Summary

- ENB and PAA/PAGP are leading midstream businesses with attractive yields and strong balance sheets.

- ENB has a better long-term track record than PAA/PAGP, but PAA/PAGP has outperformed ENB recently.

- We compare them side-by-side and explain why we think only one of these is a Buy right now.

Henrik Sorensen

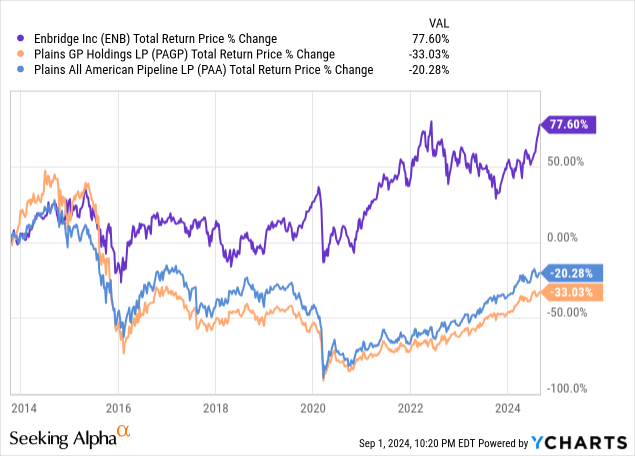

Plains All American Pipeline (NASDAQ:PAA)(NASDAQ:PAGP) and Enbridge (ENB) are two popular midstream dividend growth stocks. While Enbridge has a much more impressive long-term track record.

Data by YCharts

Data by YCharts

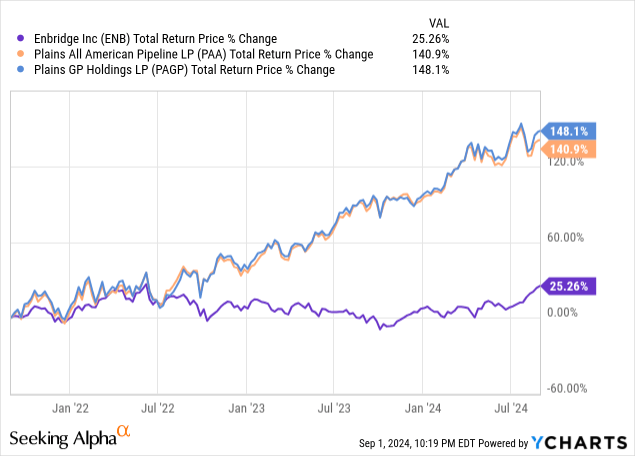

Plains has significantly outperformed ENB in recent years.

Data by YCharts

Data by YCharts

In this article, we will compare them side by side and share our view on why only one is a buy right now.

ENB Vs. PAA/PAGP: Qualitative Comparison

When it comes to balance sheet strength, both are in a strong position, but I would give the edge to ENB due to the fact that it has a slightly higher credit rating. Plains has made a lot of progress in recent years towards deleveraging its balance sheet as it has paid down debt aggressively. As a result, it has successfully brought its leverage ratio down to 3.1 times, which is below its long-term target of 3.25 to 3.75 times. Additionally, it has $3.2 billion worth of committed liquidity, which is significant for a company with an enterprise value of under $26 billion and a market cap of just over $12.5 billion. The company is also generating significant free cash flow, which positions it well to handle any potential challenges that may arise in the near term. This has earned it a credit rating upgrade to BBB from S&P and put it on very solid financial footing.

In contrast, ENB has a BBB+ credit rating from S&P, which is slightly above Plains'. However, its debt-to-EBITDA ratio is 4.7 times, which is significantly higher than Plains'. That said, it is still well within its target range of 4.5 to 5 times. This discrepancy is because ENB's underlying cash flows are almost entirely underpinned by contracted or regulated assets (98% of its cash flows either at cost of service or contracted, over 95% of ENB's customers are investment-grade, 80% of its EBITDA has inflation protections, and only 5% of its debt portfolio is exposed to floating rates).

This compares favorably with Plains, which does not have any regulated assets and relies on either commodity-sensitive or contracted assets to generate its cash flows. As a result, ENB—especially given its recent acquisitions of natural gas utilities—is in many ways a hybrid between a regular utility and a traditional midstream company, whereas Plains is more of a traditional midstream company, and therefore its cash flow stream is considered to be a bit lower quality and less secure.

ENB Vs. PAA/PAGP: Quantitative Comparison

That said, while ENB's cash flows are a bit more defensive, which effectively cancels out its higher leverage and then some, Plains' business is positioned to grow at a brisker pace moving forward, particularly in terms of its dividend. Both companies are likely to grow their distributable cash flow per share at a low to mid-single-digit pace moving forward. However, ENB is at a point where its dividend is likely going to only be in line with its distributable cash flow per share, which puts it at a 3% to at most 5% annualized rate. In contrast, Plains' payout ratio is significantly lower than ENB's. In 2023, it came in at a mere 45.5%, whereas ENB's payout ratio in 2023 was about 65%.

As a result, currently, Plains is positioned to grow its dividend at a much faster rate than its distributable cash flow per share growth rate for the foreseeable future through 2028. Analysts expect the company to grow its dividend per share at a 9.2% CAGR through 2028, in contrast to ENB, which is expected to grow its dividend at just a 3.1% CAGR over that period of time. This makes Plains a much more dynamic and exciting dividend grower than ENB. In fact, when combined with its more attractive forward dividend yield of 7.7% compared to ENB’s 6.8%, its total return profile is much more attractive as well.

Investor Takeaway

Given this comparison, for investors who are willing to take on a bit more risk in pursuit of meaningfully higher returns, Plains is a much more compelling opportunity than ENB. In contrast, ENB is more of a slow and steady, dependable utility-like dividend stock that will likely grow at a rate that meets or slightly beats inflation for years to come. As a result, we rate Plains as medium risk but give it a buy rating, whereas ENB is low risk, but we give it a hold rating at the moment as ENB's expected 3% annualized growth rate combined with its 6.8% dividend yield results in about a 10% annualized total return, which is roughly in line with long-term expected market returns, making us neutral on the stock.

That said, for retirees, I think there is certainly a place for ENB in their portfolio at the current price, but I would not expect meaningful, if any, alpha over the long term, whereas Plains is an interesting opportunity for either a more aggressive retiree investment or for a total returns-focused investor looking to generate market-beating returns. Note that PAA issues a K-1 whereas PAGP issues a 1099 tax form. ENB issues a 1099 tax form, but is a Canadian C-Corp and its dividends are declared in CAD, so keep these items in mind when making investment decisions.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments