Summary

- I remain bullish on Extra Space Storage due to its strong operational performance, strategic growth through mergers, and consistent dividend payouts, despite industry challenges.

- EXR's valuation appears fair after a recent rally, so I'm cautious about deploying significant capital at current levels without a meaningful pullback.

- The Life Storage merger and expansion of third-party managed properties enhance EXR's market position and revenue streams, supporting long-term growth.

- Current market conditions, including weak consumer sentiment and rising costs, pose risks, but a market correction would be a prime opportunity to increase my position.

SeventyFour/iStock via Getty Images

Introduction

I doubt I'm breaking any news when I say I really like self-storage.

Although one could make the case that it doesn't make sense from a diversification point of view, the two REITs in my 22-stock dividend growth portfolio are both self-storage REITs.

Initially, I bought Public Storage (PSA). I then added Extra Space Storage (NYSE:EXR), which has been a REIT I have admired for many years, before finally getting serious about dividend (growth) investing.

While I like a wide range of REITs, including warehouses, cell towers, manufacturing housing communities, and others, I never sold any of my REIT investments to diversify.

I'm glad I didn't, as the self-storage sector has come back roaring. After a challenging stock price downtrend since the end of 2021 due to rising interest rates and weakening consumer sentiment, Public Storage and Extra Space Storage have returned 25% and 31% over the past six months, respectively.

Data by YCharts

Data by YCharts

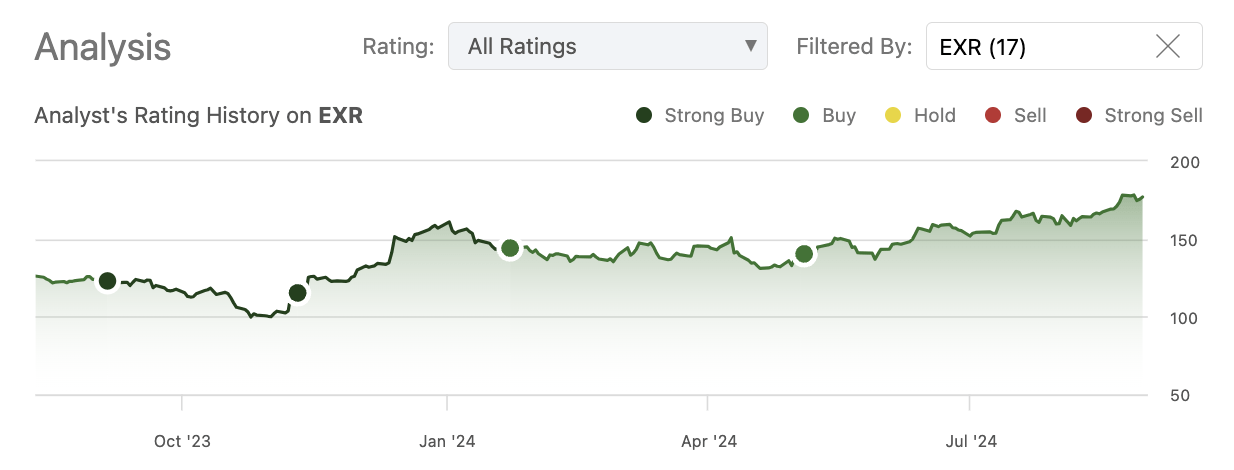

With that said, in this article, I'll update my Extra Space Storage thesis. As we can see below, since becoming bullish in 2023, my calls are profitable. This includes two Strong Buy ratings in September and November 2023 and two Buy ratings in January and May of this year.

Seeking Alpha

My most recent article was written on May 4. Since then, shares have returned 25%, beating the market's 10% return by a satisfying margin.

Now, I'll share my thoughts on the company, using its latest earnings, new self-storage developments, and other relevant developments that impact this real estate dividend grower.

So, let's get to it!

Trouble & Light At The End Of The Tunnel

I always talk about buying companies with competitive moats in industries with high barriers to entry. Yet, I have bought two self-storage REITs in an industry with extremely low entry barriers.

As I have written in prior articles, this is based on a number of reasons. This is what I wrote in my prior article on EXR:

- Low Building and Operating Costs: Self-storage facilities are relatively cheap to build and maintain.

- Flexible Pricing: Due to the month-to-month lease structure, self-storage REITs can adjust rental rates more frequently. They are not tied to very long lease agreements with slow rent escalators.

- High Demand: The need for storage space remains high due to various factors that include relocation, downsizing, and consumers buying too much stuff they don't need. Despite the assumption that younger generations are less materialistic, self-storage demand has steadily grown.

- Automation and Technology: Many operators are adopting automation technology, which can significantly reduce the need for onsite personnel and increase net operating income. In other words, operators who figure out how to efficiently offer a good tenant experience are in a great spot to exploit a highly fragmented market.

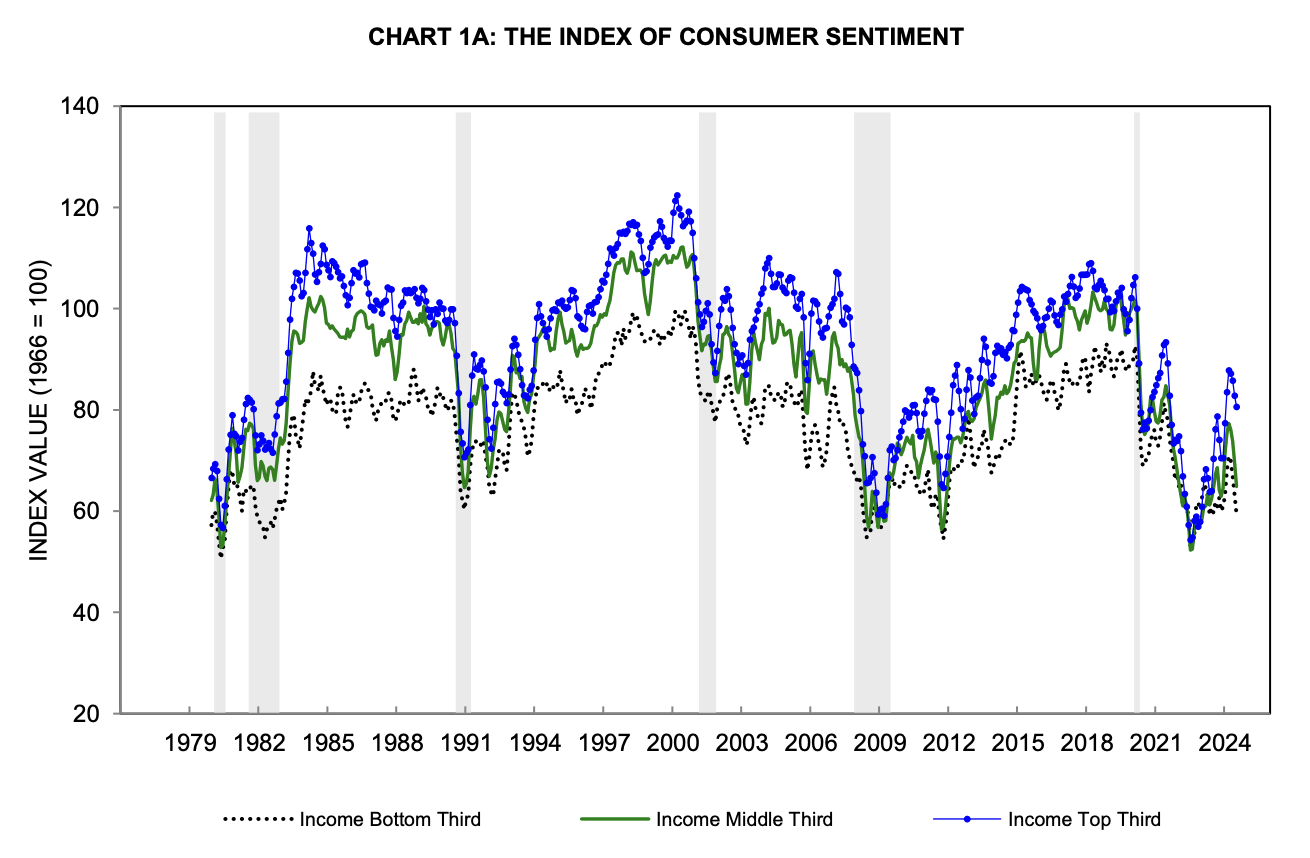

Despite these benefits, self-storage is cyclical. Generally speaking, two factors are beneficial for self-storage operators, which are a strong housing market and healthy consumer sentiment. Whenever people move and buy stuff they don't need, self-storage investors win.

Right now, this is not the case.

This is what consumer sentiment looks like:

University of Michigan

This is what pending home sales look like:

Data by YCharts

Data by YCharts

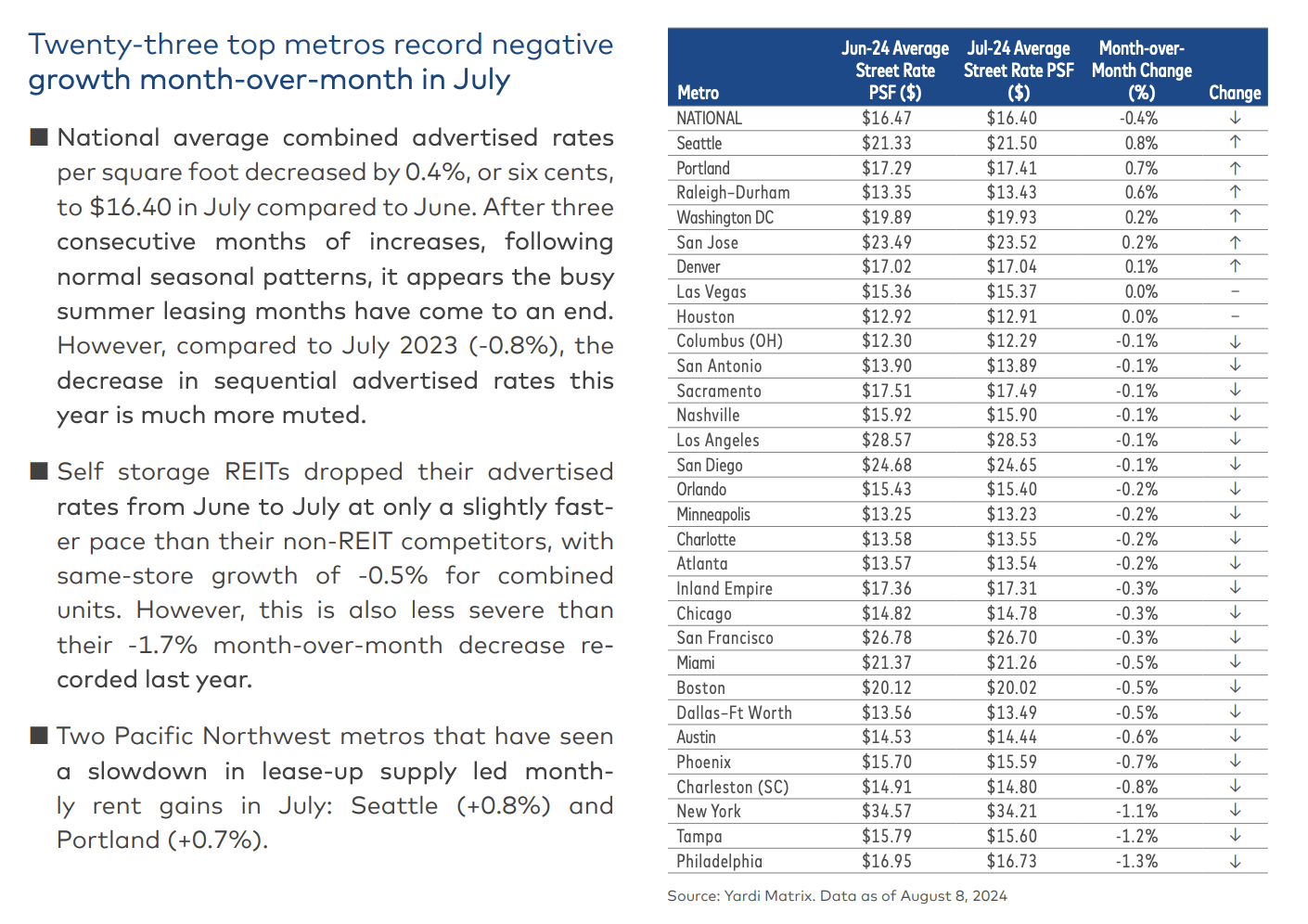

As a result, the August self-storage report from Yardi was not to write home about.

According to the report, in the second quarter, growth in the industry slowed, with average same-store revenue growth of negative 0.2%. This is the first decline since 3Q20.

The report explained that this is due to lower occupancy and lower rates, the two biggest drivers of revenues in the industry. Interestingly enough, markets like New York and Denver saw improvements, while Sunbelt markets suffered from new supply growth, the biggest drawdown that comes with their popularity.

Yardi Matrix

The good news is that elevated rates have pressured new supply growth. According to the report, the national self-storage pipeline contains 64.6 million net rentable square feet. That's 3.5% of the total existing stock. On a full-year basis, that number is expected to fall to 3.2%, potentially followed by a decline to 2.6% in 2025.

Despite these somewhat poor numbers, the EXR stock price has been doing well. Including dividends, EXR has returned 379% over the past ten years. It has outperformed the market by a wide margin and erased most of the post-2021 downtrend.

Data by YCharts

Data by YCharts

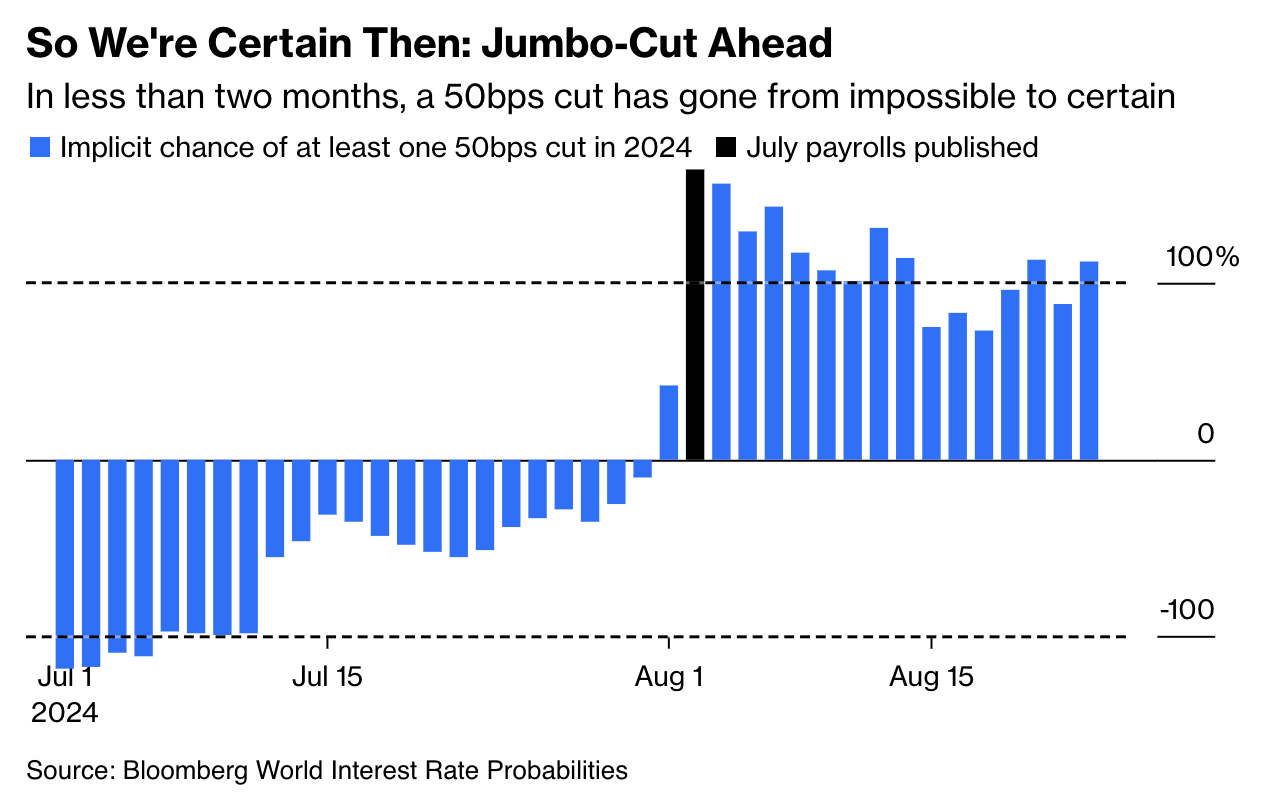

The market is not impressed by poor self-storage fundamentals, as it expects lower rates to fuel higher demand in the housing market and in the consumer space. That's why investors are frontrunning the good news by buying self-storage and many other financial assets.

As we can see below, this year, the market expects at least two 25 basis points cuts (or one 50 basis points cut).

Bloomberg

If the Fed achieves a soft landing, where it can bring inflation to 2% without causing a recession, self-storage REITs are a fantastic place to be.

What To Make Of Extra Space Storage?

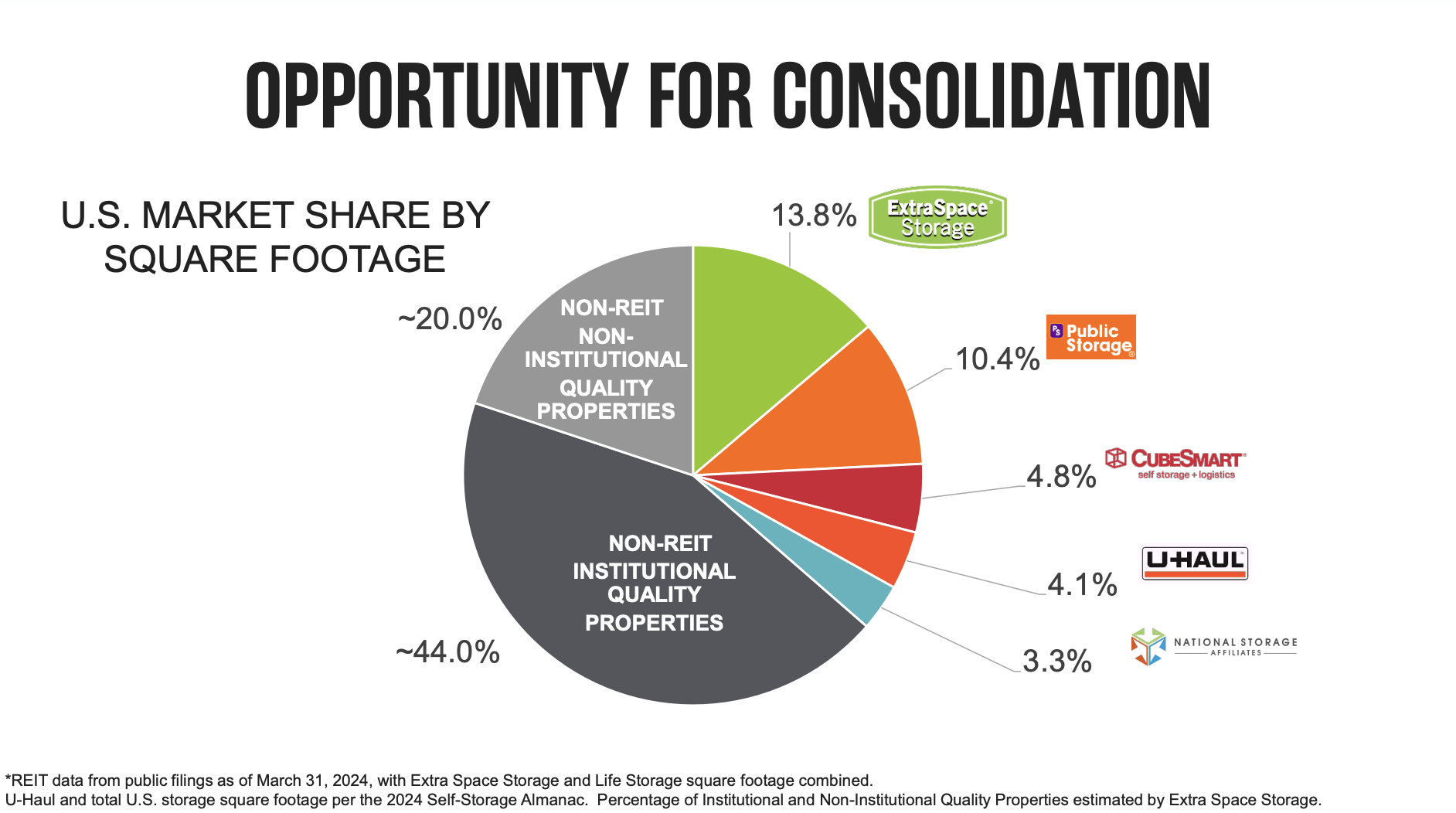

Founded in 1977, the company has become the biggest operator in its industry. This includes the 2023 merger with Life Storage, which allowed the company to take the crown away from Public Storage, which has been the industry leader for a very long time.

Extra Space Storage

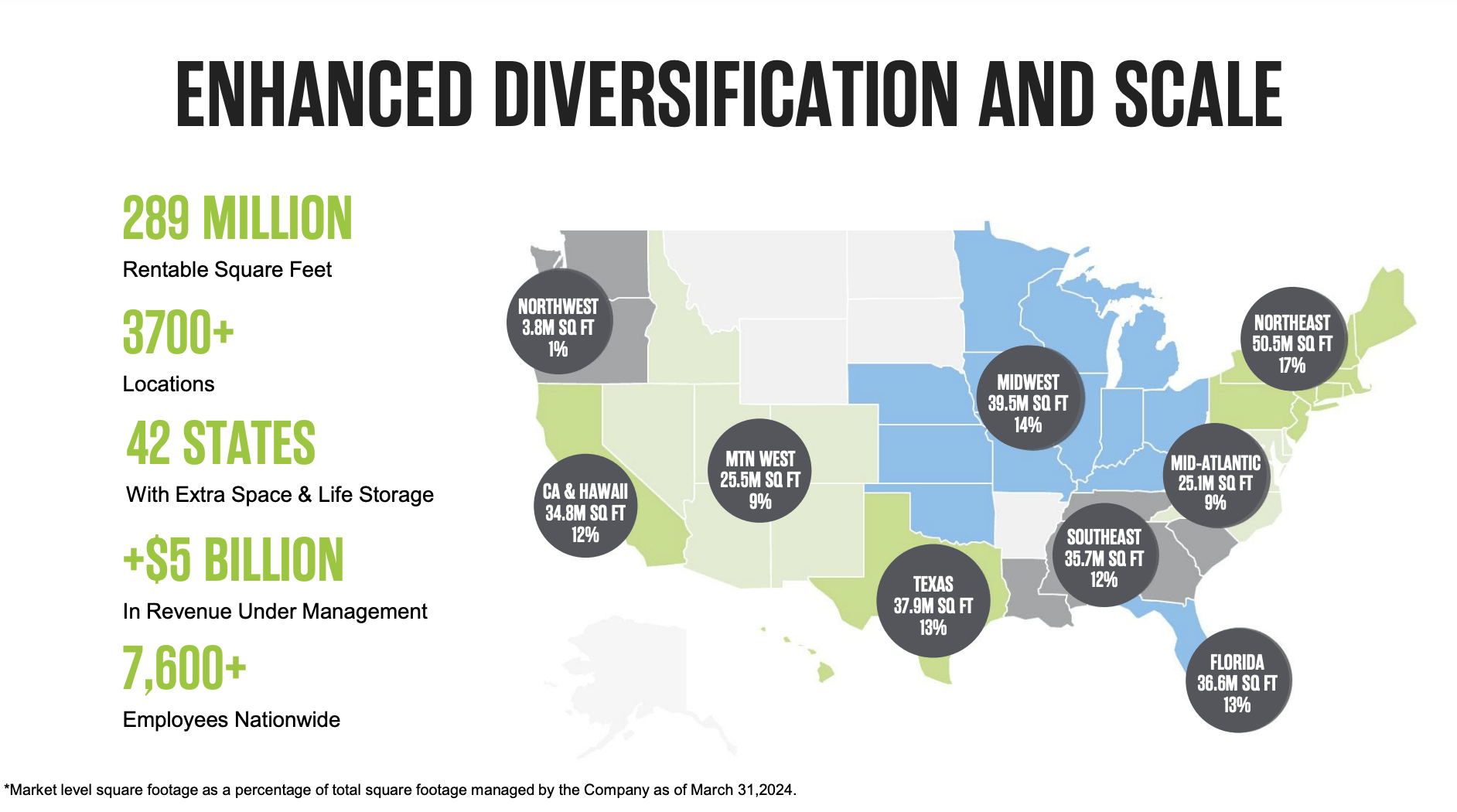

Moreover, the S&P 500 member operates in 42 states, where it owns close to 3,800 properties with 2.6 million storage units.

No market accounts for more than 14% of its total exposure.

Extra Space Storage

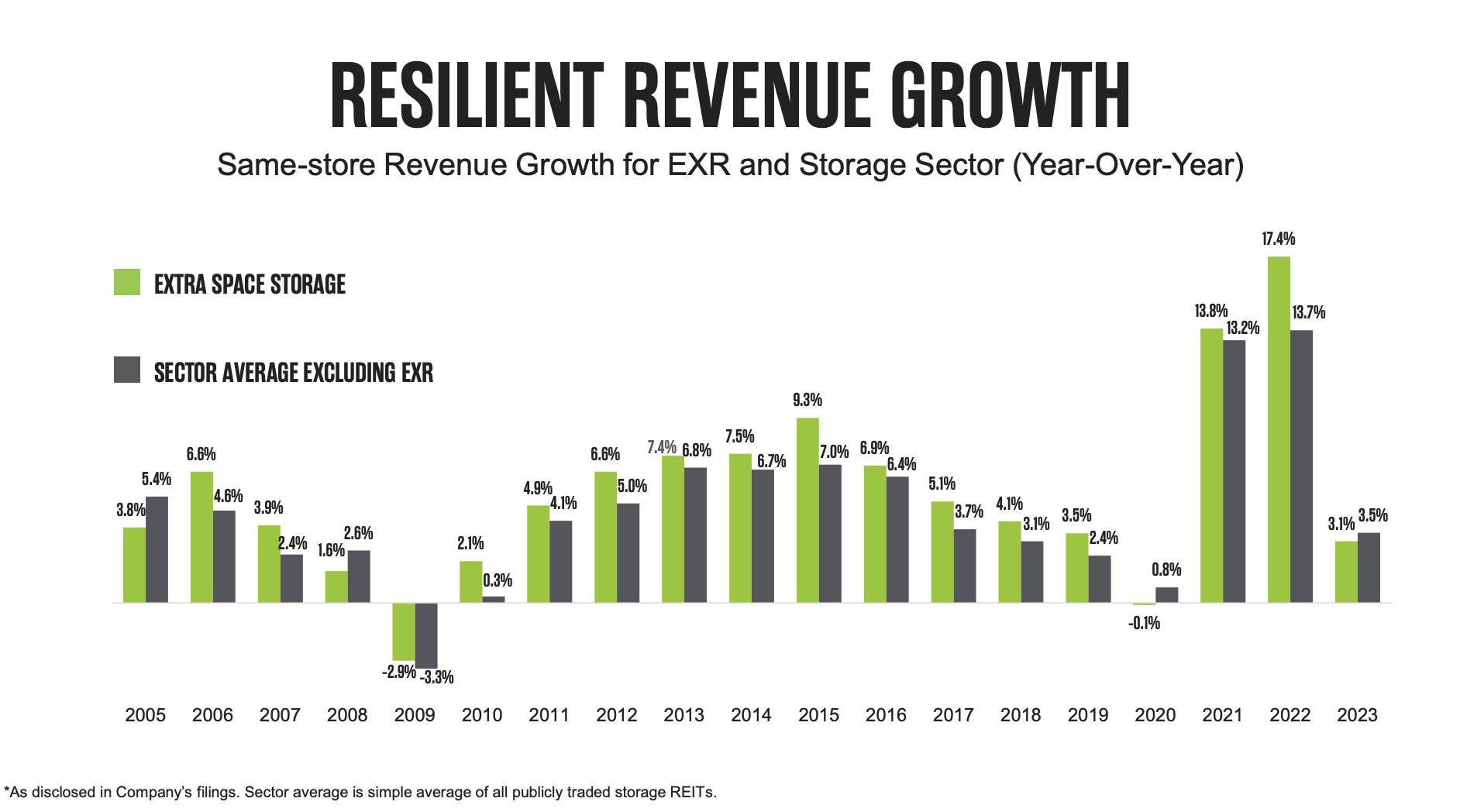

What's fascinating is that EXR isn't just the largest self-storage REIT but also one of the most successful, as it has consistently outperformed its peers on a same-store revenue growth basis. Since 2005, the company has underperformed its industry just four times.

Extra Space Storage

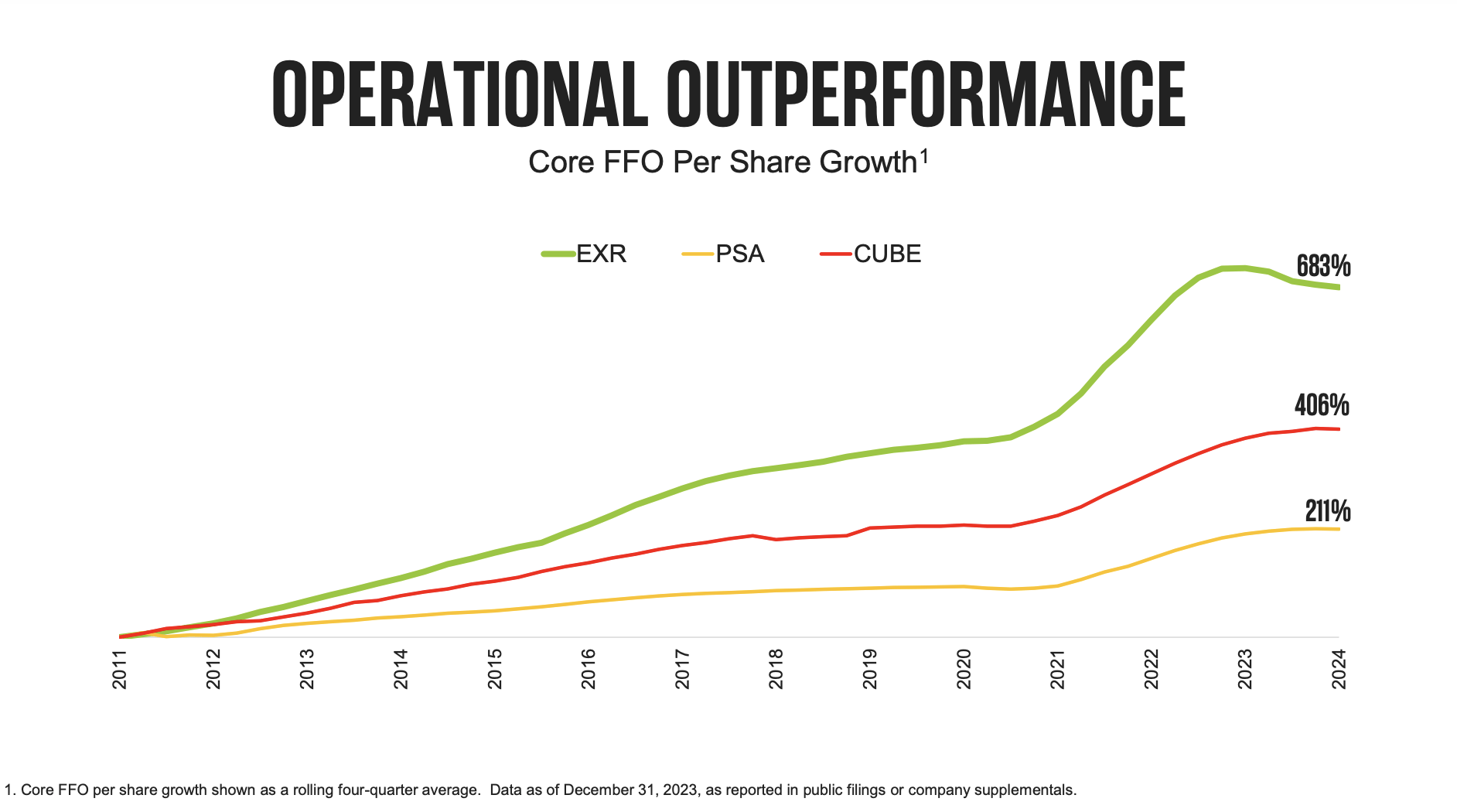

As a result of this consistency, the company has grown its core funds from operations ("FFO") by 683% since 2011, a mile above the performance of its two biggest peers.

Extra Space Storage

With that said, and in light of industry challenges, in the second quarter, the company said its performance was better than expected, thanks to its strong operational execution.

For example, the same-store occupancy rate improved to 94.3%. This reflects a 110 basis point gain from the previous quarter and a 30 basis point year-over-year increase. Meanwhile, the average move-in rate improved by 12%. However, it's still 8% below last year's average moving rate.

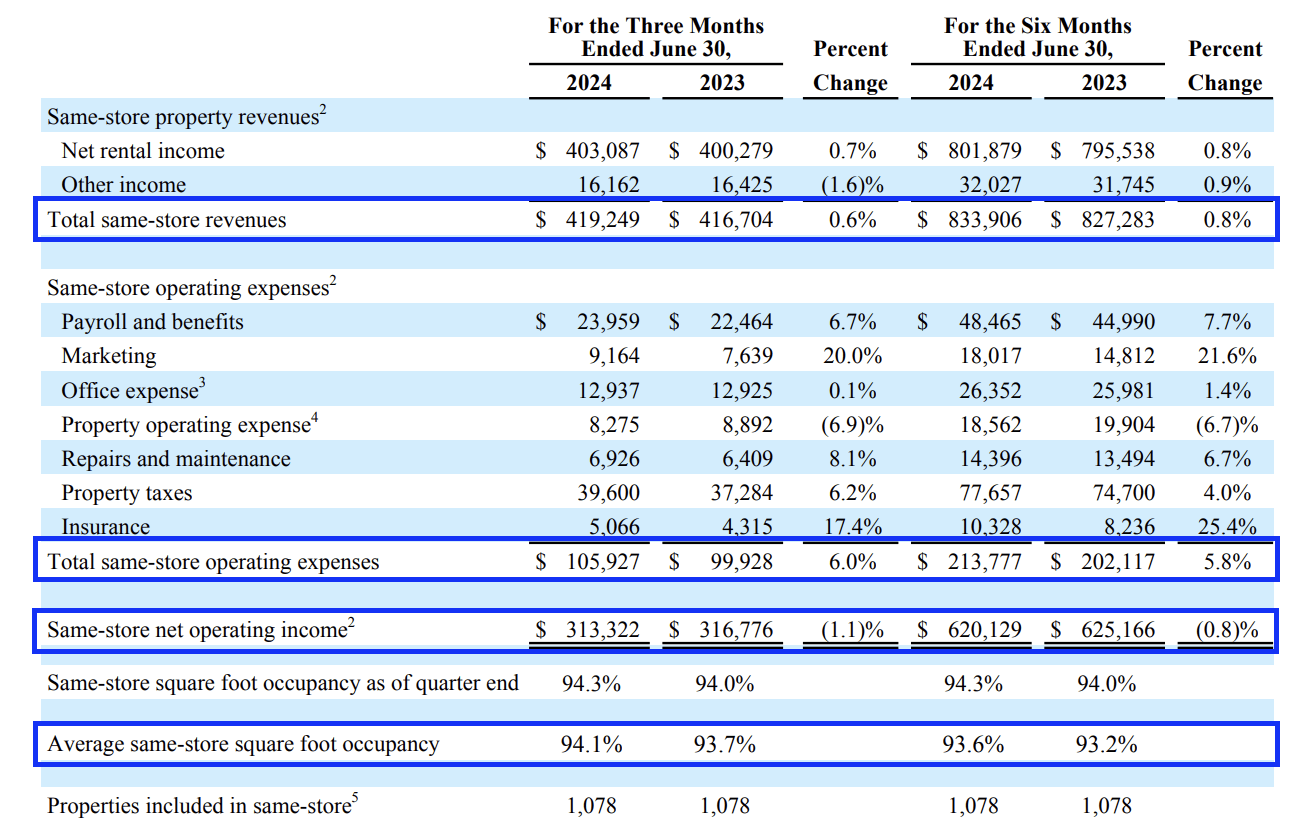

Nonetheless, thanks to these numbers, the company's same-store revenue increased by 0.6% (see the table below).

Extra Space Storage

Unfortunately, despite a focus on costs, total same-store expenses were 6.0% higher, causing same-store net operating income ("NOI") to drop by 1.1%.

The good news is that this was expected, as the cost challenges in the industry have been a topic of discussion for a while.

What matters more is the integration of Life Storage properties. In the second quarter, the Life Storage same-store pool saw an occupancy increase of 400 basis points to 93.8%. This caused 1.8% same-store revenue growth - despite pricing challenges.

The company is also more careful when it comes to using move-in discounts, as it strives for revenue maximization.

Moreover, the company, which enjoys a BBB+ credit rating (one step below the A range), is expanding its third-party managed portfolio. Managing properties owned by others generates fees with very limited capital spending.

In 2Q24, EXR added 77 third-party managed stores and a total of 86 net stores on a year-to-date basis.

