Summary

- Dividend stocks have rebounded sharply recently.

- However, some high-quality high-yield stocks remain market laggards.

- We share some of our top picks of the moment.

z1b

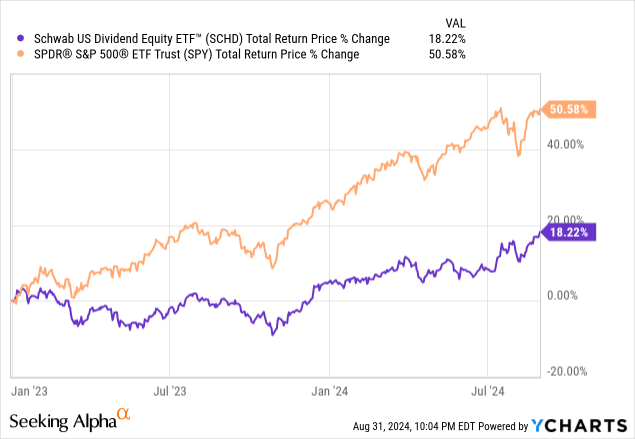

The dividend stock sector (SCHD) has made a strong comeback in recent weeks, after lagging the broader market ever since the beginning of 2023 as the AI boom, coupled with elevated interest rates, lifted mega-cap tech stocks while weighing heavily on interest rate-sensitive yield sectors such as REITs and utilities.

Data by YCharts

Data by YCharts

That being said, some high-yield stocks have largely failed to rally along with the broader dividend sector, including some high-quality ones that appear to be meaningfully undervalued at the moment. As a result, we are buying these stocks aggressively in our portfolio, and I will share two of them with you today.

Big Dividend Stock #1

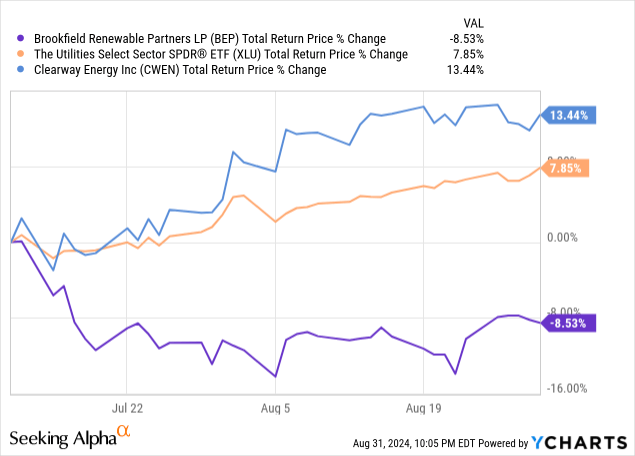

The first one is Brookfield Renewable Partners (BEP)(BEPC). As the chart below illustrates, BEP has not only underperformed the high-yield space and utility space recently (XLU), but it has also underperformed peers like Clearway Energy (CWEN)(CWEN.A). However, BEP’s weak performance in the market price does not reflect the underlying performance and quality of its portfolio.

Data by YCharts

Data by YCharts

First of all, BEP is arguably the strongest and best-diversified renewable power producer in the world, as it has a presence in all major power markets across 20 different countries. BEP has a significant presence in hydropower, wind power, utility-scale solar, distributed energy, battery storage, and nuclear reactor production through its stake in Westinghouse. It also has an extensive development pipeline, particularly in the utility-scale solar and battery storage space, as well as in onshore wind and hydropower. About 60% of its assets are in North America, with about 15% in Europe and the remainder in Asia and the Pacific region, including geographies like China, India, and Australia.

The company also has an exceptional track record, generating a 12% FFO per unit CAGR since 2016 and growing its distribution at a 6% CAGR for the past two decades plus. Moreover, BEP's balance sheet and business model are set up to be quite defensive and to weather all sorts of macro environments, including higher inflation and interest rate environments, as well as falling inflation and interest rate environments. Seventy percent of its revenues are indexed to inflation, which means that even if interest rates and inflation rates remain higher for longer, its organic growth would likely increase to help offset increases in its interest expense. This is especially true because 95% of its debt is at fixed rates, and its average term to maturity on its corporate borrowings is 12 years and on its asset level debt, it is 11 years. This means that BEP will only have a small portion of its debt maturing each year, while 70% of its revenue will see organic growth accelerate due to higher inflation. This suggests that BEP should not suffer much at all in a higher-for-longer environment.

