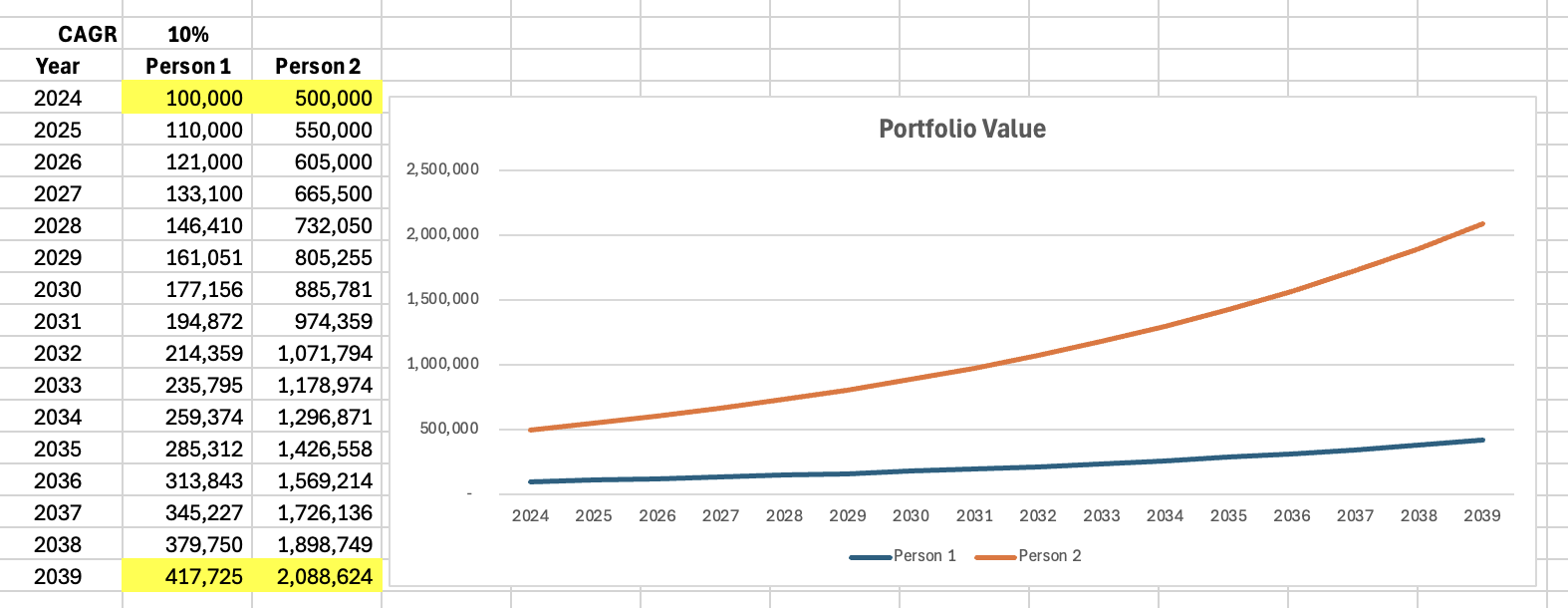

For example, let's assume two people start investing in 2024. One of them has $100,000. The other has $500,000. If we assume none of them invest a penny of additional cash in the future and return 10% per year, Person 1 turns $100,000 into $417,725 in 2039. That's a terrific result (all else being equal).

Personal 2, however, turned $500,000 into almost $2.1 million. Although he is still 5x richer than Person 1, the absolute wealth difference is more than $1.5 million.

Leo Nelissen

Don't get me wrong. This is not an attempt to discourage people from investing. All else being equal, Person 1 made the right choice. Every penny invested in the stock market is a smart decision.

My point is that compounded interest turns winners into even bigger winners.

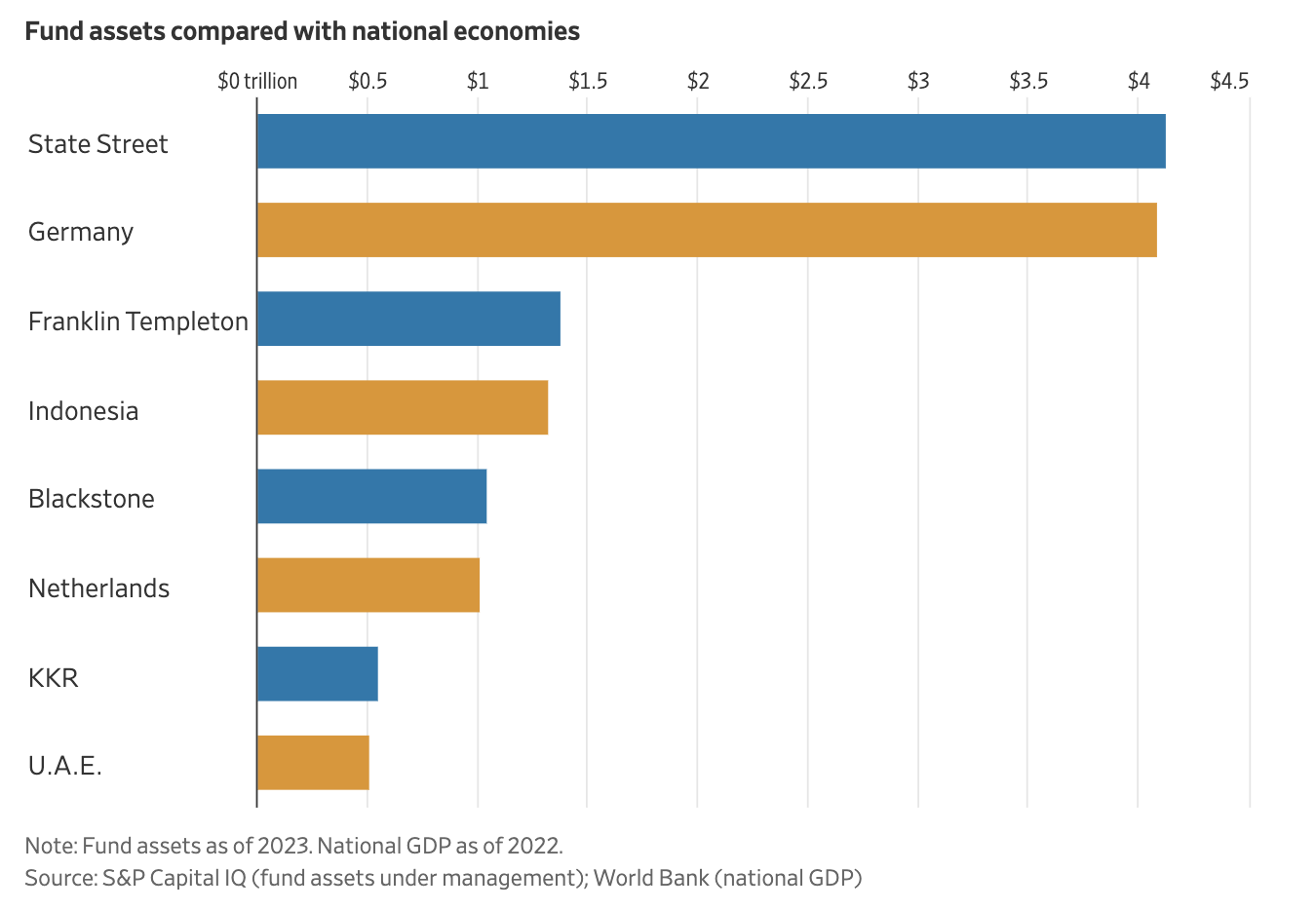

Based on that context, in April of this year, The Wall Street Journal wrote an interesting article titled "Move Aside, Big Banks: Giant Funds Now Rule Wall Street."

It used the chart below. Although it's always tricky to compare a corporation to a sovereign nation, the point is that fund-management companies have been bulking up in the past two decades, becoming more powerful in an increasing number of financial segments. Last year, State Street (STT), for example, managed more than $4 trillion, more than Germany.

The Wall Street Journal

According to the article:

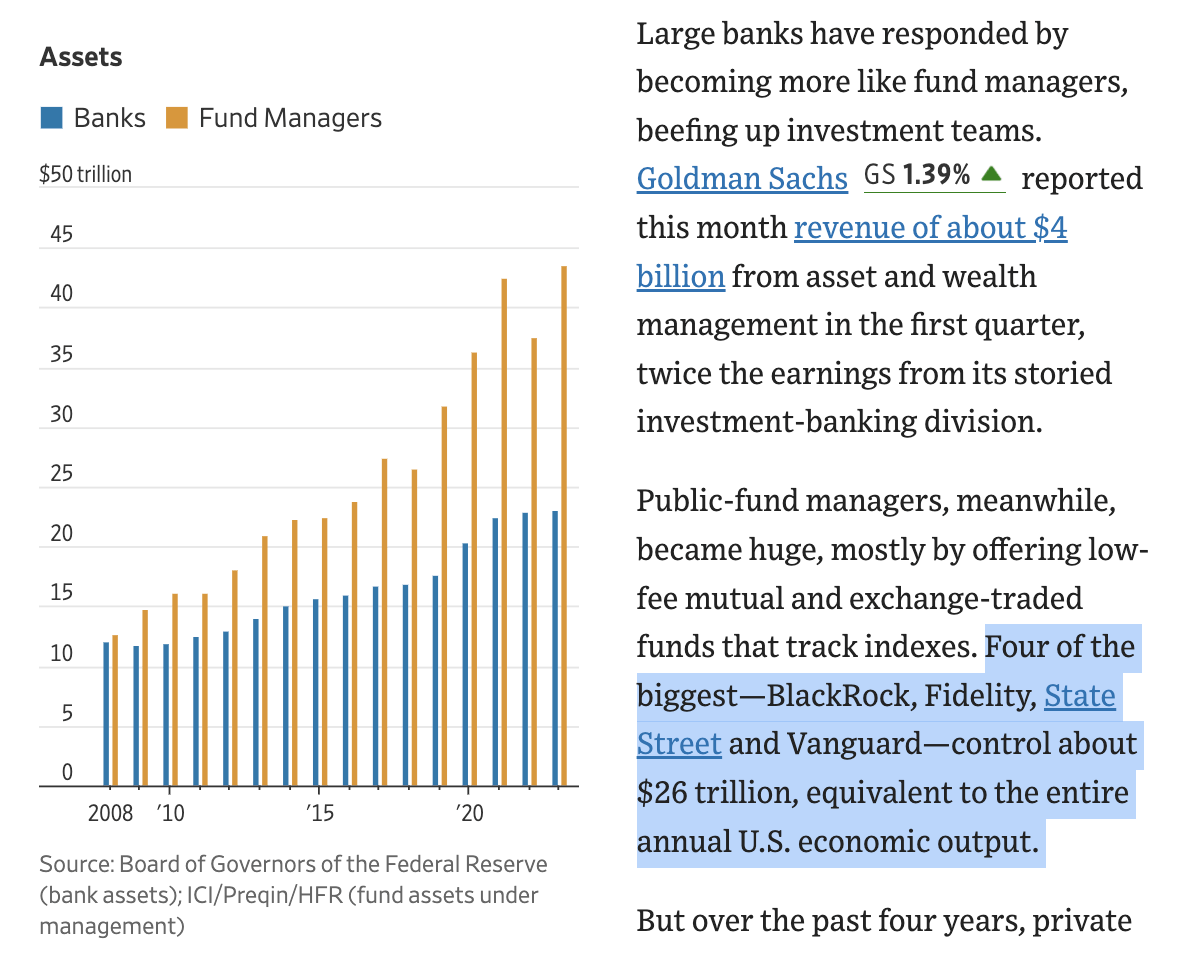

Private-equity and private-debt funds, such as Apollo Global Management and Blackstone, mostly manage money for institutions but are increasingly selling products to individual investors. Mutual-fund behemoths, including BlackRock, are growing bigger still by building or buying private-fund operations.

In 2008, banks and fund managers had similar assets. Now, fund managers have almost twice as many assets as banks. As a result, banks are increasingly diversifying, while giants like BlackRock (NYSE:BLK) (NEOE:BLK:CA), Fidelity, State Street, and Vanguard control more than the equivalent of the entire annual U.S. economic output.

The Wall Street Journal

Needless to say, they are far from done growing!

Hence, in this article, I'll update my thesis on BlackRock. My most recent article on this giant was written on April 12, when I went with the title "BlackRock: 15% Annual Returns Since 2004 - And It's Far From Done."

Since then, shares have returned 18%, beating the 10% return of the S&P 500.

In light of what we just discussed, its latest quarterly earnings, and new developments, I'll use this article to explain why I remain extremely upbeat about the future of the BLK ticker.

So, let's get to it!

BlackRock Is Firing On All Cylinders

Personally, I am not a big fan of the fact that some corporations are becoming so incredibly powerful. When I worked for a company that provided geopolitical and macroeconomic research to institutions and private clients, I worked on a project to identify the political influence of some of these corporations.

The influence was truly astonishing, as there's no way around these companies in many situations. On a side note, please note that I am by no means inferring corruption on any political level. I'm not accusing anyone of anything. This is just an observation of mine.

However, because of the aforementioned compounding interest effect and ventures into new financial sectors, these giants are hard to stop, as they are making the lives of many corporations and individuals so much easier.

As I keep telling most inexperienced investors to invest in ETFs, I'm one of the reasons why these companies keep getting bigger.

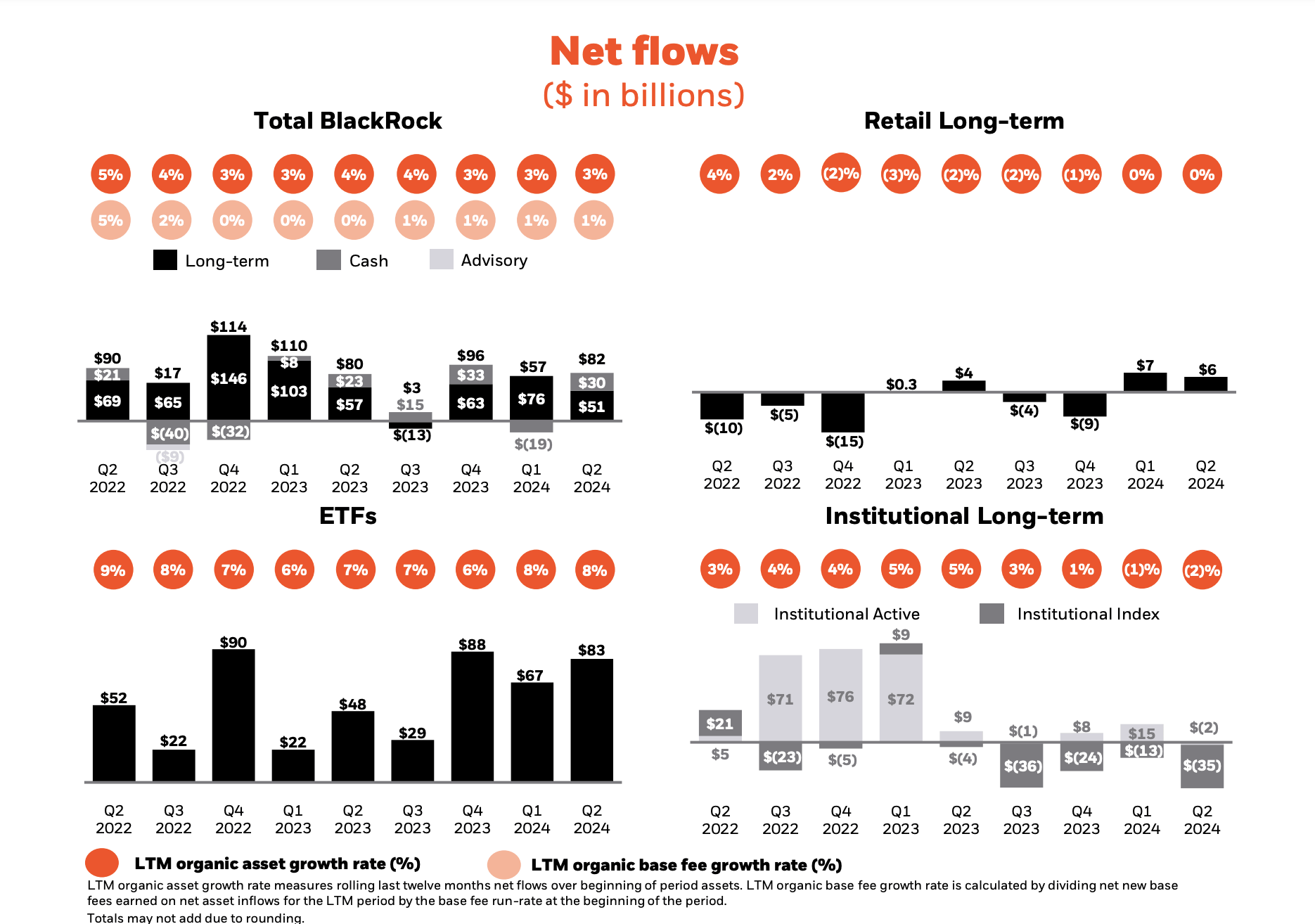

With that in mind, in the second quarter of 2024, BlackRock achieved a record $10.6 trillion in assets under management ("AUM"). This was driven by $82 billion in net inflows and translates to a 3% annualized organic asset and base fee growth rate.

BlackRock

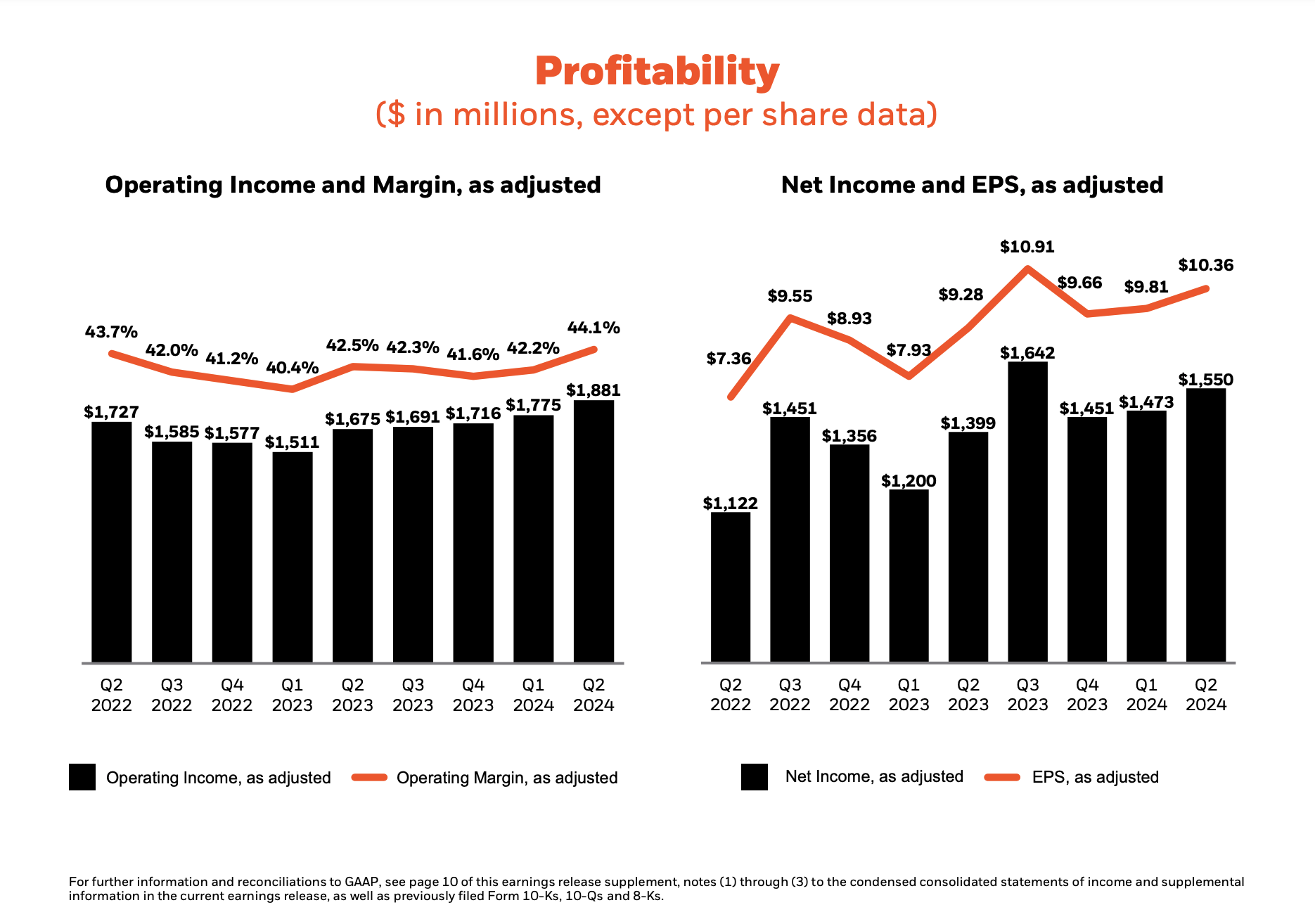

As a result, the company generated $4.8 billion in quarterly revenues, 8% more compared to the second quarter of 2023. Thanks to higher margins, operating income, and earnings per share both rose by 12%.

Additionally, as we can see above, in the first half of this year, it saw ETF inflows of $150 billion, as its iShares platform continues to do extremely well with high single-digit organic growth rates.

This is no surprise, as it has a fantastic ETF selection, including the world's biggest Bitcoin ETF, which shows that even for new products, it's the go-to provider.

BlackRock

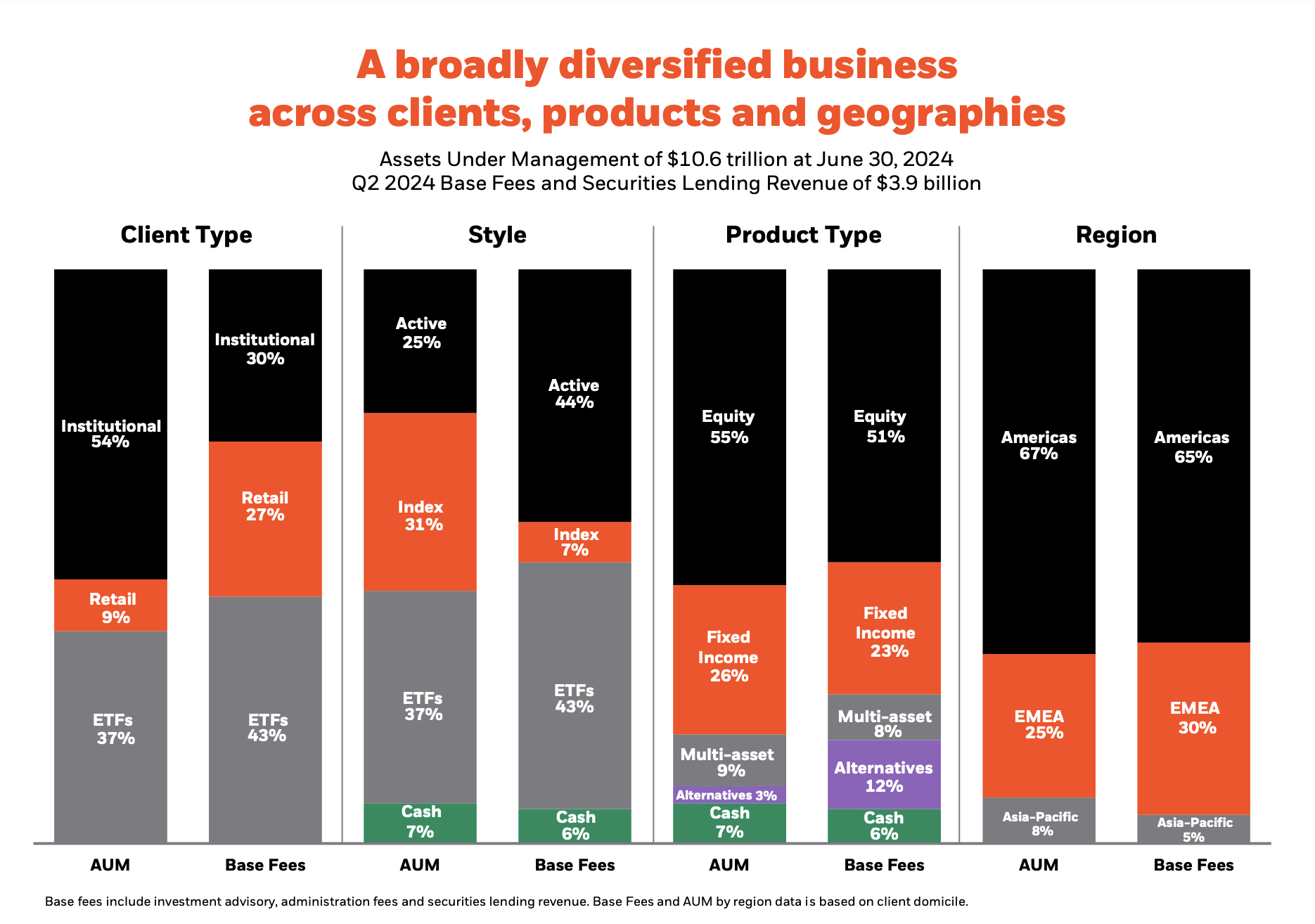

Moreover, what's interesting is the company's increasing diversification. As we discussed in the first part of this article, BlackRock (like its peers) is reaping the benefits of diversification.

The company makes the case that it is increasingly protected against economic downturns, as it is strategically building its revenue mix towards higher secular growth areas like private markets, technology, and whole portfolio mandates.

This also includes aggressive growth in areas like infrastructure, thanks to the acquisition of Global Infrastructure Partners ("GIP"). Moreover, in July, the company announced to buy Preqin for $3.2 billion. Prequin is not an infrastructure company but a data provider.

As reported by Bloomberg, this allows the company to capture more growth and create synergies with existing products.

The acquisition deepens BlackRock’s ability to oversee risks and analyze data across fast-growing markets for private assets, and also expands its Aladdin technology systems, the New York-based firm said in a statement on Sunday.

“We see data powering the industry across technology, capital formation, investing and risk management,” Rob Goldstein, BlackRock chief operating officer, said in the statement. - Bloomberg

According to BlackRock, this acquisition could add significantly to its long-term annual contract value ("ACV") growth target of low to mid-teens.

Meanwhile, the company's strategic partnerships, including with Envestnet and GeoWealth, improve its capabilities in wealth advisory and investment solutions.

This is what Envestnet wrote when it announced a deeper corporation with BlackRock and some of its peers:

Envestnet is planning on working with these firms, some of the largest asset managers in the world, to build investment strategies that are custom-tailored and can be used by advisors to help meet the specific financial goals, risk tolerance, and personal circumstances of individual investors; and deliver this at scale to the more than 109,000 advisors on its platform. - Envestnet

I believe this is a fantastic strategy, as BlackRock is using partnerships and bolt-on acquisitions to generate the most value from its existing platform and relationships.

BlackRock

Moreover, during the 2Q24 earnings call, CEO Larry Fink explained the impressive size of its expansion.

For example, the aforementioned acquisition of GIP is expected to double the company's private markets base fees and add roughly $100 billion of AUM focused on infrastructure.

As we discuss infrastructure a lot, most readers will know I like infrastructure, as it provides significant secular growth opportunities in data centers, the energy transition, supply chain modernization, and so much more.

In general, BlackRock has a great track record when it comes to acquiring growth and adding value. Here's a quote from Larry Fink I thought quite interesting. I added emphasis:

We set the standard for buy-side risk management technology by launching Aladdin on the desktops of investors over 20 years ago. We acquired BGI and iShares to redefine whole portfolio investing by blending both active and indexing to build better outcome-oriented portfolios.

iShares' AUM was about $300 billion when we announced our acquisition in 2009. Today, iShares is approaching $4 trillion of client money.

We recently celebrated the 5-year anniversary of the eFront acquisition where ACV has now more than doubled since becoming part of BlackRock.

We have never been shy about taking big, bold, strategic moves to transform ourselves, and most importantly, to transform our industry. Our successful business transformations are delivering our strong performance today and opening up meaningful new growth markets for our clients and for our shareholders. - BLK 2Q24 Earnings Call

This is reflected in its outlook and great news for shareholders.

A Lot Of Shareholder Value

When it comes to rewarding shareholders, BlackRock buys back stock and consistently hikes its dividend.

Over the past two years:

- The company has bought back 2% of its shares.

- BlackRock has hiked its dividend two times. It hiked by 2% in 1Q24 and 2.5% in 1Q23.

Currently, BLK yields 2.3% with a 50% payout ratio. Its five-year CAGR is 9.5%. As we can see below, the company's dividend growth has clearly come down in recent years, which makes sense, as uncertainty has risen due to the Fed's fight against inflation, slower global economic growth, and geopolitical issues that added another layer of unpredictability.

Data by YCharts

Data by YCharts

The good news is that BlackRock's future looks bright.

Using the FactSet data in the chart below, analysts expect 10% EPS growth this year, potentially followed by 13% and 15% growth in 2025 and 2026, respectively.

FAST Graphs

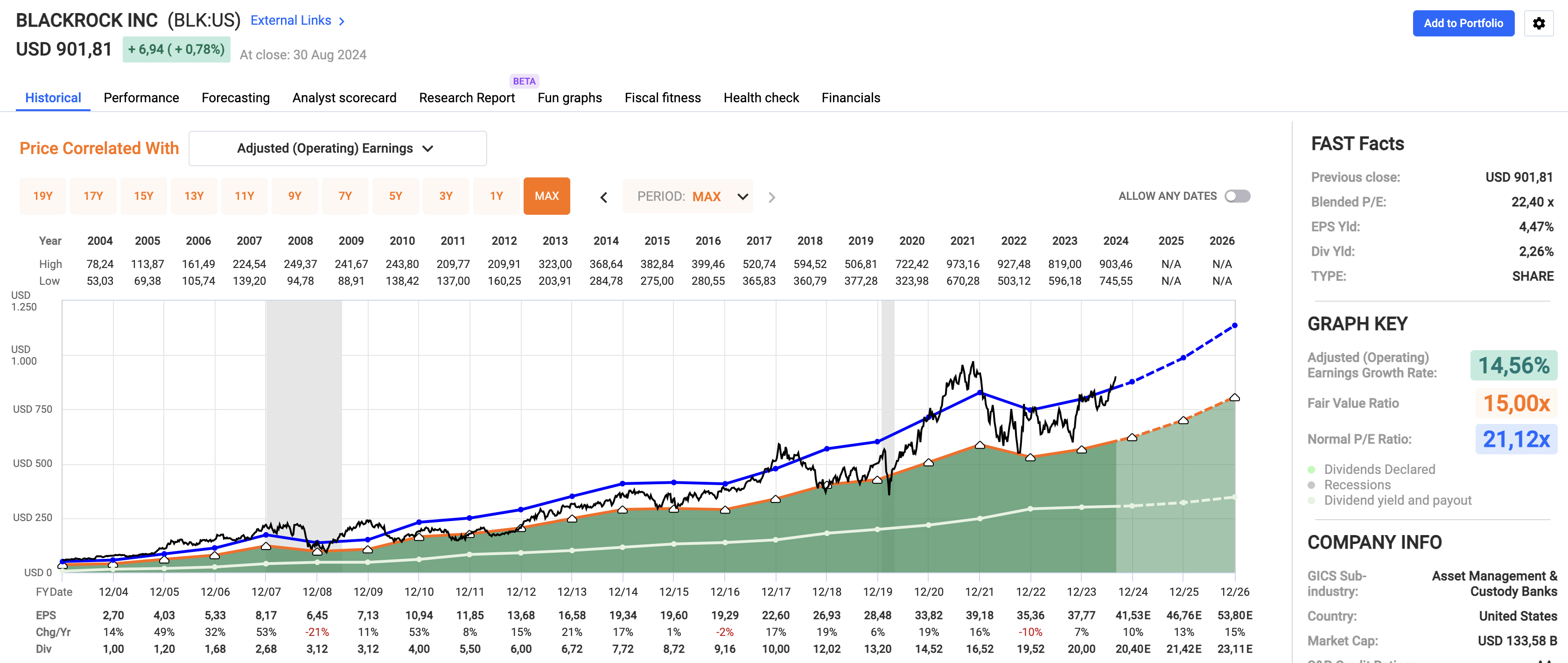

The company, which has returned 15.6% annually since 2004, has an average P/E ratio of 21.1x. I believe this multiple makes sense in the current environment.

This implies a fair stock price of $1,140, 26% above the current price.

It also enjoys an AA- credit rating, one of the safest ratings in the world.

Needless to say, I remain bullish on BLK, as I believe it is a fantastic growth stock in the financial space. The only reason why I don't own BLK is that I like to avoid asset managers. I prefer to do the work myself and pick my own investments.

All things considered, I expect BLK to beat the market for many more years to come.

Takeaway

Investing is a game where the big fish often gets bigger, thanks to the power of compounded interest.

As BlackRock continues to dominate the financial world with record-breaking assets and strategic growth, it's clear that this giant isn't slowing down.

Despite my reservations about the influence of these massive corporations, we have to recognize the impressive value BlackRock delivers to its shareholders.

With consistent dividend growth, smart acquisitions, and a bright outlook, BLK remains a fantastic player in the market.

While I prefer to manage my own investments, I expect BlackRock to keep outperforming for many years to come, making it a great investment for a wide variety of dividend investors.

Pros & Cons

Pros:

- Strong Growth Potential: BlackRock's diversified business model and move into high-growth areas like private markets and infrastructure are driving impressive revenue and asset growth.

- Consistent Shareholder Returns: With steady dividend hikes and share buybacks, BLK continues to reward its investors. I believe its track record of returning 15.6% annually since 2004 speaks for itself.

- Market Leadership: As one of the world's largest asset managers, BlackRock's scale and influence make it a dominant force in the financial sector, putting it in a great spot for long-term growth.

Cons:

- Political Sensitivity: BLK's proactive stance on sustainability and political issues may cause potential backlash.

- Valuation Risks: Despite its strong fundamentals, concerns over inflation and interest rates could lead to volatility.

- Market Dependency: In general, BLK's performance is closely tied to market conditions, making it prone to fluctuations and economic uncertainties.

Comments