Dividends & Shareholder Value

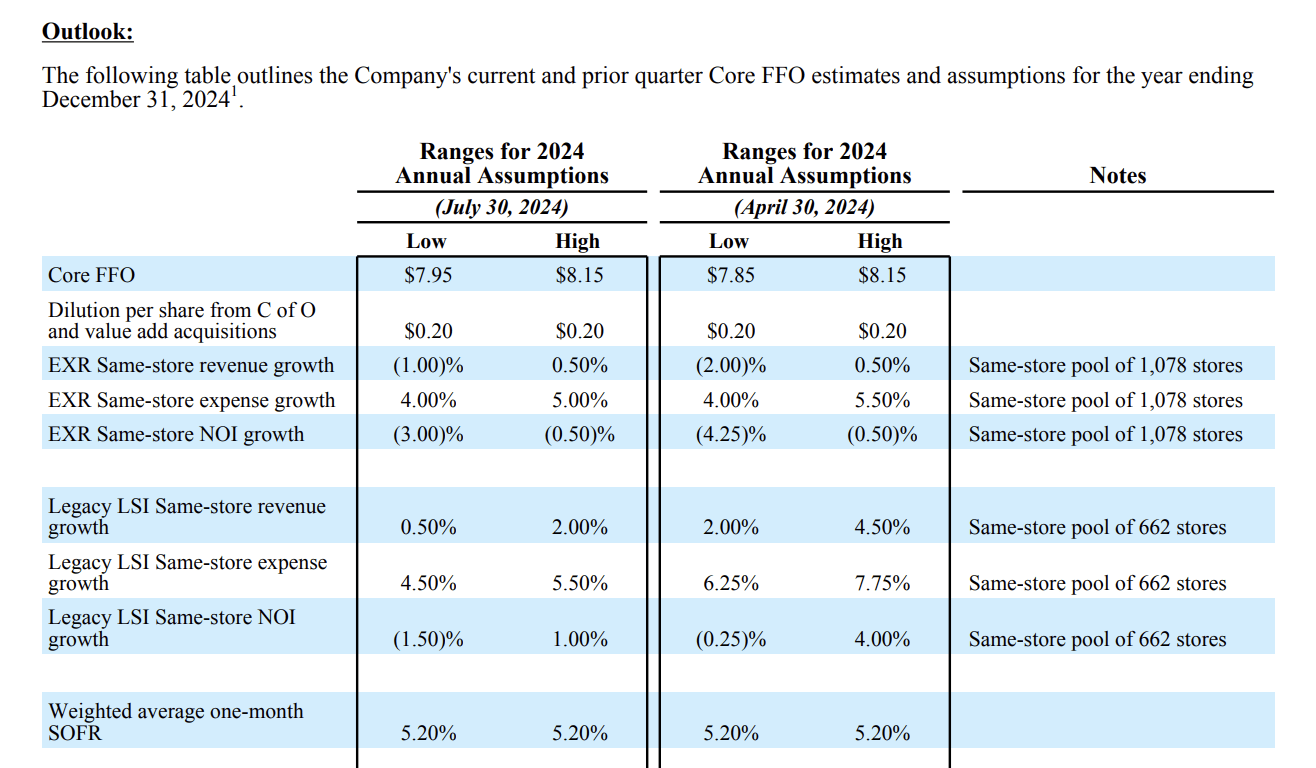

Looking forward, the company has increased the lower bound of its Core FFO guidance range and sees better-than-expected same-store revenue growth. It also hiked the lower bound of its same-store NOI growth range to negative 3.0%.

Extra Space Storage

While 2024 is a very tough year, the dividend is still in a good place.

Currently yielding 3.7%, EXR's dividend has an 86% 2024E adjusted FFO payout ratio. The five-year CAGR is 13.2%. Last year, the dividend was broken up because of the Life Storage merger.

Data by YCharts

Data by YCharts

Moreover, although its 3.7% yield isn't overly exciting, it's close to the longer-term median.

When we were buying EXR at more than 5% last year, it was truly an outlier year for the industry, meaning I do not expect another opportunity like that anytime soon.

With regard to its valuation, EXR trades at a blended P/AFFO ratio of 23.4x, roughly three points above its long-term average and 1.1 points above its ten-year average.

FAST Graphs

Analysts expect a 2% per-share AFFO contraction in 2024 to be followed by 6% and 5% growth in 2025 and 2026, respectively.

Although I believe EXR has a fair stock price of roughly $190 roughly 7% above its current price, I would not be an aggressive buyer. While gradual buying may be a smart move, I would only deploy larger sums of cash (that's relative and for everyone different) on a 10% correction.

Currently, the markets are very upbeat about potential Fed rate cuts. There's not a lot of room for error. If the Fed or a different factor causes EXR shares to suffer, I'll add to my position, as I believe the stock has what it takes to outperform the market for many more years to come.

Takeaway

I remain bullish on Extra Space Storage, despite the current challenges in the self-storage industry. The company's strong operational performance, strategic growth through the Life Storage merger, and consistent dividend payouts make it a solid long-term investment.

However, because the stock's recent rally suggests a fair valuation, I'm cautious about deploying significant capital at current levels.

However, should a market correction present itself, I would view it as a great opportunity to increase my position.

Essentially, EXR has proven its resilience and potential for continued outperformance, making it a core holding in my dividend growth portfolio.

Pros & Cons

Cons:

- Industry Leadership: Extra Space Storage is the largest self-storage operator, consistently outperforming peers in revenue growth and other operational metrics.

- Resilient Dividend: With a 3.7% yield and a strong dividend growth history, EXR offers reliable income.

- Strategic Expansion: The Life Storage merger and expansion of third-party managed properties improves its market position and revenue streams.

- Operational Efficiency: High occupancy rates and effective cost management provide much-needed support in a rather tough operating environment.

Pros:

- Valuation Concerns: The stock trades at a premium, making it less attractive for aggressive buying without a meaningful pullback.

- Cyclical Headwinds: Current market conditions, including weak consumer sentiment and a soft housing market, pose risks to the REIT's near-term performance.

- Rising Costs: Industry-wide cost pressures are pressuring its financials, while economic uncertainty adds another layer of risk.

Comments