However, if interest rates were to fall, it would also boost BEP because the net present value of its cash flows would likely go up since 90% of its cash flows are contracted for an average of 13 years. It would also likely reduce its cost of capital, enabling it to invest more aggressively in growth. On top of that, BEP has a BBB+ credit rating, which means it should have access to attractively priced debt relative to many of its peers. Since most of its peers are junk-rated, this should enable BEP to invest on a more accretive basis and also make acquisitions more accretive, as it can refinance the debt in assets that it acquires, in many cases at meaningfully lower interest rates, thereby unlocking additional cash flows from acquisitions. BEP also has $4.4 billion of available liquidity that it can invest in growth opportunities on a strategic basis, including even potentially purchasing its units, as it has been known to do in the past.

Last but not least, between its huge development pipeline and very low risk of headwinds from rising interest rate expense, given that BEP has hardly any debt maturing before 2029 or later, as well as its inflation escalators and other contractual revenue increases, its margin-enhanced programs, which are designed to cut costs and increase cash flows on re-contracting, as well as its robust capital recycling program, BEP sees a clear path to generating 10% or higher FFO per unit growth per year for the foreseeable future. Combined with its 6% current yield, BEP appears poised to deliver very attractive risk-adjusted returns, especially because its long-term contracted assets should give it considerable cash flow stability even in an economic downturn. On top of that, BEP's recent 10.5 gigawatt deal with Microsoft to provide renewable energy to power its AI investments gives it another very exciting growth opportunity, and it could also lead to additional deals with other tech giants in the future.

Big Dividend Stock #2

Another attractive dividend stock right now is Nutrien (NTR). NTR is a leading agriculture business that produces fertilizers, nutrients such as potash, nitrogen, and phosphate, and it also operates a retail segment that delivers more stable cash flows through its distribution and sale of crop nutrients, crop protection products, seeds, and merchandise products. NTR is currently investing in enhancing the profitability and efficiency of its retail business, as well as the efficiency of its potash mine operations through increased automation. NTR is also investing in brownfield nitrogen expansion and reliability projects that should increase its nitrogen production. While this space faces some headwinds from pricing, NTR still expects its business to deliver solid performance this year, with retail EBITDA likely coming in meaningfully higher year-over-year from 2023, while capital expenditures should be coming down by between $400 million and $500 million year-over-year, which should help unlock additional cash for shareholder returns in the second half of the year.

NTR also thinks that supply and demand are finally coming into balance, which should support the pricing of the crop nutrients that it produces. Management also emphasized that in the second half of 2024 and as the company moves into 2025, depending on their cash flow generation, they are certainly interested in buying back stock alongside potential opportunistic retail opportunities in North America and Australia.

NTR looks attractive from a valuation perspective, as it currently trades at a discount to its historic value on an EV to EBIT basis, with it currently standing at 6.79 times compared to 7.66 times for its historical average. Despite facing some industry weakness recently, NTR’s dividend yield of ~4.5% is very attractive compared to its historical average of 3.4%, while its levered free cash flow yield of 15.4% is also quite high compared to its historical average of about 10%.

Combining the potential for strong buybacks with NTR's history of growing its dividend at a solid clip over time and expecting to continue doing so moving forward, NTR is a nice portfolio diversifier, as well as a relatively cheap way to gain access to the agricultural space, while benefiting from a diversified business model that also has an investment-grade balance sheet.

Investor Takeaway

With stocks like BEP and NTR, investors can get yields that range between 4.5% and 6% at the moment, along with inflation-beating expected dividend per share growth in the foreseeable future backed by strong balance sheets, well-diversified quality business models, and attractive long-term per share growth and intrinsic value growth potential. By building a diversified portfolio of stocks like these, investors can have well-diversified portfolios that have significant upside potential along with attractive current income, which puts those sorts of portfolios at an advantage of outperforming over the long term, especially if combined with an opportunistic capital recycling program that I like to implement.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments